As the aging population continues to grow, pension funds are acknowledged as a significant financial resource in the economy to provide support and address the risks and challenges in the socioeconomic landscape. Pension funds are recognized as significant instruments at the national level, offering a dependable and enduring income stream to individuals throughout their retirement (D’Arcangelis et al., 2019). They aid individuals in preparing and accumulating savings for their retirement, effectively managing investments, and establishing a sense of financial security and stability during the transition from their working years to retirement. According to a recent OECD report, the combined value of assets managed by pension funds in OECD countries stood at approximately USD 10.8 trillion by the conclusion of 2021 (OECD, 2022). Pension funds revenues and expenditures provide valuable insights into the financial health and sustainability of pension funds (OECD, 2023a). The contributions indicator reflects the trend in pension fund revenues, specifically the inflows of funds from participant and employer contributions. Monitoring this indicator provides insights into the growth rate or changes in the amount of money flowing into the pension fund. Meanwhile, the benefits indicator reflects the trend in pension fund expenditures or payments made to retirees or beneficiaries as pension benefits. Monitoring this indicator helps assess the growth rate or changes in the amount of funds disbursed by the pension fund to support retirement incomes. Through a comprehensive examination of both benefits and contributions indicators, stakeholders have the opportunity to evaluate the overall financial status of the pension fund.

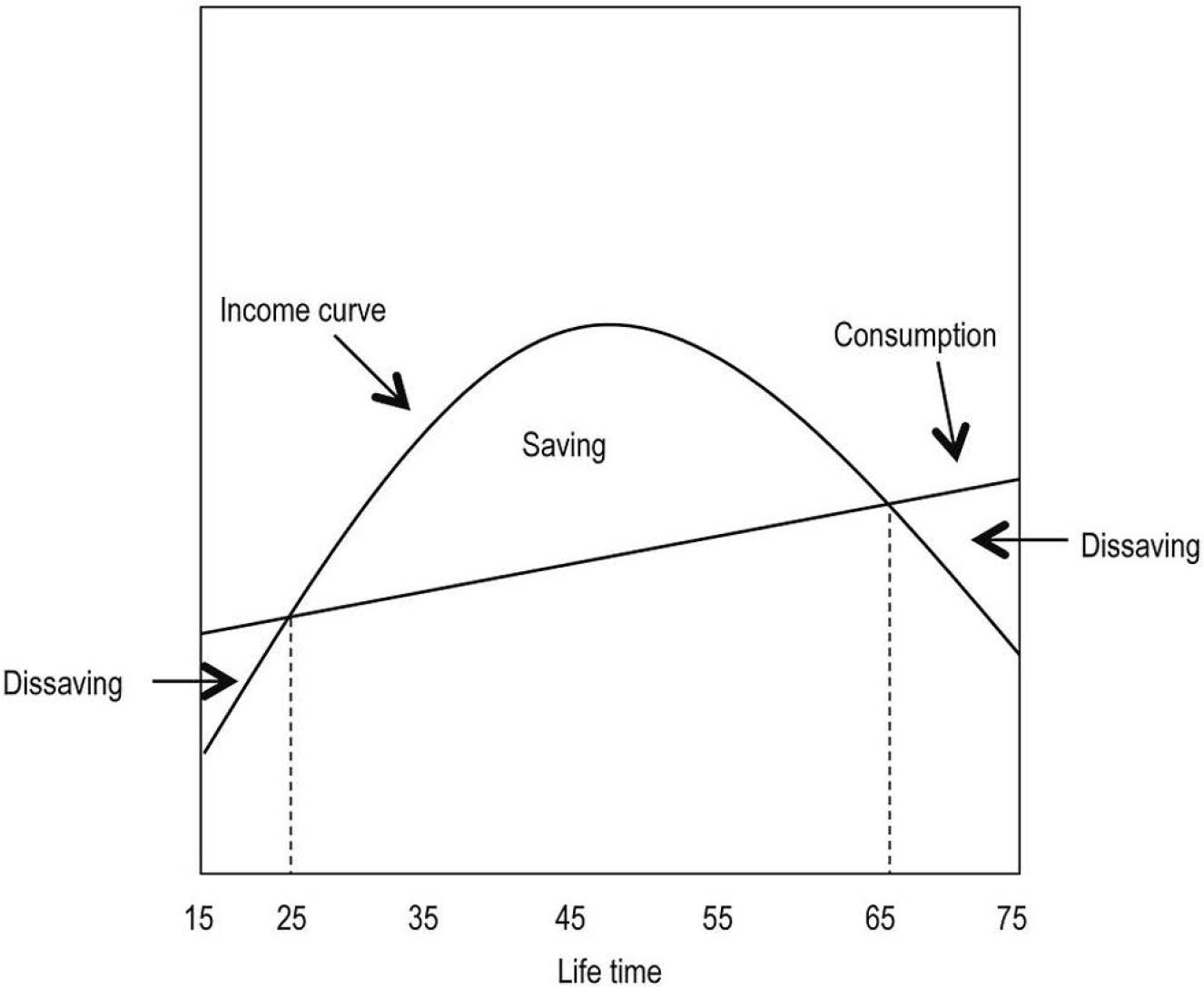

The Life Cycle Hypothesis, proposed by Modigliani and Brumberg in 1954, is an economic theory that elucidates how individuals make decisions regarding consumption and saving throughout the course of their lifetimes (Modigliani và Brumberg, 1954). The theory posits that individuals strategically determine their patterns of spending and saving by taking into account their anticipated lifetime earnings. According to this notion, individuals strive to maintain a consistent level of living standards during their lifetimes. This entails saving during their working years and subsequently utilising those savings during their retirement years.

The majority of individuals engage in borrowing during their early adulthood, particularly while pursuing education, with the expectation of future income. Throughout their professional career, individuals accumulate savings to settle the debt accumulated during their early years and to accumulate funds for their retirement. During retirement, individuals typically do not generate money from employment and tend to deplete their savings. The practice of taking loans at a young age and accumulating savings during one's working years results in the accumulation of wealth near retirement age. Initial savings may be modest or even negative during the early stages of one's employment, but they will progressively grow as retirement age approaches. As a result, one's net worth will grow during their working years and decline once they retire. Individual saving and borrowing are essential elements of the larger national saving and borrowing system, and their interactions impact the overall well-being and stability of the economy.

Both net lending/borrowing and saving play crucial roles in pension funds. National saving encompasses the combined savings made by individuals, businesses, and the government within a nation. When national saving rates are higher, it creates a larger reservoir of funds that can be directed towards investments in different sectors, including pension funds (Murphy et al., 2004). While there is a considerable body of research examining the connection between pension funds and saving rates, most of the empirical findings primarily concentrate on how pensions impact savings (Antón et al., 2014; Blau, 2016; Ertuğrul & Gebeşoğlu, 2020; Feng et al., 2011; Gebeşoğlu et al., 2023; James, 1997; Kohl & O’Brien, 1998; Murphy et al., 2004; Rezk et al., 2012; Rossi, 2009; Schmidt-Hebbel, 1998). Some studies have shown that pension has a positive effect on savings, especially national savings (Ertuğrul & Gebeşoğlu, 2020; Murphy et al., 2004; Rezk et al., 2012; Rossi, 2009; Schmidt-Hebbel, 1998). On the contrary, for some studies, the savings rate has been found to have a contrasting effect on pension funds (Blau, 2016; Feng et al., 2011; Gebeşoğlu et al., 2023). Typically, research findings of Gebeşoğlu et al., (2023) suggested that in countries with a low inclination to save, pension contributions tend to serve as notable replacements for voluntary savings. Net lending refers to the difference between an individual's savings and borrowing, indicating whether they are net lenders or net borrowers. There is a limited amount of research specifically examining the correlation between net lending/borrowing and pension funds. The research of Leonardo (2011) revealed the contributions to municipal employees’ pension funds were the main source of the municipal debts in Chile during period of 2004 to 2007. Fang & Shi (2023) analysed the relationship between public pension and farmers’ formal borrowing. The results showed that the application of pension scheme led to a decrease in farmers’ borrowing.

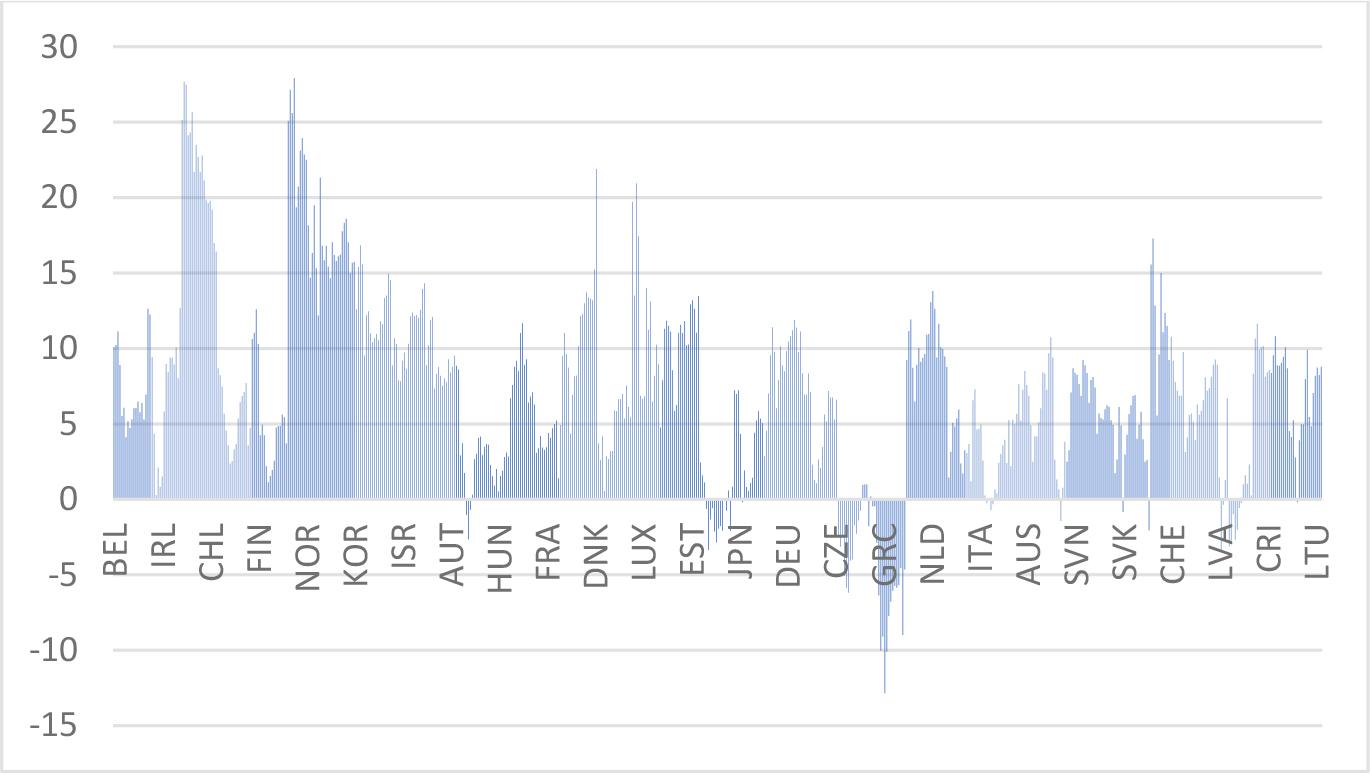

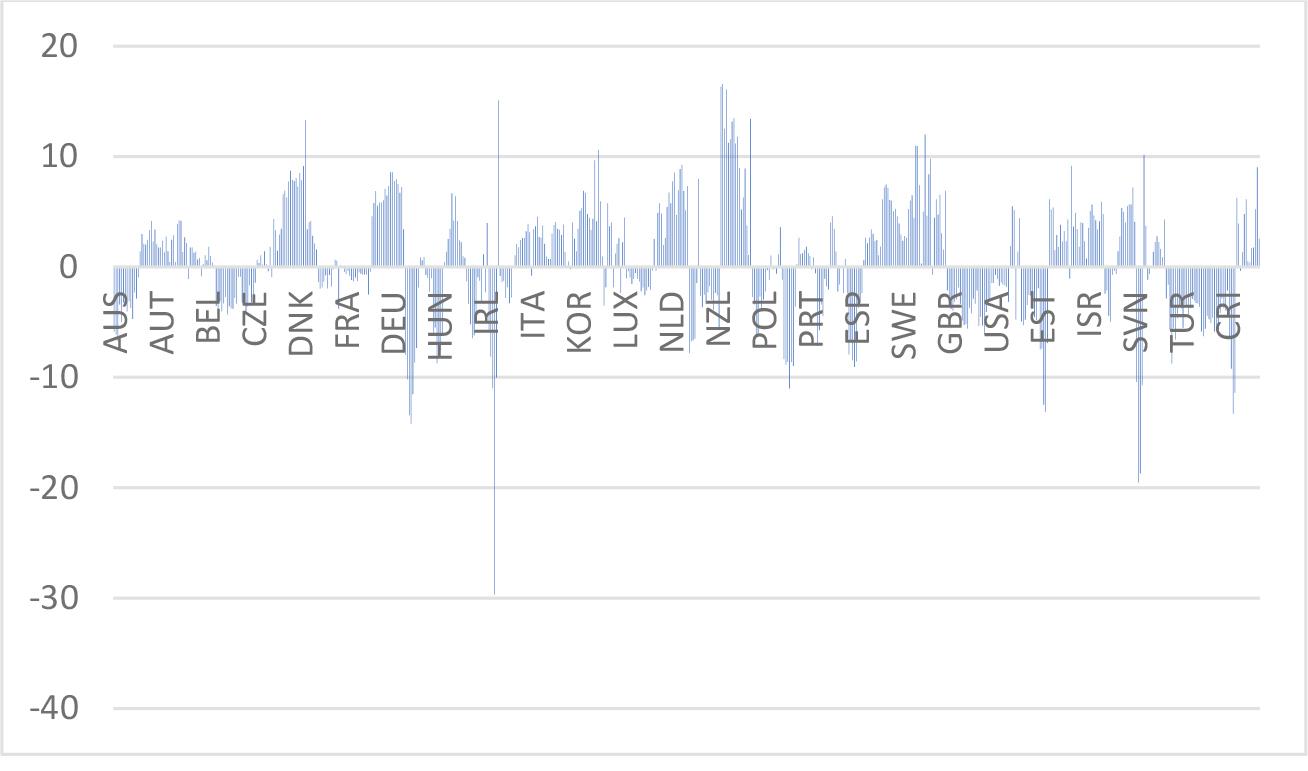

It's important to consider that saving rates and net lending can change over time due to economic conditions, policy decisions, and global events. According to Figure 1, the level of saving rate is generally high in most OECD countries during the period 2005-2022. As can be seen from Figure 2, net lending in OECD fluctuated mainly between −20% to 17% from 2005-2022. Moreover, pension funds are a vital source within a country, providing retirement income security, driving long-term investment, influencing corporate governance, promoting risk diversification, and contributing to economic stability. The effective functioning of pension funds is essential for ensuring the financial well-being of retirees and supporting sustainable economic growth as well as balancing saving rates and net lending within OECD countries. To the best of our knowledge, there is no prior research that analyses the impact of saving rate and net lending on pension funds within any countries until now. Within the OECD member countries, there are various types of pension funds that operate according to national regulations and guidelines.

Life Cycle Hypothesis

Source: (Van de Ven et al., 2017)

Saving rate in OECD countries from 2011-2021

Source: OECD (2023c)

Net lending in OECD countries from 2011-2021

Source: OECD (2023b)

Therefore, this paper thus aims to analyse the impacts of saving rate and net lending on pension funds in OECD countries. The paper presents new contributions to the existing literature by examining and extending previous empirical research with fixed effects regression models as well as testing results for robustness to various socio-economic and demographic factors.

The rest of this paper is organized as follows: Section II statistically describes the data and empirical model. The results will be analysed and explained from the empirical analysis in Section III. Finally, Section IV concludes with a discussion of the implications of our study.

To examine the impact of saving rate and net lending on pension funds, this paper adopts a two-way fixed effect model, presented as follows:

Following the prior literature (Bongaarts, 2004; Fenge and Peglo, 2018; Medeiros Garcia and Rocha da Silva, 2023), we also include a number of country-specific characteristics (represented by Zit-1) that could affect a country’s pension funds. These control variables are: GDP per capita (LNGDPCAP), measured by the natural logarithm of the real GDP per capita of each country; Internet access (INTERNET), measured by the proportion of population with Internet access; age dependency ratio (AGEDEP), measured by the percentage of total working age population; the ratio of the aged to the working-age population (AGED-TO-WORKING); trade openness (LABOREDUC), measured by the percentage of total working-age population with basic education; life expectancy (LIFEEXP), measured by natural logarithm of the life expectancy at birth; and mortality rate (MORTALITY).

All independent variables are lagged one year to deal with endogeneity issues in the form of reverse causality. δ is a kx1 parameter vector indicating the coefficients of control variables where k is the number of control variables. μi is the individual country fixed effect controlling the unobserved and time-invariant factors which are differences across countries in the model. γt is the time-fixed effect, which controls the unobserved common time-varying factors affecting the sustainable development of all countries in our sample, and εit represents the random residual term.

Given that our sample is a macro panel data, we utilize two-way fixed effect (with country and year FEs) regression method to estimate our model. The suitability of fixed-effect over random-effect regressions is supported via the robust Hausman test. Additionally, we employ robust standard errors in all regressions.

In this study, we collected data from two different sources. First, we collect data on pension contributions, pension benefits paid, saving rate and net lending from OECD statistics database. Here, the pension funds that are examined in this study represent private pension schemes. Secondly, we collect data on macroeconomic variables from the World Development Indicators (WDI) database (World Bank). Integrating data from these three sources generates a final sample of 242 country-year observations, including 26 countries over the period from 2011 to 2021. Because some countries have missing data for certain years, there are 242 observations in total. The choice for these 26 OECD countries is purely due to data availability. Table 1 presents the list of 26 selected OECD countries. Variable definitions and sources are reported in the Appendix.

List of Sample Countries

| Australia | Austria | Spain | Netherlands |

| Canada | Hungary | Estonia | Poland |

| Switzerland | Israel | Finland | Portugal |

| Chile | Italy | France | Turkey |

| Czech | Korea | United | United States |

| Republic | Kingdom | ||

| Germany | Lithuania | Greece | |

| Japan | Mexico | Costa Rica |

Table 2 presents the descriptive statistics of the main variables employed in our analysis. It can be seen that the amount of pension contributions on average accounts for 2.142% of GDP among OECD countries while the amount of pension benefits paid approximates roughly 1.554% of GDP. Next, the amount of net saving accounts for almost 7% of GDP, and its standard deviation indicates large variations across OECD economies. In contrast, the amount of net lending is only 0.88% of GDP. Regarding control variables, Internet access in OECD countries is quite high since on average more than three quarters of a country’s population use the Internet. In addition, the countries in our study sample seem to be quite comparable in terms of socio-economic conditions as reflected by the relatively low standard deviations of real GDP per capita, life expectancy and mortality rate. The proportion of the labor force with basic education differs significantly among sampled countries with the average figure being 40.969.

Summary Statistics

| N | Mean | Std. Dev. | min | p25 | Median | p75 | max | |

|---|---|---|---|---|---|---|---|---|

| PENCON | 242 | 2.142 | 2.226 | 0.183 | 0.462 | 0.986 | 2.995 | 7.816 |

| PENBEN | 242 | 1.554 | 1.898 | 0.004 | 0.215 | 0.443 | 2.772 | 5.924 |

| SAVING | 237 | 6.943 | 5.131 | -1.941 | 3.442 | 6.854 | 9.764 | 18.588 |

| LENDING | 234 | 0.88 | 3.592 | -4.835 | -1.864 | 0.748 | 3.061 | 7.755 |

| LNGDPCAP | 242 | 10.183 | 0.574 | 9.29 | 9.621 | 10.276 | 10.699 | 10.996 |

| INTERNET | 238 | 79.278 | 11.375 | 55.05 | 71.635 | 82.318 | 88.41 | 93.898 |

| AGEDEP | 242 | 51.078 | 4.416 | 41.881 | 48.414 | 51.392 | 54.207 | 58.657 |

| LABOREDUC | 238 | 40.969 | 11.960 | 18.64 | 33.31 | 42.02 | 49.98 | 59.3 |

| LIFEEXP | 222 | 4.381 | 0.033 | 4.312 | 4.361 | 4.394 | 4.407 | 4.422 |

| MORTALITY | 200 | 7.447 | 3.478 | 3.1 | 4.45 | 6.2 | 10.55 | 14.1 |

Table 3 shows the correlation matrix of the key variables in our analysis. The pension variables, namely pension contributions and pension benefits paid are highly correlated with each other. Both pension variables are negatively correlated with net lending, however, saving rate is positively correlated with pension contributions but negatively correlated with pension benefits paid. Overall, the correlation coefficients between the control variables are relatively low, with the highest being −0.65 between GDP per capita and mortality rate. We also use the Variance Inflation Factor (VIF) to check for potential multicollinearity issue and find that the VIF values for all the variables are less than 5, indicating that multicollinearity is not a concern for our empirical model (Vu et al., 2015).

Pairwise Correlations

| Variables | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) |

|---|---|---|---|---|---|---|---|---|---|---|

| (1) PENCON | 1.000 | |||||||||

| (2) PENBEN | 0.885 | 1.000 | ||||||||

| (3) SAVING | 0.239 | -0.013 | 1.000 | |||||||

| (4) LENDING | -0.043 | -0.054 | 0.363 | 1.000 | ||||||

| (5) LNGDPCAP | 0.518 | 0.694 | -0.169 | 0.166 | 1.000 | |||||

| (6) INTERNET | 0.351 | 0.442 | 0.220 | 0.297 | 0.612 | 1.000 | ||||

| (7) AGEDEP | -0.186 | -0.017 | -0.437 | 0.109 | 0.310 | 0.116 | 1.000 | |||

| (8) LABOREDUC | 0.410 | 0.323 | 0.065 | -0.203 | 0.131 | 0.020 | -0.188 | 1.000 | ||

| (9) LIFEEXP | 0.342 | 0.368 | -0.077 | 0.089 | 0.722 | 0.405 | 0.158 | 0.298 | 1.000 | |

| (10) MORTALITY | -0.117 | -0.191 | 0.190 | -0.396 | -0.650 | -0.574 | -0.470 | 0.102 | -0.586 | 1.000 |

| VIF | - | - | 1.67 | 1.58 | 3.54 | 2.55 | 1.65 | 1.36 | 2.77 | 3.62 |

Table 4 presents the results of the baseline model examining the impacts of saving rate and net lending on pension contributions (Columns 1-2) and on pension benefits paid (Columns 3-4). In this table, Columns (1) and (3) report the results of the model using country fixed effects whereas Columns (2) and (4) report the results of the model using both country and year fixed effects. Due to missing data and the use of lagged variables the regression models include 190 observations.

Regression Estimates of Pension Contributions and Pension Benefits Paid

| VARIABLES | (1) | (2) | (3) | (4) |

|---|---|---|---|---|

| SAVING | -0.038* | -0.033 | -0.053*** | -0.055*** |

| LENDING | 0.012 | 0.004 | 0.021 | 0.022* |

| LNGDPCAP | 0.356 | 0.426 | 1.076* | 0.738 |

| INTERNET | 0.007* | 0.000 | 0.003 | -0.010** |

| AGEDEP | -0.038* | -0.062** | ||

| AGED-TO-WORKING | -0.002 | 0.082* | ||

| LABOREDUC | 0.026* | 0.029* | -0.035*** | -0.027*** |

| LIFEEXP | 17.438*** | 15.307** | 9.078 | 5.243 |

| MORTALITY | 0.013 | 0.028 | 0.023 | 0.031 |

| Constant | -77.339*** | -67.225** | -46.641* | -32.310 |

| Country FEs | YES | YES | YES | YES |

| Year FEs | NO | YES | NO | YES |

| Observations | 190 | 190 | 190 | 190 |

| Within R-squared | 0.1577 | 0.1462 | 0.4215 | 0.3341 |

Note: Robust standard errors in parentheses.

*** p<0.01,

** p<0.05,

* p<0.1

Results show that the saving rate appears to be negatively associated with both pension fund revenues and pension fund expenditures as reflected in the statistically significant coefficients when controlling for only country fixed effects or for both country and year fixed effects. This implies that the impact of saving rate on pension contributions and pension benefits paid is consistent even after controlling for the unobserved time-invariant differences across countries and any time-specific shocks that affect all countries. Although higher savings rates can potentially enhance individual financial security, they can also have negative effects on private pension contributions and benefits at a larger economic scale. The dynamic relationship between decreased consumption, decelerated economic growth, and governmental measures might lead to a situation in which increased savings rates unexpectedly diminish the efficacy and advantages of private pension systems (Blau, 2016; Carroll & Weil, 1994; Feng et al., 2011; Gebesoglu et al., 2023; Modigliani et al., 1954). The negative association between saving rate and pension fund expenditures may reasonably imply that as individuals increase their current private savings, they would be less dependent on future pension entitlements. In addition, the reverse relationship between saving rate and pension contribution is consistent with the life-cycle model of intertemporal decision making, which predicts that an increase in future pension wealth will be offset by a reduction in individuals’ savings (Feng et al., 2011; Blau, 2016). Our finding also points to the substitution effects between pension contributions and savings in OECD countries. Such a negative relationship is also revealed in a recent study by Gebesoglu et al. (2023).

On the other hand, net lending does not seem to have any significant influence on pension fund revenues, however, there is a slight positive impact on pension benefits paid since this is evident in the positive coefficient of LENDING at 1% significance level in the last column of Table 4. National net lending rates refer to the difference between a country's savings and investments, often reflecting the fiscal health of the government. When a country has a positive net lending rate, it means that the government is running a surplus or at least not accumulating debt. Governments with budget surpluses have more flexibility to allocate funds to pension benefits, potentially increasing the amount paid to retirees. In addition, a positive net lending rate can be indicative of overall economic stability and growth (Fourkan, 2021). A strong economy generally leads to higher employment and wages, which increases contributions to pension funds through payroll taxes and personal savings. Increased contributions help to build larger pension reserves, enabling higher benefits paid out.

It is worth pointing out that while both saving rates and net lending influence pension fund expenditures, the impact of the former is of larger magnitude than the latter. This could be potentially owing to less imperfections in the credit market among OECD countries, which reduces the limiting effect of borrowing constraints (Diamond & Hausman, 1984; Dicks-Mireaux & King, 1984).

Regarding the control variables, it can be observed that age dependency ratio tends to exhibit negative impacts on the pension fund revenues whereas life expectancy exhibits positive impacts. These influences are however not surprising. Specifically, an increase in age dependency ratio signals a rise in the non-working population, or equivalently, a reduction in the proportion of working population, which would mean less pension contributions by employees. As individuals are living longer, they will need better pension entitlements to spend during a longer period of retirement. Based on a forward-looking behaviour, individuals would be more willing to increase their amount of pension contributions now to be able to better enjoy their retirement in the future.

On the other hand, the coefficients of Internet access and labour education seem to be significantly negative for pension fund expenditures. As a higher level of Internet access represents a higher level of technological development and also a better environment for the growth of Fintech companies, individuals can have more choices on products related to pension insurance and pension investment and as a result they would be less dependent on pension benefits received. Also, increased Internet access may provide individuals with access to alternative investment opportunities beyond traditional pension plans. Online investment platforms, crowdfunding websites, and cryptocurrency exchanges offer avenues for investing in assets with potentially higher returns or greater liquidity compared to private pension funds. Individuals may choose to allocate their savings to these alternative assets instead of contributing to private pension plans, reducing the amount of pension benefits paid out during retirement.

Besides, a more literate workforce is better prepared for their retirement, thus relying less on their pension entitlements. In addition to the higher level of preparedness, highly educated individuals may feel more confident in their ability to manage their finances effectively without relying on traditional retirement savings vehicles such as pension plans (Mitchell & Utkus, 2004). These individuals may be more inclined to invest in alternative assets, start their own businesses, or pursue higher-risk, higher-return investment strategies based on their perceived financial acumen. Consequently, they may contribute less to pension plans, resulting in lower pension benefits paid out in the future.

To ensure that our main findings are robust, we also perform a battery of robustness checks. In the first set of these tests, we perform clustered robust standard errors at both country level and region level. The main purpose is to account for heteroscedasticity and within-cluster serial correlations (Petersen, 2009)2. Next, one may also be concerned that our results might be confounded by the impact of the COVID-19 pandemic (see, among others, Feher & de Bidegain, 2020; Natali, 2020). In our model, the impact of COVID-19 is accounted by the use of time FEs that capture common time-varying shocks for all countries. Nevertheless, we still take one step further by excluding the COVID-19 period (2020-2021) and re-estimate the model accordingly. Finally, one might concern that our results could be driven by outliers in the sample. Following the standard practice, we winsorise all of our variables at 1% level on each tail and re-estimate the baseline model accordingly. The results in all of the robustness checks show that the coefficients of the variables of interest do not change materially. Detailed results are available from the authors.

This paper is likely the first to analyse the impact of savings rate and net lending on pension fund revenues and expenditures. Using fixed-effect panel regressions on a panel data of 27 OECD countries from 2011 to 2021, our results indicate a negative association between savings rate and pension contributions as well as pension benefits paid. In addition, net lending does not seem to have any significant influence on pension fund revenues, however, there is a slight positive impact on pension benefits paid. These results are robust to various model specification and estimation techniques.

Our findings provide some important implications for policy makers. First, the empirical finding about the inverse relationship between savings rate and pension contribution potentially implies the substitution effect of voluntary savings for pension contribution. Thus, in order to maintain an adequate level of contribution to the pension funds, policymakers need to carefully design incentives for both private savings and pension contributions. Overemphasizing one form of saving might inadvertently discourage the other. For example, if tax incentives are heavily skewed towards private savings accounts, individuals might reduce their contributions to employer-sponsored pension plans, potentially undermining the financial stability of these plans. Pension systems might need to be adapted to account for changes in savings behavior. For instance, if private savings rates are high and reducing the reliance on pension contributions, pension systems might focus more on providing a safety net for those with lower private savings rather than serving as the primary source of retirement income for everyone. Second, since the slight positive impact of net lending on pension benefits is revealed in our empirical analysis, policymakers should continue to improve the efficiency and transparency of the credit market. The empirical findings also point out that labour force education and the level of Internet access help to increase the pension contributions while reducing the dependence on pension benefits paid. Therefore, re-enforced efforts should be put on raising the proportion of labour force with basic education as well as implementing the Internet facilities and boosting the digitalisation process particularly in providing financial services.

However, our study is not without limitations. First, we only consider OECD countries, which are generally considered higher-income economies. Second, economic and financial literacy, which might impact an individual’s assessment of the pension wealth and the offset between pension and non pension wealth (Bernheim, 1994), thus could potentially moderate the relationship between saving rate, net lending and pension fund revenue as pension fund expenditures. Third, other factors such as urbanisation (Gebesoglu et al., 2023), the availability of credit (McKinnon, 1973; Shaw, 1973), and interest rates (Grigoli et al., 2014) might be further added into the regression models as other control variables. Finally, the choice between private savings and pension contribution is rather personal, requiring a micro-level analysis whereas our study is based on a macro-level perspective.

Based on these limitations, further research could elaborate on the impact of savings rate and net lending on pension funds in lower-income countries. In addition, examining the moderating role of financial literacy and financial inclusion could also be a promising venue for future studies. Next, other controls including urbanisation, interest rate, and credit availability could be further incorporated into the regression model. Also, future research could investigate the relationship between savings, borrowing and pension contribution through the lens of a micro-level analysis using individual survey data.