Table 1.

Description of Variables Used in the Analysis

| Code | Variable Name | Economic Relevance | Source |

|---|---|---|---|

| CPI | Consumer Price Index | Measures overall inflation and serves as the primary dependent variable. | Bureau of National Statistics |

| ConPI | Construction Price Index | Reflects cost trends in the construction sector, a major driver of urban expenses. | Bureau of National Statistics |

| AMW | Average Monthly Wages | Proxy for household income and purchasing power. | Bureau of National Statistics |

| COL | Cost of Living Index | Captures broad affordability and household burden. | Bureau of National Statistics |

| OIR | Official Interest Rate | Represents monetary policy stance and credit conditions. | National Bank of Kazakhstan |

Table 2.

Stationarity Test Results (at levels with trend)

| Variable | ADF p-value | KPSS stat | KPSS p-value | Interpretation |

|---|---|---|---|---|

| CPI | 0.993 | 0.216 | 0.010 | Non-stationary |

| ConPI | 0.002 | 0.053 | >0.1 | Stationary |

| AMW | 0.999 | 0.584 | <0.01 | Non-stationary |

| COL | 0.969 | 0.536 | <0.01 | Non-stationary |

| OIR | 0.535 | 0.170 | 0.037 | Non-stationary |

Table 3.

Johansen Cointegration Test (Trace and Maximum Eigenvalue Statistics)

| Rank | Eigenvalue | Trace Stat | p-value | Max-Eigen Stat | p-value |

|---|---|---|---|---|---|

| 0 | 0.35256 | 137.11 | 0.0000 | 57.385 | 0.0000 |

| 1 | 0.27635 | 79.729 | 0.0000 | 42.696 | 0.0001 |

| 2 | 0.14892 | 37.033 | 0.0070 | 21.285 | 0.0458 |

| 3 | 0.11221 | 15.748 | 0.0483 | 15.710 | 0.0272 |

| 4 | 0.00029 | 0.0379 | 0.8489 | 0.0379 | 0.8489 |

Table 4a.

Normalized Cointegrating Vectors (Beta)

| Variable | β1 (OIR eq.) | β2 (AMW eq.) | β3 (COL eq.) |

|---|---|---|---|

| l_OIR | 1.000 | 0.000 | 0.000 |

| l_AMW | 0.000 | 1.000 | 0.000 |

| l_COL | 0.000 | 0.000 | 1.000 |

| l_ConPI | 16.537 | 24.762 | 27.572 |

| l_CPI | −7.444 | −2.294 | −0.229 |

Table 4b.

Adjustment Speeds (Alpha Coefficients)

| Variable | α1 (to β1) | α2 (to β2) | α3 (to β3) |

|---|---|---|---|

| l_OIR | −0.05483 | 0.17731 | −0.13291 |

| l_AMW | −0.00196 | −0.00157 | 0.02066 |

| l_COL | 0.01166 | 0.04043 | −0.04333 |

| l_ConPI | 0.00076 | 0.00933 | −0.01576 |

| l_CPI | 0.00088 | 0.01319 | −0.01350 |

Table 5.

Autocorrelation and Normality of residuals

| Test | Statistic | p-value | Interpretation |

|---|---|---|---|

| Autocorrelation (LM test, up to lag 6) | Rao F (lag 6) = 0.947 (F (150, 390)) | 0.649 | No autocorrelation up to 6 lags; residuals are serially uncorrelated |

| Residual correlation matrix | Max correlation = 0.153 | - | Very low cross-equation residual correlation; no sign of misspecification |

| Eigenvalues of residual matrix | Max eigenvalue = 1.23352 | - | All eigenvalues < 1.25, suggesting residuals are well-behaved |

| Normality (Doornik-Hansen) | Chi2 (10) = 426.72 | 0.0000 | Residuals are not normally distributed, a common finding in macro models |

Table 6.

Cumulative Response of CPI to 1 SD Shocks (first 10 periods)

| Shocked Variable | Max Response | CPI | Period of Max | Interpretation |

|---|---|---|---|---|

| OIR | 0.0066 | t = 3 | A 1 SD increase in OIR raises CPI by ~0.66% | |

| AMW | 0.0018 | t = 10 | Wage increase gradually pushes CPI by ~0.18% | |

| ConPI | 0.0032 | t = 6 | Construction shocks cause short-lived CPI rise |

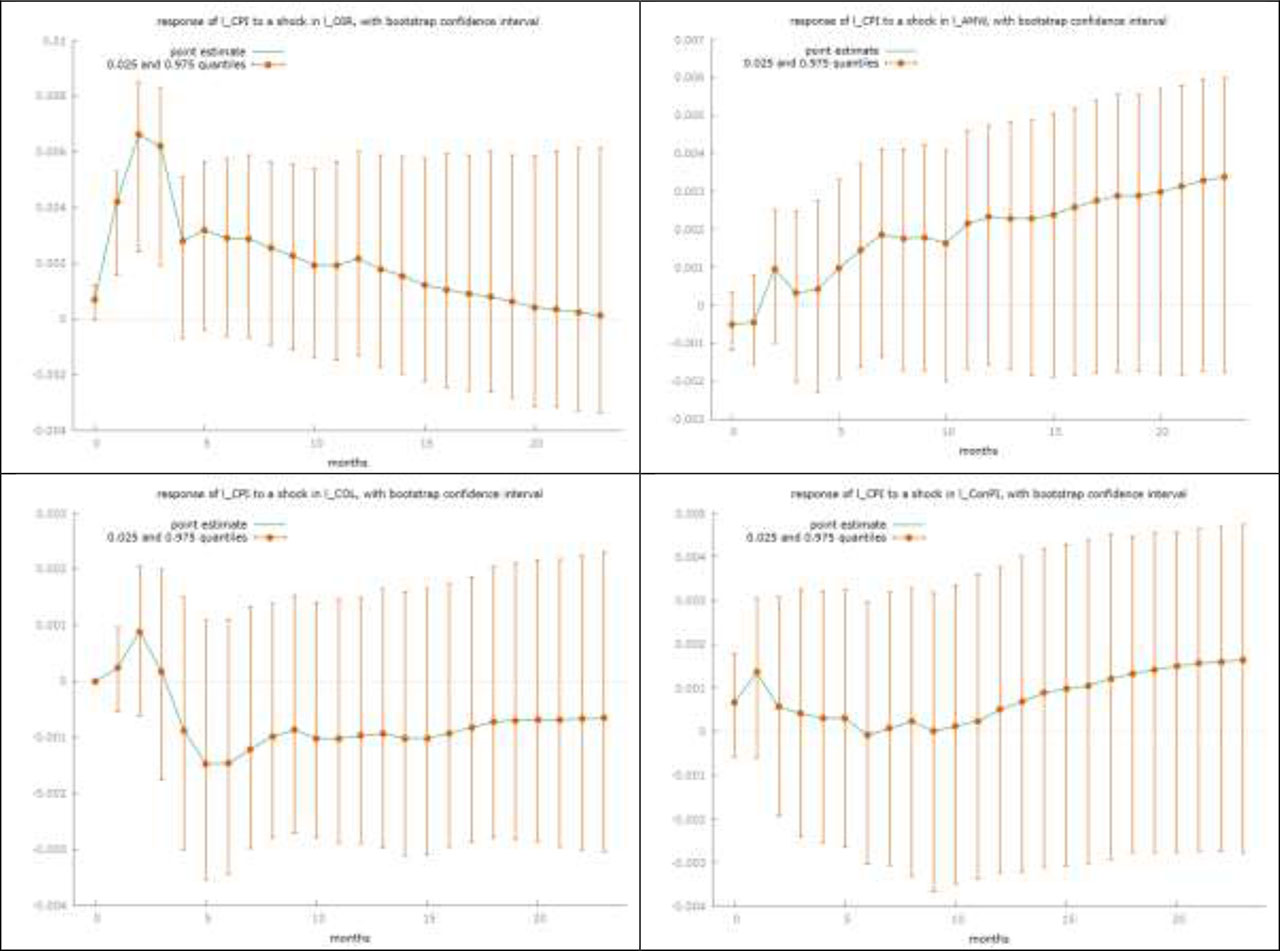

Figure 1.

Impulse Response Functions for CPI to Shocks in OIR, AMW, and ConPI.

Table 7.

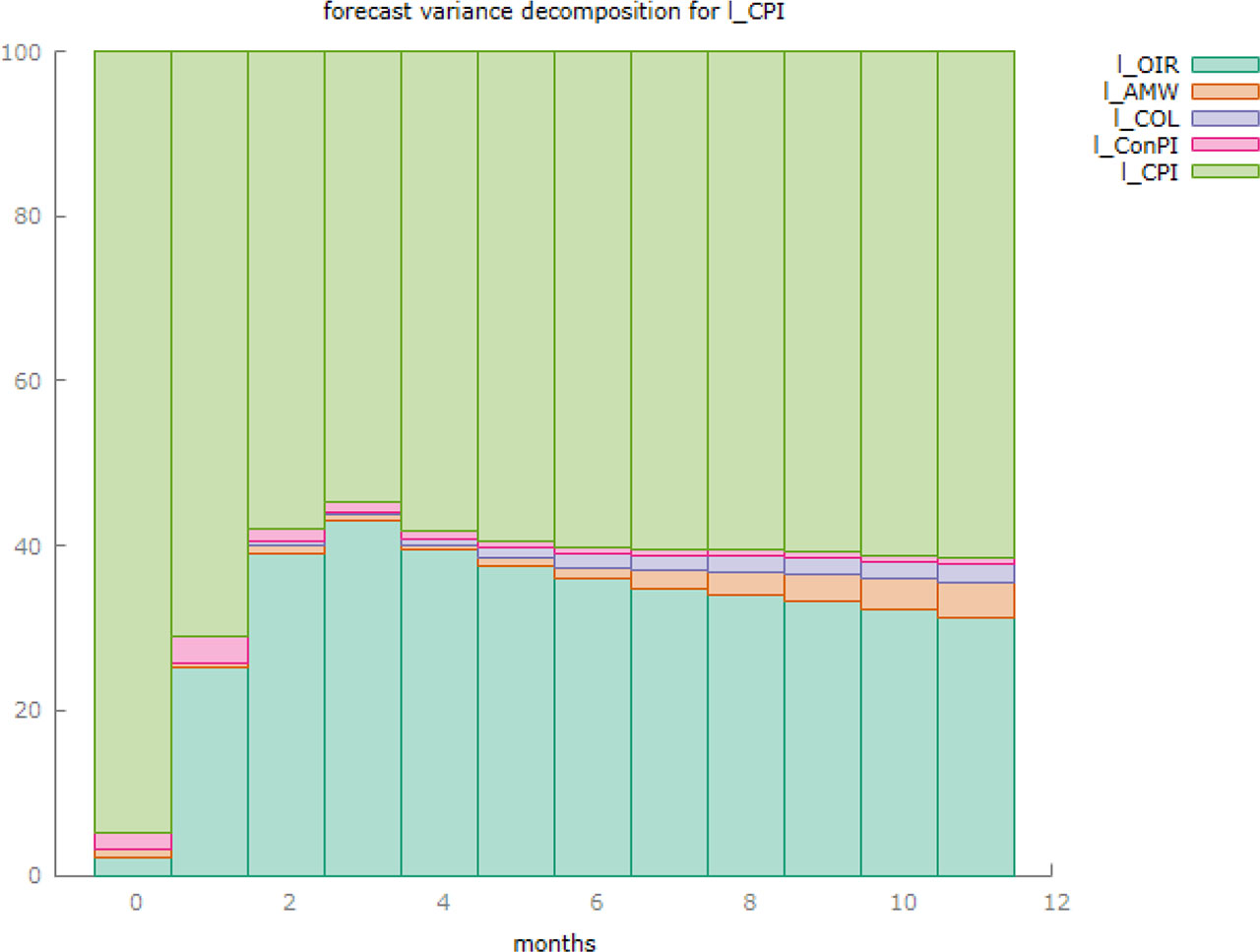

Forecast Error Variance Decomposition of CPI (t = 12)

| Source | % Contribution to CPI Variance |

|---|---|

| CPI (own) | 61.5% |

| OIR | 31.2% |

| AMW | 4.4% |

| COL | 2.3% |

| ConPI | 0.6% |

Figure 2.

Variance Decomposition of CPI Forecast Errors