Throughout the world, the availability and sophistication of digital financial services (DFS) is increasing at a rapid pace, most notably since the onset of the COVID-19 pandemic in 2020. Along with a promise of improved affordability and increased convenience of financial services for underserved populations, with the growth of DFS comes a need for consumers, particularly those new to digital services, to be more savvy, informed and able to manage these services. This is especially true for those in low- and middle-income countries (LMICs), which are typically now moving from what has been termed the “first wave” of (primarily) payment services to a broader range of products and services (Pazarbasioglu et al., 2020).

While as of 2023, 1.75 billion accounts had been registered globally with a value of approximately USD 1.4 trillion, low levels of digital and financial literacy in LMICs is still a barrier to uptake and usage of DFS, particularly for women, rural, and vulnerable populations (GSMA, 2024). Further, many of the research tools used to paint fuller pictures of digital connectivity, digital literacy, and digital and financial literacy can be time consuming and expensive, and are often not contextualized to specific economies, such as those in Pacific Island Nations.

Given this context, the United Nations Capital Development Fund (UNCDF), along with Dr. Adele Atkinson and Tebbutt Research, developed a “lean” tool for measuring digital and financial literacy beginning in 2021. The UNCDF Digital Financial Literacy Survey (DFL Survey) is part of the agency’s effort to provide a public good that can be used by the wider stakeholder community, as well as to gather the evidence needed for government, civil society, and public sector organizations to better target and measure progress on programs to build digital and financial knowledge and skills (G20/OECD-INFE, 2021). The tool is particularly valuable as part of coordinated approaches to develop and implement targeted interventions for improving digital financial competencies. Initial survey results can serve as a baseline from which future changes in competencies, access, and usage can be measured by regulators and practitioners alike.

To date, this survey has been implemented and published for six Pacific countries (Fiji, Papua New Guinea, Samoa, Vanuatu, Solomon Islands, Tonga) and Timor-Leste, leading to significant insights that will be used to shape programs and policy. For instance, in Fiji, 81% of respondents owned a smartphone and 78% have a mobile wallet; but at the same time, three out of five still find using mobile services risky, pointing to a potential need for interventions to increase confidence in users and consumer protection efforts. The survey is currently in the process of data collection in four countries in sub-Saharan Africa; the continent where the highest levels of mobile money adoption are being registered (UNCDF, 2023).

Section II of the paper outlines the survey and it its design. Section III summarizes findings obtained from the surveys. Section IV describes examples of uses of the survey to create better, more focused development actions, with a focus on underserved communities. Section V concludes with a discussion of implications and future uses of the survey.

The DFL survey, developed to fill a gap in terms of evidence-based interventions, is a quantitative measure that can provide data on digital financial product and service uptake and usage to be used to inform policy as well as to design targeted interventions for users and potential users. It took as its starting point three existing tools used internationally (Atkinson, 2021).1 The survey was first developed and implemented in the Pacific partially because of the lack of current data in Pacific countries; for example, oft-used global databases such as the Global FinDex do not yet include the Pacific Region (PEI, 2023).

Its goal was to offer a viable method of data collection across countries with limited physical and digital infrastructure, that was cost-effective, to provide findings that were easy to interpret without specific training in economics or statistics. It also needed to remain highly focused on the core concepts being explored in the populations being surveyed to keep it short enough to be cost-effective and feasible as a telephone survey tool.

A short questionnaire was developed capturing demographic information and data on the extent to which different groups report usage of digital tools in everyday life, levels of digital and financial competencies, and experience with DFS. Specific focus areas and outcome groupings are summarized in the Appendix.2 The questionnaire was scripted into data collection software and then interviewer-administered on digital devices (tablets). Some initial wording changes were made to ensure it could be interviewer-administered (as many surveys including the initial draft of the tool for this project) are designed for self-completion online.

Each question was therefore developed or refined as necessary to create a cohesive tool with a coherent narrative across the questions that made it possible to read the questions and possible responses out loud in a logical manner within a maximum 20-minute timeframe. Question wording also allowed for significant localization, to account for different local terms, names and experiences. Filters were kept to a minimum to ensure that data would be available for the whole sample on most questions, and particularly those used in the scores.

The questionnaire was designed with a view to collect comparative data not only in different localities but across time, with an initial baseline and later follow-up measure of progress (or lack thereof). This meant that the questions needed to be ‘future-proofed’ as much as possible, with questions relating to factors that are more common in highly developed economies, as well as those that are specific to the current reality of low-income countries. Even so, it will be essential to revisit the questionnaire in the future given the rapidly changing landscape for digital tools and services. A scoring system based on the four key areas (digitalization, financial competencies, digital financial competencies, and DFS outcomes) was designed to allow for a simple comparison between countries and amongst different target groups within a country or context (such as comparing by gender, locality, age ranges). Each focus area was assigned a numeric score and a system of outcome score groups from low to high was assessed for each country.

This simple approach has four main benefits: (1) it is possible to create and recreate the scores with minimum technical skills; (2) it is easy to understand the relationship between the questions and the scores; (3) there is no implicit or explicit assumption that one question is somehow more important than another (such assumptions are prone to change over time); (4) it is easy to interpret the magnitude of any difference across target groups, countries or time. The use of a simple scoring system does not exclude the possibility of undertaking more complex approaches such as factor analysis to explore the data in other ways.

Tebbutt Research, the Pacific-based firm that co-funded, localized, implemented, and analyzed survey results, completed interviews with individuals aged 15 to 74 years in each nation. The survey was administered via a mixed mode methodology. Telephone interviews utilizing Computer Assisted Telephone Interviewing (CATI) technology and Random Digit Dialing (RDD) made it possible to randomly generate mobile phone numbers and randomly assign these to interviewers located in-country.

Data from mobile phone interviews was combined with data from face-to-face interviews undertaken via Computer Assisted Personal Interviewing (CAPI) and employing a Probability Proportional to Size (PPS) methodology to draw the sample. For all of the countries, the research took place from mid-2022 to early 2023, with publication of the Pacific surveys in late 2023 and early 2024.3

The sample was designed based on current demographics for each country in terms of age ranges, urban vs. rural respondents, and male and female respondents. Table 1 displays the number of respondents in each country.

Total Number of Respondents per Country with Percentage Male and Female

| Country | Women | Men | N |

|---|---|---|---|

| Fiji | 49% | 51% | 1,678 |

| Papua New Guinea | 48% | 52% | 1,587 |

| Samoa | 49% | 51% | 1,216 |

| Solomon Islands | 49% | 51% | 1,540 |

| Timor-Leste | 49% | 51% | 1,631 |

| Tonga | 49% | 51% | 1,212 |

| Vanuatu | 50% | 50% | 1,212 |

To ascertain statistical significance, a two-tailed Z-test, p≤0.5 at 95% confidence level was used, noting that statistical significance does not necessarily note relevance. For comparison on overall scores, “low” scores were described as 0-12 points, “moderate” as 13-26 points, above average as 27-39 points, and “high” as 40-52 points, out of a possible total of 52 points.

Table 2 gives an overview of each country’s overall score in the four topic areas. From survey findings, Pacific Islands adults possess moderate levels of digital and financial literacy with significant room for growth in the uptake of digital financial services and in familiarity and awareness of safeguards for DFS usage. Fijians were assessed at the highest overall score with 26.81 out of 52 points, at moderate level overall, while Timor-Leste showed the lowest overall score with 20.47, closely followed by Timor-Leste with a mean score of 20.47 index points. While all countries fall within what was defined as the “moderate” range, countries other than Fiji are notably lower than those of Fiji, especially in terms of DFS outcomes. This may be due to higher rates of DFS ownership in Fiji vis-à-vis the other countries surveyed (Horst & Foster, 2023).

Mean Scores in Four Areas for Countries Surveyed

| Country | Digitalization | Financial Competencies | Digital Financial Competencies | DFS Outcomes | Total |

|---|---|---|---|---|---|

| Points possible | 18 | 13 | 9 | 12 | 52 |

| Fiji Papua | 7.97 | 7.65 | 3.97 | 7.22 | 26.81 |

| New Guinea | 6.15 | 7.16 | 2.94 | 4.88 | 21.13 |

| Samoa | 6.95 | 6.87 | 3.44 | 5.14 | 22.41 |

| Solomon Islands | 6.35 | 7.66 | 3.27 | 4.72 | 22.00 |

| Timor-Leste | 5.42 | 7.08 | 3.38 | 4.59 | 20.47 |

| Tonga | 6.87 | 7.19 | 4.18 | 4.98 | 23.22 |

| Vanuatu | 6.99 | 7.68 | 3.36 | 5.05 | 23.08 |

However, as may be expected, higher scores were generally found in all countries amongst higher income earners, those working outside the home, amongst men, urban dwellers and those with higher levels of formal schooling. While not the case for each group in each country, these were findings in general; and overall, in each country scores fell generally in the moderate range. Gendered differences are most apparent in Fiji, where urban women have higher mean score than urban and rural men. In other countries, the difference is unsurprisingly more marked between urban men and rural women, with Vanuatu showing the greatest gendered differences in terms of scores. Table 3 outlines the differences in overall scores by gender and locality.

Mean Total Scores by Gender and Locality

| Country | Urban Men | Rural Men | Urban Women | Rural Women |

|---|---|---|---|---|

| Fiji Papua | 23.38 | 24.55 | 27.57 | 24.52 |

| New Guinea | 24.99 | 19.62 | 22.95 | 18.92 |

| Samoa | 22.99 | 22.57 | 24.07 | 21.24 |

| Solomon Islands | 25.18 | 18.80 | 22.51 | 18.47 |

| Timor-Leste | 22.18 | 18.80 | 22.51 | 18.47 |

| Tonga | 23.41 | 23.21 | 23.55 | 22.53 |

| Vanuatu | 27.23 | 23.62 | 23.77 | 20.96 |

Note: 52 Total Points Possible

Finally, mean results also show higher scores for those with higher levels of education and formal employment. These are summarized below in Table 4. Given that the formally employed and those with higher levels of education often have higher and more regular incomes, access to formal services via work (including DFS), more opportunities to own and practice using digital tools, these results fall in line with expectations from other studies (e.g., Fitriaty et al., 2023).

Overall Scores by Educational Attainment and Work Status

| Country | Middle School or less | Secondary School | University | Self-Employment | Formal Employment |

|---|---|---|---|---|---|

| Fiji Papua | 20.78 | 25.81 | 31.31 | 25.96 | 29.26 |

| New Guinea | 17.74 | 23.32 | 26.88 | 20.71 | 26.17 |

| Samoa | 19.05 | 21.71 | 25.45 | 22.72 | 24.69 |

| Solomon Islands | 19.32 | 23.84 | 27.10 | 21.86 | 25.46 |

| Timor-Leste | 16.67 | 22.08 | 26.56 | 19.65 | 23.93 |

| Tonga | 20.60 | 23.36 | 26.77 | 24.77 | 26.87 |

| Vanuatu | 20.80 | 25.95 | 23.73 | 22.96 | 23.08 |

The data above provides a baseline and snapshot of diverse groups across these six Pacific countries and Timor-Leste that can be revisited by focus area as well as by demographic group and context in the future. Additionally, by examining individual questions and sets of questions, a more focused picture of access, uptake and usage of digital products appears. Specifically, access to digital tools and the internet is high, and is growing, 4 throughout the region, while at the same time, usage of digital financial products and services is low and cash is still “king” when it comes to normal transactions. Moreover, trust and self-confidence in usage of digital financial products and services shows room for growth, particularly in an age when scams and fraud are prevalent and are becoming more sophisticated. These findings are elaborated below.

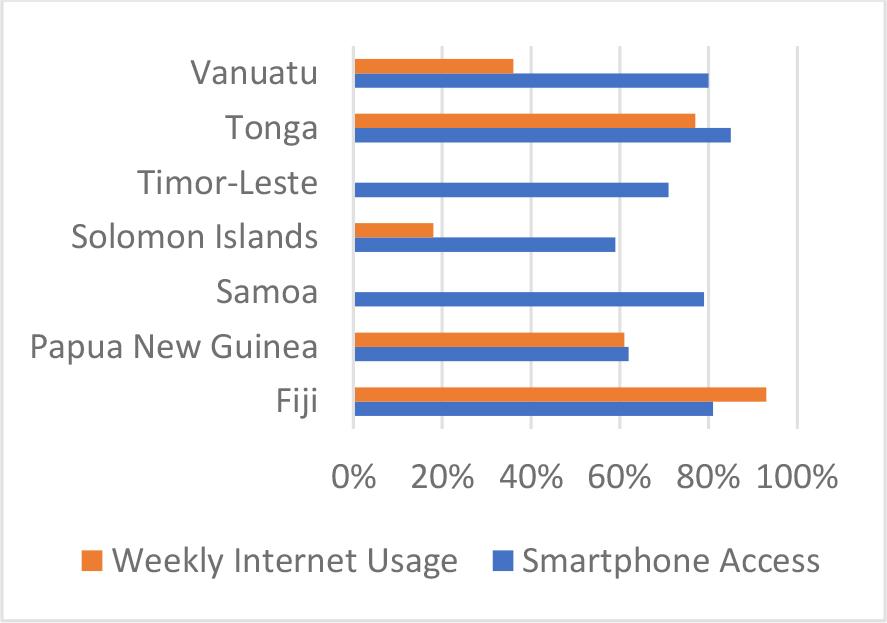

Internet access and access to smartphones, whether owned personally or for work, is high, showing that the potential for reach for digitalized services is great in Pacific markets. As shown in Figure 1, frequent internet usage varies greatly by country; however, over half of the population in each market report that they have access to a smartphone. Further, almost one-third of all respondents had computers or tablets accessible at home or work, with the highest (48%) in Tonga and lowest (28%) in Timor-Leste.

Smartphone Access and Internet Usage (Weekly) by % of Respondents

Both cost and issues of infrastructure such as quality of connection are obstacles to greater usage of digital tools. Although not shown in the figure, cost was a key issue for over half of respondents in every country except for Tonga (34%), ranging between 50% - 60% as a reason that individuals were unable to use the internet on a regular (or more regular) basis.

Table 5 shows that access to and ownership of accounts in the Pacific region is moderate overall, and other than in Fiji where mobile wallets have a high ownership rate, and shows a gap in terms of products and services available. In some cases, such as that of Samoa, mobile wallets are a relatively new product available on the market which may point to a need for more awareness and education on these services, while in Papua New Guinea, Solomon Islands, Tonga and Vanuatu, fintech and DFS are still nascent in these countries and financial ecosystems need expansion in order to reach more people in those contexts (GSMA, 2023).

Financial Product and Service Ownership by Country

| Bank/Current Account | Payment Card5 | Mobile Wallet | |

|---|---|---|---|

| Fiji Papua | 62% | 86% | 78% |

| New Guinea | 49% | 48% | 10% |

| Samoa | 40% | 27% | 24% |

| Solomon Islands | 45% | 7% | 4% |

| Timor-Leste | 48% | 46% | 24% |

| Tonga | 54% | 32% | 4% |

| Vanuatu | 53% | 40% | 9% |

Note: Payment cards included those linked to accounts at financial service providers and others such as those used for transportation.

At present cash is still “king” and constitutes the majority of financial services used by respondents. Therefore usage, especially of services like online e-commerce, is still relatively low. This is likely due to lack of available products, cost, and geographic constraints of Pacific countries in which particular obstacles to intranational commerce exist.

In addition, the use of online or internet-based information to self-educate on financial matters is low, as is use of internet to complete or submit government forms online (an aspect of growth in terms of digital public infrastructure that is a focus globally at present). While about a third of those in each country reported having used online services as a learning tool, this is again much higher amongst high income, urban, and educated populations, although low overall. Using the internet for information related to finance or money ranged from 11% in Tonga to 22% in Papua New Guinea, while filling and submitting government forms ranged from 7% in the Solomon Islands to 20% in Fiji.

The use of internet to self-educate in general, while lower in terms of money matters, points to a potential for leveraging online resources (particularly those that can reach more rural, less educated populations) to deliver digital financial education along with face-to-face delivery.

In general, survey respondents across contexts reported that DFS is an inevitable development that will become more and more prevalent and necessary for payments and money management. However, there was also a high degree of concern about the ability of individuals to navigate new services safely, mitigate risk and resolve problems when they arise.

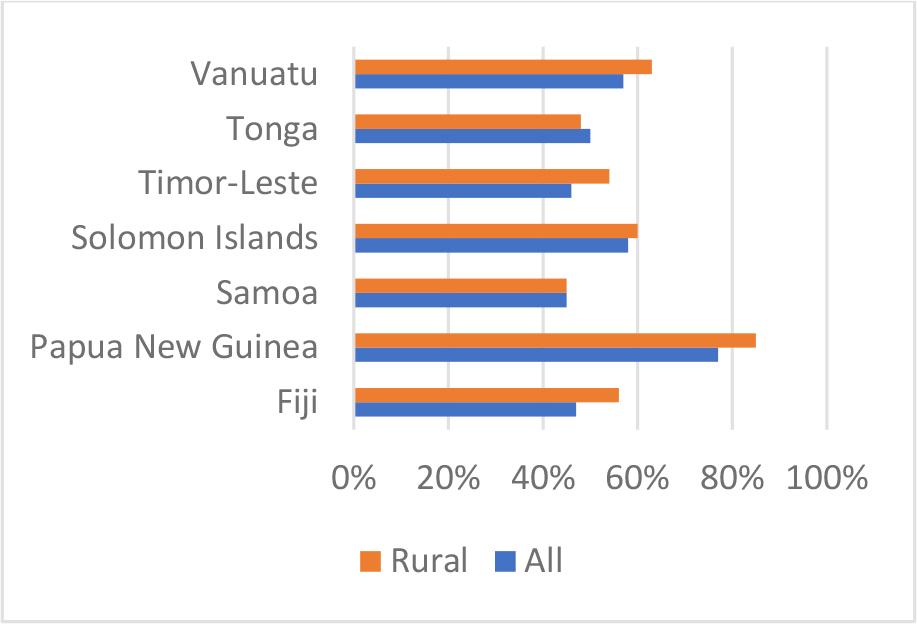

A high percentage of people in all countries surveyed reported feeling that technology is leaving them behind. Figure 2 shows the percentage of respondents, both rural and overall, who stated “yes” when asked if they feel that technology is leaving them behind. Papua New Guinea, the country with the overall lowest mean score, showed the highest level of feeling “left behind” while Fiji, with a much higher overall score than the six other countries surveyed, still showed that about half of respondents share this attitude. Even with lower scores, Tonga, Timor-Leste and Samoa are similar or lower. For Papua New Guinea, showed that at the end of 2023, there were still fewer than 40% of the population with mobile connections, while Fiji and other countries have much higher rates of connectivity; in the case of Fiji, over 100% (GSMA, 2024).

Respondents who "Feel that Technology is Leaving me Behind"

The percentage of respondents who feel that technology is leaving them behind is a strong indicator of the need for digital and digital financial literacy programs that build skills, competencies as well as self-confidence. There is also a strong belief that DFS are risky for ordinary people (Figure 4). Paired with the information that the majority of respondents also feel that digital is the future, preparing citizens in Pacific countries for new products and services so that they use them independently and feel a sense of agency and self-efficacy will be key in these products and services reaching their greatest potential (e.g., Muizzuddin et al., 2017 and Borges, Ramalho, & Forte, 2018).

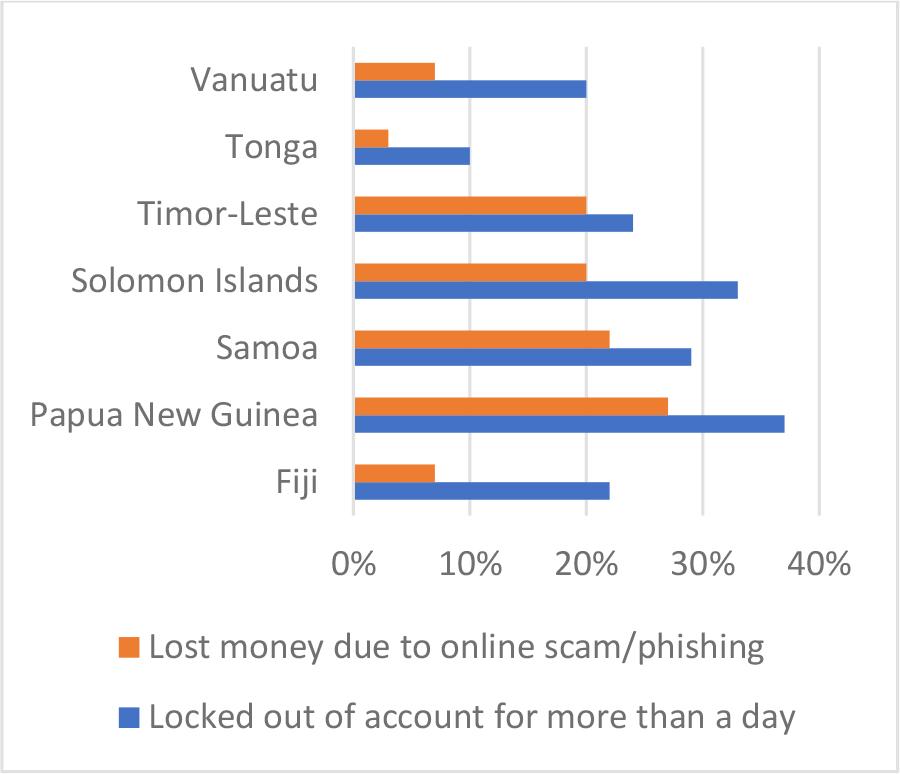

Finally, Figure 3 shows that at the time of data collection, in some contexts (Timor-Leste, Solomon Islands, Samoa and Papua New Guinea) those reporting having lost money to a same or phishing, and being locked out of their accounts, was upwards of 1/5 of those in the survey sample. The 2023 Asia-Pacific Digital Banking Fraud Trends report (Biocatch, 2023) reported that there was a 200% increase in voice scams between 2022 and 2023, as well as growing sophistication amongst fraudsters. Data on digital fraud, as well as up-to-date educational campaigns from governments and other stakeholders will be paramount in the present and the future as this trend is likely to continue. If digital products and services are to live up to their potential, a clear picture formed by data, as well as targeted policies and activities, will be necessary to ensure that populations do not lose money, but also so that they do not lose trust and have the ability to protect themselves.

Respondents who Faced Fraud or Account Issues

Practitioners and decision-makers from diverse stakeholder groups recognize that digital, financial and digital financial literacy pose a significant barrier to the safe and effective use of digital financial services as a means to economic empowerment. While both smaller market sizes and remoteness from major international markets are often hurdles to developing new financial services, digital mechanisms provide new ways to access and strengthen these markets (Chen, et al., 2020).

Promises offered by new digital opportunities, products and services, and a more robust digital financial ecosystem, when tracked and supported by data, can potentially help to make DFS more affordable, convenient, and safe for new users. Regular usage and the increase of confidence and trust, especially for those groups still underserved such as women, rural dwellers, micro- and small businesses, and migrants (G20, 2020), are areas that should be in focus for governments, practitioners and those service providers that aim to target underserved groups.

Survey data can be, and in some cases is being, used in the design and update of national financial inclusion strategies, national financial education strategies, and other digital strategies and policies. For example, in Samoa, the National Financial Inclusion Strategy 2.0. has a pillar on digital financial literacy, and survey results will be considered as a baseline for a number of strategy indicators. While not based only on the survey and a result the work of numerous actors and government objectives, the survey is part of a proposed DFL roadmap for the Central Bank of Samoa (see Figure 4). Such a roadmap provides a clear guide for other governments seeking to integrate digital and financial literacy into policy and practice.

DFL Roadmap 2024, Central Bank of Samoa

Data creates a baseline that can be measured as more digitalization of public services or “digital public infrastructure” is being built to show areas of progress or future gaps, given the low levels of usage of digital tools at present for government services.

Government offices such as Samoa’s digital transformation unit in the Central Bank can and will consider survey results to measure progress and potentially will add questions on government-to-person (G2P) and person-to-government (P2G) payments, services which have been shown to drive greater financial inclusion and product usage (Wallace, et al., 2022).

Findings from the survey are now being used to inform and support the need for an addition of digital skills and digital financial skills into the Fijian the school system, to build digital and digital financial competency widely and at young ages. As of publication of this paper, UNCDF and UNDP are beginning this process in partnership with the Fiji Ministry of Education and will pilot and scale throughout 2025. Other countries plan to announce similar activities in 2025; for example, the survey is currently under completion in Ethiopia and will be used in UNCDF and the Ministry of Innovation and Technology’s educational programs targeting both students and citizens in general.

Survey findings point to a need to target those with lower levels of education, women, those in self-employment, and other groups with lower scores in the four focus areas as well as lower uptake and usage of specific products and services. A hybrid approach, based on previous UNCDF and other practitioner experience, combining relevant and applicable face-to-face training with alternative (such as internet-based, interactive voice response, or other) delivery mechanisms should be explored (Massie & Morrow, 2022).

In 2024 and 2025, the DFL survey is being contextualized and implemented in at least four markets in sub-Saharan Africa: Ethiopia, Gabon, Malawi and Niger. Follow-up surveys are tentatively planned for three to five years after baseline in the six Pacific markets and Timor-Leste, with possible baselines in other developing markets. Likewise, given that the survey and its results are a public good, UNCDF is interested in prospective partners or in providing those interested with data or guidance in further survey implementation.

While digital financial education, or the promotion of financial and digital literacy, are not the be all and end all to drive uptake and usage, they are important pieces of the puzzle. The DFL survey and similar tools designed to be used in multiple contexts in a “lean” way provide needed tools to better target and track results of these efforts; “measuring what matters” (Singh et al., 2022) in order to create interventions and design products that contribute to economic empowerment and increased resilience and selfreliance for those still underserved at present. For the future, survey results are being considered to measure uptake and usage of products and services, inform product design, and have greater impact in wider development programming.

The surveys show a need (and potential market) for a greater diversity of financial services from supply side actors. Person-to-person payments tend to show the greatest usage, but payment services are still primarily in cash. Lessons from other markets (such as Kenya, Rwanda) can be studied and learnings applied, based on survey results showing high levels of internet access, of financial service access, but a prevalence of cash.

Mobile wallets may be harnessed as a first step for providers in promoting greater uptake of digital financial products and services, especially if agent networks, micro- and small businesses, are a focus and included in product design and in marketing. New products such as bill payments could provide an avenue for greater convenience on the demand side as well as improved revenue for the supply side.

Given the lack of self-confidence expressed by many survey respondents and the selfreporting of being locked out of accounts or losing money due to fraud, protection mechanisms should be considered during product design and development and clearly communicated with new clients. Recourse mechanisms and customer service are areas of focus that may help to cut down on problems faced in terms of usage and safety.

Differences in scores amongst target groups show the need for targeted, localized interventions based on data that addresses gaps and is easily disaggregated and collected. For example, programs with specific objectives can use survey data (where it exists or employ the survey themselves) as a baseline, and monitor using specific questions where appropriate to track progress. Qualitative data to some degree will be required for localization efforts, but simple surveys such as this can be utilized as well.

Development actors who are “agnostic” in terms of specific products and services can use data to support the development of affordable, appropriately designed services for groups that are not yet served, as well as where those products and services do not yet exist. Promotion of responsible financial inclusion, which has the potential to lead to greater opportunities and poverty alleviation so that individuals can make use of earning opportunities via improved entrepreneurship and access to work, as well as make informed financial choices, should be a focus for these actors.

While regulators and supply side are aware of potential consumer protection issues and taking steps to solve these, the onus is at present often on the user/client to safeguard their own information and digital money, and many people do not have the capacity to handle and recover from a financial loss. At the same time, global data (such as that of CGAP, see Duflow & Riquet, 2024) shows that “the nature and scale of digital financial consumer risks… and frequence of fraud and consumer data misuse” are growing. Therefore, development programs supporting economic development should have an aspect of consumer protection as well as advocate for robust consumer protection in markets where they work.

Survey findings are currently being used and will continue to be used to develop and implement targeted interventions for improving digital financial competencies among women, MSMEs, youth, migrant workers, and rural communities. The survey results are intended to serve as a baseline from which future changes in competencies, access, and usage can be measured by regulators and practitioners alike.