The functioning of the system of environmental fees in Poland requires continuous adaptation to changing economic conditions and development of enterprises - also in terms of innovation, so as to minimize negative environmental impacts. In Poland, even with considerable support from foreign programs for financing projects related to the protection of environment, the system of environmental fees has still remained an important source for funding activities and initiatives in this field.

The aim of the present study was to assess the efficiency of Poland’s system of fees paid in exchange for the use of the environment, in particular the analysis of the system incomes and environmental fee payments by obligated entities, as well as to evaluate the effectiveness of payment control mechanisms and examine the costs related to the maintenance of the environmental fee system.

The study comprised a review of current legal regulations and available data in the literature on environmental fees. The empirical analyses were carried out based on financial data published by Statistics Poland (GUS), the Polish Agency for Enterprise Development (PARP) and the National Centre for Emissions Management (KOBiZE) at the Institute of Environmental Protection - National Research Institute.

The main thesis of this study was the statement that Poland’s system of environmental fees requires modifications in order to increase the efficiency of its functioning. The study methodology consisted of the analysis of normative documents, financial data on revenues as well as costs of the system maintenance. The attempt was made to evaluate the effectiveness of the collection of payments. This article presents the examination of the possibility of introducing full computerisation and digitalisation in public administration units with regard to reporting by entities obligated to pay fees for using the environment.

The results of the analyses carried out confirm the necessity to revise the functioning of Poland’s environmental fee system, to make changes that could eliminate reporting obligations by some entities (especially those small whose activities have a relatively low environmental impact), as well to implement control tasks by the public administration units in authority with regard to fee payments by entities with high environmental impacts. Due to the widespread access to the Internet by both economic entities and administrative bodies, it would be reasonable to introduce the obligation to use only electronic reporting on the use of the environment.

Due to the fact that the efficiency of the environmental fee system has been scarcely discussed in up to date scientific publications, this article brings added value as a contribution to the debate about making changes to the existing system, in order to increase its efficiency as an important source of financing environmental protection in Poland.

The concept of organized taxation existed already in ancient times, nonetheless, environmental taxes gained in popularity merely in the last century. The implementation of economic instruments, such as environmental fees and taxes, was instigated by the recognition of adverse effects of human economic activity on the environment, which ought to be reflected in the prices of goods and services [Rogulski 2014].

Environmental taxes are one of the most commonly used tools to protect the environment and to combat climate change [Miller, Vela 2013; IMF 2019]. The theoretical basis of the environmental tax was first developed by British economist Arthur C. Pigou, and thus it was named Pigouvian Tax [Ciocirlan, Yandle 2003; Shmelev, Speck 2018]. In this context, the often cited example is environmental pollution. The polluter pays principle is the generally accepted practice for making those who produce pollution bear the costs of its management to prevent damage to human health and the environment. The protection of the atmosphere is particularly important, as air pollutants, especially carbon compounds, cause the climate to warm [Hsu 2011; Metcalf 2019].

Among scientific studies on environmental protection, and especially those addressing degradation of the environment, several aspects have been taken into consideration. One of the most important is environmental degradation resulting from economic growth [Grossman, Krueger 1995; Aye, Edoja 2017]. Particularly high environmental pollution is generated at the start of economic development and shows slightly decreasing rates in the advanced development stages when public awareness increases and attempts are made to support environmental protection by introducing rational economy [Grossman, Krueger 1995; Aye, Edoja 2017]. Another important aspect is energy consumption as it was pointed out by Rauf et al. [2018]. The utilisation of energy from different sources is, on the one hand, a result of technological progress and an increase in energy demand for machinery and equipment, and on the other, it is due to the world population growth and an increase in energy consumption by household users. Population growth and changes in lifestyles have resulted in migration of people from rural to urban areas which, inter alia, ultimately has led to adverse effects on the environment, not only through increased consumption, but also, e.g. waste generation. To make matters worse, as a result of globalisation, foreign direct investment [Abdouli, Hammami 2017], trade liberalization [Yasmeen et al. 2018; Yao et al. 2019] and financial markets [Hafeez et al. 2018] have also negatively affected environmental protection efforts. Finally, tourism [Katircioglu 2014; Azam et al. 2018] and income inequality [Hailemariam, Dzhumashev 2020] have to be identified as drivers for environmental impacts.

Already two decades ago, there were held debates on approaches to environmental management. Then raised question addressed improving or changing the three approaches, i.e.: standards and permits, economic instruments and voluntary initiatives [De Freitas, Perry 2012]. Almost 30 years ago, it was argued that regulations and control were more costly than other approaches (OECD 1994). In point of fact, the use of economic instruments, including imposition of environmental charges, need not to apply to all the polluters. To achieve the effect of overall pollution reduction, it seems sufficient to enforce fees, taxes, and environmental permits just with the largest entities. Finally, support for voluntary initiatives could have a more effective and efficient influence on environmental protection. These approaches have been permanently mainstreamed into the political debate. For example, one result of collaborative deliberations on new approaches to environmental protection is the new EU Adaptation Strategy, announced by the European Commission in 2021 [Communication … 2021].

The EU Climate Change Adaptation Strategy addresses the issue that the EU should rely on sufficient funding to cover the costs related to e.g. Climate action (Sustainable Development Goal 13). The implementation of Climate action based on appropriate funding should be consistent with fair taxation that could significantly contribute to Climate action financing and fairly redistributing the gains and costs of the transition. The EU budget and other types of revenue-generating environmental taxation have a significant role to play in this regard [https://www.etuc.org/en/document/etuc-resolution-new-eu-adaptation-climate-change-strategy-world-work].

The action plan called European Green Deal declared by the European Commission, (approved in 2020) aims to transform the EU into a modern, resource-efficient, and competitive economy [https://ec.europa.eu/info/strategy/priorities-2019-2024/european-green-deal_en] by, inter alia, incorporating environmental issues into international tax law, and thereby obligating individual countries to implement the adopted environmental regulations.

In Poland, the system of environmental fees was launched in the 1980s, compliant with the Act of 31 January 1980 on the Protection and Management of the Environment [Act... 1980]. The system has functioned at a national level and originated as a mechanism not related to EU requirements, which is confirmed by the date of bringing the aforesaid act into force. The purpose of the regulation was to make entities pay a tribute for their impact on the environment, allocated to minimize possible hazard and harmful impact sources, as well as to restore the environment through enacting the polluter pays principle.

It is worth noting here that each public contribution is connected with certain requirements and can be e.g. obligatory, of monetary character or nonrefundable. The public tributes are collected by the state with the aim to implement public tasks [Barczak 2016].

The incomes from environmental fees constitute revenues for the system of the environmental protection funds, e.g. the National Fund for Environmental Protection and Water Management (NFOŚiGW), the Provincial Funds for Environmental Protection and Water Management (WFOŚiGW), as well as revenues for the budgets of districts and municipalities. Compliant with the Act of 27 April 2001, The Environmental Protection Law [Act …2001a], these funds are intended to support financing of the tasks aimed at protecting or improving the environment. Furthermore, the loans and grants, as well as other forms of financing provided by the aforementioned funds, are planned first and foremost to subsidize large investments of national and supra-regional importance in the field of elimination of the effects of water, air and land pollution. The activities undertaken in areas such as geology and mining, environmental monitoring, counteracting environmental hazards, nature protection and forestry, dissemination of ecological knowledge, as well as research works and expert opinions are financed from these funds. The aforesaid legal regulations prove that environmental fees can be classified as environmental charges with the dual function, as they include both the incentive aspect (they encourage actions targeted at the protection of environment) and the aspect associated with the distribution of the funds from environmental fees allocated for the implementation of tasks related to environmental protection, and as such they constitute a source of financing projects aimed at reducing impacts due to human activity [Radecki 2011; Woźniak 2013; Draniewicz 2008]. The initial incentive function has lost its importance over time, and relatively low charges imposed on some entities cause that despite the legal obligation to do so, in fact only some entities pay environmental fees, settle liabilities and undertake costly investments associated with environmental protection.

The obligation to pay environmental fees, including those associated with pollutant emissions into the air, was imposed by the Act on the protection and management of the environment [Act...1980]. The system was constructed and launched on the basis of the essential principles taken into account in the Act, and fee rates were to be determined in the executive regulation of the Council of Ministers. Initially, 39 hazardous substances emitted into the air were subject to charges. Originally, the fees were fixed and collected by local public administration authorities on the basis of statements on air pollutant quantities submitted by entities (each year, until 30 January, for the preceding year). Consistent with the provisions in the Act, the charges were imposed on entities with required environmental permits for air pollutant emissions. It was not until the year 1986 that the Regulation of the Council of Ministers of 13 January 1986 on fees for economic use of the environment and introducing changes to the environment [Regulation... 1986] expanded the list of entities obligated to pay environmental fees to also comprise organizational units and individuals conducting business activities, including those who did not have the aforesaid environmental permits. In the Regulation, there also emerged a fee threshold (10 000 PLN/year — the amount before the denomination of 1995), up to which the fee was not charged. At the same time, subjective exemptions were included (social welfare institutions, orphanages and educational care centres).

In 1989, during the work on amendments to the Act on the protection and management of the environment [Act …1980], the period of collection of fines was limited to 5 years. This rule is still in force.

The Regulation of the Council of Ministers [Regulation… 1986] was amended in 1990, and the responsibility as regards environmental fees was transferred to the voivodes (provincial governors) who were authorised to require submission of the statements by entities for 6-month periods.

In 1991, during the works on further amendments to the Regulation of the Council of Ministers [Regulation…1986], there was established a list of entities exempted from charges as of 1992 that included health and social care institutions, orphanages, educational care centres, cultural-educational institutions, prison and correctional institutions, and juvenile shelters [Regulation…1991]. At that time, there were finally determined environmental fee rates for the introduction of air pollutants resulting from gasoline handling (per 1 ton of gasoline handled). This level of pollutants was related to EU requirements for the reduction of emissions of volatile organic compounds into the atmosphere [Directive... 1991].

In 1993, the Act on the protection and management of the environment [Act …1980] was amended to enable voivodes to charge quarterly fees based on entity statements on pollution submitted by 15th day of the month following the end of each quarter (in spite of the valid requirement for submission of entities’ annual statements by 30 January of the following year).

The mechanism for calculation of environmental fees independently by entities was introduced in 1998, with adoption of the Act of 29 August 1997 amending the Act on the Protection and Management of the Environment and amending certain acts [Act…1997]. At that time, the obligation was also imposed on one and all to pay fees on a quarterly basis. In 1999, the amended Regulation of the Council of Ministers specified the fee rates for air emissions, and originally determined separate fee rates as regards fuel combustion processes (depending on heat efficiency of the source and the type of fuel) as well as unit rates of charges for air pollutant emissions from fuel combustion processes in internal combustion engines (depending on the type of engine and the type of fuel combusted). At the same time, in 1997 and 1998, the list of entities exempted from fee payments for the introduction of pollutants into the air was expanded to, inter alia, kindergartens, libraries, universities, theological seminaries and prison service organisational units.

The subsequent legislation, the Act of 24 July 1998 on amending certain acts regulating competencies of the authorities of public administration bodies [Act... 1998], took away the tasks and responsibilities as regards environmental fees assigned thus far to voivodes, and the Marshalls of the newly created provincial governments were authorised in this respect.

The Act of 27 April 2001, The Environmental Protection Law [Act … 2001a] repealed the Act on the protection and management of the environment [Act …1980] but maintained the principle that entities using the environment should calculate fees on a quarterly basis and transfer payments to the accounts of the Marshall Offices responsible for fee collection. At the same time, e.g. the individuals who were not entrepreneurs and required an environmental permit were obliged to pay fees related to the use of the environment. In this Act, there were originally determined the upper unit fee rates. There was also endorsed the principle that the rates were to be increased each year as of 1 January, taking into account the annual average consumer price index for goods and services as adopted in the budget act for the preceding year. The rates for the next year were to be announced at the latest by 31 October of the preceding year. An important change then introduced was exempting some entities (e.g. schools, libraries, etc.) from paying fees for the use of the environment. However, there still remained the quota exemptions, depending on the lowest remuneration for employees.

In 2003, The Environmental Protection Law [Act …2001a] was amended by setting the threshold amount at which entities were exempted from paying fees: 200 PLN per quarter. In 2005, it was decided to amend the law with an obligation to pay environmental fees on a semi-annual basis, by the end of the month following each half-year-period. Therefore, the threshold amount exempting entities from fee payments was raised to 400 PLN per 6 months.

As of 1 January 2013, the obligation was imposed on entities to submit annual statements and pay the environmental fee for the preceding year by 31 March of the following year. The level at which entities were exempted from paying the fee was maintained and remained in effect for those whose annual fee did not exceed 800 PLN. Another important change was introduced as of 1 January 2017, when entities using the environment were exempted from submitting the statements to both the Marshall Offices and provincial environmental protection inspectorates, if their annual fee did not exceed 100 PLN.

As of 1 January 2018, charges for water abstraction and sewage pollution were excluded from the main catalogue of environmental fees, which was a result of changes associated with the adoption of the Water Law Act [Act... 2017]. The responsibility with respect to applicable fees for water abstraction and release of sewage into waters and soils was passed to the State Water Holding – Polish Waters (Wody Polskie). As a result, voivodships, municipalities, and districts were deprived of revenues from fees for water abstraction and wastewater pollution. Under the provisions of the Water Law Act, the National Fund for Environmental Protection and Water Management (NFOŚiGW) currently receives 90% of its income from environmental fees for environment pollution due to wastewater release.

Effective environmental fee rates for the year 2021 were set through an announcement by the Minister of Climate on 9 September 2020 on the rates of environmental fees for the year 2021 [Announcement ….2020]. Entities may submit their paper or electronic statements. Presently, paper statements are more commonly submitted.

In view of the above, it can be concluded that Poland’s system of environmental fees has indeed undergone several legislative changes of administrative, organizational and functional nature.

At the time of publication of the results of this study, the issues related to environmental fees are sanctioned by The Environmental Protection Law in Title V. According to the definition, the environmental fee is a financial and legal measure for environmental protection and is paid in connection with the following:

- –

introduction of gases or particulate matter into the air,

- –

emission allowances,

- –

waste disposal.

The revenues from fees for using the environment constitute incomes in the budgets of the Funds for Environmental Protection and Water Management at the national and voivodship (province) levels, as well as support the budgets of districts and municipalities.

The Environmental Protection Law clearly specifies that entities using the environment, domestic and foreign entrepreneurs, persons engaged in production activities in the agricultural sector and non-entrepreneurial entities are required to pay environmental fees. Persons who are not entrepreneurs also have to pay environmental fees, depending on the scope of undertaken activities which require a permit for releasing substances or energy into the environment.

Consistent with the rates in force in the period in which the use of the environment took place, the amount of the environmental fee due is determined by obligated entities and paid by 31 March of the following year, into the account of the responsible Marshall Office. Importantly, compliant with The Environmental Protection Law [Act....2001a], the Tax Ordinance Act [Act …1997] Section III, shall apply to environmental fees and administrative penalties, and the Marshall of a given voivodship or the regional environmental protection inspector have authority in this area. In addition, the Marshalls have the authority to levy a fee if the entity fails to submit the statement due or submits discrepant data or does not make the payment.

The Environmental Protection Law [Act …2001a] does not provide for any entity-based exemptions; nonetheless, it specifies the amount-based exemptions, under which entities pay no environmental fees for introducing gases or particulate matter into the air, as long as their annual fee does not exceed 800 PLN. If the annual fee for each type of use of the environment does not exceed 100 PLN, the entities submit no statements. The entities who use the environment without the obligatory permit for releasing gases or particulate matter into the air have to pay the environmental fee increased by 500%.

Moreover, as of 1 January 2020, the data included in environmental fee statements for air pollution submitted to the Marshall Offices should be determined based on the volume of annual emissions reported by the entities to the National database on emissions of greenhouse gases and other substances (first statements concerned the use of the environment in 2019). This solution is intended to ensure consistency of submitted and reported data on air emissions as well as to improve data quality.

As stated above, compliant with the law, the Marshall Offices are responsible for all the tasks related to keeping records on environment use, controlling fee calculations and payments, enforcing arrears, and redistributing fee revenues. Environmental fees are recorded in the accounts of the Marshall Offices and then reallocated to, among others, the accounts of districts and municipalities. Since 2018, the issues of fees for water abstraction and wastewater pollution have been regulated by the Water Law Act [Act…2017] and the State Water Holding – Polish Waters (Wody Polskie) is the authority who has taken over these responsibilities.

Compliant with the Act of 29 June 1995 on Official Statistics (Act... 1995), the environmental fee system is subject to reporting to Statistics Poland (GUS) who carries out the statistical surveys promulgated by the Prime Minister, the results of which are official statistical data presented in the statistical yearbooks. The environmental fee system reports used to be included in the yearbooks “Economic Aspects of Environmental Protection”, and now are presented in the yearbooks “Environmental Protection”. Consistent with GUS, environmental fee revenues in the years 2003–2020 are presented in the following four categories:

- –

wastewater management and water protection,

- –

atmospheric air and climate protection, CO2 emissions,

- –

waste management,

- –

other areas and other receipts, including among others: interest for overdue payments, recovered costs of enforcement proceedings, and erroneous refundable payments [Statistics of Poland (GUS): Economic... 2019–2020; Statistics of Poland (GUS): Environmental Protection... 2003–2020].

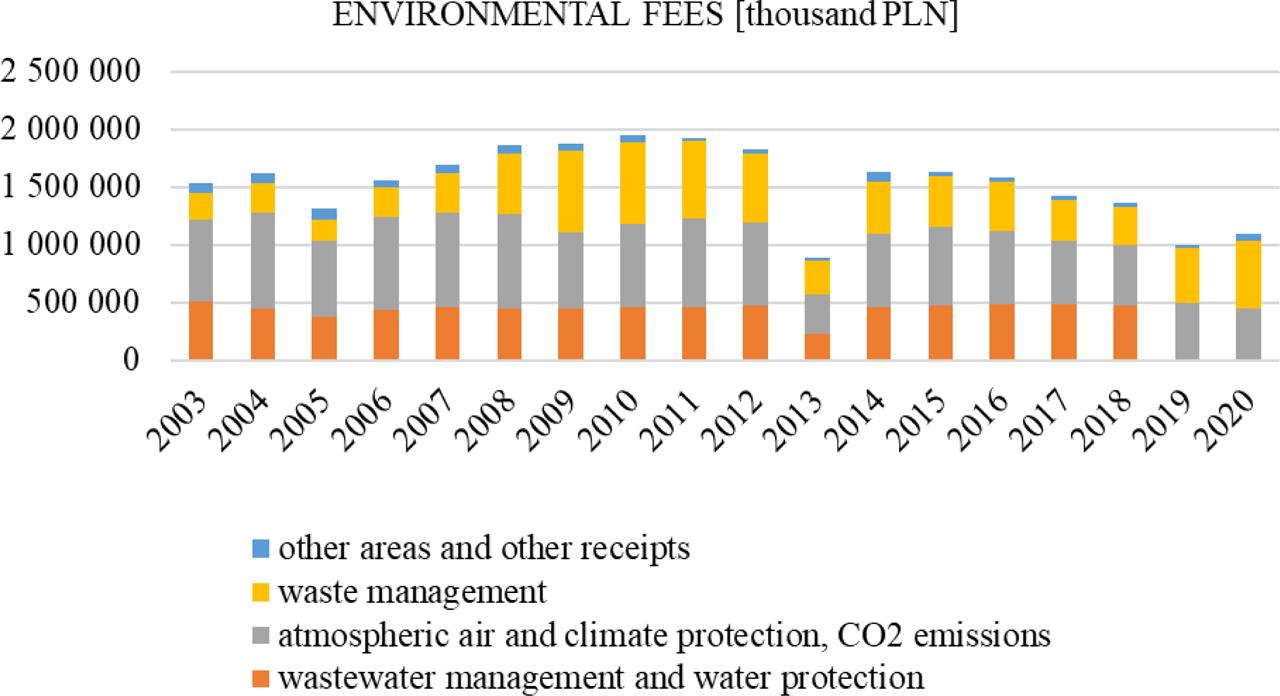

Comprehensive information on environmental fee revenue streams in the years 2003–2020 is presented in Figure 1.

Revenues from environmental charges in Poland in 2003–2020

Source: Authors’ own elaboration based on GUS data: GUS data: Economic... [GUS 2019–2020] and Environmental Protection... [GUS 2003–2020]

* As of 1 January 2013, there was introduced the obligation to submit statements on an annual basis and to pay the fee for the preceding year by 31 March of the following year, which resulted in the revenue shift

** The decrease in revenues, starting from 2019 (fees for 2018 were paid in 2019), in the category: wastewater management and water protection is a consequence of implementation of the Water Law and the takeover of fees by the State Water Holding – Polish Waters (Wody Polskie)

The responsibility for keeping data records on the use of the environment as well as for the system operation is held by the Marshall Office. At present, each of the 16 Offices maintains its own database, which is a separate IT system collecting information on the system of fees for using the environment and other relevant information. These databases are built by external companies hired by the Offices. The paper statements are still predominantly submitted by entities, which results in an additional workload for the Office employees, as they have to enter manually the statement data into the electronic system, even though their worktime could be used for verification of the data submitted by entities. The databases separately maintained by all the Offices have not been integrated at a central level, which significantly hinders access to information at a national level.

Revenues from environmental charges in Poland, in the period 2003–2020

| Year | FEE CATEGORY (thousand PLN) | Total [thousand PLN] | % y/y | |||

|---|---|---|---|---|---|---|

| Wastewater management and water protection | Atmospheric air and climate protection, CO2 emissions | Waste management | Other areas and other receipts | |||

| 2003 | 512 187.90 | 700 243.20 | 232 011.30 | 90 158.20 | 1 534 600.60 | - |

| 2004 | 443 026.90 | 834 926.60 | 249 600.30 | 90 405.00 | 1 617 958.80 | 5% |

| 2005 | 375 158.20 | 652 633.70 | 189 204.70 | 99 700.30 | 1 316 696.90 | −19% |

| 2006 | 438 779.90 | 802 906.50 | 260 911.80 | 51 546.40 | 1 554 144.60 | 18% |

| 2007 | 457 870.00 | 823 848.50 | 341 171.10 | 65 649.80 | 1 688 539.40 | 9% |

| 2008 | 449 280.00 | 817 250.50 | 522 010.50 | 68 855.00 | 1 857 396.00 | 10% |

| 2009 | 448 949.20 | 655 694.60 | 705 979.30 | 63 412.40 | 1 874 035.50 | 1% |

| 2010 | 456 589.90 | 721 388.70 | 714 576.10 | 51 609.00 | 1 944 163.70 | 4% |

| 2011 | 463 468.60 | 763 906.20 | 671 394.60 | 20 996.60 | 1 919 766.00 | −1% |

| 2012 | 470 750.70 | 724 002.70 | 595 964.50 | 34 748.10 | 1 825 466.00 | −5% |

| 2013* | 227 922.80 | 342 784.50 | 287 220.00 | 29 464.00 | 887 391.30 | −51% |

| 2014 | 459 819.30 | 640 200.00 | 450 435.50 | 76 692.70 | 1 627 147.50 | 83% |

| 2015 | 476 361.30 | 673 334.30 | 443 775.50 | 35 692.50 | 1 629 163.60 | 0% |

| 2016 | 487 585.70 | 631 878.70 | 431 022.10 | 35 760.80 | 1 586 247.30 | −3% |

| 2017 | 488 685.40 | 545 845.30 | 350 397.00 | 34 998.30 | 1 419 926.00 | −10% |

| 2018 | 467 745.80 | 532 734.70 | 330 561.40 | 35 930.00 | 1 366 971.90 | −4% |

| 2019 | 2 547.40** | 492 428.00 | 475 199.40 | 30 165.50 | 1 000 340.30 | −27% |

| 2020 | 1 278.00** | 451 708.10 | 576 689.90 | 68 774.30 | 1 098 450.30 | 10% |

Source: Own elaboration based on GUS data: Economic... [GUS 2019–2020] and Environmental Protection... [GUS 2003–2020]

As of 1 January 2013, there was introduced the obligation to submit statements on an annual basis and to pay the fee for the preceding year by 31 March of the following year, which resulted in the revenue shift

The decrease in revenues, starting from 2019 (fees for 2018 were paid in 2019), in the category: wastewater management and water protection is a consequence of implementation of the Water Law and the takeover of fees by the State Water Holding – Polish Waters (Wody Polskie)

The data obtained from the Marshall Offices in 2021 show that the number of entities paying environmental fees has been decreasing in the recent years, as illustrated by Table 2. The available information obtained from the Marshall Offices is presented.

Number of entities [thousand]* in Poland’s system of environmental fees in 2015–2019**

| Year | Overall number of entities including < 100 PLN | Number of entities > 100 PLN * | Number of entities exempted from the obligation to pay fees payments range: 100 PLN to 800 PLN | Number of entities obligated to pay fees: above 800 PLN |

|---|---|---|---|---|

| 2015 | 193 | 164.1 | 28.8 | |

| 2016 | 103 | 90.4 | 45.4 | 45 |

| 2018 | 95,9 | 89.6 | 58.4 | 31.2 |

| 2019 | 86,9 | 82 | 52.4 | 29.6 |

Source: Own elaboration based on data obtained from the surveyed Marshall Offices, compiled by KOBiZE IOŚ-PIB

The presented data refers only to the entities submitting information on gas or particulate matter emissions into the air, the number of which is basically equivalent to the total number of entities paying environmental fees, due to the specificity of the categorization of environmental use with reference to the air (e.g. operation of vehicles).

No surveys were conducted in 2017

The results presented in Table 2 prove that the solutions applied in different ways reflect the numbers of entities included in the system. For example, the exemption introduced in 2017, from submission of the environmental fee statements in the case of charges below 100 PLN/year for a given component (e.g., air emission, waste) has relieved many entities of the obligation to prepare and submit the fee statement. On the other hand, however, such a solution is a burden for the charging bodies, as it requires a number of verification and control activities to: identify the entity and determine whether it actually uses the environment - if so, to find out to what extent and whether a calculated fee is below 100 PLN and, accordingly, to verify whether the entity is in fact exempted.

The revenues in the category of wastewater management and water protection show a stable trend (excluding 2013, 2019 and 2020); the average contribution to the budget amounted to 460 million PLN.

In the category: air protection, the average revenue for the period of 2003–2020 amounted to over 655 million PLN; nonetheless, in the recent years (since 2015), it has shown a downward trend. In 2020, the revenues amounted to approximately 452 million PLN, which resulted, among others, from actions taken by large plants as part of their adaptation to environmental requirements imposed by the EU.

The income from waste management, the category with considerable revenue fluctuations, developed differently. The average revenue in the last eighteen years was over 430 million PLN, and the highest revenue was recorded in 2009 and 2010 (over 700 million PLN). In the years 2019–2020, there was observed an average annual increase in fee payments of over 30% year-on-year. In 2020, nearly 580 million PLN constituted revenue for the budgets.

In the category: other areas and other receipts, the revenues did not exceed the threshold of 5% of the revenues identified in the study period. The results of the analyses carried out under this study showed considerably higher total revenues from environmental fees in the period of 2010–2018, i.e. before the State Water Holding – Polish Waters (Wody Polskie) had taken over part of the payments. Afterwards, the revenues decreased by as much as 30% when compared to the highest environmental fee revenue attained earlier. Many factors have contributed to the decrease in revenues, and one of the most important is the lack of adequate control capabilities. For organizational and financial reasons, it is impossible to verify all the entities that should pay fees. The reverse charge approach applied has made the leakage of the system highly dependent on control and verification activities undertaken by the authorities responsible for charging environmental fees. As a result, the decreasing value of revenues is largely a consequence of the decreasing number of entities paying fees.

Consistent with the act, The Environmental Protection Law [Act... 2001a], the revenues from fees for using the environment paid to the Marshall Offices are distributed to:

- –

the National Fund for Environmental Protection and Water Management (NFOŚiGW),

- –

Provincial (Voivodeship) Funds for Environmental Protection and Water Management (WFOŚiGW),

- –

municipality budgets,

- –

district budgets.

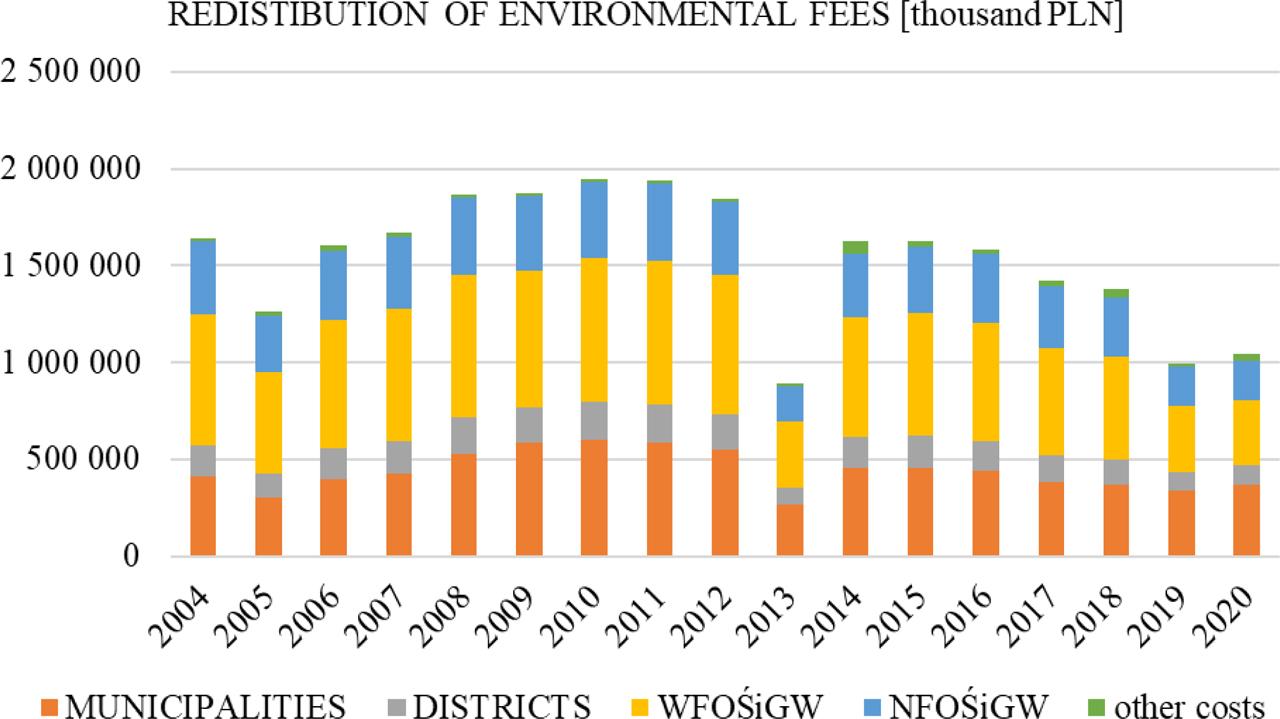

Environmental protection funds used to be handled by municipalities and districts who granted subsidies, however, they lacked legal enforcement power. The provisions of the Environmental Protection Law [Act... 2001a] also refer to allocation of part of the funds to cover other costs related to the functioning of the environmental fee system. This aspect is discussed in the following sections of this paper. How the funds were distributed in the period of 2004–2020 is shown in Table 3 and Figure 2. Since 2010, the reallocation of environmental fees to municipalities and districts has shown a downward trend, starting in 2011 in the case of WFOŚiGW and NFOŚiGW. The results obtained show that the redistribution of revenues from environmental fees in 2010–2018 decreased by almost 30%, which is an expected consequence of changes in the volume of revenues from fees.

Redistribution of the environmental fees in Poland in 2004–2020

| Year | Municipality | District | WFOŚiGW | NFOŚiGW | Other costs | Total [thousand PLN] | Change % y/y |

|---|---|---|---|---|---|---|---|

| [thousand PLN] | |||||||

| 2004 | 410 949.90 | 162 286.00 | 676 142.40 | 373 407.30 | 17 630.10 | 1 640 415.70 | - |

| 2005 | 306 552.90 | 122 924.50 | 523 431.70 | 291 474.80 | 21 780.50 | 1 266 164.40 | −23% |

| 2006 | 399 688.00 | 159 032.90 | 660 908.30 | 356 433.90 | 27 945.20 | 1 604 008.30 | 27% |

| 2007 | 427 103.40 | 165 279.50 | 685 662.30 | 369 976.60 | 23 387.20 | 1 671 409.00 | 4% |

| 2008 | 531 456.40 | 185 879.80 | 737 148.10 | 396 956.00 | 17 622.70 | 1 869 063.00 | 12% |

| 2009 | 584 042.40 | 185 594.80 | 706 018.40 | 380 187.20 | 19 988.30 | 1 875 831.10 | 0% |

| 2010 | 604 028.30 | 195 271.10 | 740 374.40 | 390 752.10 | 12 775.80 | 1 943 201.70 | 4% |

| 2011 | 587 639.70 | 193 016.10 | 744 797.20 | 398 037.70 | 12 531.70 | 1 936 022.40 | 0% |

| 2012 | 549 774.30 | 183 290.30 | 715 313.30 | 382 438.90 | 13 869.80 | 1 844 686.60 | −5% |

| 2013 | 265 007.60 | 87 973.00 | 342 315.20 | 182 895.20 | 14 401.30 | 892 592.30 | −52% |

| 2014 | 454 377.10 | 158 784.00 | 616 996.40 | 330 236.10 | 68 102.00 | 1 628 495.60 | 82% |

| 2015 | 459 001.00 | 162 158.00 | 637 106.20 | 341 031.40 | 30 164.60 | 1 629 461.20 | 0% |

| 2016 | 441 843.00 | 155 608.80 | 609 519.00 | 352 311.60 | 25 692.80 | 1 584 975.20 | −3% |

| 2017 | 384 592.60 | 139 264.10 | 552 792.50 | 316 015.70 | 26 964.50 | 1 419 629.40 | −10% |

| 2018 | 367 471.10 | 133 504.90 | 531 999.30 | 303 621.60 | 44 383.00 | 1 380 979.90 | −3% |

| 2019 | 337 555.60 | 96 798.90 | 340 488.70 | 200 876.60 | 19 037.50 | 994 757.30 | −28% |

| 2020 | 368 319.00 | 100 485.50 | 339 331.60 | 198 181.00 | 35 975.40 | 1 042 292.50 | 5% |

Source: Own elaboration based on GUS data from annual reports of Environmental Protection-4-year-period and GUS data from Economic…. [GUS 2019–2020] and Environmental Protection [GUS 2004–2020]

As of 1 January 2013, there was introduced the obligation to submit statements on an annual basis and to pay the fee for the preceding year by 31 March of the following year, which resulted in the revenue shift

Redistribution of the environmental charge in Poland, in the period 2004–2020

Source: Own elaboration based on data from annual reports EO-4/yr. (received from GUS) and based on GUS data published in Economic... [GUS 2019–2020] and Environmental Protection... [GUS 2004–2020]

* As of 1 January 2013, there was introduced the obligation to submit statements on an annual basis and to pay the fee for the preceding year by 31 March of the following year, which resulted in the revenue shift

Under the framework of the environmental fee system, the predicted costs related to the implementation of legally due fees are related to creating and updating databases with information on entities using the environment, employing persons responsible for registration of the entity statements as well as controlling and collecting environmental fees.

These costs are covered to a large extent from fee revenues, as since 2014, compliant with The Environmental Protection Law, before transferring the funds to NFOŚiGW and WFOŚiGW accounts, the Executive Boards of Voivodships have been reducing them by:

- –

3% in the case of voivodships where the revenue from environmental fees paid in the preceding calendar year were up to 100 million PLN;

- –

1.5% in the case of voivodships where the revenue from environmental fees paid in the preceding calendar year exceeded 100 million PLN.

Variability in the amount of redistribution costs in 2010–2020 is presented in Table 4.

Costs of redistribution of environmental fee revenues in Poland in 2010–2020

| Year | Costs related to payment enforcement | Costs related to bank account maintenance | Costs related to transfer of repayable contributions | Costs related to interest on overdue fee payments | Fees due to the Marshall Offices | Other costs | Total costs |

|---|---|---|---|---|---|---|---|

| [thousand PLN] | [thousand PLN] | ||||||

| 2010 | 657.80 | 2.10 | 11 090.60 | 0.00 | 968.00 | 57.30 | 12 775.80 |

| 2011 | 544.00 | 1 884.00 | 7 992.60 | 0.00 | 1 600.80 | 510.30 | 12 531.70 |

| 2012 | 768.70 | 0.90 | 11 629.90 | 0.00 | 1 419.80 | 50.50 | 13 869.80 |

| 2013 | 413.50 | 0.60 | 12 880.80 | 0.00 | 1 067.00 | 39.40 | 14 401.30 |

| 2014 | 366.70 | 0.40 | 42 913.40 | 0.00 | 24 750.70 | 70.80 | 68 102.00 |

| 2015 | 501.90 | 0.40 | 8 296.30 | 0.00 | 20 936.20 | 429.80 | 30 164.60 |

| 2016 | 200.80 | 0.20 | 5 578.90 | 0.00 | 19 882.90 | 30.00 | 25 692.80 |

| 2017 | 139.90 | 0.00 | 8 436.80 | 0.00 | 18 334.20 | 53.60 | 26 964.50 |

| 2018 | 256.30 | 0.10 | 26 367.10 | 0.00 | 17 719.60 | 39.90 | 44 383.00 |

| 2019 | 173.10 | 0.10 | 7 380.20 | 0.00 | 11 465.50 | 18.60 | 19 037.50 |

| 2020 | 160.60 | 0.10 | 21 139.70 | 0.00 | 14 652.90 | 22.10 | 35 975.40 |

Source: Own elaboration based on the unpublished GUS data obtained from annual reports OŚ-4/r. and published GUS data: Economic... [GUS 2019–2020] and Environmental Protection... [GUS 2010–2020]

The GUS data analysed can be divided into two categories:

- 1)

costs, which include:

- –

costs related to payment enforcement,

- –

costs related to bank account maintenance,

- –

fees due to the Marshall Offices.

- –

- 2)

expenses, which include:

- –

expenditures for transfer of reimbursable payments,

- –

expenditures related to interest on overdue payments of fees,

- –

other expenses.

- –

In 2020, the total cost amounted to 15 million PLN. The cost breakdown analysis shows that in the recent years, the costs related to payment enforcement and those related to bank account maintenance remained at a very low level in relation to the total costs and amounted to only 0.01% of the total costs. At the same time, the fees due to the Marshall Offices, received for operation of the environmental fee system. constituted the largest portion (just about 100%) in the total cost analysed. However, in 2020, the total expenditures amounted to 21 million PLN, and these did not support activities targeted at the system operation but served regulation of financial flows in the fee system.

As said above, the system of environmental fees was launched in Poland in 1980, i.e. much earlier than Poland accessed the European Union (2004). Despite numerous modifications over the last 40 years, the system has been fulfilling its role, notwithstanding the changes in the political system and new tasks emerging in the area of environmental protection.

When implementing the tasks focused on environmental protection, it is important to ensure appropriate financial outlays. Otherwise, the implementation of environmental goals would be less effective or even impossible. In the subject literature, the term efficiency refers mainly to maximising profits with the least possible outlays. In other words, actions will have the attribute of efficiency only when they are characterized by efficacy, profitability and cost-effectiveness (economy) [Walkowiak 2011]. A similar concept of efficiency usually refers to the principle of rational management formulated on the basis of two variants: efficiency (maximization of the effect) and economy (minimization of the outlay) [Matwiejczuk 2000]. The benchmarking is defined correspondingly and refers to the evaluation of management performance through the use of comparative analysis, which must focus on the most important factors affecting the company’s efficiency, i.e. the factors that facilitate the performance of the tasks for which the organization was established [Bramham 2004].

It is worth citing the authors who point out that the lack of competition and sanctions imposed on public administration may result in putting too little emphasis on increasing the efficiency, which, therefore, cannot be improved through enhanced coordination of the entire system [Niedbała, Sierpińska 2003]. Bearing the above in mind, it is necessary not so much to exert pressure but to emphasize of the need to increase the fee system efficiency which will ultimately improve environmental protection.

The results of the analysis of the costs of system maintenance show considerable expenditures on IT activities, yet the use of information technology alone does not lead to the success in business or in social and economic life. Higher and higher expenditures on digitalisation do not translate into a distinct increase in the productivity of employees, companies, industries or entire economic systems. Actually, given the results of statistical data analysis, the contrary conclusion is called for - there is no correlation between expenses on IT and measurable indicators of productivity. This situation is referred to as “the productivity paradox” [Dudycz, Dyczkowski 2006].

As a final point, the efficiency can be defined as the ratio of the outcomes to the expenditures incurred to achieve them [Jaruzelski 2009]. This definition of efficiency should lead us to analyse all the costs of the environmental fee system.

When assessing the efficiency of the environmental fee system, it seems natural to analyse the value of generated revenues and their distribution, as well as the costs of maintaining the system. It should be noted that in the case of environmental protection undertakings, the fee system is assessed in relation to the state of environmental protection, and also with reference to financial or material outlays. The legislature introduced numerous restrictions and explicatory elements, the purpose of which was to ensure, on the one hand, appropriate generation of financial resources and, on the other, restrictive policies regarding the valid standards and quantities of substances emitted to the environment as a result of its use.

Poland’s system of environmental fees has been modified several times. The analysis of the course of changes since launching of the system shows that modifications have been made at various levels, e.g. subject-based exemptions were established (later abandoned) and the flat-rate system for fee calculations was introduced without specification of pollutant emissions into the air. This shows that the system of environmental fees has been continuously developed and shaped by the ministry responsible for environmental issues. The analysis indicates, however, that regardless of various measures taken to rationalise the fee system, e.g. through:

- –

switching from quarterly to half-yearly, and finally, to yearly statements submitted by entities using the environment,

- –

exemption from fees for emissions as a result of rescue operations,

- –

exemption from submitting the fee statement if a given fee component does not exceed PLN 100/year,

When analysing revenues from environmental fees, it can be seen that the fees show a downward trend. Does this mean that the environmental impact of entities using environmental resources is decreasing? Without doubt, it can mean greater socio-economic awareness of the entities, expressed in their actions for environmental protection and, thus, minimizing the costs of using the environment.

In contrast, in the recent years, an indisputable increase has been observed in the category “other costs”, mainly related to the payments due to the Marshall Offices. This category includes the costs of operation of the fee systems established at the Offices, which entail the costs of consumption of materials and energy, external services, salaries together with social insurance contributions and other costs.

Regrettably, reports by GUS are partial in this respect and no detailed data on particular cost categories are available. Bearing the above in mind, the issue would require a separate analysis of the group “other cost”, as well as a comprehensive assessment of the functioning of this very segment of the environmental fee system.

The analysed revenue stream shows an evident downward trend. There are more than 2 million enterprises in Poland [PARP 2021]. Industrial and construction activities are carried out by 25% of the total number of enterprises, i.e. by over 500 thousand entities. The number of enterprises paying fees remains at a level of about 30 thousand, which equals less than 1.4% of the total number of relevant enterprises. Assuming that enterprises involved in industrial or construction activities use the environment most intensively, the number of entities that currently pay environmental fees (30 thousand PLN) seems somewhat low.

The Marshall Offices do not have much legal, organizational, or financial capacity to carry out detailed inspections of entities and to confirm that the polluter pays principle is followed. It seems impossible to audit all the companies, but certainly better control tools could contribute to tightening the system and increasing revenues from environmental charges.

On the other hand, the growing costs of maintaining the fee system are alarming. In the recent years, there has been a significant increase in costs, which combined with falling revenues makes the fee system less efficient.

As discussed above, the system of environmental charges has been operating in Poland for over 40 years. It is obvious that during this period, numerous modifications and improvements have been implemented and have contributed to the development of the current model of operation. This, in turn, affects the costs related to the functioning of the fee system. Yet, system operation costs have been recently increasing, mainly due to increasing salaries of office staff and, especially, IT employees. These circumstances may lead to a further increase in the costs of the fee system functioning and ultimately reduce its efficiency.

As Statistics Poland (GUS) pointed out, in 2020, when the world was overwhelmed by the pandemic, the use of digital technologies played a very important role and facilitated the functioning of society in many aspects of life. The rapid flow of information about the current situation enabled both authorities and enterprises to react immediately and to take key decisions on health care and functioning of economy in this exceptional situation [GUS 2020].

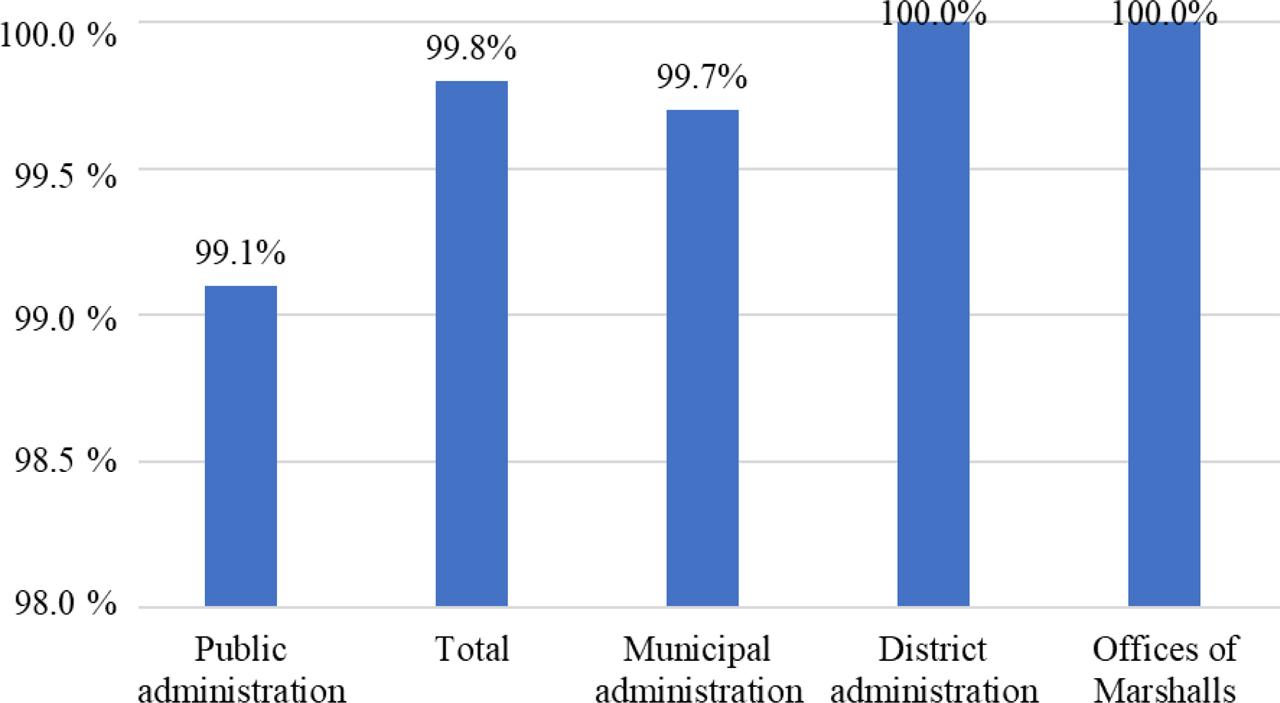

The COVID-19 pandemic, ongoing since 2020, may paradoxically reduce the cost of operation of the environmental fee system. Only a few years ago, the implementation of electronic tasks in the area of public administration seemed unattainable, likely to prove impossible. Even though digital services were offered by all the Marshall Offices, and as of 2019, the share of public administration units with fixed-line broadband Internet access was 99.8%, electronic solutions were not widely used. Improved access to the Internet gives opportunities for computerization of the environmental fee system. Earlier, both businesses and households did not use electronic communication and data exchange with public administration bodies readily, even having access to the Internet. Then again, access to the Internet through a fixed line established in public administration units is very high, reaching 100% in some offices. Detailed data on access to the Internet in public administration units is presented in Figure 3.

Government entities with fixed-line broadband Internet access by entity type (data for 2019) Source: GUS, Society … [GUS. 2020]

Poland’s activities in support of information technology and development of electronic administration were determined under the framework of a newly established government administration area, i.e. informatisation. The provisions for the latter were set in the Act of 21 December 2001 on amending the act on the organisation and work mode of the Council of Ministers and the scope of action of ministers, the act on government administration departments and amending some acts (effective as of 2002) [Act ….2001b].

The introduction of informatisation is part of the implementation of the National Integrated Informatisation Programme aimed at putting into effect the use of modern digital technologies related to public administration. The Program was originally introduced in 2017 as part of the Strategy for Responsible Development until 2020, which after the evaluation in 2018, was updated to be implemented in 2019–2022 (with the perspective of 2030). It should be recapped that as late as 2007, more than 83% of public administration units in Poland did not have any IT systems for handling public procurement [ARC Rynek i Opinia 2008]. The Polish legal system which was not adjusted for providing electronic administration services, as well as the lack of incentives for the society to use electronic administration services were pointed out by public officials as the principal factors in the delay of implementation of IT solutions [Lisiak-Felicka 2009].

It was not until the COVID-19 pandemic that a breakthrough in the implementation of electronic communication occurred. This was mainly due to the fact that then obligations of an administrative nature had to be fulfilled with instantaneous constraints on interpersonal contacts and limited possibilities for communicating through traditional means for exchange of documents.

The turning point was a new very important change in the implementation of the Public Procurement Law [Act …2019], effective as of January 2021. Since 2017, the legislature has introduced partial changes related to IT implementation in certain entities. The full computerisation of procurement procedures for all contracting authorities and all procurement types was initially supposed to be effective as of 1 January 2020. However, as a result of the amendment to the Public Procurement Law, full computerisation of public procurement was postponed until 1 January 2021. Thus, only the pandemic and problems with traditional documentation flow as well as the amendment to the Act [Act …2019] launched fully electronic procurement procedures. In practice, contracting authorities had to pick out a system for conducting electronic proceedings, with a choice between commercial platforms or a free of charge tool provided by the Public Procurement Office, i.e. a mini-portal and the e-Procurement Platform. Through these systems it is possible to communicate during the proceedings and submit offers. Documents and statements submitted must be signed with a qualified electronic signature, in the case of the proceedings that exceed “EU thresholds”. In the case of proceedings that do not exceed these thresholds, the documents and statements can be signed with a trusted or personal signature. In practice, the contractors have been forced to set up and use one of these signature types. Due to the change in the way of communicating during the proceedings, it was necessary to introduce new legal regulations as regards the form of submitting obligatory statements and documents, technical requirements for electronic documents, electronic communication means and minimum requirements for ICT systems. The ordering parties have to take all these changes into account in their proceedings by introducing appropriate provisions in the documents.

Such remarkable changes in the area of public procurement would not have been possible without already existing widespread usage of information technology and technological capabilities by both businesses and state entities. On the other hand, the introduction of such changes was possible because of the willingness of employees working in each area of the state functioning and the implementation of numerous laws streamlining the electronic circulation of documents, reports, and information.

On the basis of to date experience with computerisation, as well as taking advantage of the pandemic situation in terms of electronic exchange of information, it seems logical to switch to electronic procedures in the system for reporting and processing data related to fees for the use of the environment with respect to the fee statements currently submitted mainly in writing. Replacing paper statements with electronic statements, entered by the entity directly into the dedicated IT system, would contribute to reducing the costs of the fee system operation and improve system management efficiency. The electronic statements would enable fast detection of discrepancies and errors (e.g. by the implementation of checking algorithms), as well as quick communication between the office and the entity, which would be a great added value. Thanks to computerisation, it will be possible to improve collected data quality (e.g. with the use of verification algorithms when the entity is submitting its statement), as well as to reduce the costs of handling the environmental fee system, which will generate savings for the public finance system.

Easier access for the responsible institution to data on charges for using the environment, also at a central level, could positively influence the effectiveness of decision making processes regarding environmental protection and responding to problems occurring in the fee system. Effective managers focus on particularly important issues, in attempt to make just a few important decisions at the highest level, whereas the appropriate decision making process comprises several consecutive stages [Drucker 2001].

Accordingly, the electronic operation of the environmental fee system could influence the efficiency of management, improve the control of fee calculation precision, and support tasks carried out by the units subordinate to the minister responsible for the environment.

In spite of various important funds (mainly foreign) presently available for projects undertaken in the sector of environmental protection, the operational system of environmental fees is necessary for the proper functioning of mechanisms supporting environment-friendly investments and activities. Maintaining the system is also necessary to implement the polluter pays principle, thanks to which any entity compensates for the use of environmental resources in its activities. In Poland’s system of fees for using the environment, a given entity independently determines the scope of this use and if it exceeds certain thresholds, it pays an appropriate fee. At the same time, the responsible authority uses control tools to check the correctness of data provided by entities. Due to the fact that the fee system was created more than 40 years ago, certain patterns of its operation were adopted at the start and continue to function today, regardless of new technologies already used by the public administration who has gone through transition towards full computerisation. Therefore, it seems that with the current advancement of informatisation, the commitment of employees, both on the part of those using the environment and the public administration, the failure to introduce full informatisation of the fee system would be a missed opportunity to make developmental changes. Computerisation would also contribute to lowering the costs of handling the fee system and, through control activities, would certainly influence the enforcement of environmental fees from entities that evade payments, even though they exploit environmental resources to a large extent. Increased public awareness about environmental protection in the era of climate change and rapid changes in the environment are not without significance. We will find out in the near future whether the necessary modifications are implemented and the opportunities taken advantage of. For decades, policy makers have been working continuously to develop effective approaches to environmental protection. Considering changing climate, it is important to note that actions should be more effective and implemented more efficiently. Having in mind the good of our planet and the future of humanity, the authors hope that this time chosen an environmental strategy will effectively protect our planet.