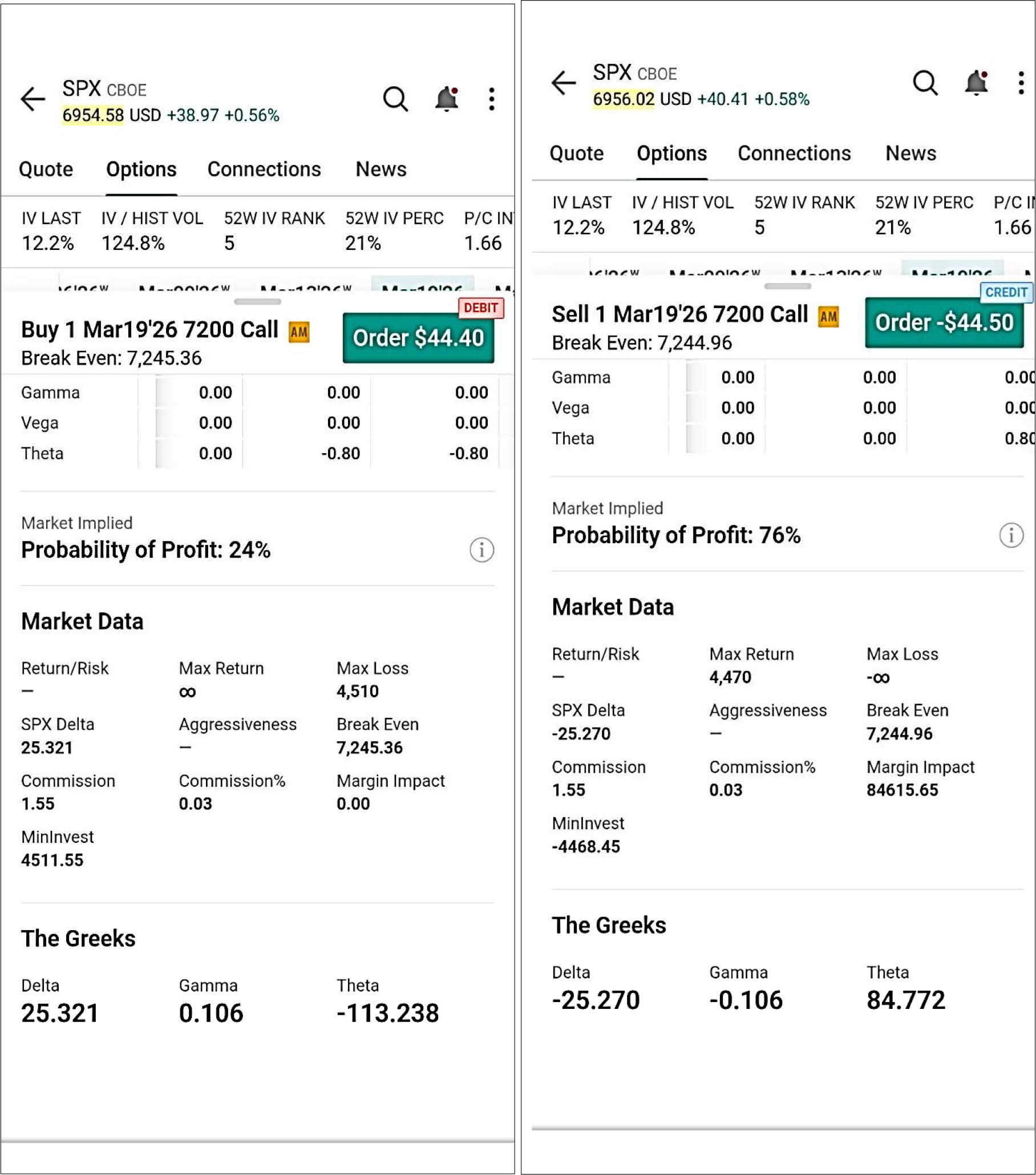

Figure A1.

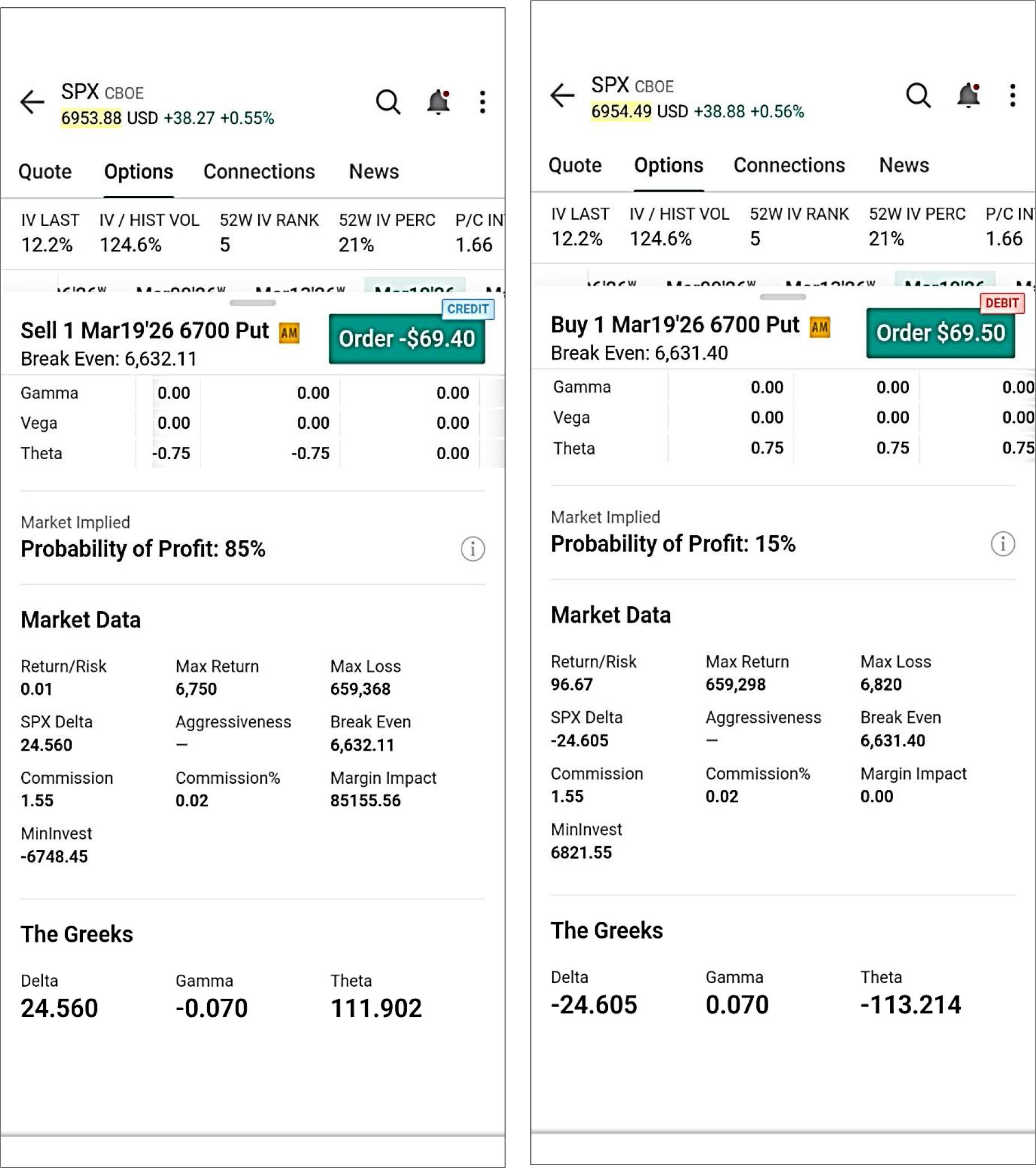

Figure A2.

Figure A3.

Defined-risk option strategies

| Strategy | Notes |

|---|---|

| Generate Cash Flow in Stagnated or Sideways Market | |

| Covered call: hold the underlying asset and sell OTM call |

|

| Protect Underlying Asset from Severe Drawdowns | |

| Protective put: hold the underlying asset and buy OTM (or ATM) put |

|

| Protect Underlying Asset from Severe Drawdowns at Reduced Cost | |

| Collar: hold the underlying asset, buy OTM put and sell OTM call |

|

| Mitigate Severe Drawdowns by Using Cash Secured Call | |

| Cash secured call/Fiduciary call: buy call and invest cash in risk-free asset |

|

| Limited Upside (Bull Spread) or Downside (Bear Spread) Participation with Preset Losses | |

| Bull Spread |

|

| ii. Put spread: buy put at X1 and sell at X2 where X2 > X1 |

|

| Bear Spread |

|

| ii. Call spread: sell put at X1 and buy at X2 where X2 > X1 |

|