The turbulence of the conditions in which companies operate, observed over the past decades, has significantly intensified in recent years. In addition to longterm and evolutionary phenomena, although developing at different paces, there were sudden and unexpected events that significantly changed the rules of the markets. Events such as the COVID-19 pandemic and the conflict in Ukraine have brought unforeseen disruptions to global supply chains, the energy sector, and agriculture, with a significant impact on economies (Pacut, 2024). These sudden factors have made it necessary for both consumers and businesses to adapt to the new realities, presenting markets with a number of new challenges.

In the United States, the COVID-19 pandemic represented an unprecedented shock to small businesses, comparable only to the Great Depression of the 1930s. In March 2020, 43% of businesses were temporarily closed, and employment fell by 40%. Entrepreneurs had little cash on hand at the beginning of the pandemic, which meant they had to drastically cut expenses, take on additional debt, or declare bankruptcy (Bartik, et al., 2020). In Asia, particularly in China and South Korea, authorities swiftly implemented strict lockdowns and other pandemic control measures, which directly impacted many industries, notably leading to the closure of food establishments and a subsequent drop in their revenues (Kim, et al., 2021; Liu, et al., 2023).

In many other countries, restrictions on the operation of restaurants were also introduced, such as limits on the number of customers, bans on in-person service, and social distancing requirements (Nicola, et al., 2020; Liu, et al., 2023). The food service industry had to quickly adapt to the new realities, for instance, by expanding delivery and takeout services (Gössling, et al., 2020; Shi and Xu, 2024; Szymańska, et al., 2024). It became evident that economies with more developed tourism sectors were more severely affected by the economic crisis caused by the pandemic than economies less dependent on this sector (Seržantė and Pakalka, 2022).

In Poland, the pandemic led to numerous bankruptcies of small and medium-sized enterprises, including those in the food service industry. Restaurant owners faced multiple challenges, such as a decline in customers, the need to implement sanitary protocols, and liquidity issues (Grochowicz, 2020). In 2020, Poland's accommodation and food service sector recorded a 31% drop in revenues. Case studies (Orzeszak, 2022) of many businesses in this sector highlighted difficult conditions, including a decline in profits and revenues as well as increased debt. Consequently, state assistance was necessary to mitigate the effects of lockdown policies, similar to other countries (Vojtekova and Kliestik, 2024).

Another shock for the food service industry was the outbreak of armed conflict in Ukraine, which contributed to rising food prices and supply chain issues, further destabilizing the already fragile financial situation of food establishments (Jagtap, et al., 2022; Urak, 2023). The cumulative impact of these events (COVID-19 pandemic, disruptions in global supply chains, geopolitical tensions) led to a general rise in prices (Churski and Kaczmarek, 2022). For the food service sector, which was already struggling with financial problems, this meant the need to adapt to rapidly changing economic conditions. One of the most significant aspects of inflation's impact on the industry was the rising cost of raw materials and food products. The prices of basic items like meat, dairy, vegetables, and grains increased by an average of 15%–30% compared to the previous year (Kowalska, et al., 2023). This forced restaurant and bar owners to raise menu prices, which could lead to reduced demand from consumers, especially among lower-income groups. Rising energy costs, particularly gas and electricity, posed another significant problem for the food service industry. Establishments, which rely on a constant supply of energy for cooking, cooling, and lighting, had to contend with increasing bills, directly affecting their profitability (Ari, et al., 2022).

The aim of this article is to identify and assess the impact of rising inflation on the condition and functioning of the Polish food service sector, based on the analysis of recent industry reports and market data. The aim of this article is to determine how the COVID-19 pandemic and the conflict in Ukraine influenced the functioning of the food service sector in Poland between 2020 and 2023. The article seeks to illustrate how these global events affected changes in the food service industry, disruptions in supply chains, inflation levels, and consumer behavior in the food services market.

The article addresses the following research questions:

- (1)

How has inflation affected the operating costs and profitability of food service businesses in Poland?

- (2)

What changes in consumer behavior have been observed in the gastronomy market during this period?

The source of information on the condition of the food service industry included industry research reports and data from household budgets by Poland's Central Statistical Office (GUS). The article is divided into four parts. Following the introduction, the impact of inflation on the food service sector in Poland is described, considering the rising costs of raw materials and services. It also presents how entrepreneurs adapted their pricing and operational strategies in response to changing economic conditions. The next section analyzes how consumers reacted to rising prices in food service by adjusting their purchasing habits. It highlights changes in spending levels on food services and accommodation in household budgets, as well as consumer preferences for choosing restaurants and the frequency of using food services in the context of rising costs.

This study is based on a descriptive-analytical approach combining secondary data analysis and review of recent reports related to the Polish food service sector between 2020 and 2023. The main sources of data include publications from the Central Statistical Office of Poland (GUS), national debt registers, sectoral reports by PMR Market Experts, and ARC Rynek i Opinia, as well as selected scientific literature published between 2020 and 2024. Depending on data availability and analytical needs, some references also include data from earlier (e.g., 2000–2019) or later periods (e.g., early 2024), to ensure continuity and completeness of trends and comparisons.

The data used in this article are quantitative in nature and pertain to economic indicators such as inflation, food service turnover, household expenditures, and price indices. Qualitative insights are drawn from existing surveys and interviews with restaurateurs published in industry reports. These materials were selected using purposive sampling, focusing on publicly available sources with a national scope, relevant to the HoReCa industry during the pandemic and postpandemic period.

The structure of the article follows a thematic approach, organized around three major research areas:

- 1.

The economic impact of the COVID-19 pandemic and the war in Ukraine on the food service sector.

- 2.

Consumer behavior and expenditure patterns in response to inflation.

- 3.

Regional and segmental differentiation in the response of the food service market.

While this study does not rely on original empirical research, it synthesizes and integrates multiple verified data sources to provide a comprehensive overview of recent sectoral transformations. The validity of the findings is supported by statistical significance tests reported in the source materials and triangulation across multiple data sets.

In Poland, the process of destabilizing the economy began with the first case of SARS-CoV-2 in March 2020, and the effects of this crisis are still visible today (Szczęsny, 2021).

The pandemic has introduced enormous uncertainty that has affected many sectors of the economy. Industries that require direct contact with customers, such as gastronomy, tourism, and education, have been particularly hard-hit (Szyriajewa and Makarenko, 2020). Companies offering these services did not predict a long-term epidemic in their forecasts, which significantly disrupted their operations. They kept product stocks at an optimal level. However, the introduction of restrictions related to the coronavirus pandemic has led to the destabilization of production plans, deliveries, and inventories (Kacperska, et al., 2023). Supply chains have been interrupted, which has caused delays in the supply of raw materials and materials necessary for production. Shortages of finished products in warehouses and delays in deliveries to stores led to increased demand from consumers, who bought groceries and households en masse for fear of shortages. Shelves in stores began to empty and brick-and- mortar sales moved online (Brząkała, 2022). Entrepreneurs were forced to adapt their businesses to restrictive requirements or completely give up running a business that was then becoming completely unprofitable (Skwirowski, 2024).

The relative calm and stabilization of this market was again disturbed by the war in Ukraine, which led to another collapse of supply chains and an increase in the prices of raw materials, which had an impact on the costs of operations conducted by all companies. The conflict in Ukraine has plunged global food and energy markets (Krzykowski, 2022). The increases incurred have had a real impact on the increase in prices and inflation. According to research conducted by Grzelak and Sobczyk (2024), disruptions in the functioning of global supply chains caused an increase in food prices in the first period of the conflict by about 34%. The result was therefore an increase in inflation, which at the end of 2022, in relation to catering services, reached around 17% (data source: Central Statistical Office).

The Russian aggression against Ukraine caused an increase in consumer price indices, which manifested itself in the form of rising prices of fuel, energy, and raw materials or the weakening of the currency, and resulted in large debts of over PLN 363 million in 2023 (National Debt Register, 2023). According to the National Debt Register, the catering sector struggled with increasing operating costs and a growing outflow of customers (National Debt Register, 2023). This was contrary to the data published by the Central Statistical Office (Table 1).

Revenues from catering activities in the years 2020–2022

(Source: Own study analysis based on CSO, 2022)

| Specification (in PLN million) | 2020 | 2021 | 2022 |

|---|---|---|---|

| Total revenue | 37,645.6 | 48,680.6 | 64,643.4 |

| From the sale of goods | 4,592.1 | 5,569.2 | 7,848.2 |

| From catering production | 32,596.4 | 42,564.8 | 56,107.2 |

| From other activities | 457.1 | 546.6 | 688.0 |

Data on the catering market show that revenues from catering activities at current prices in 2022 amounted to PLN 64.6 billion, which meant an increase of PLN 15,962.8 million (32.8%) compared to the previous year. The increase in revenues was largely the result of rising prices, which were intended to compensate for the effects of inflation. Thus, the recorded increase was not an indicator of a real improvement in the financial condition of companies in this industry. The high revenues were the result of inflationary pressure, not an increase in sales volume.

The vast majority of HoReCa debts were related to multifactorial difficulties in the commodity market (increased inflation due to droughts, the COVID-19 pandemic, the Russian invasion) and operating costs. The factors causing the sharp increase in food production costs were the increase in the prices of agricultural fertilizers, high prices of natural gas, which is responsible for the production of nitrogen fertilizers, and fuel necessary for the operation of agricultural machinery (Górska and Kuchciński, 2024). The increase in the prices of agricultural raw materials contributed to increases in the prices of food products, and limited access to agricultural fertilizers increased the costs of food production, including confectionery, which directly affected the prices of final products in the catering sector (Prokopowicz, 2024).

The conflict in Ukraine has increased entrepreneurs' concerns about the stability of energy supplies, including from Russia, which was responsible for 1/4 of global natural gas exports and supplies of raw materials for food production, which resulted in the search for alternative supplies. Diversification of supplies has therefore become a priority, regardless of rising costs (Górska and Kuchciński, 2024). Restaurateurs were, therefore, forced to raise prices, which affected the demand for their services.

According to a report by the PMR Market Experts research agency entitled “HoReCa market in Poland 2023. Market analysis and development forecasts for 2023-2028. The impact of inflation, the war in Ukraine and the effects of the COVID-19 pandemic,” developed in spring 2023, the key challenges for companies operating in the catering sector were rising prices and rising operating costs. Increased costs of maintaining the premises, such as fees for utilities or food raw materials, were then the main obstacle to the effective running and further development of the catering business. Compared to previous years, this barrier has increased by more than 30 percentage points (PMR Market Experts, 2023).

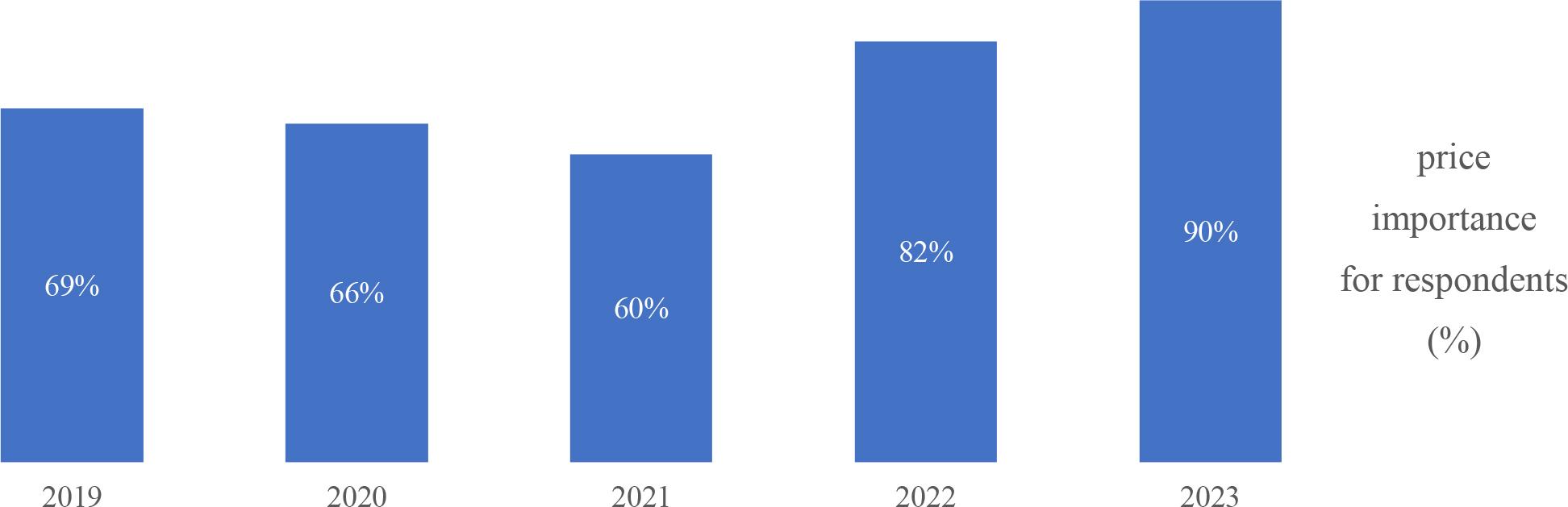

In 2023, galloping inflation and rising costs of doing business have made price an even more important criterion when choosing a supplier of products for catering establishments. Of the 595 respondents, 90% of them considered the prices of their products to be the most important factor influencing the choice of a given supplier of goods in the PMR Market Experts report (Figure 1), which is 8% more than in 2022. The second place was taken by the quality of goods (85%), while aspects such as speed and timeliness of deliveries and a wide selection of products turned out to be less important.

Price significance when choosing a supplier of goods by gastronomy owners in 2019–2023

(Source: Own study analysis based on PMR Market Experts, 2023)

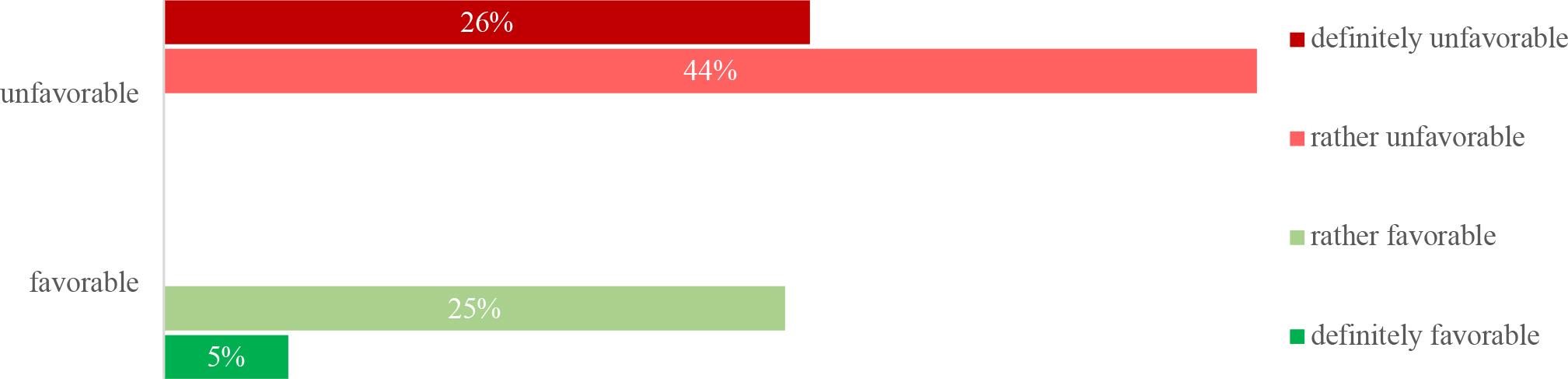

A report expanding on these observations was the study “For Restaurant. Market research and report 2023/2024. Informational contribution for the future of the HORECA industry in Poland” conducted by the ARC Rynek i Opinia Research Institute and FOR Solution (ARC Rynek Opinia & FOR Restaurant, 2023). The survey involved 302 restaurateurs who undertook to assess the conditions prevailing in 2023, 70% of whom considered them to be definitely unfavorable for running a catering business (Figure 2).

Conditions for running a catering establishment in 2023

(Source: Own study analysis based on ARC Rynek Opinia & FOR Restaurant, 2023)

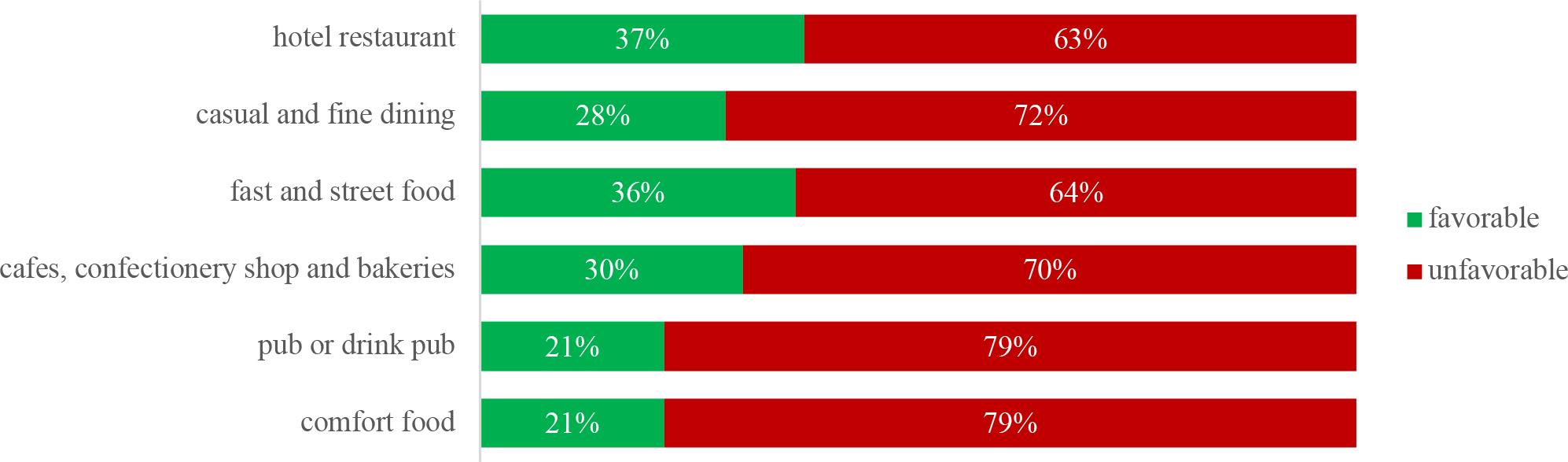

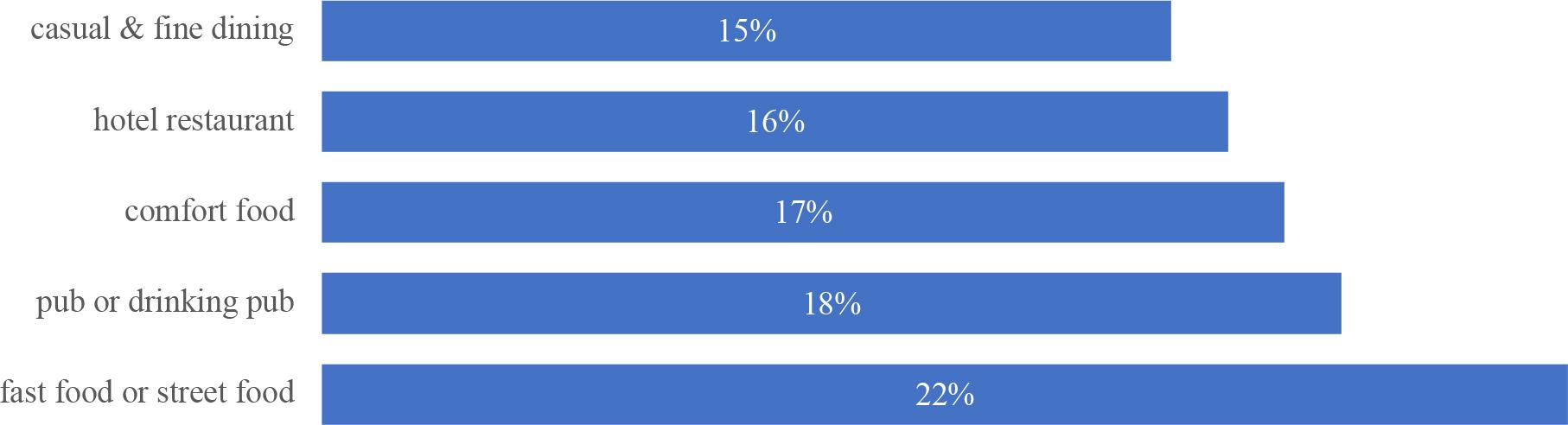

According to the respondents, the most difficult situation was then in the comfort food segments, that is, in restaurants offering traditional dishes, as well as in bars and pubs (Figure 3).

Conditions for running a catering establishment in 2023 with a breakdown of the answers for individual segments

(Source: Own study analysis based on ARC Rynek Opinia & FOR Restaurant, 2023)

Relatively better moods were noticed in the fast food and street food segments, as well as in hotel restaurants. They could result, among other things, from the habits of consumers, who most often reach for dishes from fast food restaurants. On the other hand, in the case of hotel restaurants, less pressure could be responsible for the better results than in the case of other establishments. In hotel restaurants, the customer base is often provided by the hotels to which the restaurants are assigned, so the owners of such places do not feel the need to put the restaurant above the hotel industry. The study also analyzed prices, finding that 80% of the restaurateurs surveyed indicated an increase in prices in their premises in 2023 (Figure 4).

Price increases in individual restaurants in 2023

(Source: Own study analysis based on ARC Rynek Opinia & FOR Restaurant, 2023)

Across the industry, prices increased by 18% compared to the previous year. However, this was less than in the fast food/street food segment itself, where prices increased by 22%. As noted in the Report, the largest jump in prices was recorded in the eastern macroregion—directly adjacent to Ukraine. Voivodeships such as Lubelskie, Podkarpackie, and Podlaskie experienced a 24% increase in prices in restaurants compared to the previous year. According to respondents, in these regions, the turnover in their catering establishments remained largely unchanged or even decreased (Table 2).

Turnover in catering establishments in 2023

(Source: Own study analysis based on ARC Rynek Opinia & FOR Restaurant, 2023)

| Voivodship | Turnover dynamics | Turnover remained unchanged | ||

|---|---|---|---|---|

| Dolnośląskie Voivodship | 38% | |||

| Kujawsko-Pomorskie Voivodship | 46% | |||

| Lubelskie Voivodship | 36% | |||

| Lubuskie Voivodship | 44% | |||

| Łódzkie Voivodship | 30% | |||

| Małopolskie Voivodship | 35% | |||

| Mazowieckie Voivodship | 30% | |||

| Opolskie Voivodship | 38% | |||

| Podkarpackie Voivodship | 36% | |||

| Podlaskie Voivodship | 36% | |||

| Pomorskie Voivodship | 46% | |||

| Śląskie Voivodship | 35% | |||

| Świętokrzyskie Voivodship | 30% | |||

| Warmińsko-Mazurskie Voivodship | 46% | |||

| Wielkopolskie Voivodship | 44% | |||

| Zachodniopomorskie Voivodship | 44% | |||

In the eastern region, turnover in catering establishments increased in the case of only 30% of the restaurateurs surveyed. The remaining group of respondents noticed a stagnation in sales or a decrease in the total value of orders. The situation was different in central Poland, where an increase in turnover was observed in relation to 58% of restaurateurs. Smaller increases were also recorded by restaurateurs from the Pomeranian, Kuyavian-Pomeranian, and Warmian-Masurian Voivodeships. In this area, on average, one in five restaurateurs noticed an increase in turnover in their establishment. It is also worth noting that the levels of increases in these prices are higher than the average inflation level recorded in the first half of 2023, which, according to GUS data, was 15% at the time. This means that the average increase in costs in gastronomy may be higher than the cost of the entire economy. Therefore, raising prices in the industry results not only from the desire to increase profits but also from the pressure exerted on entrepreneurs in this industry and the prices of products and fees (utilities) related to running a business, which they have to pay.

The response of the food service industry to the numerous challenges it faced involved various adaptive strategies, such as modifying menus, introducing smaller portion sizes, increasing price diversity of products, and developing alternative sales methods, including takeout and catering services (Hundertmark & Pettersson, 2023). Additionally, restaurants began to utilize technology more intensively by implementing online reservation systems and automating orders and payments, which helped reduce operational costs and improve efficiency (Rezaei, et al., 2024; Türkeș, et al., 2021; Messabia, et al., 2022).

The effects of inflation were also felt among consumers. Restrictions on real household incomes have forced society to decide which expenditures to reduce or which to give up altogether. Consumers experiencing such a strong increase in prices have been forced to limit the purchase of goods and services that are not necessary for life, that is, goods other than the first order. Such goods include catering services (ARC Rynek Opinia & FOR Restaurant, 2023).

The economic crisis caused by the pandemic has also had a significant impact on the functioning of households. The increase in the cost of living, which is a consequence of inflation and disruptions in global supply chains, contributed to the deterioration of consumer sentiment. Concerns about further price escalation have led to the phenomenon of so-called accelerated consumption, which involves the earlier purchase of durable goods for fear of further increases. At the same time, a decline in the propensity to save was observed, which could have had a huge impact on the financial stability of households in the long term.

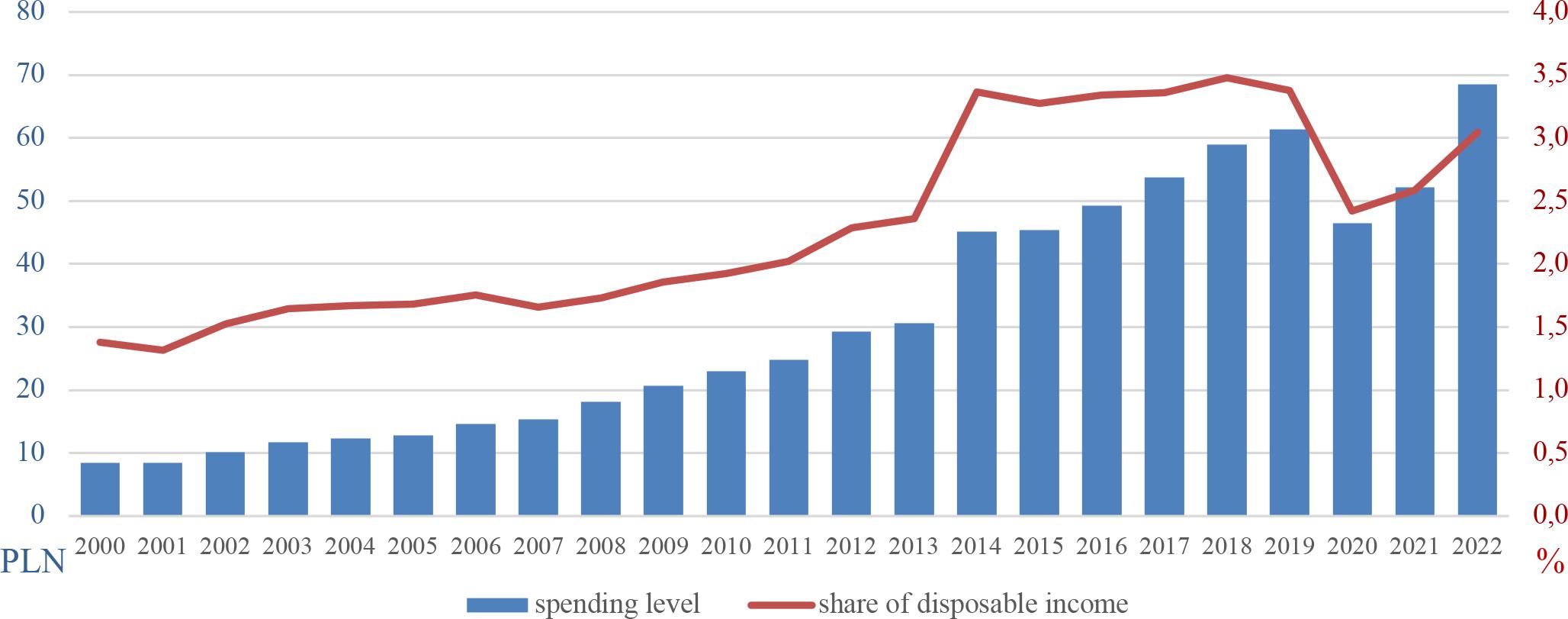

Moving to the analysis of expenditures on food services and accommodation over a longer period, specifically from 2000 to 2022, it should be noted that in Polish households, these expenditures statistically significantly increased (p < 0.0000), averaging an annual rise of 2.76 PLN. A statistically significant increase was also recorded in the share of expenditures on food services and accommodation in disposable income, averaging an annual growth of 0.095%. The upward trend in expenditures was weakened by the COVID-19 pandemic, which led to a reduction in both the level and share of expenditures on food services and accommodation. Analyzing the period from 2019 to 2022, there was a noticeable decline in expenditures on food services and accommodation in household budgets, dropping from over 61 PLN in 2019 to slightly above 46 PLN in 2020 and 52 PLN in 2021. In 2022, expenditures on food services and accommodation in Polish households increased, surpassing the level of 2019 and reaching nearly 69 PLN. Following the decline in expenditure levels for these services during the COVID-19 period, their share in disposable income also decreased, from 3.4% in 2019 to 2.4% in 2020. In 2022, the share of expenditures in this category rose to 3.0% of disposable income. In nominal terms, expenditures on food services and accommodation increased by over 31% in 2022, while in real terms, the rise was nearly 21%. This situation was influenced by a 15.6% increase in prices for food and accommodation services in 2022 compared to 2021 (Figure 5).

The level of expenditures on restaurant and hotel services per person in the household (in PLN) and their share in disposable income (%) from 2000 to 2022

(Source: Own study based on data from household budgets from subsequent years, GUS)

Expenditures on food services and accommodation vary according to socioeconomic and demographic variables. The most is allocated to food and accommodation services in households led by individuals with higher education and the most favorable financial situation (Piekut, 2013) as well as from socioeconomic groups: employees in non-manual positions and selfemployed individuals (Piekut, 2019). Analyzing expenditures on food services and accommodation in household types based on the level of education of the household representative from 2019 to 2022, it can be stated that with an increase in the level of education, expenditures on these services increased, meaning that the higher the education level of the household representative, the greater the expenditures on food services and accommodation. Between 2019 and 2020, there was a decrease in expenditures on food and accommodation services across all types of households according to education level, after which these expenditures began to rise in the following years. In 2022, expenditures in households of individuals with basic vocational, secondary, or higher education exceeded the expenditures from 2019. In households of individuals with at most primary education, expenditures on food services and accommodation in 2022 remained lower than in 2019 (Table 3). In the early years of the pandemic, the gap in expenditures on food services and accommodation between households with the lowest and highest levels of expenditure narrowed. In 2019, the expenditure gap between household types with individuals having at most primary education and households with individuals with higher education was 66 PLN, which decreased to 57 PLN the following year. In 2022, this expenditure gap reached its highest level at 77 PLN.

The level of expenditures on food services and accommodation (in PLN) in households according to the education level of the household representative from 2018 to 2022

(Source: Own calculations based on GUS household budgets)

| Specification | 2019 | 2020 | 2021 | 2022 |

|---|---|---|---|---|

| Unit of measure | PLN | |||

| At most primary school education | 38 | 24 | 27 | 34 |

| Basic vocational education | 36 | 26 | 29 | 45 |

| Secondary education | 58 | 39 | 46 | 60 |

| Higher education | 104 | 81 | 91 | 111 |

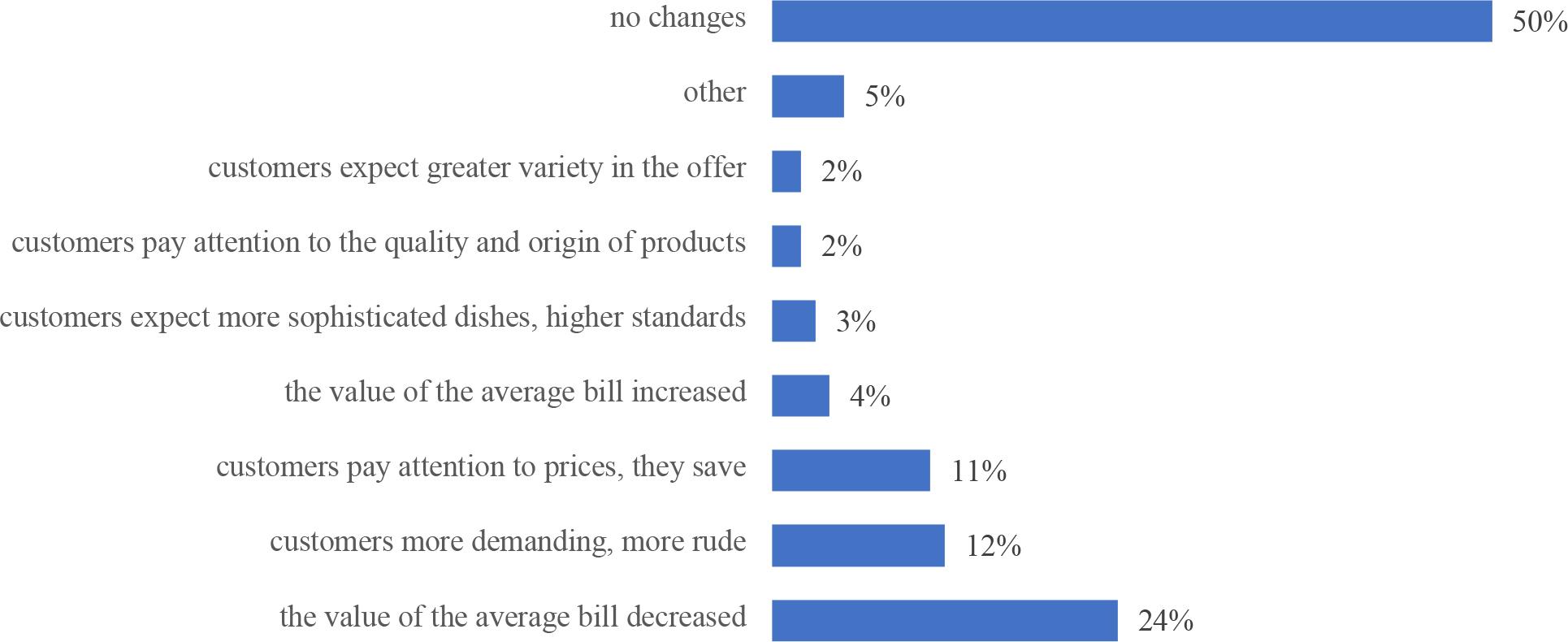

Galloping inflation has led to changes in consumer behavior in the catering and hotel services market. The “For Restaurant” Report analyzes orders and bills in the HoReCa sector (Figure 6).

Changes in customer behavior in 2023

(Source: Own study analysis based on ARC Rynek Opinia & FOR Restaurant, 2023)

The report found that almost one in four restaurateurs noticed a decrease in the average size of the bill paid by the customer compared to the previous year, primarily indicated by restaurateurs from the fast food/street food segment (29% of respondents) and bars and pubs (29% of respondents). According to restaurateurs, customers affected by inflation have become more demanding, demanding and rude, as indicated by 12% of respondents, 30% of whom represented cafes, pastry shops, and bakeries. According to the survey, one in ten restaurateurs indicated a visible trend in saving money and making more thoughtful orders. In this area, the biggest changes were felt by restaurateurs from the comfort food segment, that is, local pizzerias, milk bars, or local places with simple menus. There were also reasons to require a higher standard (3%), the search for better quality of the goods offered (2%), as well as greater diversity in the offer (2%). Half of the respondents did not notice any changes in the behavior of their guests.

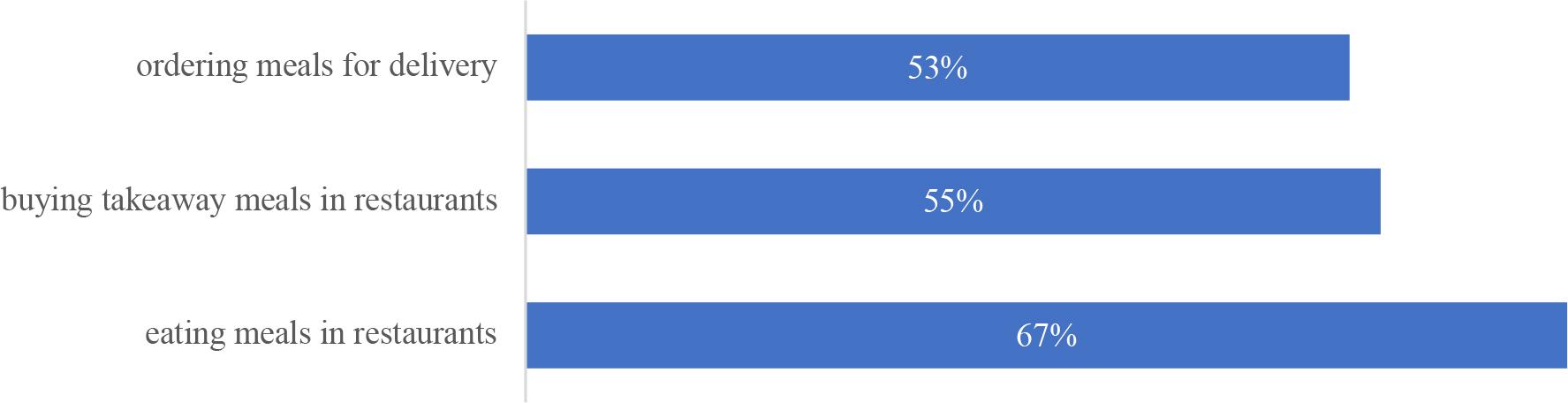

The PMR Report entitled “HoReCa market in Poland 2023. Market analysis and development forecasts for 2023-2028. The impact of inflation, the war in Ukraine and the effects of the COVID-19 pandemic” showed that in 2023, 67% of respondents who were buyers of catering services regularly ate meals in catering establishments (Figure 7).

Declarations regarding the use of HoReCa services in 2023

(Source: Own study analysis based on PMR Market Experts, 2023)

According to the report, take-away and delivery options were also increasingly used. Delivery options using Glovo, Uber Eats, or Wolt were becoming more and more popular. Restaurateurs who introduced the possibility of using an application to order dishes noted an increase in interest in the service offer. The data show that 55% of respondents using catering services in the surveyed period chose the option of buying takeaway meals, which could result from the need to save time or protect against potential health threats in public places. In turn, 53% of the respondents indicated that they mainly ordered meals with home delivery, without having to go to a restaurant.

The increase in activity in the catering sector may have resulted from the improvement of the economic situation after the period of slowdown caused by the pandemic and from the gradual increase in social mobility, which was the result of the lifting of restrictions and unblocking the possibility of travel. The easing of restrictions allowed consumers to return to restaurants, bars, and cafes, which contributed to the recovery of demand for food services. The increase in the prices of groceries and catering services, driven by rising inflation, has significantly burdened household budgets. Inflation, by driving up the cost of living, has forced consumers to save and be more prudent about spending, especially non-essential spending, such as eating out or ordering delivery.

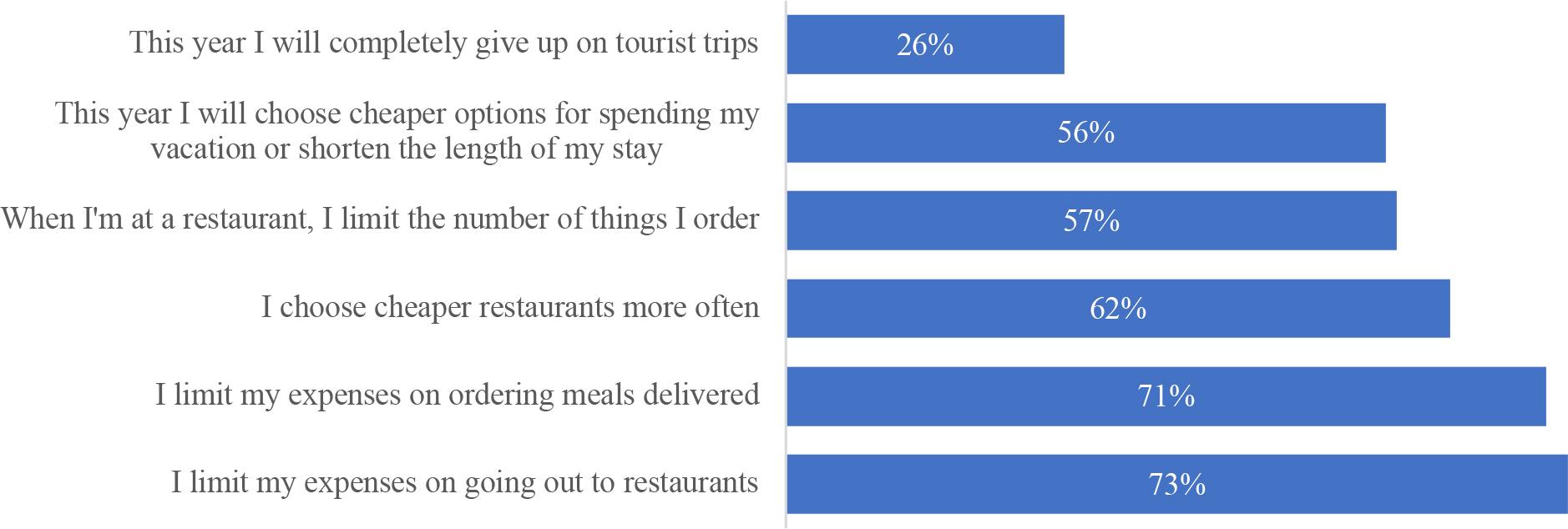

Additionally, economic uncertainty resulting from global crises such as the COVID-19 pandemic and the war in Ukraine has also prompted consumers to cut back on spending. Fears of further price increases and a deterioration in the financial situation in the future have led many consumers to choose cheaper alternatives, even for occasional outings to restaurants. Other consumer attitudes toward the use of catering services are presented in Figure 8.

Attitudes toward the use of catering services in the situation of rising prices in Poland

(Source: Own study analysis based on PMR Market Experts, 2023)

According to the PMR Market Experts Report, 73% of respondents reduced their spending on going out to restaurants, which could suggest that consumers prefer to spend their funds on basic needs, such as food and household fees. The fact that 62% of respondents chose restaurants because of their prices confirms that prices are becoming a key factor in deciding whether to use food services.

As a result, consumers are adapting their behavior to more challenging economic conditions, looking for savings and choosing options that offer the best value for money. A significant number of respondents cannot afford this type of activity, and if they do decide to go out, they choose cheaper options. The increase in the prices of groceries and catering services, supported by inflation, is prompting consumers to make more prudent choices.

This article offers an original synthesis of macroeconomic, sectoral, and behavioral dimensions of change in the Polish food service market. Its novelty lies in combining economic indicators with consumer behavior trends and industry-specific insights from multiple data sources, including recent trade reports and statistical publications. By connecting the effects of two major global crises—COVID-19 and the war in Ukraine—with inflation dynamics and regional variations in food service outcomes, this study presents a unique and multidimensional view of the sector’s transformation. The COVID-19 pandemic and the conflict in Ukraine have had a profound impact on the hospitality sector in Poland, leading to significant operational and financial challenges for business owners. The introduction of numerous restrictions, disruptions in supply chains, and soaring inflation caused a sharp increase in raw material prices and operating costs, forcing businesses to raise prices for gastronomic services. Despite revenue growth, this was primarily the result of price increases rather than an actual rise in sales, highlighting the industry's difficulty in maintaining profitability. The rising prices also altered consumer behavior, as customers increasingly opted for cheaper alternatives or reduced spending on dining services. The conflict in Ukraine further exacerbated the sector's challenges, particularly in the eastern regions of the country.

In the long-term perspective, sustained high inflation may lead to further changes in the structure of the hospitality market. Businesses will need to contend with ongoing challenges related to operational costs and shifting consumer preferences, which will require flexibility and innovation in business approaches. It is possible that the industry will undergo consolidation, where smaller, independent establishments will be replaced by larger chains that are better equipped to cope with cost pressures (García-Madurga, et al., 2021). To survive in challenging economic conditions, hospitality entrepreneurs will need to continuously adjust their operational and financial strategies while seeking new sources of revenue and cost savings. However, it is encouraging that interest in dining and accommodation services is rebounding post-pandemic, and in wealthier societies, there is a noticeable trend toward the “servicization” of consumption.

Practical implications: The results of this study may be of practical use to policymakers, hospitality sector entrepreneurs, and consumer behavior analysts. They provide valuable insights for designing support measures for small and medium-sized enterprises (SMEs) in the food service industry, particularly during periods of economic uncertainty. Entrepreneurs may also use the findings to adapt business models to shifting consumer preferences by diversifying service offerings (e.g., take-out, delivery, dynamic pricing strategies) or by investing in digital solutions to improve operational efficiency.

Limitations of the study: This study is limited by the availability and scope of data, which is predominantly quantitative and aggregated at the national level. Regional nuances and qualitative aspects—such as individual consumer motivations—are not deeply explored. Moreover, due to the rapidly evolving nature of the economic environment, the findings reflect a snapshot of a dynamic and ongoing process.

Directions for future research: Future studies could expand this research by exploring regional disparities in greater detail or by conducting qualitative interviews with restaurateurs and consumers. Further investigation is also recommended into the long-term effects of inflation and geopolitical crises on the structure and resilience of the HoReCa market. Moreover, a comparative study with other EU countries could offer broader insights into how national policy frameworks mitigate or exacerbate sectoral vulnerabilities.