Introduction

1.

Over the pluperfect decade, Kazakhstan gone through a rapid structural transformation and macroeconomic shift induced by a complicated interweaving of international commodity cycles, the post-Soviet adaptation challenges, Artyom state-oriented development programs. Despite some economic advances, the country continues to exist inflationary pressures, while affordability concerns grow in urban centers, which have the dissimilarity of rising house prices and concurrent real wages without increase. Inflation control has become a key policy issue as policymakers pursue price stability with growth and welfare of households.

Construction prices, average wages, and interest rates are said to be the prime determinants of inflation and prices of living. Construction prices are seen as dual in nature: on the one hand, prices depend on the capacity present in the domestic territory; on the other, they depend on the prices of imported inputs. Wages, on the other hand, as we all know, are a prime determinant of one’s ability to pay for basic necessities of goods and services. Official interest rates, conversely, should theoretically yet work as the principal monetary policy instrument used by the National Bank of Kazakhstan to shape inflation expectations and influence flows of credit. Not much is known about the complex interrelationships in precious little researched emerging market in Kazakhstan among these variables and the effect these relationships have, individually or collectively, on all consumer prices and hence household costs.

This study aims at answering the following research question: What are the short-run and long-run macroeconomic determinants of inflation and the cost of living in Kazakhstan? Using the VECM on monthly data from 2011–2022, this paper studies the cointegrated relationships between consumer price inflation (CPI), construction price, wages, interest rates, and a wider index of the cost of living. The model identifies the long-run equilibrium linkages and short-run adjustments through the IRFs and FEVDs.

The empirical investigation must have at least three contributions to the literature: First, it gives the rare quantitative studies into inflation dynamics with high-frequency macroeconomic data from Kazakhstan. Second, it folds in various facets of affordability-construction costs, wages, and living costs-into a unified time-series framework. Third, it identifies research topics that have implications for macroeconomic policymakers seeking to control price stability, labor market health, and household welfare in an ever-changing policy environment.

The findings have implications for the coordination of fiscal and monetary policies, wage determination systems, and mechanisms for ensuring housing affordability. We next present a review of the relevant literature, followed by a presentation of the data and methodology. After that, the key findings from the VECM analysis will be reported, with a discussion

Literature Review

2.

Inflation and the forces determining its dynamics have been the theoretical aspects widely scrutinized in the macroeconomic literature. Basic monetary theories, such as Friedman’s (1968) quantity theory of money, contend that, chiefly, inflation is an outcome of excessive money growth. The monetarist view was, thereafter, refined by that of New Keynesians, who put prices stickiness with inflation expectations and central bank credibility into their respective analyses (Clarida, Galí, & Gertler, 2000). These models had interest rates as the main channel of transmission for monetary policy. Inflation is caused by both demand-pull and cost-push pressure. Under the demand side of the equation, higher wages and increased spending put upward pressure on price levels. Empirical research, for example, Blanchard and Galí (2007), strongly support the link between wage growth and inflation in open economies. Central banks adjust this effect through interest rates; Mishkin (2007) explains how changes in policy rates feed into inflation expectations and aggregate demand. On the cost-push side, prices for inputs such as construction materials and housing costs rise-the latter being important in economies where investment is mainly state-led and bottlenecks impede supply, Dabla-Norris and Floerkemeier (2006).

Generally, the cointegration and error correction models are employed by economists to understand the dynamic relationship between inflation and the drivers of it. Johansen (1995) delineated the maximum likelihood-based cointegration test, whereas Juselius (2006) provided a farmhand application of the VECM framework. These methods help discriminate between transitory and permanent relationship structures of various macroeconomic aggregates. Égert (2007) applied the VECM to Central and Eastern European countries for the analysis of the inflation pass-through and wage reaction to monetary policy. In Kazakhstan, empirical analyses regarding inflation are few and seemingly uncoordinated. Among the few available analyses, most are descriptive or confined to single-variable regressions. More precisely, the World Bank (2017) and ADB (2019) identify housing price adjustments, regulated utilities, and public wage increases as main inflation determinants of Kazakhstan. The studies from the National Bank of Kazakhstan (NBK, 2020) hint at a weak transmission from policy rates to consumer prices, possibly due to structural rigidities. On a regional level, Kutan and Wyzan (2005) find that Central Asia’s monetary transmission is slower and more volatile than that in Eastern Europe. Still, VECM studies for Kazakhstan are yet to be undertaken in full scale.

Research Gap

2.1.

While existing research does provide insights on single components of inflation, there does not yet exist any study in the Kazakhstani context which simultaneously models the macroeconomic transmission channels between the CPI, construction costs (ConPI), average monthly wages (AMW), cost of living (COL), and official interest rates (OIR) using a VECM method. This study fills that gap with a fully integrated time-series method using monthly data from 2011–2022 to capture any structural changes and policy alterations. By means of a simultaneous estimation of long-run equilibrium and short-run adjustment processes, the model will contribute to the ongoing debate regarding monetary and wage policies specific to the further evolution of the macroeconomic environment of Kazakhstan.

Data and Methodology

3.

The data for the present study consists of monthly observables for Kazakhstan, from January 2011 to December 2022. Table 1 delineates the five macroeconomic variables central to this study.

Table 1.

Description of Variables Used in the Analysis

| Code | Variable Name | Economic Relevance | Source |

|---|---|---|---|

| CPI | Consumer Price Index | Measures overall inflation and serves as the primary dependent variable. | Bureau of National Statistics |

| ConPI | Construction Price Index | Reflects cost trends in the construction sector, a major driver of urban expenses. | Bureau of National Statistics |

| AMW | Average Monthly Wages | Proxy for household income and purchasing power. | Bureau of National Statistics |

| COL | Cost of Living Index | Captures broad affordability and household burden. | Bureau of National Statistics |

| OIR | Official Interest Rate | Represents monetary policy stance and credit conditions. | National Bank of Kazakhstan |

All variables were transformed by applying the natural logarithm. This transformation has two purposes: namely, 1) stabilizing the variance of the time series given heteroscedasticity, and 2) helping to interpret coefficients in the model as elasticities, which is economically meaningful for the assessment of percentage changes as a response to shocks. The ADF and KPSS tests were employed to check if the time series were stationary. All variables were I(1) series, satisfying the requirement for cointegration analysis. Then Johansen’s cointegration test was used to indicate the existence of long-run equilibrium relationships among the variables. The Johansen’s trace statistic pointed to three cointegrating relations at the 5% significance level. This implies that in spite of short-term fluctuations, the variables remain related in the long-term and can be modeled into a Vector Error Correction Model or VECM for short. The lag length for the model was decided upon on account of many selection criteria, such as the AIC, HQC, and BIC. AIC and HQC supported a lag length of 6, but BIC points to a more parsimonious model. Striking a balance between the degree of richness of the dynamic structure and degrees of freedom, lag length 6 was chosen to give more room for residual diagnostics and dynamic accuracy. Given that the series are I(1) and cointegrated, a VECM was estimated. The model captures short-run dynamics and long-run equilibrium adjustments between the variables. The general form of the VECM for a system of k endogenous variables with r cointegrating vectors is:

where:- γt is a vector of endogenous variables in logarithms,

- Δ - is the first-difference operator,

- Π captures the long-run equilibrium through the cointegration matrix β and adjustment coefficients α,

- Γi are short-run dynamic coefficients,

- Dt represents deterministic components (including constant and seasonal dummies),

- ɛt is a vector of white noise error terms.

The seasonal dummies:(February through December with January omitted) account for possible monthly seasonality in macro variables, including prices and wages.

Thus, the VECM framework allows identifying both long-run equilibrium relationships and short-run responses subjected to economic shocks, providing grounds for the subsequent sections on impulse response and variance decomposition analysis.

Results and Discussion

4.

Stationarity and Cointegration Tests

4.1.

All variables were tested for stationarity using the Augmented Dickey-Fuller (ADF) and KPSS tests. Results are summarized below:

Table 2.

Stationarity Test Results (at levels with trend)

| Variable | ADF p-value | KPSS stat | KPSS p-value | Interpretation |

|---|---|---|---|---|

| CPI | 0.993 | 0.216 | 0.010 | Non-stationary |

| ConPI | 0.002 | 0.053 | >0.1 | Stationary |

| AMW | 0.999 | 0.584 | <0.01 | Non-stationary |

| COL | 0.969 | 0.536 | <0.01 | Non-stationary |

| OIR | 0.535 | 0.170 | 0.037 | Non-stationary |

Only the construction price index (ConPI) was found to be stationary at the level with trend by both ADF and KPSS tests. All other series are clearly non-stationary and need to be first-differenced.

The Johansen cointegration test was then applied to check for long run equilibrium relationships. The test results are below:

Table 3.

Johansen Cointegration Test (Trace and Maximum Eigenvalue Statistics)

| Rank | Eigenvalue | Trace Stat | p-value | Max-Eigen Stat | p-value |

|---|---|---|---|---|---|

| 0 | 0.35256 | 137.11 | 0.0000 | 57.385 | 0.0000 |

| 1 | 0.27635 | 79.729 | 0.0000 | 42.696 | 0.0001 |

| 2 | 0.14892 | 37.033 | 0.0070 | 21.285 | 0.0458 |

| 3 | 0.11221 | 15.748 | 0.0483 | 15.710 | 0.0272 |

| 4 | 0.00029 | 0.0379 | 0.8489 | 0.0379 | 0.8489 |

The test confirms the existence of three cointegrating relations for the five variables, in conformity with the economic theory that posits an intertwined long-run dynamic between prices, wages, and some variable of monetary policy.

Table 4a.

Normalized Cointegrating Vectors (Beta)

| Variable | β1 (OIR eq.) | β2 (AMW eq.) | β3 (COL eq.) |

|---|---|---|---|

| l_OIR | 1.000 | 0.000 | 0.000 |

| l_AMW | 0.000 | 1.000 | 0.000 |

| l_COL | 0.000 | 0.000 | 1.000 |

| l_ConPI | 16.537 | 24.762 | 27.572 |

| l_CPI | −7.444 | −2.294 | −0.229 |

This table reveals long-run equilibrium relations between the variables. The first equation is normalized on OIR (official interest rate), the second on average monthly wages (AMW), and the third on the cost-of-living index (COL). For instance, in the first vector, a one-percent increase in ConPI raises the OIR by 16.5%, whereas a one-percent increase in the CPI lowers the OIR by about 7.4% in the long run.

Table 4b.

Adjustment Speeds (Alpha Coefficients)

| Variable | α1 (to β1) | α2 (to β2) | α3 (to β3) |

|---|---|---|---|

| l_OIR | −0.05483 | 0.17731 | −0.13291 |

| l_AMW | −0.00196 | −0.00157 | 0.02066 |

| l_COL | 0.01166 | 0.04043 | −0.04333 |

| l_ConPI | 0.00076 | 0.00933 | −0.01576 |

| l_CPI | 0.00088 | 0.01319 | −0.01350 |

The alpha matrix shows how fast each variable adjusts to deviation from the long-run equilibrium. The official interest rate, e.g., has relatively fast adjustment speeds with respect to the second and third cointegrating vectors (0.177 and −0.133), whereas wages (AMW) exhibit little response. That is, the OIR responds actively to disequilibrium conditions, perhaps reflecting policy actions.

Residual Diagnostics

4.2.

The selected VECM model (lag length = 6) was subjected to standard diagnostic tests:

Table 5.

Autocorrelation and Normality of residuals

| Test | Statistic | p-value | Interpretation |

|---|---|---|---|

| Autocorrelation (LM test, up to lag 6) | Rao F (lag 6) = 0.947 (F (150, 390)) | 0.649 | No autocorrelation up to 6 lags; residuals are serially uncorrelated |

| Residual correlation matrix | Max correlation = 0.153 | - | Very low cross-equation residual correlation; no sign of misspecification |

| Eigenvalues of residual matrix | Max eigenvalue = 1.23352 | - | All eigenvalues < 1.25, suggesting residuals are well-behaved |

| Normality (Doornik-Hansen) | Chi2 (10) = 426.72 | 0.0000 | Residuals are not normally distributed, a common finding in macro models |

The LM autocorrelation test indicating no serial correlation in the residuals up to lag 6 validates the dynamic specification of the model. The residual correlation matrix also indicates weak cross-dependence between equations (max 0.15). The Doornik-Hansen test indicates a statistically significant rejection of the null hypothesis of multivariate normality, which is a standard result in macroeconomic data and is in no way detrimental to any inferences made by the model, which is robust in large samples. All eigenvalues are less than the critical values; hence, the model is dynamically stable.

Impulse Response Functions (IRFs)

4.3.

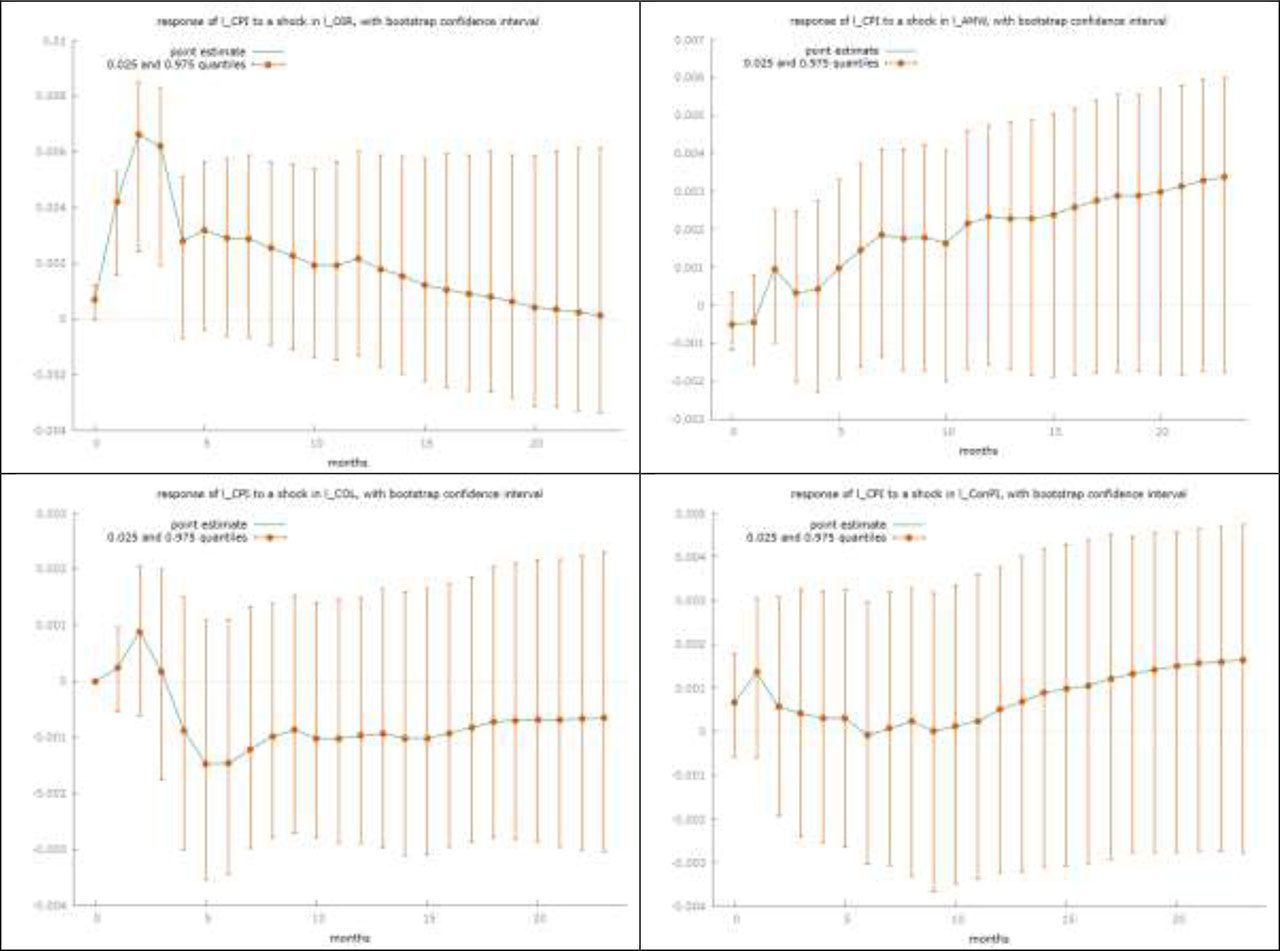

IRFs were computed based on a Cholesky ordering (ConPI → OIR → AMW → CPI → COL). The selected results are shown below:

Table 6.

Cumulative Response of CPI to 1 SD Shocks (first 10 periods)

| Shocked Variable | Max Response | CPI | Period of Max | Interpretation |

|---|---|---|---|---|

| OIR | 0.0066 | t = 3 | A 1 SD increase in OIR raises CPI by ~0.66% | |

| AMW | 0.0018 | t = 10 | Wage increase gradually pushes CPI by ~0.18% | |

| ConPI | 0.0032 | t = 6 | Construction shocks cause short-lived CPI rise |

Economic shocks on interest rates induce a quicker and higher inflation response. Wage shocks enhance CPI much more slowly, revealing after-the-fact increases in costs. Construction prices have a moderate impact but less persistent in dimension.

Figure 1 represents impulse response functions of CPI of Kazakhstan to identified shocks of key explanatory variables - OIR, AMW, COL, and ConPI. The CPI responds with point estimates (solid lines) along with the confidence intervals at the 95% level based on bootstrapping, so the clear interpretation of statistical significance and timing of effects is available.

Figure 1.

Impulse Response Functions for CPI to Shocks in OIR, AMW, and ConPI.

The CPI reacts in a positive and statistically significant manner during the first 3–4 months to an interest rate shock and peaks around month 3 with an estimated increase of about 0.0067. This might constitute some short-run cost-push mechanism whereby higher interest rates translate into higher costs and prices, perhaps as finance-related costs to businesses and the mortgage markets elevate. Such an effect begins tapering away after month 4 and becomes statistically indistinguishable after month 10. The gradual but only slowly adjusting wage-related shocks induce CPI increases with broad confidence intervals in the earliest months but gaining in significance and steadiness from month 6 onward to a measure of around 0.003 a month 20. This settles the issue of cost-push inflation-by-wage channels with slow pass-through; actually, this conforms perfectly to wage-price spirals in sectors of labor sanctions. Surprisingly, CPI responses to COL shocks are rather small, initially staying negative. A negative deviation does develop up to a maximum of −0.001 around month 6 but with wide confidence bands. This could imply that COL changes are more an effect of general inflation rather than causal agents of it. It also suggests multicollinearity with CPI or lagged household behavior adjustment. Construction cost shocks bring about a slightly positive CPI reaction in the short run (about 0.0012 at month 2), which dissipates in time. The response remains in a tight confidence range, indicating limited inflationary pressure of construction sector cost increases, most probably due to the sector being capital-intensive and with delayed transmission to the broader production sector.

Forecast Error Variance Decomposition (FEVD)

4.4.

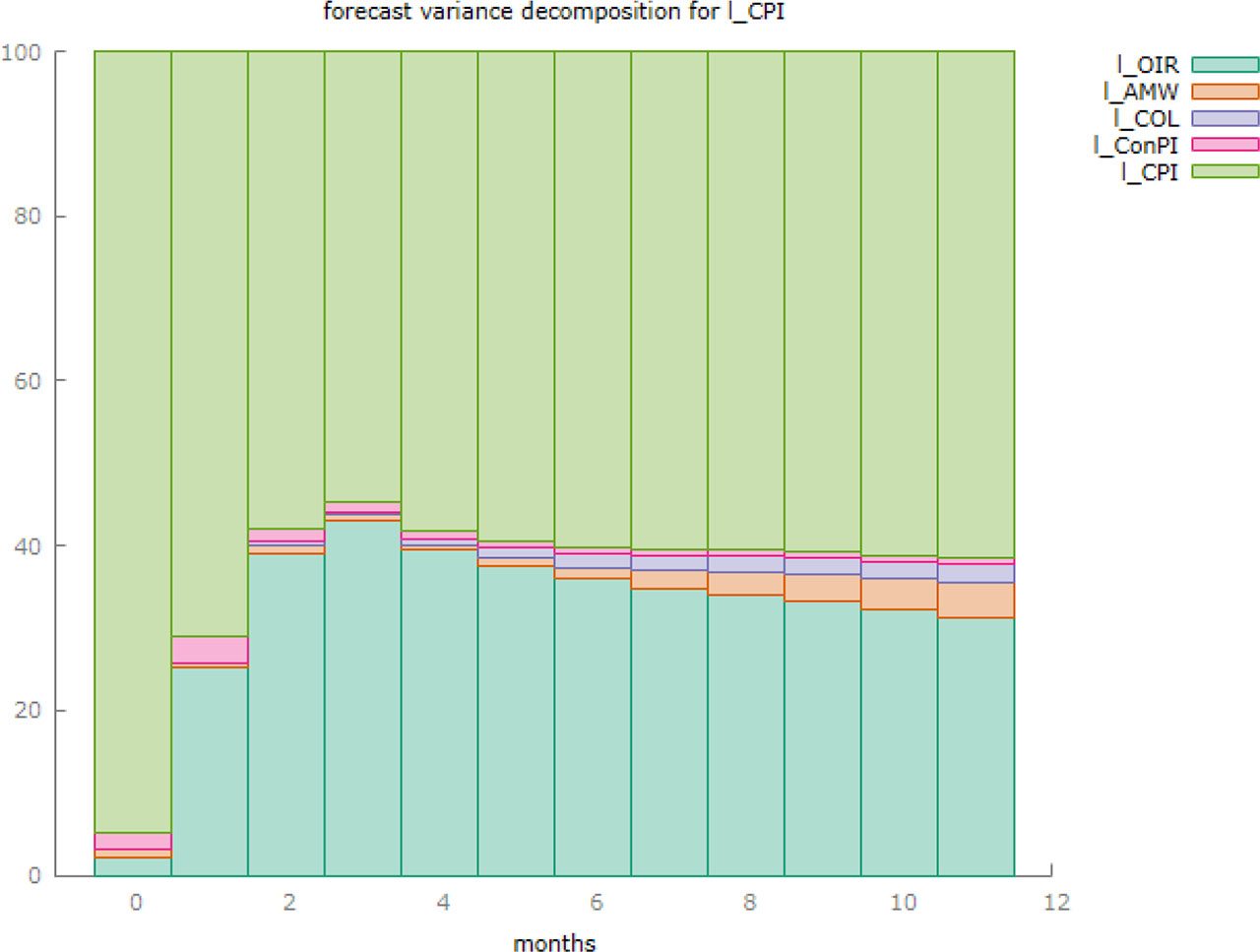

FEVD shows how much each source of shock contributes to the forecast error variance in each variable:

Table 7.

Forecast Error Variance Decomposition of CPI (t = 12)

| Source | % Contribution to CPI Variance |

|---|---|

| CPI (own) | 61.5% |

| OIR | 31.2% |

| AMW | 4.4% |

| COL | 2.3% |

| ConPI | 0.6% |

Nearly one-third of variation is driven by interest rates, underlining the importance of timely and effective monetary policy. Wages and living costs play a modest but non-negligible role in shaping inflation trajectories.

Figure 2 illustrates that OIR contributes the largest share for CPI, stabilizing around 31%, indicating the importance of monetary policy in influencing inflation variability. AMW (wages) contributes around 4–5%, while COL and ConPI remain minor contributors. These proportions validate the centrality of policy rates in inflation dynamics, while also highlighting that wage and cost shocks have smaller, delayed effects.

Figure 2.

Variance Decomposition of CPI Forecast Errors

Discussion

5.

This paper investigates the macroeconomic interrelationships between inflation (CPI), construction costs, average wages, cost of living, and interest rates in Kazakhstan within the framework of a VECM model. The results lend empirical support to many well-established predictions of monetary economics and of price-wage dynamics.

Monetary Transmission and Inflation: According to the results of the impulse response analysis, shocks from the OIR do significantly affect inflation dynamics. A 1-standard deviation increase in the OIR results in about a 0.66% increase in CPI at the third period. This reaction is consistent with the view that, in the short run, monetary tightening increases borrowing costs and hence prices through cost channels. With the passage of time, the effect stabilizes and strengthens the status of the policy rate of the National Bank of Kazakhstan as the main lever in inflation targeting (Mishkin, 2007).

Wage and Cost Pressures: AMW and ConPI also exert upward pressures on CPI, but with slower transmissions. Wage shocks are propagated slowly and can take longer to realize their full effect, reaching their maximum effect of about 0.18% at period 10. This stagnation of cost-push inflation is consistent with Blanchard’s (2006) framework on labor market frictions. Moreover, ConPI shocks have a fleeting impact on CPI, consistent with the pattern of sector-specific price rigidity and delayed pass-through mechanisms documented in transitional economies.

Variance Decomposition Results: The FEVD results highlight the importance of inflation inertia. However, shocks to interest rates account for 31.2%, thus showing that macroeconomic volatility in Kazakhstan is still highly responsive to monetary policy. The limited role of wages (4.4%) and living costs (2.3%) indicates that structural reforms in institutions for wage setting and housing will only gradually make an impact on price stability.

Policy Recommendations:

Strengthen Monetary Policy Transmission: Given the responsiveness of CPI to OIR shocks, the National Bank should enhance transparency and forward guidance to reinforce policy credibility.

Target Real Wage Adjustments: Since wage shocks impact CPI gradually, wage indexing mechanisms in public contracts should be monitored to avoid inflationary spirals.

Mitigate Construction Cost Shocks: Temporary spikes in ConPI, while not persistently inflationary, can be addressed via procurement reforms and improved material import logistics.

Broaden CPI Monitoring Tools: With a portion of inflation explained by non-monetary components, CPI decomposition and sectoral inflation targeting (e.g., housing, food) could complement aggregate policy instruments.

In conclusion, empirical evidence supports the hypothesis that inflation in Kazakhstan is not only responsive to policy but also structurally embedded. A joint consideration of the IRF and FEVD results serves to validate the specification of the VECM and gives meaningful indications for macroeconomic stabilization in resource-rich emerging markets.

Conclusion

6.

This research investigated dynamic relations among Kazakhstan’s pertinent macroeconomic variables: consumer price index, average monthly wages, construction price index, cost-of-living indicator, and official interest rates. The model chosen is VECM, to discern how, in a transitional economy, structural and monetary variables interact to affect inflation dynamics.

It is established that CPI is affected by monetary policy elements (OIR) and structural cost elements (AMW, ConPI), with the evidence favoring long-run cointegration between all the variables. The response to shocks elucidates that in the immediate term and the long run, inflation is mostly affected by interest rate shocks; wages and construction costs feed into CPI in a rather gradual manner. The variance decomposition asserts that CPI is mainly influenced by its own past values, but interest rate shocks contribute to around one-third of its forecast error variance, emphasizing the importance of monetary policy as a tool to manage the inflation level.

The National Bank of Kazakhstan should institutionalize forward guidance mechanisms to better anchor inflation expectations, given the proven sensitivity of CPI to OIR.

Public infrastructure investment programs should incorporate inflation-contingent budgeting or subsidies during peak construction cycles, to buffer CPI against cost spikes from the ConPI component.

Further Research Directions: Further studies may consider expanding the VECM model by including some external variables of oil price, exchange rate, or geopolitical uncertainty indices, which are mainly relevant to Kazakhstani open and resource-dependent economy. Moreover, another area of investigation can examine disaggregating CPI by sector (e.g., food, housing, transportation) in future work, thereby influencing the type of policy targeted.