When people are asked about their regrets in life, they are more likely to regret inaction than action: the investment opportunities forsaken, the career not pursued or the relationship not cultivated. It may be because the outcome of an action is set in stone, but that of inaction feels like boundless opportunity wasted. According to the theory of regret, “actions produce greater regret in the short-term, whereas inactions generate more regret in the long run” (Gilovich & Medvec, 1994, p. 361). The string of regret for missed opportunity looms much larger in one’s mind. When people do not believe in their ability to complete a task, they are unlikely to take action in the first place or put in the effort needed to succeed. Therefore, we know confidence plays an important role in human behavior.

In personal finance, the negative impact of overconfidence, such as excessive stock trading or risktaking in investing, have been studied extensively (Barber & Odean, 2001). By contrast, the impact of underconfidence in one’s financial capability has received far less attention (Heo et al., 2021). Underconfidence can be especially consequential for financial tasks that are complex and effortful. Many financial activities, including investing, retirement planning, and estate planning, require longterm thinking, technical knowledge, and sustained engagement. As financial systems become increasingly complex, individuals who underestimate their financial capability may feel overwhelmed or fearful of making mistakes. This lack of confidence may discourage action, limit engagement with planning tasks, and ultimately reduce long-term financial satisfaction. Despite these implications, little is known about the specific mechanisms through which underconfidence shapes financial outcomes.

While prior work has examined the relationship between underconfidence and retirement planning (Angrisani & Casanova, 2021) and between underconfidence and financial satisfaction (Pearson & Korankye, 2023), no study to our knowledge has tested whether the retirement planning process mediates the relationship between underconfidence and financial satisfaction. Although some studies have examined mediation pathways between confidence and financial satisfaction, these have focused on general financial behaviors rather than retirement planning specifically (Dare et al., 2020). This is a notable omission, given evidence that retirement preparation is strongly linked to financial well-being and life satisfaction (Adam et al., 2017; Pearson et al., 2024).

The purpose of this study is to fill these gaps using the 2021 U.S. National Financial Capability Study. While the relationships among underconfidence, retirement planning, and financial satisfaction have been documented in other national contexts (Bialowolski et al., 2025; Chen & Chen, 2023; Lind et al., 2020), this study extends that work by explicitly testing retirement planning as a mediating pathway and identifying subgroup heterogeneity within a large-scale U.S. sample. By focusing on underconfidence, rather than the more frequently studied overconfidence, and by identifying retirement planning as a key behavioral pathway, this study contributes to the growing literature on financial literacy, retirement planning, and financial satisfaction.

Self-confidence refers to individuals’ beliefs about their ability to perform tasks effectively (Shrauger & Schohn, 1995). People often struggle to assess their competence accurately, creating a gap between what they know and what they think they know, a phenomenon known as knowledge miscalibration (Kruger & Dunning, 1999). Miscalibration can take the form of overconfidence, when people overestimate their abilities, or underconfidence, when they systematically underestimate them.

Evidence from domains outside personal finance illustrates the broad costs of underconfidence. In education, students who underestimate their academic or math ability may avoid selective institutions or math-intensive fields, contributing to underrepresentation in STEM and less ambitious career choices (Jouini et al., 2018). In consumer research, underconfident individuals tend to overinvest effort in information search, set low expectations, choose simpler products, and perform more poorly in sales roles (Kidwell et al., 2021).

In personal finance, emerging evidence suggests underconfidence also carries its own costs. Using data from the United States, Forbes and Kara (2010) suggest that underconfident investors tend toward passive participation in retirement plans and infrequent portfolio adjustments. Heo et al. (2021) further demonstrate that underconfidence leads individuals to take lower financial risk and disengage from investment decisions. Chen and Chen (2023) and Yeh and Ling (2022) both find that underconfident individuals are less likely to plan for retirement in China and Japan, respectively. Similar patterns have been observed in European contexts, where underconfident individuals are less likely to engage in positive financial behaviors, both in the short and long term (Lind et al., 2020). These distorted selfbeliefs are especially important in the context of retirement planning and overall financial satisfaction, where confidence often determines whether individuals act on the financial knowledge they possess.

Confidence plays a central role in whether individuals engage in retirement planning. Studies show that people who feel more confident in their financial knowledge and capability are more likely to calculate how much they need for retirement, own retirement accounts, and make active contribution and investment decisions (Kim et al., 2019; Yeh & Ling, 2022). In this sense, financial confidence can complement objective literacy: even when knowledge is limited, individuals are more likely to translate what they know into planning behaviors when they believe they can manage financial tasks successfully (Anderson et al., 2017; Bannier & Schwarz, 2018).

By contrast, underconfidence in financial capability acts as a barrier to retirement preparation. Underconfidence has been shown to negatively affect both short-term and long-term investment decisions (Ahmad, 2020). Underconfident investors underestimate their own knowledge and skills but overestimate downside risk, which leads to lower trading volume, immobility, and status quo bias (Forbes & Kara, 2010). Because of this passivity, underconfident individuals are slow to join beneficial retirement plans, tend to stick to basic diversification strategies in their retirement portfolios, and avoid necessary portfolio changes (Benartzi & Thaler, 2007). Although they often express interest in learning more about retirement, their lack of confidence limits concrete planning actions, such as participating in a retirement plan or setting aside additional funds for retirement (Angrisani & Casanova, 2021; Bannier & Schwarz, 2018). Underconfidence is also associated with lower wealth accumulation (Van Rooij et al., 2012) and a reduced likelihood of serving as the household’s financial decision-maker (Peters et al., 2019). Over time, this pattern of inaction likely undermines retirement readiness and overall financial satisfaction.

Financial satisfaction is often described as contentment with one’s current financial situation (Joo & Grable, 2004), though it has also been conceptualized as a sense of freedom from financial worry or strain (Zimmerman, 1995). Evidence from a systematic review spanning 303 studies across 36 countries (Tahir et al., 2006) positions financial satisfaction as a key contributor to overall well-being, given its documented associations with life satisfaction (Xiao et al., 2009), relationship quality and stability (Archuleta et al., 2011; French & Vigne, 2019), and psychological health (Owusu, 2023; Prawitz et al., 2006). These interconnections underscore the importance of identifying the determinants of financial satisfaction as a means of supporting individuals' holistic well-being (Archuleta et al., 2011; Joo & Grable, 2004; Prawitz et al., 2006; Xiao et al., 2009).

A growing body of research suggests that financial confidence is one such factor. Studies find that people who feel more confident in their ability to manage money report higher levels of financial satisfaction, even after accounting for objective financial knowledge (Atlas et al., 2019; Dare et al., 2020; Xiao & O’Neill, 2018). Confidence may promote satisfaction by increasing perceived control, lowering financial anxiety, and encouraging engagement in adaptive behaviors such as saving, budgeting, and debt management. Conversely, low confidence and pessimism about one’s financial situation are associated with lower levels of financial satisfaction (Barrafrem et al., 2020). Pearson and Korankye (2023) further show that underconfident individuals experience lower levels of financial satisfaction. In this context, underconfidence is likely to reduce financial satisfaction both directly, through feelings of discontent, worry, and lack of control, and indirectly, by discouraging positive financial behaviors such as saving for retirement.

Only a few studies have examined whether positive financial behaviors mediate the relationship between financial confidence and financial satisfaction. Atlas et al. (2019) test the mediating role of credit card use and found that the link between confidence and satisfaction was partly explained by healthier credit card behavior. In contrast, Dare et al. (2020) reports that financial confidence has a direct effect on financial satisfaction, while the indirect effect through positive behaviors such as active saving, adjusting spending, and shopping for better deals is not significant. These mixed findings suggest that the behavioral pathways linking confidence and financial satisfaction are not yet fully understood, particularly in relation to retirement planning.

Confidence cannot be explained without the distinct and interrelated concept of self-efficacy (Gist & Mitchell, 1992). Therefore, this study employs Self-Efficacy Theory (SET) (Bandura, 1977, 1999) to examine how underconfidence (low financial self-efficacy) shapes retirement planning and financial satisfaction. SET proposes that beliefs about one’s capabilities determine whether people initiate action, how much effort they invest, and how persistently they cope with obstacles. Self-efficacy varies along three dimensions: magnitude (the level of task difficulty one believes they can handle), strength (the certainty of that belief), and generality (the extent to which confidence transfers across tasks and situations) (Bandura, 1977).

In the financial context, individuals with low financial self-efficacy (i.e., underconfidence) may avoid retirement planning because they perceive retirement planning as too difficult (low magnitude), doubt their ability to complete it successfully (low strength), and fail to generalize confidence from simpler financial tasks, such as budgeting or saving, to more complex ones (low generality). Empirically, underconfident individuals are less likely to have a retirement plan, set aside funds for retirement, or engage in short- and long-term investing (Ahmad, 2020; Yeh & Ling, 2022). Thus, we propose two main hypotheses (1a and 1b):

Beyond behavior, SET also predicts positive outcomes: higher self-efficacy fosters perceived control, mastery, and progress toward goals which are core ingredients of well-being (Bandura, 1997, 1999, 2006). Empirically, perceived control and capability are robust correlates of financial satisfaction (Xiao et al., 2014; Xiao & O'Neill, 2018). Therefore, we expect that underconfidence reduces engagement in retirement planning, which in turn lowers financial satisfaction:

The following hypotheses extend the primary model by examining whether the pathways differ across subgroups defined by gender and education. Individuals develop their self-efficacy through experiences, social expectations, and feedback from others (Bandura, 1994). Drawing on Social Role Theory (Eagly & Wood, 2012), gender differences and similarities are viewed as products of societal expectations. These expectations affect individuals’ behaviors, attitudes, and skills. In many societies, men are expected to display competence, control, and independence, particularly in financial decisionmaking (Courtenay, 2000; Fonseca et al., 2012). As a result, financial self-efficacy becomes an important component of masculine identity, and experiencing underconfidence may therefore be more psychologically disruptive and behaviorally consequential for men than for women. Empirically, Yeh and Ling (2022) found that the positive association between financial confidence and retirement planning behaviors was stronger for men than for women, consistent with the idea that confidence is more strongly encouraged and socially reinforced among men in financial decision-making contexts. Thus, we hypothesize:

Furthermore, higher education tends to raise financial knowledge and awareness of how complex finances can be (Bannier & Schwarz, 2018). It also makes people more aware of what they do not know, holding themselves to higher standards, which can lead to more cautious and self-critical decisions (Farrell et al., 2016; Lusardi & Mitchell, 2014). Bannier and Schwarz (2018) found that, particularly among highly educated men, confidence relates more strongly to financial outcomes than objective literacy, suggesting that confidence can amplify behavioral effects in this group. Accordingly, we hypothesize:

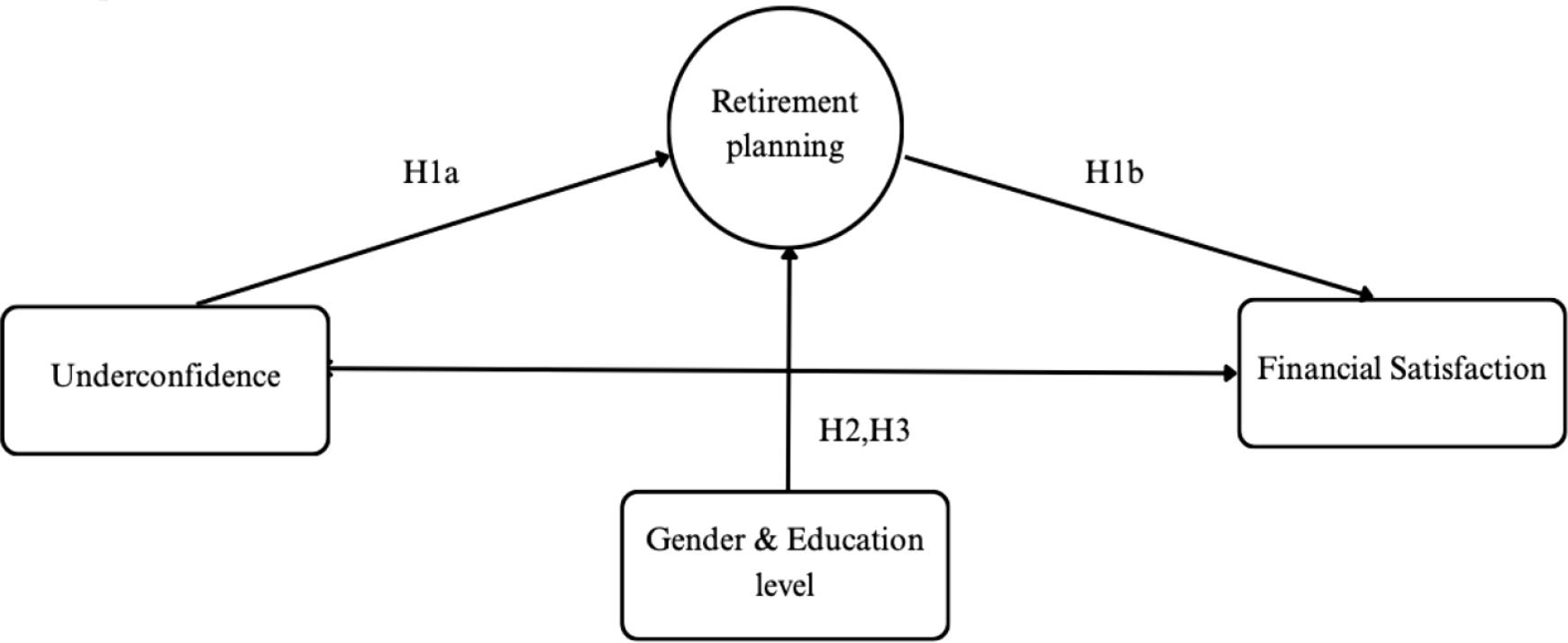

The conceptual model is illustrated in Figure 1. As shown, retirement planning behaviors are hypothesized to mediate the relationship between underconfidence and financial satisfaction (H1a and H1b), with gender and education level serving as moderating variables in the extended model (H2 and H3).

Conceptual Model

The data used for this study comes from the 2021 US National Financial Capability Study (NFCS), a large-scale, ongoing project sponsored by the Financial Industry Regulatory Authority (FINRA). Data collection started in 2009 and continues every three years. The NFCS provides detailed measures of the US populations’ financial literacy, capability, behaviors, as well as demographic characteristics. The original sample (n=27,118) was reduced for analytic purposes to 21,060, comprising all respondents who provided answers to the key questions used for the measurement of variables of interest.

The dependent variable is financial satisfaction. The NFCS survey includes one question measuring financial satisfaction, stated, “Overall, thinking of your assets, debts and savings, how satisfied are you with your current personal financial condition?” Responses range from 1 to 10, with higher numbers indicating greater degrees of financial satisfaction. Multiple and single item measures of financial satisfaction have been shown to be equally valid and reliable (Joo & Grable, 2004).

The key independent variable for this study is underconfidence in financial knowledge. An individual is underconfident when their actual financial knowledge is higher than their self-perceptions. Objective financial knowledge variable is based on the number of correct answers to six financial literacy questions. “Don’t know”, or “Prefer not to say” responses are coded as incorrect, in line with a previous study (Allgood & Walstad, 2016). The subjective financial literacy variable is measured by a single self-assessed question: “On a scale from 1 to 7, where 1 means very low and 7 means very high, how would you assess your overall financial knowledge?”. Following the methodology from previous literature (Allgood & Walstad, 2016; Lind et al., 2020), both objective financial knowledge (0-6) and subjective financial knowledge (1-7) are split into two categories based on individual responses above or below the mean: low group (≤ mean) and high group (>mean). From the two groups within each measure, four variables are constructed: literate (high objective-high subjective), underconfident (high objective-low subjective), overconfident (low objective-high subjective), and illiterate (low objective-low subjective).

Another key variable in this study is a measure of retirement planning behavior. Two aspects of retirement planning behavior are examined: calculating retirement needs and owning retirement accounts. In this study, three variables were created. First, respondents were asked, “Have you tried to figure out how much you need to save for retirement?” or “Before you retired, did you try to figure out how much you needed to save for retirement?” Respondents who answered that they tried to figure it out (either currently or before retirement) were coded as 1. This variable was coded as binary. Respondents were also asked about ownership of retirement accounts through two questions: “Do you (or your spouse/partner) have any retirement plans through a current or previous employer, such as a pension plan, Thrift Savings Plan, or 401(k)?” and “Do you (or your spouse/partner) have any other retirement accounts not through an employer, such as an IRA, Keogh, SEP, or any other self-set-up retirement account?” These two types of retirement account ownership (employer-sponsored and nonemployer-sponsored) were separated into two binary variables. These three variables were treated as observed indicators of a latent retirement planning behavior construct in the structural equation model.

For controlling demographic effects, seven sociodemographic variables were included in the model: gender (male, female), race (white, otherwise), marital status (married, single, and divorced/widowed/separated), employment status (full-time employee, self-employed, part-time employee, homemaker, student, disabled, unemployed, and retired), education (less than bachelor's degree, above bachelor’s degree), age (continuous), and income (continuous). These variables were controlled because prior research has shown their associations with both financial satisfaction and financial planning behaviors (Xiao & O’Neill, 2018).

To investigate the relationships between underconfidence, retirement planning behaviors, and financial satisfaction, Structural Equation Modeling (SEM) is used. SEM is well-suited for this study because it allows us to examine complex relationships between multiple variables and test the mediating role of retirement planning behaviors in the relationship between underconfidence in financial knowledge and financial satisfaction.

In the mediation analysis, bootstrapping was used to provide more robust and accurate estimates of the indirect effects between underconfidence, retirement planning behaviors, and financial satisfaction. Bootstrapping, as described by Preacher and Hayes (2008), involves repeatedly resampling from the data to create numerous simulated samples. This method helps to address the limitations of traditional estimation techniques, which may rely on assumptions that can be restrictive or unrealistic. By generating 1000 bootstrap samples and analyzing these, we can estimate the confidence intervals for the indirect effects without relying on normality assumptions. This approach yields a more reliable assessment of the mediation effect, ensuring that results are not biased and that confidence intervals reflect the true variability in the data.

Furthermore, two multiple-group path analyses were conducted to examine whether the structural relationships differed by gender (men vs. women) and by education level (highly educated vs. less educated individuals). Cross-group invariance was first tested by comparing two nested models. In the constrained model, key parameters (e.g., path coefficients and variances) were restricted to be equal across groups. In the unconstrained model, these parameters were freely estimated for each group. A chi-square difference test between the constrained and unconstrained models was used to assess whether allowing parameters to vary significantly improved model fit.

When the chi-square difference test indicated overall no invariance, follow-up analyses was conducted to identify the specific sources of group differences. First, each structural path was freed one at a time while all other parameters remained constrained, allowing the ability to determine whether the direct effects (e.g., the effect of underconfidence on financial satisfaction) significantly differed between groups. In addition, we tested whether the indirect effect of underconfidence on financial satisfaction through retirement planning differed across groups. All mediation and multiple-group analyses were performed in R using the RStudio environment.

Table A1 in the Appendix reports the sample characteristics. Among the full sample, 12.5% were underconfident and 22.8% were overconfident about their financial knowledge. Underconfidence was more prevalent among females (13.0% vs. 11.8% among males) and those with lower education (13.2% vs. 12.4% among highly educated), while overconfidence was more common among males (25.4% vs. 19.8% among females) and individuals with lower education (25.9% vs. 17.2% among highly educated). As expected, retirement planning behaviors, such as calculating retirement needs and owning retirement accounts, were more frequent among men and those with higher education.

Financial satisfaction was also higher among men (x = 6.5) and highly educated respondents (x=6.5), compared to women (x=5.5) and those with lower education (x=5.4). Lastly, both objective and subjective financial knowledge scores were higher among men and individuals with more education. These descriptive patterns are consistent with prior research showing that men and highly educated individuals typically fare better in retirement planning and report greater levels of financial satisfaction (Nolan & Doorley, 2019; Noone et al., 2018).

Appendix table A2 shows that financial satisfaction was significantly correlated with underconfidence (negatively correlated) and the three retirement planning behaviors (all three were positively correlated). These significant associations among key variables support the assumptions necessary for further mediation multivariate analysis.

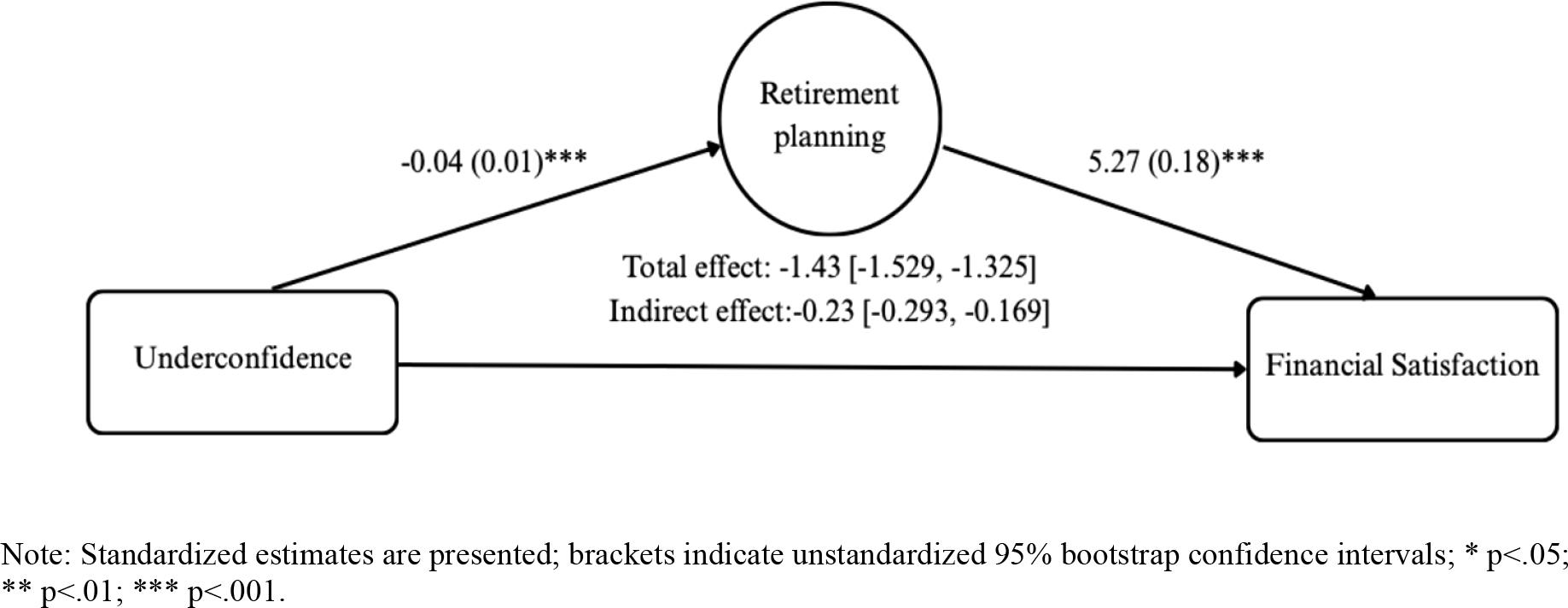

The full-sample model is shown in Figure 2. The fit of the mediation model was relatively strong: RMSEA (0.05) was less than the benchmark value (0.06); CFI (0.95) was over the cut-off value (0.90); and SRMR (0.02) was lower than the criterion value (0.08). By evaluating all criteria, the model in Figure. 2 could be considered a good fit.

Structural Equation Model Predicting Financial Satisfaction

Based on Figure 2, the SEM reveals both direct and indirect relationships between underconfidence, retirement planning, and financial satisfaction. The direct effect of underconfidence on financial satisfaction was negative and significant (β = -1.20), indicating that underconfident individuals tend to report lower financial satisfaction.

Retirement planning was found to partially mediate this relationship. Specifically, underconfidence negatively predicted retirement planning behaviors (β = -0.04), and retirement planning positively predicted financial satisfaction (β = 5.27). The indirect effect from underconfidence to financial satisfaction via retirement planning was also statistically significant (indirect effect = -0.23, 95% CI [0.293, -0.169]). The total effect of underconfidence on financial satisfaction was significant (total effect = -1.43, 95% CI [-1.529, -1.325]). These findings suggest that retirement planning serves as a significant partial mediator: underconfident individuals are less likely to plan for retirement, which in turn contributes to reduced financial satisfaction. Thus, Hypothesis 1a and 1b were supported.

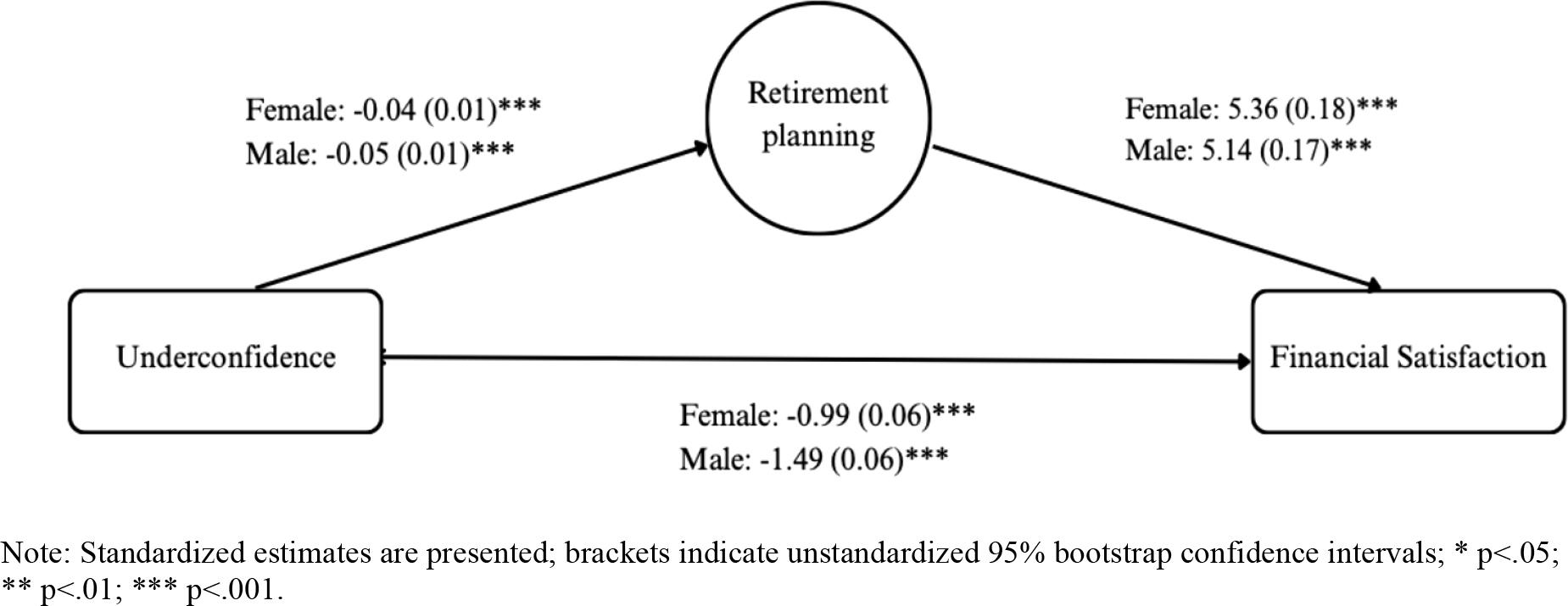

Multiple-group path analysis was conducted to examine gender differences in the proposed model. As shown in Appendix table A3, a chi-square difference test comparing the constrained and free models revealed a significant overall difference between males and females (Δχ2 = 191.2, Δdf = 18, p < .001). To explore the source of this difference, we tested each path individually. The path from underconfidence to financial satisfaction showed a significant gender difference (Δχ2 = 21.1, p < .001), with the negative association being notably stronger among males (β = -1.49) than females (β = -0.99; see Figure 3). This finding suggests that men may be more vulnerable to the negative consequences of low financial confidence, despite traditionally being perceived as more financially self-assured. Thus, Hypothesis 2 was supported.

Structural Equation Model with Gender

The mediation effect of retirement planning between underconfidence and financial satisfaction was observed in both genders, with the indirect effect accounting for approximately 17% of the total effect among females and 15% among males, as shown in table A4. However, the difference in the size of the indirect effects between groups was not statistically significant, indicating that while mediation exists for both genders, its strength does not meaningfully differ.

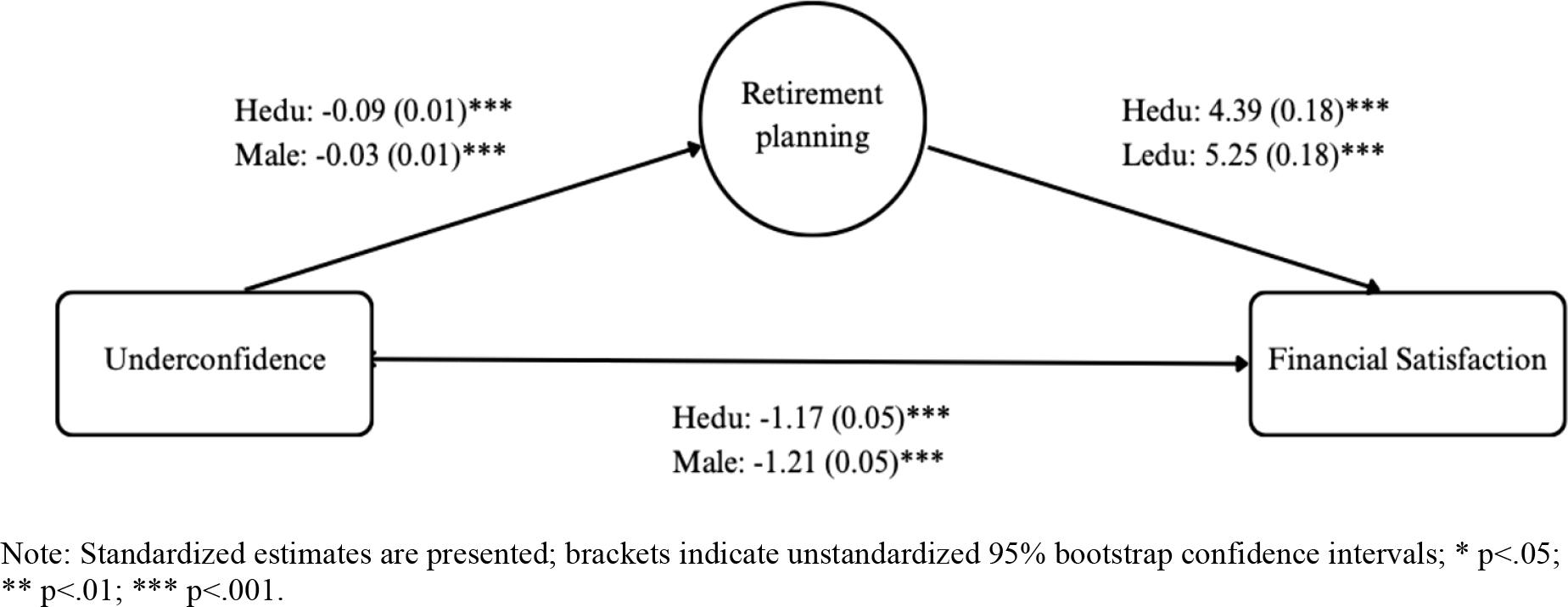

Next, the structural model is assessed for differences across education levels, comparing participants with a bachelor’s degree or higher (Hedu) to those with less than a bachelor’s degree (Ledu). A comparison between the constrained and free models revealed a significant overall difference between the two groups (Δχ2 = 258.2, Δdf = 18, p < 0.001; see Appendix table A5). To pinpoint the source of these differences, each path was tested separately. Significant differences were found in the path from underconfidence to retirement planning (Δχ2 = 21.92, p < 0.001) and from retirement planning to financial satisfaction (Δχ2 = 5.42, p < 0.05). Notably, the negative association between underconfidence and retirement planning was stronger among the highly educated group (β = -0.09) than the lower educated group (β = -0.03; see Figure 4). This result suggests that even with greater financial knowledge, highly educated individuals may be more sensitive to their own lack of confidence, which acts as a barrier to engaging in retirement planning. Therefore, Hypothesis 3 was supported.

Structural Equation Model with Education Level

Finally, the mediating effect of retirement planning differed significantly by education level (table A6). Among highly educated individuals, the indirect effect accounted for 25% of the total effect, compared to only 10% among those with lower education. This indicates that retirement planning plays a more substantial mediating role for highly educated individuals, compared to low educated individuals.

This study contributes to the financial literacy and satisfaction literature as results indicate that underconfident individuals are less likely to engage in retirement planning, and this lack of proactive behavior contributes to lower financial satisfaction. These findings reinforce prior research suggesting that financial satisfaction depends not only on financial knowledge but also on confidence in applying that knowledge (Dare et al., 2020; Xiao & O'Neill, 2018).

The study also reveals meaningful group differences. Although the descriptive results show that men and highly educated individuals generally report higher retirement planning participation, greater financial knowledge, and higher financial satisfaction, the multigroup analyses tell a more nuanced story. The adverse effects of underconfidence are particularly evident among these same groups. For men and highly educated individuals, lacking confidence in financial knowledge undermines engagement in retirement planning and financial satisfaction more significantly than it does for other groups. This pattern suggests that underconfidence operates as a hidden barrier, even for individuals who appear to be financially capable.

Traditional financial education has focused primarily on improving knowledge, yet prior research and the present findings suggest that knowledge alone does not lead to lasting behavior change and improved well-being (Kaiser & Menkhoff, 2017; 2021). This study highlights that even individuals with adequate financial knowledge may hesitate to engage in retirement planning due to low confidence in their abilities. These findings suggest that financial education programs should go beyond delivering financial content and explicitly target participants' confidence and efficacy in applying and acting on that knowledge.

Drawing on Self-Efficacy Theory (Bandura, 1997), financial educators can strengthen financial selfefficacy through several evidence-based strategies. First, mastery experiences, like having participants successfully complete small, manageable planning tasks such as estimating basic retirement expenses or checking eligibility for employer-sponsored plans, can build perceived competence through direct experience. Second, verbal encouragement and positive feedback from educators and peers can reinforce participants' belief in their own capabilities. Third, vicarious learning through peer stories about how others began preparing for retirement can help underconfident individuals see planning as achievable. Together, these approaches help participants recognize that their existing financial knowledge is sufficient and build the confidence needed to translate that knowledge into action thus addressing the gap this study identified between what individuals know and what they feel capable of doing.

Although financial education often prioritizes low-income, women, and other vulnerable populations, who are statistically more likely to face financial insecurity (Collins & O’Rourke, 2010), the present findings show that men and highly educated individuals may also require targeted support when they experience low confidence in their financial knowledge. Because they are often assumed to be financially capable, their lack of confidence may go unrecognized, and instruction may move too quickly from information to action, risking disengagement among underconfident participants.

For men, one practical implication is the importance of creating private, low-pressure learning environments, since they may be less willing to express uncertainty or ask questions in group settings. Offering one-on-one consultations or anonymous digital formats might make it easier for them to engage. For example, a brief online confidence assessment completed before a program can be used to privately gauge perceived financial self-efficacy and planning readiness, followed by individualized recommendations.

A second implication is to leverage life transitions as natural motivators. Research suggests that men’s financial behaviors are closely linked to major life changes and role expectations; for example, men often increase their savings behavior when they become fathers (Lewis & Messy, 2012). Such transitions may also strengthen financial self-efficacy as men assume provider roles. Although the present study did not examine life transitions directly, these findings raise the possibility that financial education targeting underconfident men may be most effective when aligned with such moments, potentially framing retirement planning as a way to protect one's family or secure intergenerational stability, and linking specific planning actions to valued roles and identities.

Prior research indicates that financial education tends to have a larger positive impact on financial literacy for individuals with lower education than for those with higher education (Wagner, 2019). However, the present findings suggest that highly educated individuals are not automatically protected: when they are underconfident, they may be especially likely to disengage from retirement planning. This implies that they also warrant attention in financial education and counseling, not because they lack knowledge, but because they struggle to translate that knowledge into action. For highly educated but underconfident individuals, a useful strategy is to build on strengths they already possess. Educators can draw attention to participants’ prior mastery experiences in other complex domains, such as academic work, professional problem-solving, or project management, and explicitly link these experiences to retirement planning. Framing planning as another form of analysis, long-term thinking, and risk assessment helps reclassify it as something they are already capable of doing rather than a completely new or overwhelming task. Rather than providing more information, educators can help participants recognize that their existing financial knowledge is sufficient and show them how to use that knowledge to take the next step in retirement planning. Finally, highly educated individuals tend to hold themselves to higher standards and may delay action until they feel fully prepared. For underconfident individuals in this group, financial educators can help shift the focus from perfection to progress, emphasizing that good enough decisions move them forward and that plans can be revised over time. This approach lowers the psychological barrier to action and supports gains in financial self-efficacy.

While the findings from this study are noteworthy, especially regarding gender and education differences in the role played by underconfidence in retirement planning and financial satisfaction, several limitations should be considered when evaluating the results. First, the data is cross-sectional, which cannot be used to test causality. Future research may address this issue using longitudinal data. Second, the dataset is limited to residents of one country. Culture has a significant influence on the relationship among the variables assessed in this study. In a different culture, the relationship between these variables could be different based on normative roles and expectations as well as socio-economic supports. Future research could use data from multiple countries to explore the effects of underconfidence and financial planning on financial satisfaction. Third, similar to previous studies (Tahir et al., 2022; Xiao et al., 2014), the measurement of financial satisfaction contains only one question. In future research, multiple questions could be used to measure financial satisfaction, as other studies have proposed (Fachrudin et al., 2022). Finally, the self-reported retirement planning behaviors used in this study are not a comprehensive portrayal of the behaviors that comprise retirement planning. Individuals planning for retirement may also take lifestyle and life expectancy into consideration, as well as other sources of income, such as Social Security benefits. In future studies, actual financial behaviors could be assessed, for instance, by collecting information about whether someone is currently contributing to a retirement account, rather than just owning one or more, like the current study. Or individuals could be asked to provide their financial statements or retirement account data. Despite these limitations, the study draws attention to the overlooked role of underconfidence in personal finance and provides actionable insights for financial professionals seeking to support client engagement and well-being.