Remittances (REM) have become a vital lifeline for developing economies, particularly in Central Asia, where they often exceed 20% of Gross Domestic Product (GDP), as seen in Tajikistan (World Bank, 2023a, 2023b) Tajikistan’s REM, primarily from migrant workers in Russia, have historically accounted for 30%–50% of GDP, peaking at 50.9% in 2022 before normalising to 37.4% in 2023, reflecting volatility tied to Russia’s economic conditions (Coface, 2024; World Bank, 2024). This volatility is particularly significant as 40% of households in Tajikistan had at least one migrant worker from abroad in 2021, underlining the important contribution of REM to household income and consumption (World Bank, 2022). In such a highly REM-dependent economy, inflation is a key indicator of economic stability and household welfare, as REM inflows affect prices through consumption demand, monetary policy and exchange rate (EXR) mechanisms. The 2014 Russian Ruble crisis and the 2022 Ukraine conflict significantly reduced remittance inflows, triggering inflation and liquidity challenges in Tajikistan’s banking sector (Migration Policy Institute, 2019).

Remittance inflows serve as a crucial support system for Tajikistan, a country with a significant migrant labour force that often surpasses other forms of external financial support, such as aid or foreign direct investment (INV) (World Bank, 2024). These transfers not only enhance household consumption but also influence inflation and various macroeconomic indicators (Clément, 2011). Understanding the connection between REM and inflation is crucial for Tajikistan, where price stability is essential for maintaining economic welfare and informing effective policy. This study investigates the long-term impact of REM on Tajikistan’s inflation rate while controlling for several macroeconomic indicators.

This study is driven by the unique economic conditions of Tajikistan, characterised by a heavy reliance on REM and a relatively underdeveloped domestic production sector. Inflation, as measured by the GDP deflator, is a key indicator of economic stability that significantly affects living costs and informs policy decisions. While REM can stimulate demand-driven inflation through increased consumption, their impact on the EXR and money supply (MS) adds complexity. While existing studies mostly focus on the importance of REM for economic development and poverty reduction in regions such as South Asia, their impact on inflation in post-Soviet countries, such as Tajikistan, remains largely unexplored. As a recently emerged economy that operated under the centrally planned Soviet Union for decades, Tajikistan presents a unique case for this study. Unlike most South Asian countries, Tajikistan’s transition involves structural shifts from state-mandated pricing to market volatility, where REM have peaked at over 50% of GDP, the highest globally (World Bank 2023a, 2023b).

This study employs a time-series framework, using quarterly data from 2004Q4 to 2022Q4, consistent with the assertion by Pesaran, Shin and Smith (2001) that time-series analyses more effectively capture the unique economic dynamics of individual countries than panel data methodologies. The long-term associations between REM, government spending (GE), MS, EXR, economic growth and INV with inflation are examined using an autoregressive distributed lag (ARDL) bounds test approach. This paper contributes by using a random forest (RF) machine learning (ML) approach to analyse key predictors of inflation in Tajikistan’s unique economic context. Furthermore, to the best of the authors’ knowledge, no previous study has explored the predictive importance of the determinants of inflation using an ML-based RF technique. It is essential to recognise that the feature importance obtained from the RF model indicates the predictive significance – namely, its capacity to diminish forecasting errors – and does not depict the structural economic contribution. This study is associational rather than causal in nature: the ARDL framework identifies long-run relationships but does not provide causal identification, as potential endogeneity cannot be fully ruled out without an instrumental variable (IV) or structural approach. Findings should, therefore, be interpreted as long-run associations, not causal effects. Instruments proposed in the broader REM literature, such as destination-country GDP growth or EXR movements, are either unavailable at the required frequency for Tajikistan or belong in the model as regressors given their large independent associations with domestic prices – the EXR, in particular, accounts for 46% of RF predictive importance and carries a long-run ARDL coefficient of 2.6336, confirming that it operates through channels well beyond the remittance transmission mechanism.

This paper is split into five parts. The first part introduces the study. The second part provides an overview of the literature on the main determinants of inflation considered for this study. The third part provides a summary of data and methodology. The fourth part presents empirical results, and the fifth part summarises the study and its conclusions.

Numerous studies in the existing literature have examined the primary factors influencing inflation, with particular emphasis on the impact of REM across different economies. Studies have examined how the inflow of REM affects prices through various channels, considering a range of macroeconomic variables. Common determinants in these studies are the EXR (Singer, 2010; Ball, Lopez & Reyes, 2013), MS and monetary policy (Akinbobola, 2012; Amassoma, Sunday & Onyedikachi, 2018; Buthelezi, 2023), GE or fiscal policy (George-Anokwuru & Ekpenyong, 2020), economic growth (EG) (Azam & Khan, 2022) and INV (Le Thanh, 2018).

In many developing nations, REM serve as a source of external funding, providing protection against economic instability and significantly enhancing both family well-being and the country’s overall revenue. However, their macroeconomic consequences remain uncertain and context-specific, especially concerning inflation. Several empirical studies have analysed the remittance–inflation nexus using diverse econometric methods, datasets and country-specific contexts. These studies generally fall under three time-based dimensions. According to the first dimension of those studies, REM tend to increase household consumption and the MS, raising aggregate demand and placing upward pressure on prices, particularly in countries with constrained supply responses (Narayan, Narayan & Mishra, 2011; Khan & Islam, 2013; Abdul-Mumuni & Quaidoo, 2016). The second dimension illustrates a negative short-run impact of REM on inflation, indicating that REM could contribute to a reduction in inflation. This effect may arise from EXR appreciation, which lowers import costs or facilitates consumption smoothing. Studies contend that, in certain instances, REM reduce inflationary pressures in the short run under flexible EXR regimes (Chami et al., 2008; Basnet, Donou-Adonsou & Upadhyaya, 2022). The variability in short-run findings, in contrast to the consistent long-run effects, underscores the importance of time horizons in analysing the remittance–inflation nexus. The third dimension concludes that REM have an insignificant impact on inflation, indicating that remittance inflows do not consistently or statistically significantly affect inflation. This is typically attributed to effective monetary policy frameworks, liquidity sterilisation driven by REM or inherent structural economic factors. Thus, the notion that the impact of REM on inflation is conditional and may be negligible under specific macroeconomic conditions (Khan & Islam, 2013; Abdul-Mumuni & Quaidoo, 2016; Rivera & Tullao, 2020). The inconclusiveness of evidence regarding the remittance–inflation nexus arises from variations in data periods, model specifications, estimation methods and country-specific characteristics. This uncertainty necessitates a country-level analysis that considers domestic economic structures and policy contexts.

These contradictory findings suggest that the inflationary effects of REM are not uniform; instead, they seem to depend on a range of country-specific factors, such as the existing EXR regime, the depth of financial markets and the overall credibility of the monetary framework. In economies characterised by high remittance dependency and restricted production flexibility, features common to transition states, inflows are frequently channelled into demand-driven price spikes. On the other hand, these inflationary pressures are typically either muted or transient in areas with stronger institutional cushions. This inherent heterogeneity suggests that relying on broad cross-country generalisations may mask critical transmission channels, thereby reinforcing the need for studies grounded in a strictly defined national context.

The EXR plays a crucial role in influencing inflation, particularly in open economies that are heavily reliant on international trade. To understand EXR dynamics, this study draws on the Exchange Rate Overshooting Model, first introduced by Dornbusch (1976). The primary component of this model is the assumption of ‘sticky prices’ in the short run versus flexible prices in the long run. This structural asymmetry causes the nominal EXR to ‘overshoot’ its long-run equilibrium level in response to monetary shocks, leading to immediate cost-push inflationary pressures as the currency adjusts faster than domestic goods prices. When the domestic currency depreciates, it leads to an immediate rise in the prices of imported goods and services, a phenomenon known as import inflation or cost-push inflation. This situation arises because companies incur higher costs for imported materials, which they subsequently pass on to consumers. In contrast, when the domestic currency appreciates, it can lower import expenses, thus applying downward pressure on domestic price levels. Notable research, including studies by Singer (2010) and Ball et al. (2013), highlights the significant impact of EXR fluctuations on a country’s inflation trends and overall macroeconomic stability.

The connection between the MS and inflation is fundamental to monetary theory, often expressed through the quantity theory of money. This theory posits that a substantial increase in the MS, leading to the growth of real output, is accompanied by a widespread rise in prices, commonly referred to as demand-pull inflation. Central banks employ various monetary policy instruments, such as adjusting interest rates or implementing quantitative easing or tightening, to regulate the MS and maintain price stability. These concepts are extensively covered in fundamental texts on monetary economics (e.g., Mishkin, 2007). Empirical studies from diverse settings, including Akinbobola (2012) for Nigeria and Buthelezi (2023) for South Africa, consistently indicate that an expansionary monetary policy, if not meticulously controlled, can exacerbate inflationary pressures. Additionally, Roberts (2004) examines monetary policy and inflation dynamics, analysing how monetary policy changes have influenced the relationship between inflation and unemployment, as well as the volatility of output and inflation.

Government expenditure, as a fundamental element of aggregate demand, directly affects the overall level of economic activity and, consequently, inflation. When GE rises significantly without a proportional increase in the economy’s productive capacity, it can boost aggregate demand beyond the existing supply, leading to demand-pull inflation. Nevertheless, the inflationary effects of GE are not always clear-cut. If fiscal expenditures are allocated towards productive INVs in areas such as infrastructure, education or healthcare, they can improve long-term supply-side capabilities, potentially alleviating future inflationary pressures. George-Anokwuru and Ekpenyong (2020) highlight this intricate relationship in Nigeria, stressing that decisions regarding government expenditure (fiscal policy) are vital in shaping a country’s inflationary landscape. The Fiscal Theory of the Price Level (FTPL), first introduced by Leeper (1991) and further examined by scholars such as Woodford (2001), presents an alternative viewpoint in which fiscal policy, independent of monetary policy, can influence the price level. The core component of this theory is the government’s intertemporal budget constraint; it posits that if future primary surpluses do not entirely offset public debt, the price level must adjust to ensure the real value of the debt matches the discounted value of those surpluses. In the context of Tajikistan, this implies that fiscal expansion not backed by future revenue can lead to inflationary pressures regardless of the central bank’s stance.

The relationship between EG and inflation is a topic of considerable discussion, frequently analysed through the framework of the Phillips curve. The model consists of two primary components: the output gap (the difference between actual and potential GDP) and inflation expectations. During periods of rapid economic growth, especially when demand surges and the economy nears full capacity, businesses may face rising costs (such as labour and raw materials), leading to higher prices. This scenario can illustrate either demand-side pressures or capacity limitations. On the other hand, EG, driven by productivity and supply-side efficiencies, can lead to disinflation, as it increases the availability of goods and services, thereby reducing inflationary pressures. Azam and Khan (2022) delve into these dynamics, providing further empirical evidence from both developed and developing economies and identifying threshold effects in the relationship between inflation and economic growth.

INV, especially gross capital formation, serves a dual purpose in affecting inflation. In the short term, an increase in INV activity can put upward pressure on inflation by boosting aggregate demand for capital goods, labour and other resources. This surge in demand may lead to higher prices if the supply side cannot adjust promptly. Conversely, in the long term, INV is crucial for enhancing an economy’s productive capacity. By augmenting the capital stock and improving efficiency, sustained INV can result in a greater supply of goods and services, which ultimately functions as a counter-inflationary mechanism. Le Thanh (2018) highlights the significance of INV, often driven by REM, in fostering long-term economic development and, in turn, indirectly aiding inflation management through supply expansion in developing countries in the Asia-Pacific region. Classical and neoclassical growth theories, as illustrated by Solow (1956), emphasise the essential role of INV in capital accumulation and long-term economic growth, which can, in turn, affect aggregate supply and price stability.

Within the Central Asian and Tajikistan-focused literature, research on REM has tended to emphasise growth, poverty alleviation, labour-market dynamics and household-level outcomes, reflecting the region’s development priorities and data constraints. By comparison, the implications of remittance inflows for inflation and price dynamics appear to have received less explicit attention, particularly in studies that model inflation as a primary outcome rather than as an auxiliary control variable. From a theoretical perspective, this represents a potentially important omission, as REM may influence inflation through multiple channels, most notably aggregate demand pressures, EXR movements and interactions with monetary policy, whose relevance is likely to be context-specific in transition economies. Accordingly, a more focused examination of inflation dynamics in highly remittance-dependent economies such as Tajikistan may help clarify how these transmission mechanisms operate in practice and complement the existing regional literature. Thus, this study aims to analyse the determinants of inflation, with a special focus on REM in Tajikistan, using quarterly data from 2004Q4 to 2022Q4. It controls for additional macroeconomic variables and employs rigorous estimation methods to provide insights relevant to policy development. The following section presents a description of the data and methodology used in this study, with the primary purpose of providing an overview.

Although the conventional ARDL model remains the preferred approach for identifying long-term cointegrating relationships, recent macroeconomic research emphasises the limitations of linear frameworks in capturing the complexities of inflation, especially in transition economies susceptible to structural change. ML techniques, particularly RF, have been used to capture non-linearities and high-dimensional interactions that are often overlooked by standard models (Medeiros et al., 2021; Aras & Lisboa, 2022). Using ensemble tree-based methods helps identify the hierarchical predictive importance of variables associated with inflation, which is crucial when external shocks and domestic policies interact in complex ways. In economies that rely heavily on REM, such as Tajikistan, the ‘spending effect’ might only trigger inflation once certain structural thresholds are surpassed. Using RF adds a useful layer of predictive validation (Goulet et al., 2022). This combined method is supported by evidence indicating that ML excel at filtering ‘noise’ from high-frequency macroeconomic data, thereby improving the stability of the long-term coefficients identified by the ARDL model. Drawing from these frameworks, this study addresses three research questions: (1) Is there a long-run association between REM and inflation in Tajikistan? (2) Do the EXR, MS, government expenditure, economic growth and INV exhibit significant long-run associations with inflation? (3) Which variables have the greatest predictive importance when non-linear interactions are considered? The ARDL approach addresses questions 1 and 2 by estimating long-run cointegrating relationships (Pesaran et al., 2001), while the RF addresses question 3 by capturing nonlinear interactions that linear models may obscure (Medeiros et al., 2021), together offering a more complete empirical picture than either method alone.

From a theoretical standpoint, REM can influence inflation through both demand-pull and monetary channels. Specifically, the influx of REM can increase overall demand, which may lead to inflationary pressures, particularly when domestic supply cannot keep pace. Conversely, REM might also contribute to an appreciation of the EXR or alterations in the MS, thereby complicating the overall dynamics of the transmission process. To empirically examine this dynamic, we specify the functional and econometric models outlined in Eqs (1) and (2), respectively.

Drawing inspiration from monetary theory and empirical macroeconomic inflation models (Chami et al., 2008; Acosta, Lartey & Mandelman, 2009), inflation is expressed as a function of REM, GE, MS, EXR, EG and INV. The functional form is specified as

In Eqs (1) and (2) INF represents inflation measured as the GDP deflator, REM denotes remittances as a percentage of GDP, GE indicates government expenditure as a percentage of GDP, MS refers to the money supply measured by M2 as a percentage of GDP, EXR signifies the exchange rate in somoni per USD, EG represents the real GDP growth rate as a percentage, and INV stands for investment gross capital formation as a percentage of GDP. In Eq. (2), ε and t stand for the error term and time, respectively, while β0 denotes the constant, and β1–β6 are the coefficients attached to the macroeconomic indicator of inflation.

This study uses the GDP deflator as the primary proxy for inflation to capture the multifaceted price dynamics inherent in Tajikistan’s domestic production structure. This methodological choice is necessitated by the significant role of REM in driving growth in the non-tradable sector, specifically, the construction industry expanded by a notable 22.5% in 2023. Such a sectoral surge aligns with the ‘Dutch Disease’ framework, wherein substantial financial inflows catalyse a ‘spending effect’, inflating the prices of non-tradable goods and potentially eroding the competitiveness of the tradable sector (Acosta et al., 2009). While the consumer price index (CPI) remains sensitive to fluctuations in global commodity prices, the GDP deflator offers a more systemic reflection of inflationary pressures in critical domestic segments, including the financial services sector, where robust remittance-related fees have sustained profitability. Consequently, the deflator effectively accounts for price shifts in domestic value-added spanning transport, trade and infrastructure, which function as the primary conduits through which Tajikistan’s record-high remittance inflows permeate the domestic economy. This choice is consistent with prior studies using the GDP deflator to capture economy-wide dynamics driven by external income flows (Acosta et al., 2009). We acknowledge, however, that CPI sub-indices (food, non-food, and core) may capture additional heterogeneity; future research using CPI-based measures would usefully extend this analysis.

This paper utilises quarterly data from 2004Q4 to 2022Q4. Quarterly data were chosen to capture more frequent economic fluctuations, including potential seasonal patterns inherent in Tajikistan’s remittance-driven economy. This higher frequency also provides a richer dataset for a more dynamic analysis of short- and long-run relationships. To facilitate this, original annual data for all variables were converted into quarterly frequency using EViews’ Quadratic-match average interpolation method, following the established procedures of Chow and Lin (1971) and Denton (1971). The following method was chosen to ensure a smooth and consistent disaggregation that preserves the mean of the annual series while accurately reflecting intra-year fluctuations. Quadratic-match average interpolation is a standard practice when high-frequency data are unavailable in developing economies (Chow & Lin, 1971; Denton, 1971). It preserves annual means and was applied uniformly across all variables to reduce differential bias, and post-estimation diagnostics confirm stability and no systematic distortion. We acknowledge that artificial smoothness remains a limitation, and future research using native quarterly data would further validate the findings. The resulting dataset enabled robust analysis using the ARDL bounds testing approach, a methodology well-suited for mixed-order integration series, as established by Pesaran et al. (2001). Information regarding INF, REM, GE, EG and INV is derived from the World Bank’s World Development Indicators, and MS is derived from the Asian Development Bank.

In contrast, EXR information is sourced from the International Monetary Fund’s International Financial Statistics. The variables are presented in real terms where relevant and have been seasonally adjusted. Table 1 provides information about the description and source of the data regarding the variables included in this study.

Variable information

| Variables | Description | Sources |

|---|---|---|

| INF | Inflation is proxied by the GDP deflator | World Bank |

| REM | Remittance inflows as % of GDP | World Bank |

| GE | Government expenditure as % of GDP | World Bank |

| MS | Broad money supply as % of GDP | Asian Development Bank |

| EXR | Exchange rate (somoni per USD) | International Financial Statistics |

| EG | Real economic growth rate in % | World Bank |

| INV | Gross capital formation, proxy for investment, % of GDP | World Bank |

Source(s): Authors’ creation.

EG, economic growth; GE, government spending; INV, investment.

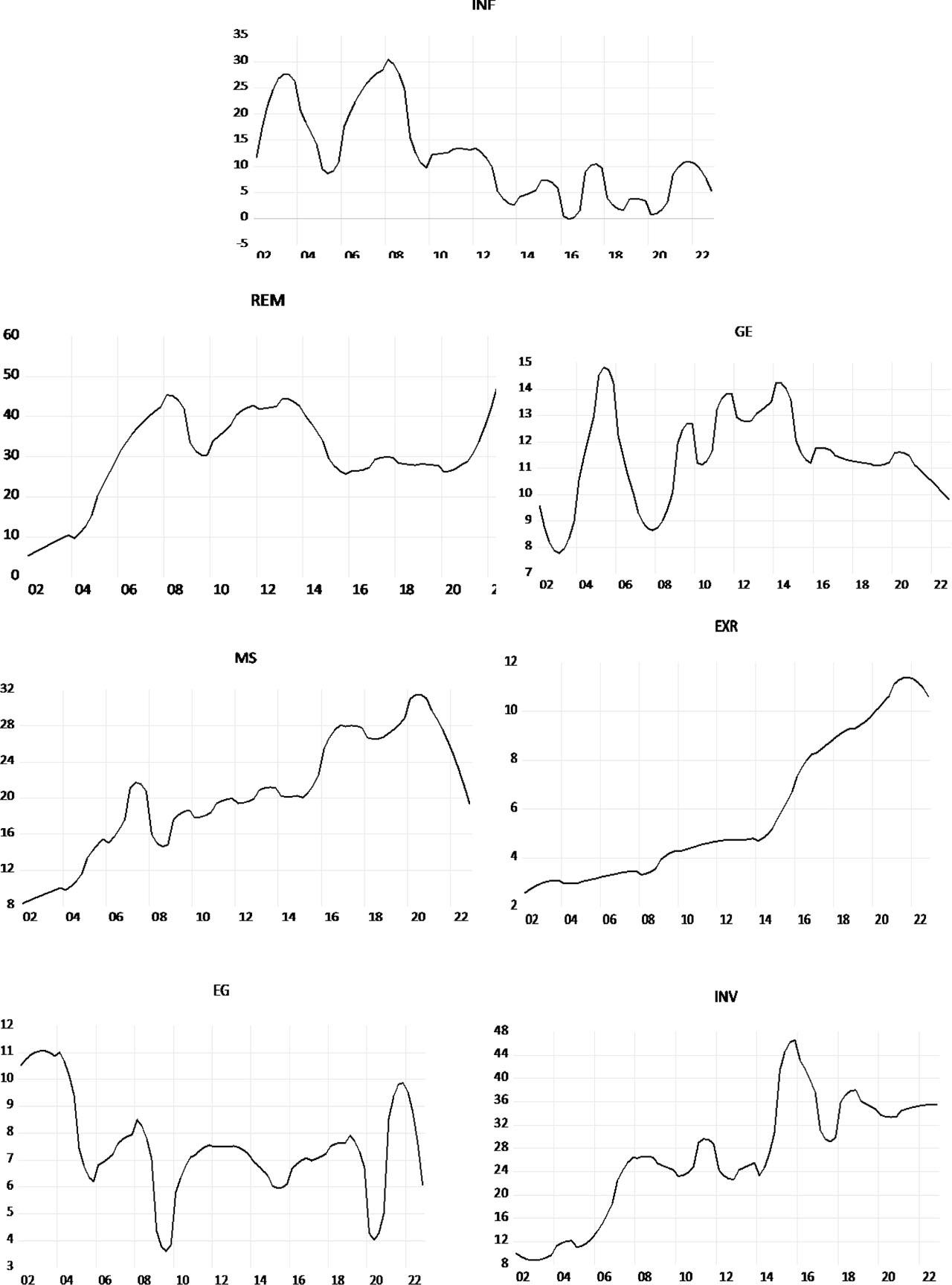

Figure 1 illustrates the time series trends of the variables considered in this study’s primary purpose from 2004Q4 to 2022Q4.

Trends of the variables. EG, economic growth; EXR, exchange rate; GE, government spending; INV, investment; MS, money supply; REM, remittances

We begin the empirical analysis by conducting unit root tests to determine the order of integration for each variable. Both the Augmented Dickey-Fuller (ADF) and the ADF with structural breaks tests are applied at the 10% significance level. Only variables that are I(0) or I(1) are included to satisfy ARDL requirements.

Following this, the Pesaran et al. (2001) bounds testing approach is applied to determine whether a long-run relationship exists between inflation and its macroeconomic determinants. If the F-statistic exceeds the upper bound critical value, we reject the null hypothesis of no cointegration.

The ARDL model provides a structured yet flexible framework for selecting optimal lag lengths, enabling the analysis to capture the dynamic and country-specific transmission mechanisms without imposing restrictive assumptions. It remains appropriate for relatively small samples, which is particularly important when working with quarterly data for a transition economy with limited historical coverage. The method also accommodates regressors integrated of different orders, as long as none are I(2), thereby aligning with the integration properties identified in the dataset. After establishing cointegration via the bounds testing procedure, we derive the associated Error Correction Model to link short-run fluctuations to the long-run equilibrium relationship. The error-correction term quantifies the speed at which inflation converges back to its equilibrium path following a transitory disturbance. This strategy allows the analysis to model long-run relationships and short-run adjustments within a unified and empirically consistent framework.

Post-estimation diagnostics are applied, including the Breusch-Godfrey LM test for serial correlation, the Breusch-Pagan-Godfrey test for heteroscedasticity and the Ramsey RESET test for model specification. To test for parameter constancy, the Cumulative Sum (CUSUM) and Cumulative Sum of Squares (CUSUMSQ) tests are conducted. Optimal lag lengths are selected using the Akaike Information Criterion, a standard practice in the ARDL literature (Pesaran et al., 2001). It should be acknowledged that the ARDL framework does not fully address potential endogeneity from bidirectional relationships between inflation and its regressors; the lagged structure partially mitigates but does not eliminate simultaneous bias. Results should, therefore, be interpreted as long-run associations, and future research employing IV or structural VAR approaches would more rigorously address identification. While variables such as the EXR have been proposed as instruments in the REM literature (Chami et al., 2008), the exclusion restriction is difficult to defend for Tajikistan, given that EXR has a large independent association with domestic inflation – confirmed by both its significant long-run ARDL coefficient (2.6336) and its dominant RF predictive importance (46%). EXR is, therefore, included as a regressor to control for EXR pass-through effects, which produces more reliable estimates of the remittance coefficient by partialing out this channel.

Furthermore, the RF ML technique is applied, which builds multiple decision trees by utilising different subsets of the data and randomly selecting a subset of features at each split. The final prediction is calculated as the average of the predictions from all individual trees. This approach is highly regarded for its robustness against overfitting and its ability to capture non-linear relationships. The application of the RF requires several steps, starting with data preprocessing. This preparation involves cleaning the dataset to remove or correct missing and duplicate values, handling outliers and ensuring that it is free from discrepancies that could misinform the model. After cleaning, the dataset is divided into x and y, where x is a set of columns comprising the independent variables, and y is a single column containing the dependent variable. The next step is to split the dataset into training and testing sets, which is a common practice in ML. This verifies the model’s accuracy and performance. An ML algorithm trains the model using the characteristics of the data, and its performance is assessed on a different dataset. Once the dataset is ready, an ML model object is generated. This model employs an algorithm to analyse the behaviour and relationships between the independent and dependent variables. Generally, these ML models are utilised via the scikit-learn library. The training set trains the model on the data, while the test set evaluates how well the model makes accurate predictions. Consequently, relevant performance metrics, such as accuracy and root mean square error, are used to assess the model’s effectiveness. ML involves a cycle of trials and enhancements. Following the assessment, the model can consistently improve by adjusting its parameters until a desired result is achieved. The predictive performance of an ML model is often compromised by either overfitting or underfitting. The presence of either issue limits the model’s ability to generalise to new data. Overfitting occurs when the model learns too much, picking up noise and irrelevant information from the dataset, thereby compromising its predictive accuracy. As a result, the model performs well on the training dataset but poorly on the test data, rendering it unsuitable for extrapolation. Conversely, underfitting happens when an ML model fails to learn sufficient information from the dataset. In this instance, the model performs poorly on the training dataset and, consequently, cannot be relied upon for new data. One of the main objectives of an effective model is to mitigate these issues by either acquiring more relevant data, removing variables that are least pertinent to the model or adjusting model parameters.

It should be noted that, while the ARDL framework determines the long-term equilibrium and the direction of influence of inflation determinants, incorporating RF enhances the paper’s empirical approach. Instead of merely serving as a robustness check, the RF model is used to reveal the hierarchical predictive structure and non-linear dependencies present in Tajikistan’s transition economy – insights that are often hidden by the averaging effect of linear coefficients. Therefore, RF is used as a complement to the ARDL approach’s findings.

The next part of the study summarises the empirical findings.

This part begins by displaying the results of the unit root tests for the series in Table 2, including both the ADF and the ADF with structural breaks. In Table 2, the t-statistics from the ADF and ADF with breaks tests indicate that all variables are stationary in first differences at the 1% and 5% significance levels.

Unit root test results

| ADF | ADF with breaks | |||

|---|---|---|---|---|

| Variable | Level | 1st Diff. | Level | 1st Diff. |

| INF | −1.807 | −4.191*** | −3.488 | −7.841*** (2011Q1) |

| REM | −0.06 | −2.492** | −3.099 | −4.405** (2020Q2) |

| GE | −0.621 | −4.622*** | −4.718** (2014Q1) | |

| MS | −0.353 | −2.247** | −3.162 | −4.711*** (2021Q2) |

| EXR | −0.406 | −2.310** | −3.222 | −4.222* (2021Q2) |

| EG | −1.450 | −3.400*** | −4.966** (2008Q3) | |

| INV | −0.674 | −2.597*** | −3.128 | −4.587** (2004Q1) |

Note: *** and ** denote the statistical significance at 1% and 5% levels, respectively.

ADF, augmented Dickey-Fuller; EG, economic growth; EXR, exchange rate; GE, government spending; INV, investment; MS, money supply; REM, remittances.

According to the ADF test, none of the variables – INF, REM, GE, MS, EXR, EG and INV – are stationary at the level, but all are stationary at first difference, confirming they are I(1). The ADF with structural breaks test shows that GE and EG are stationary at the level, making them I(0), while INF, REM, MS, EXR and INV are not stationary at the level but are stationary at the first difference, confirming they are I(1). This mixed order of integration, with GE and EG as I(0) and INF, REM, MS, EXR and INV as I(1), satisfies the prerequisites for ARDL bounds testing, as established by Pesaran et al. (2001).

The ADF test, which accounts for structural breaks as detailed in Table 3, reveals significant structural changes in the time series of the examined variables, highlighting key economic episodes that have influenced Tajikistan’s macroeconomic dynamics. For inflation (INF, break at 2011Q1), the identified structural break likely aligns with the global surge in commodity prices during 2010–2011, particularly in the food and energy sectors, which exerted upward pressure on prices in Tajikistan. As a net importer, the country depends heavily on REM to support household consumption (World Bank, 2011). REM, break at 2020Q2) exhibit a break linked to the Covid-19 pandemic, which disrupted global labour markets and led to a decline in remittance inflows to Tajikistan due to lockdowns and economic downturns in host countries such as Russia (International Monetary Fund [IMF], 2020). Government expenditure (GE, break at 2014Q1) corresponds with the economic slowdown in Russia triggered by falling oil prices and Western sanctions following geopolitical tensions, which constrained remittance inflows and, in turn, Tajikistan’s fiscal capacity given its reliance on remittance-driven revenues (European Bank for Reconstruction and Development [EBRD], 2014). The breaks in (MS, 2021Q2) and (EXR, 2021Q2) likely reflect post-Covid-19 monetary policy adjustments by the National Bank of Tajikistan and EXR fluctuations amid global economic recovery, as the economy responded to inflationary pressures stemming from supply chain disruptions (Asian Development Bank [ADB], 2021). EG, the break at 2008Q3 is associated with the global financial crisis, which substantially reduced remittance inflows and disrupted economic activity through weakened household spending and INV (World Bank, 2009). INV, break at 2004Q1 may be linked to economic reforms and liberalisation initiatives following the civil war in the early 2000s, which altered INV patterns by encouraging private sector participation and foreign direct INV (United Nations Development Programme [UNDP], 2005).

ARDL bounds test

| F-statistics | Significance level (%) | Lower bound | Upper bound |

|---|---|---|---|

| 8.954*** | 10 | 2.631 | 3.589 |

| 5 | 3.043 | 4.100 | |

| 1 | 3.966 | 4.630 |

Note: *** and ** denote the statistical significance at 1% and 5% levels, respectively.

Theoretically, these structural breaks underscore the asymmetric transmission of external shocks within a remittance-dependent framework. The 2008Q3 break represents a turning point in the Dutch Disease spending effect, where a contraction in remittance inflows curtailed demand for nontradable goods, contributing to a shift in the long-run relationship between external transfers and domestic price levels. The EXR break identified in 2021Q2 is consistent with standard overshooting dynamics described by Dornbusch (1976). The nominal EXR appears to have adjusted more rapidly than domestic prices following post-pandemic liquidity shocks, with inflation responding only gradually. These breaks also allow a comparison of macroeconomic dynamics in Tajikistan before and after major crises, including the Global Financial Crisis and the Covid-19 pandemic. By accounting for these breaks at the stationarity testing stage and confirming parameter stability through subsequent diagnostic tests, the ARDL framework accommodates potential structural instability characteristic of transition economies without imposing additional regime-specific controls. This helps ensure that the estimated coefficients reflect underlying economic relationships rather than being driven by episodic historical volatility.

In line with the ARDL literature, parameter stability is formally assessed using recursive residual diagnostics such as the CUSUM and CUSUM of squares tests (Brown, Durbin & Evans, 1975). As these tests do not indicate coefficient instability, there is no statistical evidence of regime-dependent parameter shifts within the estimated model. Consistent with the emphasis on parsimonious specification in ARDL frameworks, particularly in finite samples (Pesaran et al., 2001; Narayan, 2005), the inclusion of additive structural break dummies is, therefore, not warranted and may unnecessarily reduce degrees of freedom.

The ARDL-based bounds test is used to determine whether the variables are in a long-term relationship after the order of integration for the series has been determined. The results of the ARDL bounds cointegration test are shown in Table 3.

Since the F-statistic (8.954) exceeds both the lower bound critical value (2.631) and the upper bound critical value (3.966) at the 1% significance level, we reject the null hypothesis and conclude that there is a long-term relationship between the variables in the model.

We next apply the ARDL model to assess the long-term effects of the independent variables on inflation. The long-term outcomes of the ARDL approach are presented in Table 4, which confirms that REM have a significant impact on inflation at a 10% significance level. A 1% increase in remittance flows leads to a 0.2267% rise in inflation. This implies that REM boost aggregate demand and, consequently, places pressure on prices to rise. This evidence confirms conclusions in available literature that REM are one of the demand-led inflation drivers in developing economies. In addition, GE is shown to have a statistically significant negative long-term relationship with inflation, with a coefficient of −1.7010 (p = 0.0001), which aligns with the findings of George-Anokwuru and Ekpenyong (2020).

ARDL approach test results

| Variable | Coefficient | Std error | t-statistic | Prob | Conclusion |

|---|---|---|---|---|---|

| REM | 0.2267 | 0.1143 | 1.9831 | 0.0526 | Significant |

| GE | −1.7010 | 0.3958 | −4.2971 | 0.0001 | Significant |

| MS | −0.6213 | 0.1866 | −3.3297 | 0.0016 | Significant |

| EXR | 2.6336 | 0.7046 | 3.7375 | 0.0005 | Significant |

| EG | 0.3124 | 0.1522 | 2.0526 | 0.0452 | Significant |

| INV | 0.0342 | 0.0407 | 0.8390 | 0.4053 | Insignificant |

| TREND | −0.5635 | 0.1102 | −5.1130 | 0.0000 | Significant |

| ECT (-1) | −0.7582 | 0.8409 | −9.0175 | 0.0000 | Significant |

EG, economic growth; EXR, exchange rate; INV, investment; MS, money supply; REM, remittances.

GE negatively impacts inflation in the long run. Although this result may seem counterintuitive, it likely reflects that GE in Tajikistan is directed primarily toward supply-enhancing uses of infrastructure, healthcare and agriculture that alleviate bottlenecks and restrain prices over the long run, consistent with the FTPL (Leeper, 1991) and evidence from other developing economies where capital-oriented spending moderates inflation (George-Anokwuru & Ekpenyong, 2020). Similarly, the MS is negatively and significantly associated with inflation (−0.6213; p = 0.0016), consistent with effective monetary sterilisation by the National Bank of Tajikistan offsetting remittance-driven liquidity through reserve requirements and foreign exchange interventions (Chami et al., 2008; Narayan et al., 2011). The EXR is positively and significantly associated with inflation, with a long-run coefficient of 2.6336 (p = 0.0005), consistent with EXR pass-through to import prices in small open economies such as Tajikistan (De Alwis, Athukorala & Dewasiri, 2025). Additionally, EG exhibits a positive and statistically significant long-run effect on inflation, with a coefficient of 0.3124 (p = 0.0452). This suggests that a 1% increase in EG raises inflation by approximately 0.3124%, reflecting demand-driven inflationary pressures in an expanding economy with supply constraints. The coefficient for INV is positive but statistically insignificant at (0.0342; p = 0.4053). These results indicate that capital accumulation might put upward pressure on prices; however, its effect on inflation in this data in the long run is statistically insignificant under this model. Finally, the trend variable is negative and highly significant (−0.5635; p < 0.000), likely reflecting structural improvements or declining inflationary momentum over the sample period. The ECT coefficient of −0.7582 (p < 0.001) indicates that approximately 75.8% of any deviation from long-run equilibrium is corrected within one quarter. This fast speed of adjustment is economically plausible in Tajikistan’s remittance-dependent economy, where large, volatile inflows generate rapid price adjustments consistent with ECT magnitudes documented in other small open economies with significant external income flows (Narayan et al., 2011). The significant ECT, alongside stable CUSUM diagnostics, confirms the validity of the long-run cointegrating relationship.

Table 5 displays the findings related to serial correlation, heteroscedasticity and misspecification. The probability values associated with the test statistics indicate that the ARDL model does not have issues of serial correlation, heteroscedasticity or misspecification. Additionally, the results from the CUSUM and CUSUM of squares tests confirm the model’s stability at a 5% significance level. Figures 2 and 3 illustrate the outcomes of the model’s stability tests. Consequently, it can be concluded that the empirical model is adequately robust for formulating policies aimed at regulating inflation.

Result of the CUSUM

Result of the CUSUM of squares.

Diagnostic and stability tests

| Test | Null hypothesis | Test stat. (prob) | Conclusion |

|---|---|---|---|

| BPG | Homoscedasticity | 0.2613 (0.9991) | The model is homoscedastic |

| BGLM | No serial correlation | 2.2684 (0.1140) | No evidence of serial correlation |

| Ramsey | No misspecification errors | 0.6108 (0.4381) | No misspecification error |

| CUSUM | Stable | ||

| CUSUM SQ | Stable |

Source(s): Authors’ own work.

BGLM, Breusch-Godfrey LM; BPG, Breusch-Pagan-Godfrey.

The final step of the empirical analysis involves applying RF to assess the extent to which each feature contributes to predicting the target variable. Before applying the RF, the dataset was divided into training and testing subsets, with 70% of the data allocated for training and 30% reserved for testing. The Scikit-learn library was employed to invoke the splitting algorithm, train models and evaluate metrics. The results are shown in Figure 4.

Feature importance. EG, economic growth; EXR, exchange rate; INV, investment; MS, money supply; REM, remittances.

As illustrated in Figure 4, EXR emerges as the most significant predictor of INF, representing 46% of the model’s predictive significance. This is subsequently followed by GE, REM, MS, INV and EG, which account for 33%, 12%, 5%, 2% and 2%, respectively. These percentages illustrate the utility of these features in reducing prediction error within the model, offering predictive insights rather than establishing structural economic causality or proportional economic impact.

Importantly, the hierarchical order of predictive significance derived from the RF model closely corresponds with the absolute magnitudes of the long-term coefficients estimated in the ARDL model (see Table 4). EXR exhibits the largest absolute ARDL coefficient (2.6336) and accordingly commands the highest predictive importance within the RF model at 46%. Likewise, GE demonstrates the second-largest absolute ARDL effect (−1.7010) and ranks second in RF importance with 33%. INV, which is statistically insignificant in the ARDL framework (coefficient of 0.0342), is appropriately positioned at the lowest level of the RF predictive hierarchy at 2%. The alignment between the linear, structural ARDL estimates and the non-linear, algorithmic RF predictions enhances the robustness of the results, corroborating that EXR and GE are the primary macroeconomic influences on inflation dynamics in Tajikistan across both analytical approaches.

The performance of an ML model can be hindered by issues of overfitting or underfitting. In either case, the model’s predictions are flawed and cannot be trusted. Therefore, we conducted a test to identify any potential overfitting or underfitting in the model. Since the accuracies on the training data (0.94) and test data (0.85) do not differ significantly, the absence of overfitting and underfitting is confirmed. Therefore, the results of the RF can be trusted to be generalised well to new data.

This study investigates the long-run determinants of inflation in Tajikistan using the ARDL approach applied to quarterly data from 2004Q4 to 2022Q4. The analysis examines the impact of REM, government expenditure, broad MS, the EXR, EG and INV on inflation, measured by the GDP deflator, in a small open economy in which REM account for over 30% of GDP. The findings establish a stable long-run cointegrating relationship among the variables, with stationarity tests incorporating structural breaks in 2008–2009 due to the global financial crisis confirming the model’s robustness. The results reveal that REM and EXR depreciation drive inflation upward, fuelled by remittance-induced household consumption and increased input costs from currency depreciation, respectively. Conversely, government expenditure and MS mitigate inflationary pressures, reflecting strategic fiscal INVs in supply-enhancing sectors, such as infrastructure and agriculture, and effective monetary sterilisation by the National Bank of Tajikistan to manage remittance-driven liquidity. EG contributes positively to inflation, indicating demand-driven pressures, while INV exerts a negligible effect, suggesting REM primarily support consumption rather than capital accumulation. A declining inflation trend suggests the need for structural reforms or policy interventions. The results suggest that REM contribute to long-run inflation in Tajikistan, through consumption-driven demand pressures, consistent with Narayan et al. (2011) and Abdul-Mumuni and Quaidoo (2016). Unlike Chami et al. (2008) and Basnet et al. (2022), who report inflation-reducing effects via EXR appreciation, we find that depreciation amplifies imported price pressures, highlighting the context-specific role of the EXR. Government expenditure and monetary sterilisation appear to moderate inflationary pressures, in line with the FTPL (Leeper, 1991) and prior evidence on conditional fiscal and monetary effects (Akinbobola, 2012; George-Anokwuru & Ekpenyong, 2020). Overall, the findings suggest that the remittance-inflation relationship depends on national structural and policy contexts, reinforcing the need for country-specific analysis in transition economies.

This study contributes to the literature by providing country-specific evidence on inflation dynamics in a highly remittance-dependent post-Soviet economy. The study examines how standard inflation determinants operate within Tajikistan’s distinctive institutional context, marked by large remittance inflows, ongoing price liberalisation and weak supply responsiveness. By shifting attention from growth to price stability, the analysis highlights inflation as a core macroeconomic challenge in economies where household consumption depends heavily on external income. The findings complement cross-country studies by showing that the long-run associations between REM, fiscal policy and EXR movements with inflation depend on national economic structures and policy settings. Additionally, it applies an ML-based RF technique to confirm the results obtained from ARDL and explore feature importance. RF outcomes complement the findings of the ARDL approach by affirming that the EXR serves as the most significant predictor of inflation in Tajikistan, with government expenditure ranking second. Notably, the hierarchy of predictive significance within the RF model closely corresponds to the magnitude of the long-term ARDL coefficients, with the EXR and government expenditure exerting the most influence in both models. This congruence offers strong, cross-methodological validation of the principal factors driving inflation in Tajikistan. A key limitation is that potential endogeneity cannot be fully addressed within the ARDL framework, as feedback loops between inflation and REM may influence the results. While the ARDL framework’s lagged structure reduces bias, it does not fully eliminate the risk of simultaneous causality among the policy variables.

The analysis focuses on aggregate national-level data and does not distinguish between formal and informal remittance channels, which may operate differently in shaping inflationary pressures. Furthermore, the standard ARDL framework does not address potential endogeneity; the lagged structure reduces but does not eliminate simultaneous bias. Future studies could explore remittance channels separately and consider alternative frameworks. In particular, the Non-linear Autoregressive Distributed Lag model proposed by Shin, Yu and Greenwood-Nimmo (2014) would allow investigation of asymmetric short-run and long-run effects of remittance inflows on inflation. IV approaches or structural VAR frameworks could also help establish stronger identification. Future research using native quarterly data, should they become available for Tajikistan, would further strengthen confidence in the findings. These findings highlight the need for dynamic policy measures to address the inflationary associations of EXR fluctuations, government expenditure and REM, while leveraging fiscal and monetary policies to achieve price stability. Policymakers should focus on enhancing supply capacity through INVs in productive sectors and strengthening monetary tools to absorb excess liquidity, fostering sustainable growth alongside stable prices.

The empirical results of this research highlight the considerable inflationary pressures arising from remittance inflows in Tajikistan, indicating the need for a coordinated policy framework that balances their economic benefits with macroeconomic stability. To address these issues, policymakers should prioritise integrating remittance flows into the National Bank of Tajikistan’s inflation-targeting strategy. By incorporating REM into forecasting models and policy simulations, the central bank can enhance its ability to predict and mitigate demand-driven price pressures, thereby improving the effectiveness of monetary policy. At the same time, promoting the productive utilisation of REM is crucial to mitigate its inflationary effects. Initiatives that direct REM through formal financial institutions and encourage their INV in savings or non-consumption-driven sectors, such as small enterprises or technology, can lessen immediate demand pressures while fostering sustainable growth.

The results show that REM and EXR depreciation increase inflation, while targeted GE and monetary measures help moderate price pressures. Policies should integrate remittance flows into forecasting models, promote their productive use and strengthen supply-side capacity through strategic INVs. Stabilising the EXR and prioritising productive fiscal expenditures can further reduce inflationary pressures. These measures directly respond to the mechanisms observed in the study, aligning policy actions with evidence from Tajikistan’s macroeconomic context.

To further ease inflationary constraints, the government should focus on enhancing domestic supply and production capabilities. Strategic INVs in infrastructure, agriculture and manufacturing will help address supply-side limitations, build resilience against external shocks and reduce price volatility. Given the significant impact of EXR depreciation on inflation, maintaining stable EXRs is also vital. To mitigate inflationary pressures arising from EXR depreciation, the National Bank of Tajikistan should prioritise targeted foreign exchange interventions, bolster reserve accumulation and pursue structural reforms to enhance export competitiveness, thereby stabilising domestic prices amid currency volatility. Complementing these efforts, the negative long-run relationship between government expenditure and inflation highlights the counter-inflationary potential of fiscal policy. By prioritising productive and social INVs in sectors such as healthcare, education and rural development, policymakers can not only reinforce price stability but also foster sustainable economic growth, leveraging fiscal measures to support Tajikistan’s macroeconomic resilience.