Introduction

1.

Stock investments offer investors not only capital gains stemming from firms' growth potential and profitability but also a predictable cash flow through regular dividend payments. Dividend policy provides an important signal regarding a company's corporate governance quality, financial stability, and long-term growth prospects, forming an essential component of firm valuation (Baker & Weigand, 2022). Particularly during periods of elevated market volatility, the attractiveness of dividend-paying firms increases, making dividend policies more influential on investor decision-making (Fama & French, 2021).

Recent trends in Türkiye's capital markets show a rising interest in dividend-paying firms. As of 2024, dividend yield has become a key investment criterion in Borsa İstanbul, especially within sectors such as energy, automotive, durable consumer goods, and technology (BIST, 2024). Increasing macroeconomic uncertainties have enhanced the role of cash-based value distribution to investors, thus intensifying academic and practical interest in dividend-oriented models (OECD, 2023).

One of the most widely used valuation methods centered on dividend policy is the Constant Growth Dividend Discount Model (DDM), originally developed by Gordon and Shapiro (1956). The model values a stock by discounting future dividends under the assumption of a constant growth rate. It is particularly applicable to firms with stable dividend histories and has long been considered a fundamental valuation tool within modern finance (Damodaran, 2023; Gordon, 1959).

International literature generally suggests that constant-growth models effectively explain stock prices for firms with stable dividend patterns. Studies such as Lee, Naranjo, and Nimalendran (2021) and Han (2025) show that the DDM produces reliable results, especially in sectors characterized by stable cash flows. Conversely, other studies argue that the model performs poorly in industries where dividend growth is volatile (Vyas & Sapra, 2023).

In the Turkish context, existing findings largely affirm the model's effectiveness for firms with consistent dividend payouts (Arslankaya & Toprak, 2021; Çoban, 2023; Camgöz, 2022). However, comprehensive long-term empirical research on the DDM remains limited, underscoring the need for further investigation.

This study aims to fill this gap by testing the reliability of the Constant Growth DDM using data from 23 BIST-listed companies that paid regular dividends between 2014 and 2023. The analysis compares theoretical stock prices generated by the model with actual market prices, employing sMdAPE and the Wilcoxon Signed-Rank test to evaluate predictive accuracy.

Literature Review

2.

Dividend policy is a strategic decision that determines how much of a firm's periodic profit will be distributed to shareholders. Despite Modigliani and Miller's (1961) dividend irrelevance theorem, the behavioral finance literature and empirical evidence indicate that dividends serve as an important signal for investors. Firms that regularly distribute dividends create an impression of sustainable profitability and corporate credibility, which positively influences stock value particularly in emerging markets (Baker & Weigand, 2022).

In the Turkish market, dividend payments emerge as a factor that reduces investors' risk perception and increases the predictability of cash flows. The heightened market volatility in the post–COVID-19 period has further amplified the significance of dividend policies in corporate valuation (OECD, 2023).

Jareño and Navarro (2007) examined data from 115 companies listed on the Spanish Stock Market for the period 1993–2005 and found that DDM-based valuations closely matched actual stock prices, achieving nearly 50% similarity.

İnam (2011) analyzed data from four companies listed on Borsa İstanbul (BIST) for the period 2006–2010 and found that valuations obtained using the Geometric Brownian Motion method were consistent with actual stock prices, indicating that the method produced reliable results.

Olweny (2011), using data from 18 selected companies listed on the Nairobi Securities Exchange for the 1995–1999 period, found that DDM valuations matched actual stock prices in only three companies, while the remaining fifteen showed discrepancies, concluding that the method was not reliable for determining intrinsic value in that market.

Bozacı (2012) reported that both the Price/Earnings and Market Value/Book Value methods provided valuations consistent with actual stock prices for Garanti Bank (2007–2011), indicating the reliability of these approaches.

İlarslan (2014) demonstrated that the Markov Chains method, applied to data from ten BIST-listed banks for the year 2010, generated valuations consistent with actual stock prices and provided reliable results.

Ivanovski, Ivanovska, and Ivanovska (2015) showed that DDM valuations based on data from the ALK company listed on the Macedonian Stock Exchange for 2008–2010 aligned with actual prices, concluding that the method provides reliable intrinsic value estimates.

Özçalıcı (2017), using data from three companies listed on the New York Stock Exchange for 2001–2016, found that Extreme Learning Machines produced estimates consistent with actual stock prices and yielded reliable results at a rate of 59.32%.

Gacus and Hinlo (2018) demonstrated that DDM-based valuations for 15 selected companies listed on the Philippine Stock Exchange (2012–2016) matched actual stock prices and that the model was reliable for intrinsic value estimation.

Ong'ele (2018), analyzing nine banks listed on the Nairobi Securities Exchange for 2002–2015, found that DDM valuations differed significantly from observed prices, concluding that the model produced weak results and recommending the use of multi-factor flexible models better suited to market conditions.

Iyer and Paul (2019) examined data from the top five companies listed on the Indian National Stock Exchange during 2009–2018 and found that DDM valuations closely matched actual stock prices, confirming the model's reliability.

Sutjipto, Setiawan, and Ghozali (2020) found that both DFC and DDM valuations aligned with actual stock prices for 43 selected companies listed on the Indonesia Stock Exchange (2014–2019), and that DDM was more reliable than DFC for determining intrinsic value.

Dukalang, Koni, and Mokoagow (2021) evaluated two banks listed in the Jakarta Islamic Index (2016–2020) and concluded that BRIS stock was overvalued and BTPS stock undervalued under DDM, whereas FCFF results indicated the opposite, showing the sensitivity of valuation outcomes to model selection.

Arslankaya and Toprak (2021) demonstrated that Machine Learning and Deep Learning models produced valuations consistent with actual stock prices for Ereğli Demir ve Çelik (2014–2020), with Random Forest Regression performing best and Polynomial Regression performing worst.

Kleriawan and Dwiyono (2021) found that DDM valuations for 11 companies listed on the Indonesia Stock Exchange (2014–2018) were consistent with actual stock prices.

Febriani et al. (2021) showed that DDM valuations for three companies listed in the IDX index (2011–2020) matched observed market prices.

Camgöz (2022), using data from 25 BIST-listed companies (2011–2021), found—via Hatemi-J asymmetric bootstrap causality and Toda–Yamamoto tests—that dividend yield caused stock prices for seven companies, with the Hatemi-J test identifying fewer causal relationships than Toda–Yamamoto.

Vikas, Charithra, and Sharma (2022) found that DDM valuations for ten mid-sized Indian firms (2021) differed significantly from actual prices, concluding that the model did not yield reliable intrinsic value estimates for these companies.

Çoban (2023), analyzing eight companies from various sectors in Türkiye (2013–2021), found that RNN, LSTM, and GRU models achieved high predictive accuracy when trained on Symlets wavelet-transformed data.

Umamik and Matnin (2023) showed that DDM valuations for three companies listed on the Indonesia Stock Exchange (2010–2014) were consistent with market prices.

Yulianto (2024) demonstrated that DDM and FCFF valuations for one Indonesian company (2019–2023) aligned with actual stock prices, but RMSE results indicated that FCFF provided more accurate estimates than DDM.

Hutagalung and Alexandri (2024) analyzed eight companies listed in the LQ45 Index (2018–2022) and found that both DDM and DFC valuations were consistent with actual stock prices, with DDM outperforming DFC in terms of accuracy.

Han (2025) concluded that DDM valuations for two U.S.-listed companies (2016–2023) were consistent with market prices, supporting the model's reliability.

Research Methodology And Findings

3.

Purpose and Scope of the Research

3.1.

The primary aim of this study is to test the reliability of the Constant Growth Dividend Discount Model (DDM) in valuing the stock prices of companies that have regularly distributed dividends over the past ten years. The study analyzes data from 23 selected firms. Although 30 companies in Türkiye have paid regular dividends during the last decade, only 23 were included in the analysis due to data availability and consistency considerations.

The dataset covers a ten-year period from 2014 to 2023. Variables for the years 2014–2023 were obtained from companies' official websites and statistical data published by Fintables and Investing Türkiye. The study employs the DDM, symmetric median absolute percentage error (sMdAPE), and the Wilcoxon Signed-Rank Test.

Three main analytical approaches were used in the study:

Constant Growth Dividend Discount Model (DDM)

The theoretical stock values of the companies were calculated using the Gordon–Shapiro model:

Where:P0: Current stock price

D1: Expected dividend for the following year

r: Required rate of return (cost of equity)

g: Dividend growth rate

The dividend growth rate was calculated using the geometric mean method, while the required rate of return was estimated by considering firms' return on equity (ROE) and sectoral risk premiums.

Symmetric Median Absolute Percentage Error (sMdAPE)

To assess model forecasting performance, sMdAPE was preferred over traditional MAPE because it evaluates positive and negative deviations symmetrically. This metric eliminates one-sided error bias by assigning equal weight to overvalued and undervalued estimates.

An sMdAPE value below 30% indicates strong predictive power (Armstrong, 2022).

Statistical Fit Test: Wilcoxon Signed-Rank Test

The non-parametric Wilcoxon Signed-Rank test was applied to determine whether a statistically significant difference exists between DDM estimates and actual market prices.

p < 0.05: significant difference

p ≥ 0.05: no significant difference

Research Limitations

The study was conducted under several limitations:

DDM can only be applied to dividend-paying companies.

The assumption of constant dividend growth may not fully reflect real-world dividend patterns.

High volatility in Türkiye's capital markets may influence the calculation of required returns.

Comparison with alternative valuation models is beyond the scope of this study.

Companies Included in the Research

Table 1.

Companies Analyzed in the Study

| No | Company Name | Code |

|---|---|---|

| 1 | Akçansa Çimento Sanayi ve Ticaret A.Ş. | AKCNS |

| 2 | Akmerkez Gayrimenkul Yatırım Ortaklığı A.Ş. | AKMGY |

| 3 | Aksa Akrilik Kimya Sanayii A.Ş. | AKSA |

| 4 | Alarko Holding A.Ş. | ALARK |

| 5 | ASELSAN Elektronik Sanayi ve Ticaret A.Ş. and Subsidiaries | ASELS |

| 6 | Aygaz A.Ş. | AYGAZ |

| 7 | Anadolu Hayat Emeklilik A.Ş. | ANHYT |

| 8 | BİM Birleşik Mağazalar A.Ş. | BIMAS |

| 9 | EİS Eczacıbaşı İlaç, Sınai ve Finansal Yatırımlar A.Ş. | ECILC |

| 10 | Eczacıbaşı Yatırım Holding Ortaklığı A.Ş. | ECZYT |

| 11 | Enka İnşaat ve Sanayi A.Ş. | ENKAI |

| 12 | Ford Otomotiv Sanayi A.Ş. | FROTO |

| 13 | İndeks Bilgisayar Sistemleri Mühendislik Sanayi ve Ticaret A.Ş. | INDES |

| 14 | İş Yatırım Menkul Değerler A.Ş. | ISMEN |

| 15 | Jantsa Jant Sanayi ve Ticaret A.Ş. | JANTS |

| 16 | Koç Holding A.Ş. | KCHOL |

| 17 | Nuh Çimento Sanayi A.Ş. and Subsidiaries | NUHCM |

| 18 | Polisan Holding A.Ş. | POLHO |

| 19 | Pınar Entegre Et ve Un Sanayii A.Ş. | PETUN |

| 20 | Hacı Ömer Sabancı Holding A.Ş. | SAHOL |

| 21 | Selçuk Ecza Deposu Ticaret ve Sanayi A.Ş. | SELEC |

| 22 | Türkiye Şişe ve Cam Fabrikaları A.Ş. | SISE |

| 23 | Tofaş Türk Otomobil Fabrikası A.Ş. | TOASO |

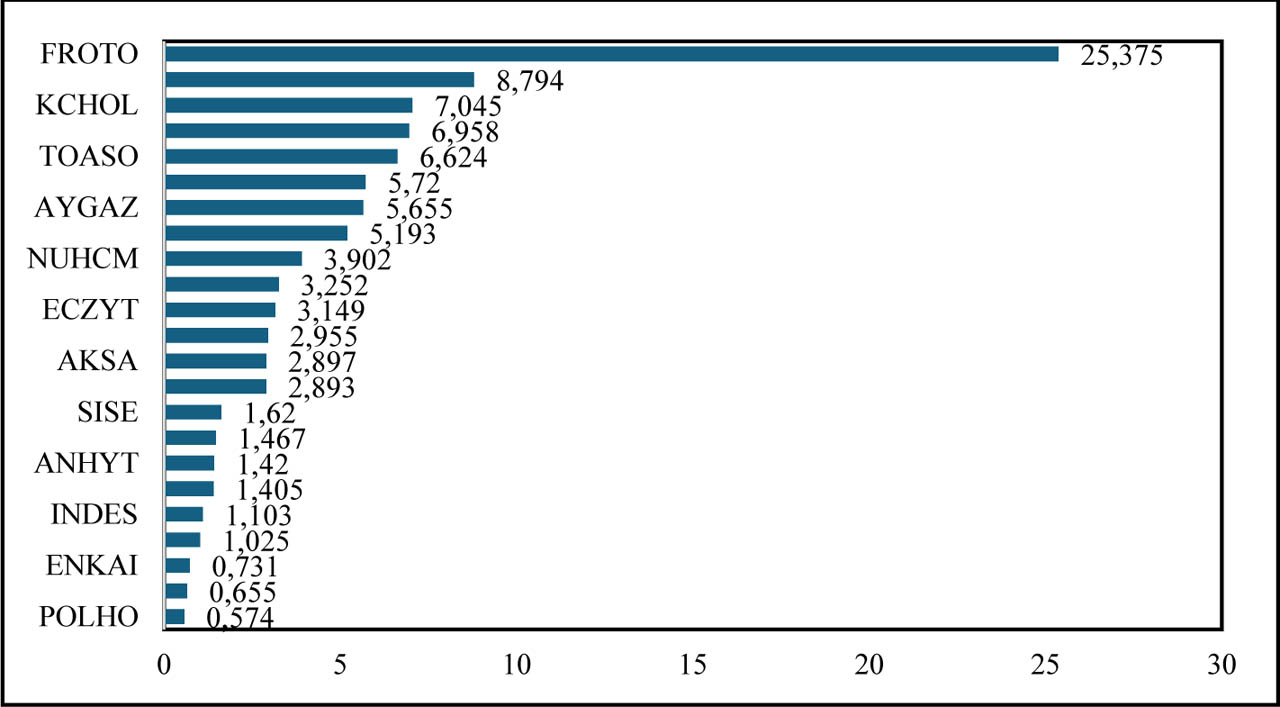

In Figure 1, the highest average dividend per share is observed for FROTO at 3.921 TL, while the lowest value belongs to POLHO at 0.056 TL.

Figure 1.

Average Dividend per Share

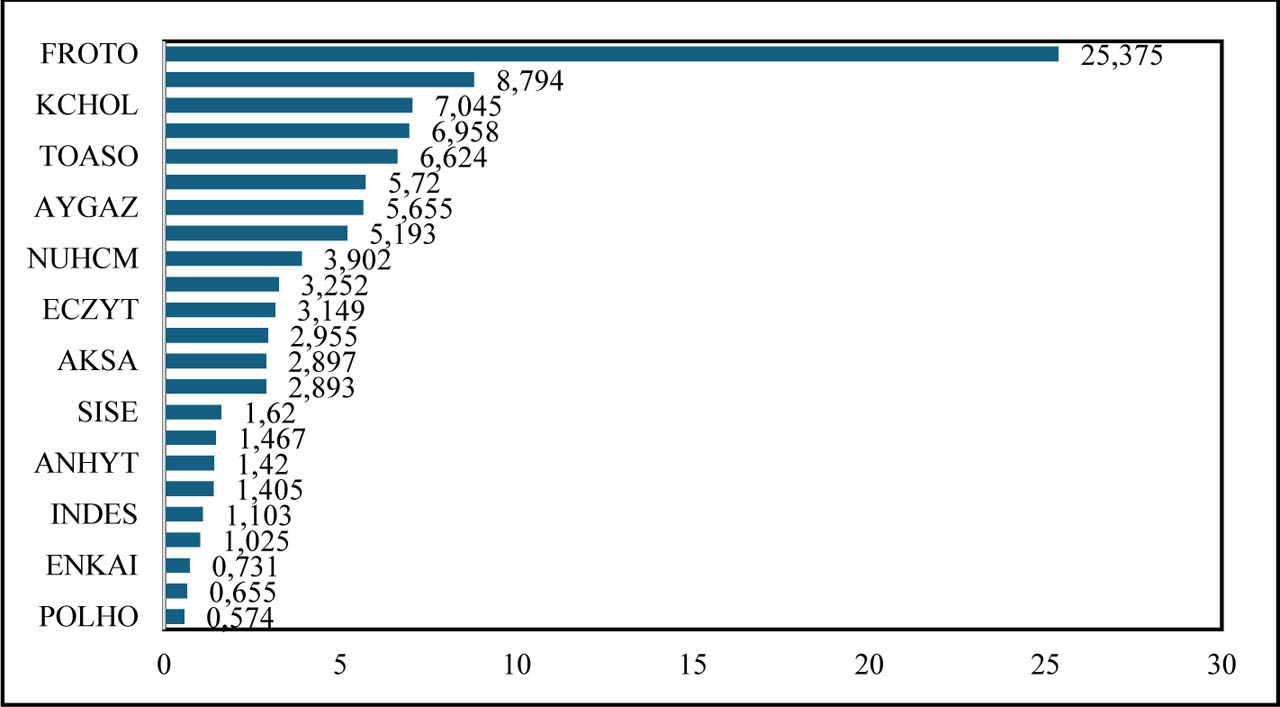

In Figure 2, the highest average earnings per share is observed for FROTO at 25.375 TL, while the lowest value belongs to POLHO at 0.0574 TL.

Figure 2.

Average Earnings per Share

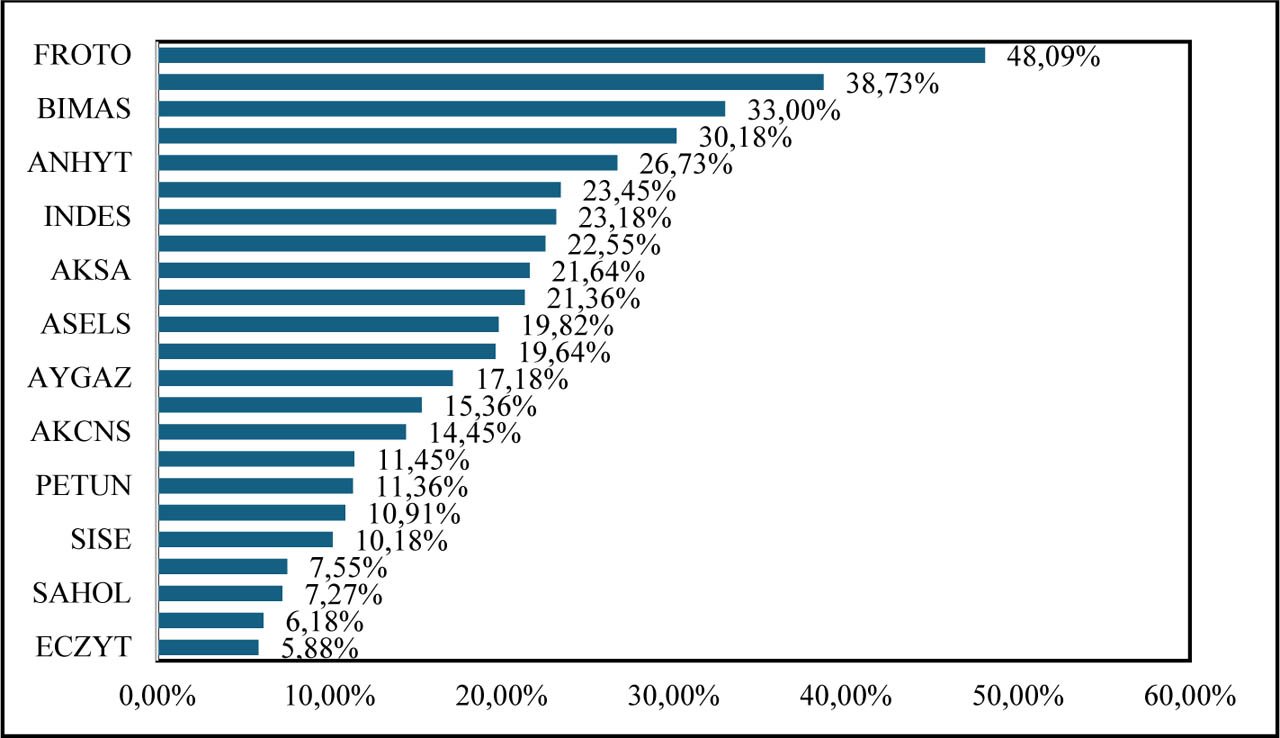

In Figure 3, the highest average ROE is observed for FROTO at 48.09%, while the lowest ROE belongs to POLHO at 5.88%.

Figure 3.

Average ROE (%)

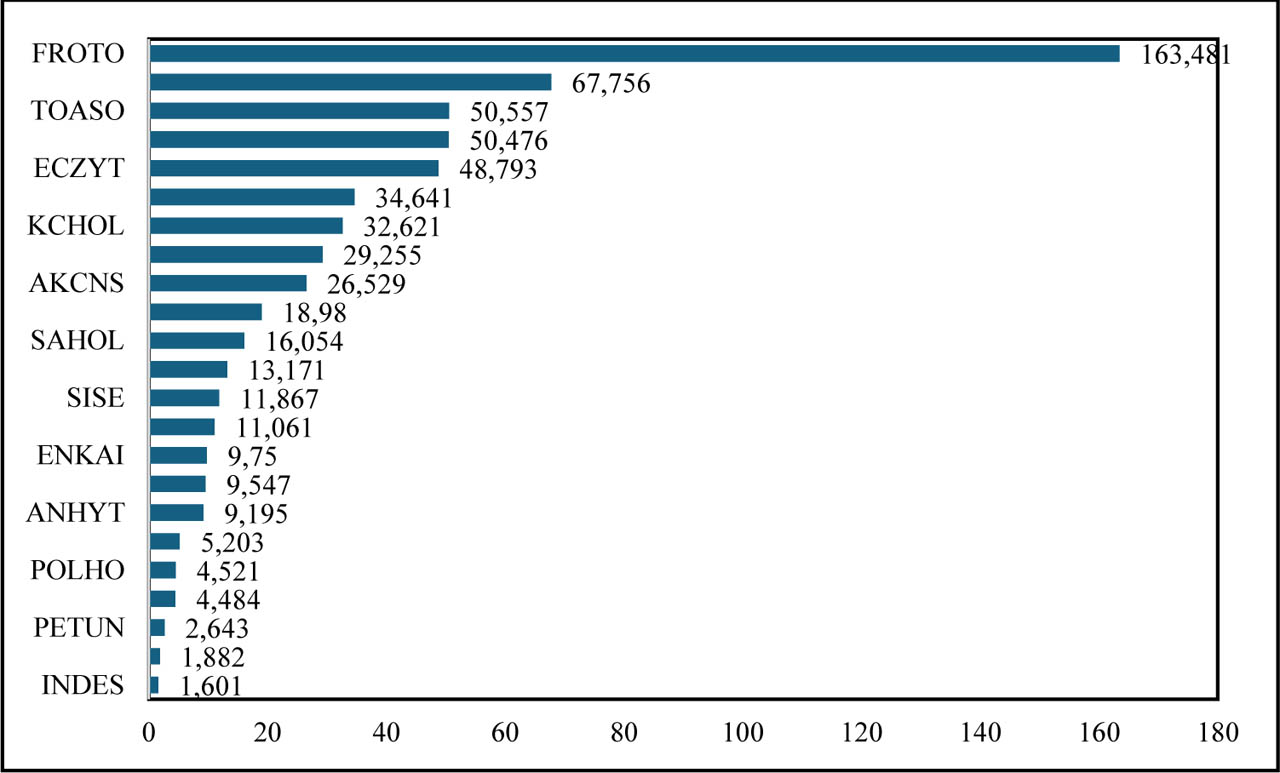

In Figure 4, the highest average stock price is observed for FROTO at 163.481 TL, while the lowest average stock price belongs to INDES at 1.601 TL.

Figure 4.

Average Stock Price

Findings

3.2.

Based on the data presented in Table 2, it is observed that the expected dividend payments for the following year show a consistent upward trend. As of 2023, the highest expected dividend payment belongs to FROTO, while the lowest expected dividend payment is associated with ASELS. Examining the dividend growth rates reveals that the highest growth rate is 39.17% for FROTO, whereas the lowest growth rate is 3.56% for ECILC.

Table 2.

Company-Specific Parameters

Expected Dividend Payment for the Following Year

| Company Code / Year | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | Dividend Growth Rate (%) | Expected Rate of Return (%) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| AKCNS | 0,71 | 1,08 | 1,21 | 1,01 | 0,60 | 0,62 | 0,22 | 0,50 | 0,45 | 1,36 | 5.06 | 11.84 |

| AKMGY | 1,41 | 0,23 | 1,88 | 1,07 | 0,85 | 0,62 | 1,34 | 0,54 | 0,86 | 4,39 | 17.23 | 23.91 |

| AKSA | 0,53 | 0,60 | 0,72 | 0,93 | 0,98 | 1,00 | 0,71 | 0,98 | 2,53 | 2,28 | 12.77 | 193.92 |

| ALARK | 0,06 | 0,06 | 0,23 | 0,29 | 0,24 | 0,17 | 0,08 | 0,15 | 0,35 | 0,24 | 17.70 | 22.13 |

| ASELS | 0,05 | 0,12 | 0,01 | 0,03 | 0,03 | 0,05 | 0,05 | 0,19 | 0,22 | 0,08 | 18.05 | 20.42 |

| AYGAZ | 0,51 | 0,32 | 0,94 | 1,36 | 1,22 | 1,07 | 0,41 | 0,51 | 0,72 | 1,04 | 9.62 | 17.30 |

| ANHYT | 0,13 | 0,15 | 0,23 | 0,31 | 0,37 | 0,31 | 0,65 | 0,86 | 1,18 | 1,43 | 16.28 | 21.80 |

| BIMAS | 0,32 | 0,44 | 0,55 | 0,63 | 0,84 | 0,42 | 0,56 | 2,44 | 1,95 | 3,58 | 23.82 | 25.93 |

| ECILC | 0,08 | 0,07 | 0,34 | 0,41 | 0,18 | 0,25 | 0,07 | 0,20 | 0,32 | 0,39 | 3.56 | 9.76 |

| ECZYT | 0,09 | 0,09 | 1,04 | 1,02 | 0,66 | 0,65 | 0,42 | 1,13 | 1,56 | 1,78 | 3.87 | 9.74 |

| ENKAI | 0,07 | 0,06 | 0,03 | 0,04 | 0,04 | 0,13 | 0,18 | 0,31 | 0,45 | 0,35 | 6.26 | 8.19 |

| FROTO | 0,49 | 0,59 | 0,92 | 1,24 | 1,31 | 1,40 | 3,87 | 5,61 | 9,26 | 41,29 | 39.17 | 41.74 |

| INDES | 0,05 | 0,35 | 0,56 | 0,63 | 1,03 | 0,42 | 0,34 | 0,22 | 0,26 | 0,75 | 9.05 | 73.73 |

| ISMEN | 0,07 | 0,12 | 0,09 | 0,12 | 0,29 | 0,26 | 0,46 | 1,09 | 1,41 | 2,21 | 16.05 | 55.76 |

| JANTS | 0,62 | 0,80 | 0,28 | 0,77 | 1,53 | 2,16 | 5,12 | 4,67 | 0,93 | 2,70 | 13.66 | 165.27 |

| KCHOL | 0,15 | 0,17 | 0,27 | 0,30 | 0,32 | 0,36 | 0,20 | 0,55 | 1,03 | 1,72 | 9.82 | 11.45 |

| NUHCM | 0,35 | 0,73 | 0,76 | 0,79 | 0,79 | 0,63 | 0,75 | 1,53 | 2,69 | 1,03 | 13.65 | 20.03 |

| POLHO | 0,03 | 0,03 | 0,04 | 0,04 | 0,05 | 0,03 | 0,01 | 0,01 | 0,03 | 0,37 | 10.44 | 11.85 |

| PETUN | 0,67 | 0,55 | 0,87 | 0,89 | 0,45 | 0,80 | 0,62 | 1,37 | 1,19 | 3,04 | 6.36 | 72.19 |

| SAHOL | 0,09 | 0,09 | 0,13 | 0,18 | 0,27 | 0,27 | 0,30 | 0,33 | 0,81 | 1,62 | 6.85 | 9.06 |

| SELEC | 0,05 | 0,06 | 0,06 | 0,08 | 0,10 | 0,10 | 0,16 | 0,17 | 0,54 | 0,23 | 12.23 | 14.19 |

| SISE | 0,04 | 0,05 | 0,12 | 0,11 | 0,13 | 0,16 | 0,12 | 0,16 | 0,44 | 0,67 | 8.10 | 10.22 |

| TOASO | 0,62 | 0,96 | 0,76 | 0,76 | 1,59 | 1,75 | 2,38 | 3,44 | 8,75 | 7,17 | 22.67 | 29.11 |

In terms of expected rates of return, the highest value is observed for AKSA at 193.92%, while the lowest value belongs to ENKAI at 8.19%. Furthermore, dividend growth rates and required rates of return appear to move in parallel, suggesting that an increase in dividend growth is likely to result in a higher expected return.

Table 3 presents the sMdAPE (%) values and the Wilcoxon Signed-Rank test results. The findings indicate that the companies generally exhibit sMdAPE values at or well below 30%. This implies that the model achieves an accuracy level exceeding 70% in predicting stock prices for the companies analyzed.

Table 3.

sMdAPE (%) and Wilcoxon Signed-Rank Test Results for Selected Stocks in Türkiye

| Company Code | sMdAPE(%) | Wilcoxon Signed-Rank Test |

|---|---|---|

| AKCNS | 6.47962304 | 0.114 |

| AKMGY | 16.3949656 | 0.114 |

| AKSA | 11.9216902 | 0.285 |

| ALARK | 15.2972863 | 0.333 |

| ASELS | 17.2538566 | 0.203 |

| AYGAZ | 10.4883657 | 0.203 |

| ANHYT | 13.1111165 | 0.074 |

| BIMAS | 21.4213217 | 0.575 |

| ECILC | 4.21937214 | 0.047 |

| ECZYT | 3.7134706 | 0.059 |

| ENKAI | 6.11261502 | 0.059 |

| FROTO | 30.3725444 | 0.445 |

| INDES | 19.381131 | 0.037 |

| ISMEN | 14.2360689 | 0.022 |

| JANTS | 14.6876461 | 0.241 |

| KCHOL | 9.13557341 | 0.074 |

| NUHCM | 12.2512525 | 0.285 |

| POLHO | 9.88797096 | 0.959 |

| PETUN | 6.03527185 | 0.646 |

| SAHOL | 6.87781668 | 0.203 |

| SELEC | 12.4855263 | 0.114 |

| SISE | 7.61347029 | 0.169 |

| TOASO | 18.9409013 | 0.203 |

The Wilcoxon Signed-Rank Test, used to determine whether the difference between the actual and estimated stock prices is statistically significant, reveals that for ECILC, INDES, and ISMEN, a significant difference exists at the 5% level; and for ANHYT, ECZYT, ENKAI, and KCHOL, a significant difference exists at the 10% level. For the remaining 16 companies, no statistically significant difference was found between actual and estimated prices.

Overall, the results demonstrate that the DDM is a reliable model for predicting the stock prices of dividend-paying companies in Türkiye.

The findings are consistent with those of Jareño and Navarro (2007), Ivanovski, Ivanovska and Ivanovska (2015), Gacus and Hinlo (2018), Iyer and Paul (2019), Sutjipto, Setiawan and Ghozali (2020), Kleriawan and Dwiyono (2021), Febriani et al. (2021), Umamik and Matnin (2023), Hutagalung and Alexandri (2024), and Han (2025), while differing from the results reported by Olweny (2011), Ong'ele (2018), Vikas, Charithra and Sharma (2022), and Yulianto (2024).

Conclusion

4.

This study estimates the stock values of 23 BIST companies that regularly distributed dividends between 2014 and 2023 using the Constant Growth Dividend Discount Model (DDM) and evaluates the model's validity. The findings clearly demonstrate that the DDM is a highly effective valuation method for firms with stable dividend policies in the Turkish capital markets. The sMdAPE values being below 30% for 20 out of the 23 companies indicate that the model forecasts stock prices with a high degree of accuracy. In particular, the very low error rates observed for ECZYT (3.71%) and ECILC (4.21%) show that the model performs strongly for companies with consistent dividend growth.

The results of the Wilcoxon Signed-Rank test further reveal that, for 16 companies, there is no statistically significant difference between theoretical and actual stock prices. This suggests that the DDM accurately reflects market prices for these firms. However, significant differences found in seven companies can be attributed to fluctuations in dividend growth rates, sector-specific dynamics, and period-specific macroeconomic conditions. These findings imply that the model may exhibit limited performance for firms with unstable dividend policies or volatile growth patterns.

Overall, the results align with international studies affirming the reliability of the DDM, including those by Jareño & Navarro (2007), Gacus & Hinlo (2018), Iyer & Paul (2019), Sutjipto et al. (2020), and Han (2025). On the other hand, the findings diverge partially from studies such as Olweny (2011), Ong'ele (2018), and Vikas et al. (2022), which highlight limitations of the model in certain sectors. Taken together, the study concludes that the DDM is an effective and applicable valuation method for dividend-paying firms in Türkiye. In general, the results confirm that the model can be successfully applied to companies with stable dividend distribution and is a practical tool in stock valuation.

For future studies, applying two-stage or multi-stage DDM models may provide deeper insight into the impact of fluctuating dividend growth rates on valuation accuracy. Additionally, incorporating macroeconomic indicators—such as interest rates, inflation, and exchange rate movements—into the model could help reveal its sensitivity to broader market conditions. Comparing sectors may also help identify the industries in which the model performs best, thereby expanding its practical relevance.

This study fills a significant gap in the literature by testing the Constant Growth DDM over a long period and across a wide sample of companies with stable dividend policies in Türkiye. Evaluating the model's forecasting performance using both advanced error metrics, such as sMdAPE, and statistical tests like the Wilcoxon Signed-Rank test provides robust empirical evidence specific to Turkish capital markets. Moreover, analyzing a multi-sector sample and identifying the sectors in which the DDM performs more effectively contributes valuable methodological and practical insights to the valuation literature.