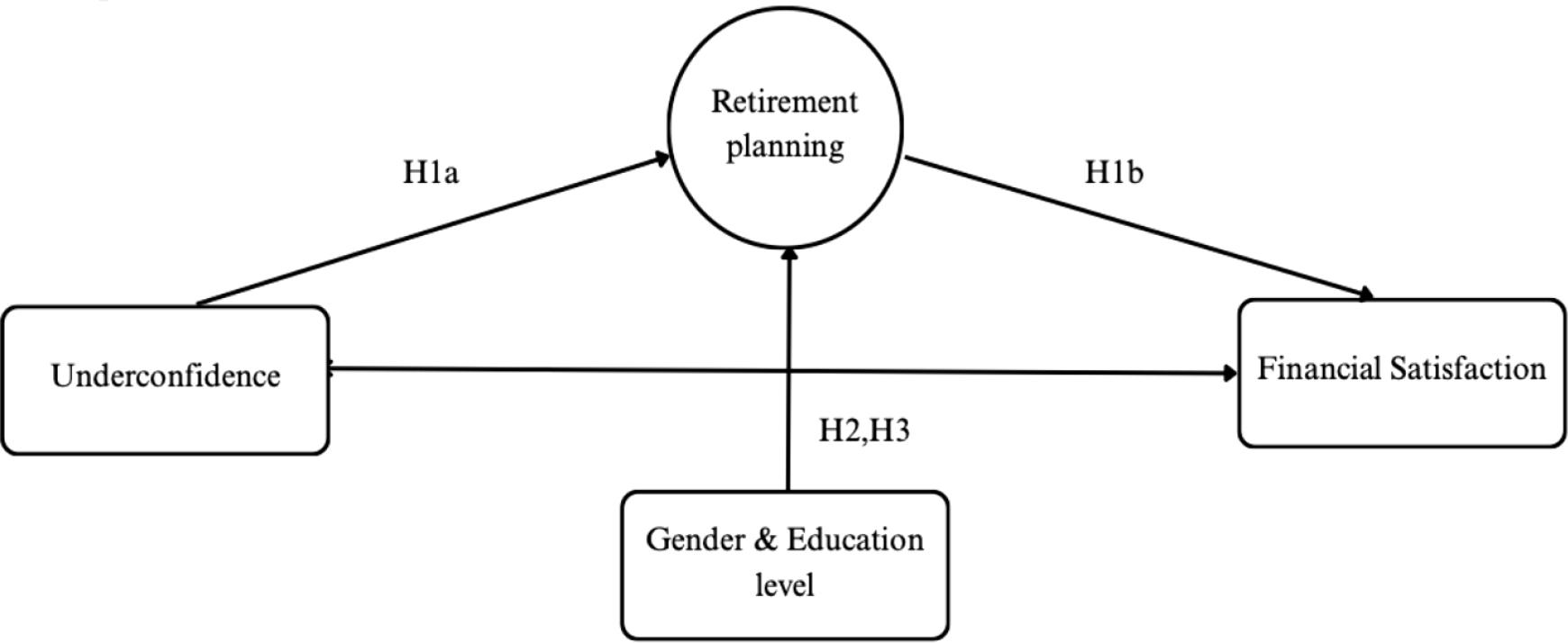

Figure 1.

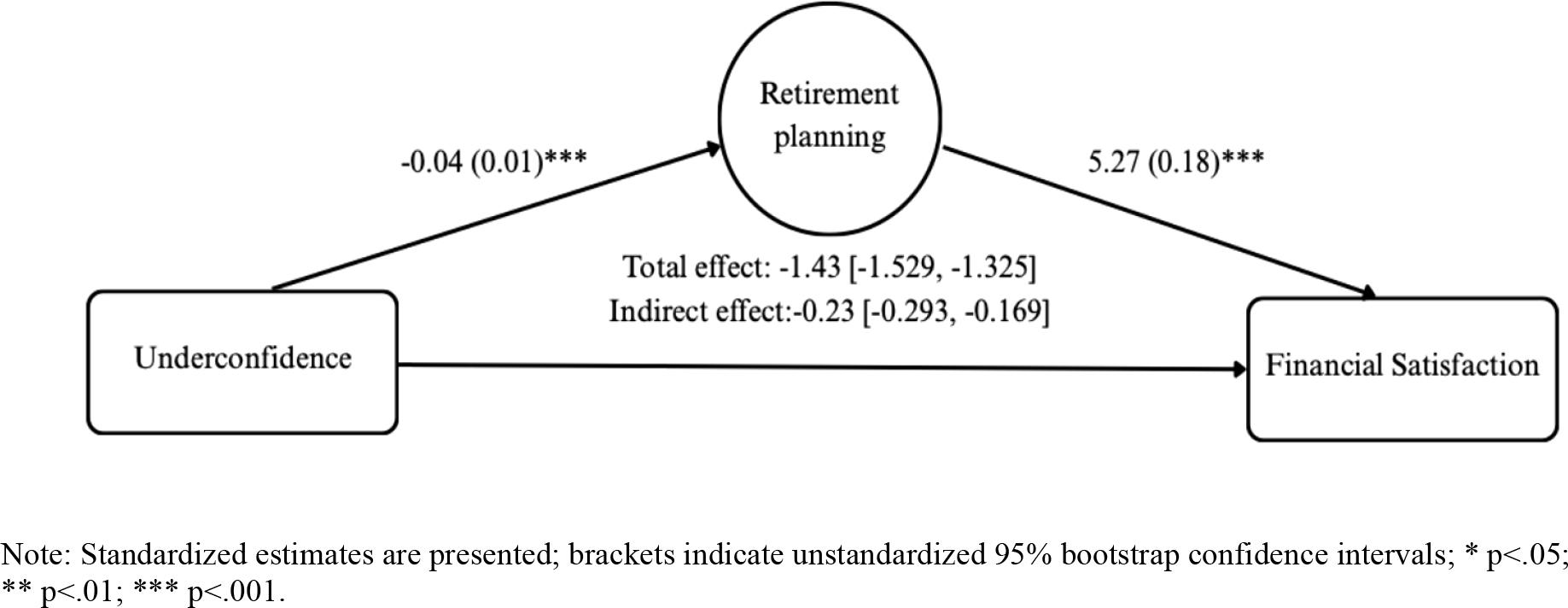

Figure 2.

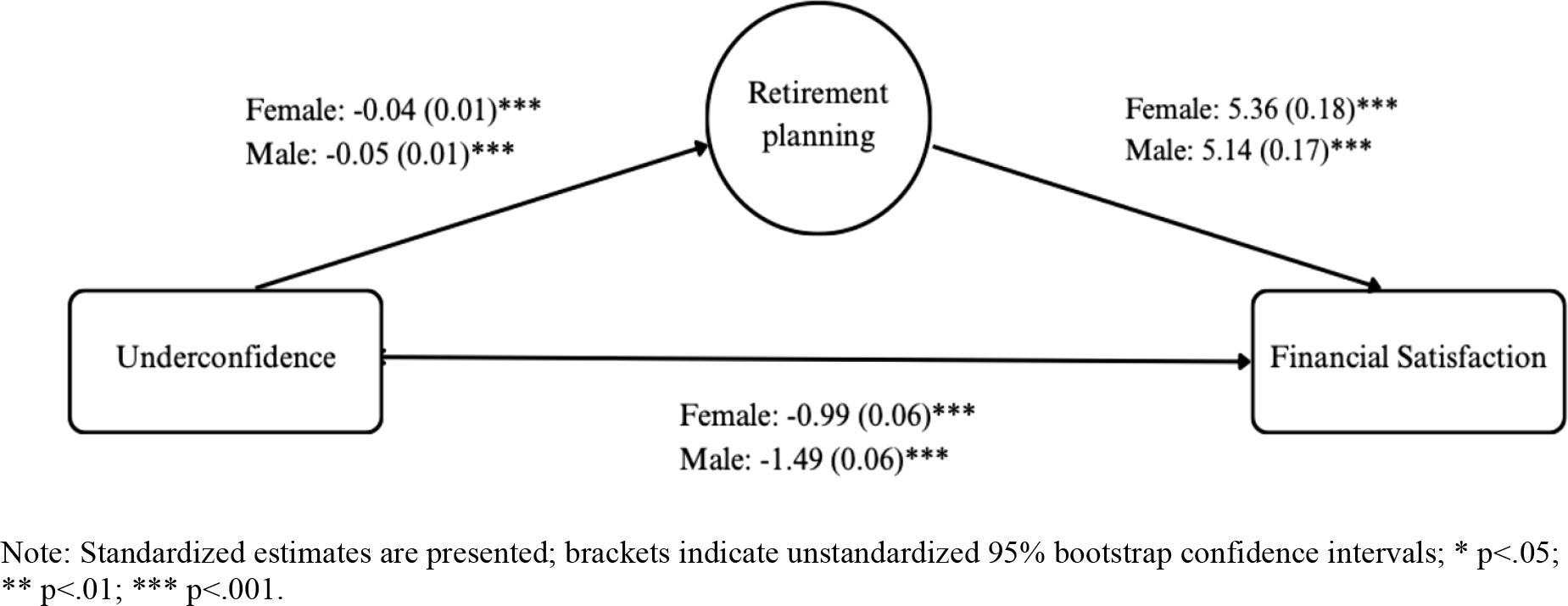

Figure 3.

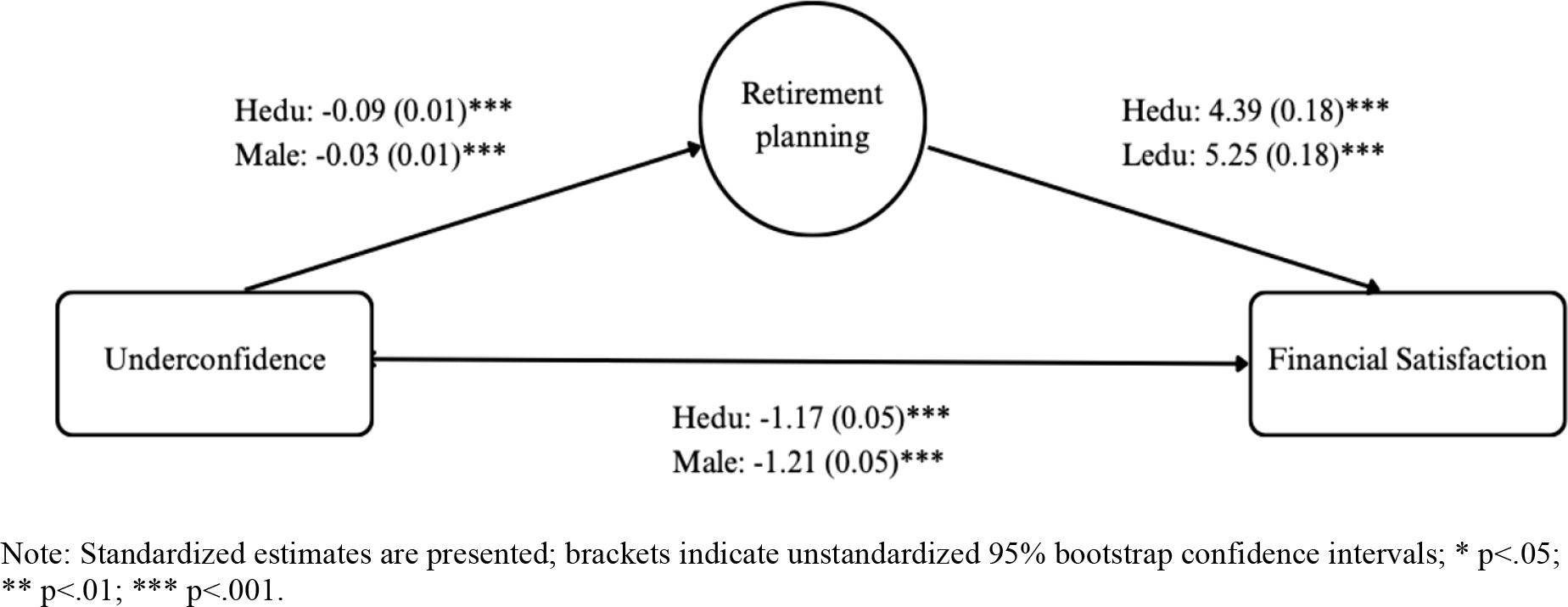

Figure 4.

Comparison between constrained and free model by gender

| χ2 | df | Δχ2 | Δdf | P | CFI | RMSE A | |

|---|---|---|---|---|---|---|---|

| Constrained model | 1733.5 | 50 | .933 | .058 | |||

| Free model | 1542.2 | 32 | 191.2 | 18 | <0.001 | .944 | .068 |

| Model with following constraints | |||||||

| UC → RetPlan | 1543.7 | 33 | 1.54 | 1 | 0.21 | .938 | .067 |

| UC → Sat | 1563.3 | 33 | 21.1 | 1 | <0.001 | .938 | .068 |

| RetPlan → Sat | 1542.3 | 33 | 0.34 | 1 | 0.55 | .938 | .067 |

Correlation among key variables

| 1 | 2 | 3 | 4 | 5 | |

|---|---|---|---|---|---|

| 1. Financial satisfaction | 1 | -0.21*** | 0.33*** | 0.31*** | 0.36*** |

| 2. Underconfidence | 1 | -0.08*** | -0.07*** | -0.09*** | |

| 3. Retirement needs | 1 | 0.33*** | 0.38** | ||

| 4. Employer retirement account | 1 | 0.36*** | |||

| 5. Non-employer retirement account | 1 |

Indirect and direct effects by education level

| HighEd | LowEd | |

|---|---|---|

| Indirect effect: | -0.40 | -0.14 |

| UC → RetPlan → Sat | [-0.52, -0.29] | [-0.21, -0.07] |

| Direct effect: | -1.17 | -1.21 |

| UC → Sat | [-1.35, -0.98] | [-1.34, -1.08] |

Sample characteristics

| Variable | All | By Gender | By Education | ||

|---|---|---|---|---|---|

| Percentage | Whole sample (20,198) | Female (10,845) | Male (9,353) | Low education (13,091) | High education (7,107) |

| Underconfidence | 12.5 | 13.0 | 11.8*** | 13.2 | 12.4* |

| Overconfidence | 22.8 | 19.8 | 25.4*** | 25.9 | 17.2*** |

| Retirement planning | |||||

| Calculating retirement needs | 46.0 | 40.8 | 51.9*** | 37.3 | 61.4*** |

| Employer retirement account | 56.2 | 53.9 | 59.7*** | 45.6 | 76.4*** |

| Non-employer retirement account | 34.4 | 30.0 | 39.5*** | 23.5 | 57.3*** |

| Gender | |||||

| Female | 54.0 | 57.5 | 47.8*** | ||

| Male | 46.0 | 42.5 | 52.2*** | ||

| Marital Status | |||||

| Married | 49.0 | 46.5 | 51.9** | 42.3 | 61.1*** |

| Single | 33.4 | 31.3 | 35.8*** | 37.8 | 25.4 |

| Divorced/widowed/separated | 17.6 | 22.2 | 12.3*** | 19.9 | 13.5 |

| Employment Status | |||||

| Work full-time | 38.6 | 31.9 | 46.4*** | 31.1 | 51.7*** |

| Work part-time | 7.9 | 6.5 | 9.6 *** | 8.3 | 7.2*** |

| Self-employed | 8.7 | 10.2 | 7.0 *** | 9.5 | 7.2*** |

| Homemaker | 6.7 | 11.6 | 1.0 *** | 8.3 | 3.8*** |

| Full-time student | 2.8 | 3.2 | 2.3 *** | 3.7 | 1.1*** |

| Permanently sick/disabled | 5.6 | 6.3 | 4.9 *** | 7.9 | 1.6*** |

| Unemployed | 8.1 | 8.5 | 7.7 *** | 10.6 | 3.6*** |

| Retired | 21.6 | 21.9 | 21.2 *** | 20.3 | 39.4*** |

| Mean | |||||

| Financial satisfaction (1-10) | 5.9 | 5.5 | 6.5*** | 5.4 | 6.5*** |

| Objective literacy (0-6) | 3.0 | 2.8 | 3.4*** | 2.6 | 3.7*** |

| Subjective literacy (1-7) | 5.1 | 4.8 | 5.3*** | 4.9 | 5.4** |

| Age (1-6) | 3.7 | 3.7 | 3.8 | 3.6 | 4.0*** |

| Education (1-7) | 4.4 | 4.3 | 4.6*** | ||

| Income (1-10) | 4.2 | 4.0 | 4.7*** | 3.6 | 5.6*** |

Indirect and direct effects by gender

| Female | Male | |

|---|---|---|

| Indirect effect: | -0.20 | -0.26 |

| UC → RetPlan → Sat | [-0.27, -0.12] | [-0.35, -0.17] |

| Direct effect: | -0.99 | -1.48 |

| UC → Sat | [-1.12, -0.84] | [-1.64, -1.32] |

Comparison between constrained and free model by education level

| χ2 | df | Δχ2 | Δdf | P | CFI | RMSE A | |

|---|---|---|---|---|---|---|---|

| Constrained model | 1742.9 | 50 | .912 | .058 | |||

| Free model | 1485.7 | 32 | 258.2 | 18 | <0.001 | .925 | .067 |

| Model with following constraints | |||||||

| UC → RetPlan | 1507.6 | 33 | 21.92 | 1 | <0.001 | .924 | .067 |

| UC → Sat | 1485.8 | 33 | 0.15 | 1 | 0.69 | .924 | .066 |

| RetPlan → Sat | 1491.1 | 33 | 5.42 | 1 | <0.05 | .924 | .064 |