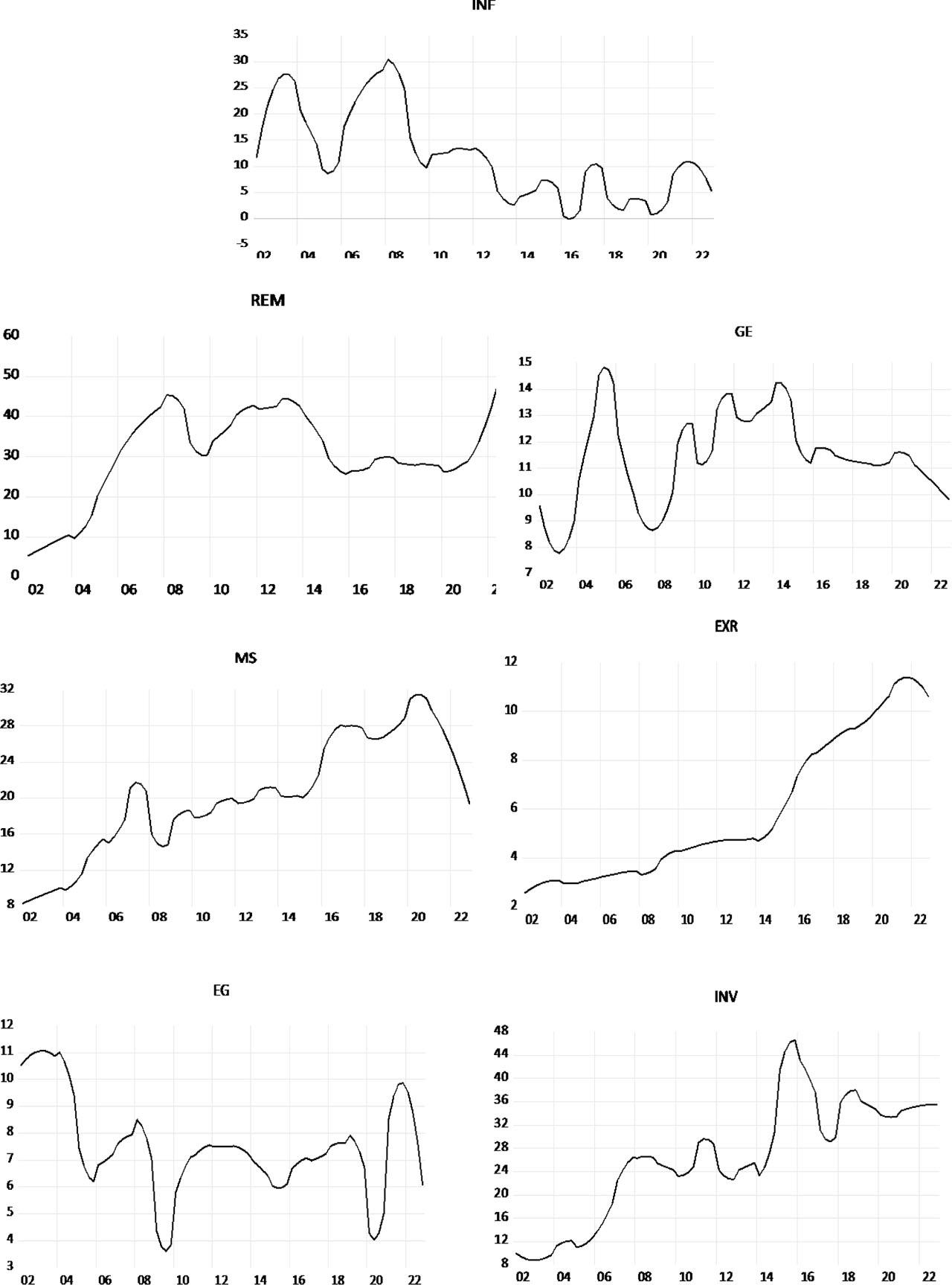

Figure 1.

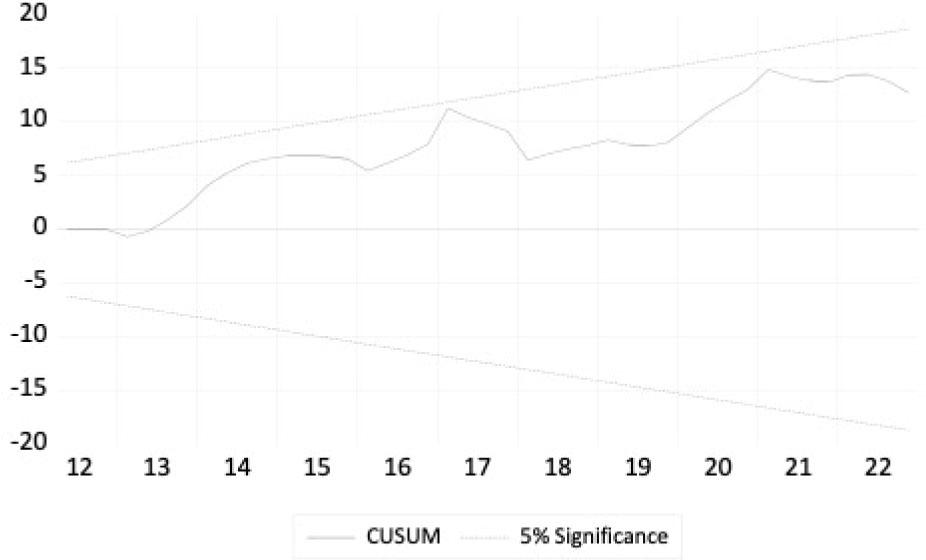

Figure 2.

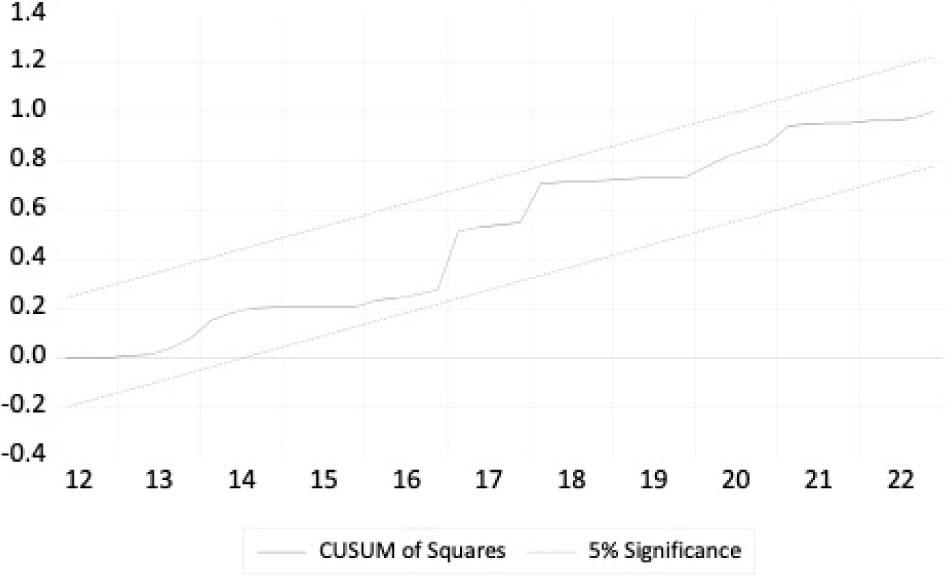

Figure 3.

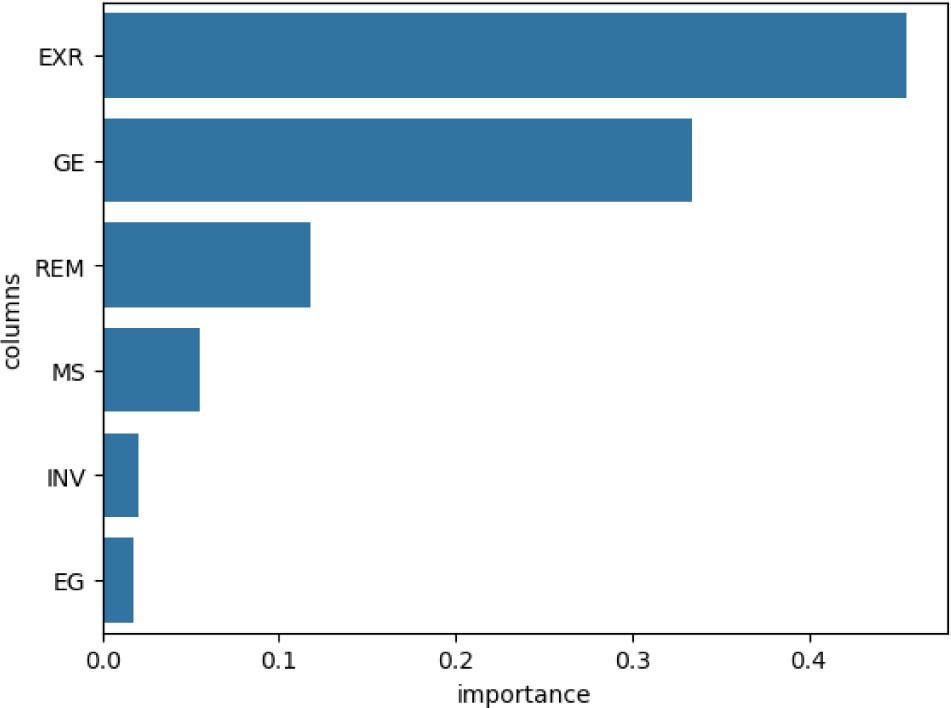

Figure 4.

ARDL bounds test

| F-statistics | Significance level (%) | Lower bound | Upper bound |

|---|---|---|---|

| 8.954*** | 10 | 2.631 | 3.589 |

| 5 | 3.043 | 4.100 | |

| 1 | 3.966 | 4.630 |

Diagnostic and stability tests

| Test | Null hypothesis | Test stat. (prob) | Conclusion |

|---|---|---|---|

| BPG | Homoscedasticity | 0.2613 (0.9991) | The model is homoscedastic |

| BGLM | No serial correlation | 2.2684 (0.1140) | No evidence of serial correlation |

| Ramsey | No misspecification errors | 0.6108 (0.4381) | No misspecification error |

| CUSUM | Stable | ||

| CUSUM SQ | Stable |

ARDL approach test results

| Variable | Coefficient | Std error | t-statistic | Prob | Conclusion |

|---|---|---|---|---|---|

| REM | 0.2267 | 0.1143 | 1.9831 | 0.0526 | Significant |

| GE | −1.7010 | 0.3958 | −4.2971 | 0.0001 | Significant |

| MS | −0.6213 | 0.1866 | −3.3297 | 0.0016 | Significant |

| EXR | 2.6336 | 0.7046 | 3.7375 | 0.0005 | Significant |

| EG | 0.3124 | 0.1522 | 2.0526 | 0.0452 | Significant |

| INV | 0.0342 | 0.0407 | 0.8390 | 0.4053 | Insignificant |

| TREND | −0.5635 | 0.1102 | −5.1130 | 0.0000 | Significant |

| ECT (-1) | −0.7582 | 0.8409 | −9.0175 | 0.0000 | Significant |

Variable information

| Variables | Description | Sources |

|---|---|---|

| INF | Inflation is proxied by the GDP deflator | World Bank |

| REM | Remittance inflows as % of GDP | World Bank |

| GE | Government expenditure as % of GDP | World Bank |

| MS | Broad money supply as % of GDP | Asian Development Bank |

| EXR | Exchange rate (somoni per USD) | International Financial Statistics |

| EG | Real economic growth rate in % | World Bank |

| INV | Gross capital formation, proxy for investment, % of GDP | World Bank |

Unit root test results

| ADF | ADF with breaks | |||

|---|---|---|---|---|

| Variable | Level | 1st Diff. | Level | 1st Diff. |

| INF | −1.807 | −4.191*** | −3.488 | −7.841*** (2011Q1) |

| REM | −0.06 | −2.492** | −3.099 | −4.405** (2020Q2) |

| GE | −0.621 | −4.622*** | −4.718** (2014Q1) | |

| MS | −0.353 | −2.247** | −3.162 | −4.711*** (2021Q2) |

| EXR | −0.406 | −2.310** | −3.222 | −4.222* (2021Q2) |

| EG | −1.450 | −3.400*** | −4.966** (2008Q3) | |

| INV | −0.674 | −2.597*** | −3.128 | −4.587** (2004Q1) |