Scholarly and policy interests in asset-building programs for low-income populations have increased since the 1990s as assets and savings have become acknowledged as crucial tools for long-term economic security and development (Sherraden, 1991). In contrast to income-based social policy that focuses mainly on basic economic needs for short-term survival, asset-based social policy aims to enable individuals to achieve fuller economic potential by motivating low-income individuals to save for long-term economic development (e.g., education) and security (e.g., emergency) (Nam, Huang, et al., 2008; Sherraden, 1991).

To promote asset-building among low-income populations, Sherraden proposed an Individual Development Accounts (IDAs) policy. In contrast to traditional policies that facilitated asset-building mostly for middle- and high-income families through the tax system (e.g., tax incentives for homeownership), IDAs are an active public investment that expands asset-building opportunities for the economically disadvantaged. IDAs provide matching funds to incentivize program participants to save for longer-term economic goals such as homeownership, higher education, and business start-ups (Sherraden, 1991).

IDA policies have been tested or implemented in many areas of the world. The first IDAs program, the American Dream Demonstration (ADD), was initiated in the United States between 1997 and 2002, using grants from private foundations (Schreiner & Sherraden, 2007; Mills et al., 2008). In 1998, the U.S. Congress enacted the Asset for Independence Act (AFI) that offered grants to state governments and non-profit organizations to run IDA programs for low-income families. In fiscal year 2014, the federal government supported 846 AFI projects using $214 million (Mills et al., 2019; Nam, McKernan, & Ratcliffe, 2008). The United Kingdom government started the Saving Gateway program as a pilot project in 2002 and expanded it to a national policy in 2010 (Rablen, 2010; Sodha & Lister, 2006). In Taiwan, the Taipei City Government initiated Taipei Family Development Accounts in 2000, which was adopted by several local governments (Zou et al., 2015). In Canada, Social and Enterprise Development Innovation, a non-profit organization, initiated an IDA program, Learn$ave, in 2009 (Leckie, Hui, Tattrie, Robson, & Voyer, 2010).

South Korea adopted IDA programs rapidly and widely. The concept of IDAs was first introduced at the 56th Korean Meeting on National Policy Tasks in 2004. The Seoul Metropolitan Government launched an IDA program for working-poor families in 2007 (Han & Kim, 2015). The national government launched a series of nationwide IDA programs for different groups of working poor: “Hope” Accounts I in 2010, “Tomorrow” Accounts in 2013, and “Hope” Accounts II in 2014 (Han & Kim, 2015; Kim et al., 2015).

Although multiple national and local governments and community organizations adopted IDA programs, empirical evidence about the impacts of this policy innovation has been lacking. A small number of studies have examined IDA programs, mostly in the United States, and these studies generated mixed results (Birkenmaier et al., 2022). Ten-year research on the American Dream Demonstration (ADD) shows little or no impact of IDAs on net worth (Mills et al., 2008) and retirement savings (Grinstein-Weiss et al., 2015). In terms of homeownership, renters in the treatment group were significantly more likely to buy a house than their counterparts in the control group during or shortly after the intervention period (Mills et al., 2008). However, the treatment control group differences declined over time and their statistical significance disappeared after 10 years (Grinstein-Weiss et al., 2013b). The ADD’s treatment effects on home ownership, however, remained significant among renters with disabilities after 10 years (Huang, Lombe, Putnam, Grinstein-Weiss, & Sherraden, 2016). ADD treatment significantly increased college enrollment, but did not make a significant impact on degree completion (Grinstein-Weiss et al., 2013a). However, a recent study on the Assets for Independence (AFI) program indicates more positive impacts. Government-funded IDAs in Albuquerque and Los Angeles increased participants’ liquid assets significantly and reduced their risk of experiencing material hardship and utilizing check-cashing services (Mills et al., 2019).

There are fewer empirical studies of IDAs outside the United States. Canada’s Learn$ave program is estimated to have little impact on net worth and liquid assets but to have increased education enrollment and business start-ups. At the same time, Learn$ave encouraged IDA participants to do budgeting and save regularly (Leckie et al., 2010). The United Kingdom’s Saving Gateway generated mixed results: Saving Gateway participation is associated with reduced savings among individuals with access to credit, but increased savings among individuals with credit constraints (Rablen, 2010).

Korea is not an exception. Although South Korea has implemented multiple IDA programs at the national and local levels, few empirical studies examined the effects of these programs. A quasi-experimental study of Seoul Metropolitan City’s Hope Plus Savings Accounts showed positive effects on financial behaviors: treatment group members were significantly more likely to make financial plans, save for unexpected economic costs, and educate their children about financial management than comparison group members with similar socioeconomic status (Kim, Lee, & Sherraden, 2012). Among Hope Plus Accounts participants, mean monthly savings amounts in non-IDAs (private accounts) declined over time, suggesting that program participants saved in their IDAs instead of non-IDAs to take advantage of financial incentives (Kim, 2014). A monitoring and evaluation report of Hope Accounts, nationwide IDAs for public assistance recipients, showed somewhat negative effects: 34.5% of participants dropped out of the program within three years of policy implementation, suggesting that a substantial proportion of public assistance recipients had a hard time saving in their IDAs. Participants also showed ambivalent attitudes towards the policy: 42% were hesitant to participate in the program mainly because of the following program rule: Participants must exit public assistance programs to receive saving incentives (Choi, Han, & Choi, 2012). In summary, previous studies on Korea’s IDA policies generated mixed results and our knowledge of the effects of IDAs on savings outcomes is limited.

To fill the gaps in our knowledge, this study investigates the associations between access to (eligibility for) a nationwide IDA policy and low-income individuals’ savings outcomes in Korea. Using survey data from a probability sample of the Self-Sufficiency Program (SSP) participants, this study asks whether and how being eligible for IDAs affects SSP participants’ savings.

This study utilizes survey data collected from Self-Sufficiency Program (SSP, “Jawhal”) participants in Korea. SSP was launched soon after the 1997 Asian economic crisis to address skyrocketing unemployment and poverty rates. President Kim Dae-Jung’s Administration restructured the welfare system in Korea, establishing SSP in 2001 under the National Basic Livelihood Security Act (NBLSA). Because of the unique socioeconomic conditions in Korea at that time, NBLSA had both social democratic and neoliberal characteristics. While recognizing the need for an active government role in maintaining safety nets for all Koreans and the expansion of social welfare institutions, the Kim administration was pressured to control social spending and minimize welfare dependency. Accordingly, NBLSA was a consequence of political compromise (Hong & Song, 2006; Kim & Zurlo, 2007). On one hand, NBLSA enhanced the welfare system by offering cash assistance to everyone living in poverty. On the other hand, NBLSA required able-bodied recipients of cash assistance to work or to participate in SSP.

As described above, SSP is primarily a workfare program for able-bodied cash assistance recipients and offers employment opportunities and job training. While SSP mandates able-bodied welfare recipients to participate in the program, it allows non-beneficiaries of cash assistance to partake in the program if they meet income and other eligibility rules. It offers two types of job opportunities: social service jobs at non-profit or public-sector organizations, and market-entry jobs at private companies. Participants in the market-entry job program are usually more competitive in the labor market than those in the social service job program. Participants are allowed to stay on SSP for up to five years. SSP is implemented and operated by local self-sufficiency centers under the supervision of the Korea Development Institute for Self-Sufficiency and Welfare, a government agency (Kim & Zurlo, 2007; Ministry of Health and Welfare, 2019a).

The Tomorrow Accounts (TAs) IDA program was added to SSP in 2013 as a way to enhance long-term economic security and development among SSP participants (Han & Kim, 2015; Choi et al., 2012). The Korea Development Institute for Self-Sufficiency and Welfare operates the nationwide TAs program in collaboration with local self-sufficiency centers. SSP participants are automatically eligible for and have access to the TAs program. That is to say, low-income SSP participants can open and start saving into an IDA (TA) and taking advantage of generous asset-building programs immediately after their participation in SSP. After being enrolled in the TAs program, SSP participants are required to save fixed amounts (50,000 or

100,000, or $50 or $100, assuming an exchange rate of

1000 to $1) each month for three years. Savings incentives in the TAs are strong: a 100% saving match from the government, 100% or 50% savings match from self-sufficiency centers, and up to $150 profit sharing from employers. If TA participants meet all eligibility criteria and save $100 per month for three years, they receive up to $16,200, plus interest. Participants are allowed to use TA funds for housing (home purchase or rent deposit), higher education or job training, and business start-ups (Ministry of the Health and Welfare, 2019b).

At the same time, the TAs program has very strict rules. First, TAs participants are required to deposit a predetermined monthly saving amount without interruption. If participants have not deposited a monthly saving amount for six months, their TAs are automatically closed and only their own deposits and interest are returned. Participants are permitted to stop their saving into TAs temporarily when they face economic challenges (e.g., illness). Second, TAs participants are required to achieve self-sufficiency to receive savings incentives. Low-income SSP participants must exit cash assistance programs and may not rely on public assistance. Third, TAs participants are required to withdraw their own savings, interest, and incentives within three months of completing three years on the TAs program. At the same time, they are mandated to provide proof that their withdrawals will be used for permitted activities. If TAs participants are unable to meet all program requirements after three years’ participation in TAs, they receive only their own deposits and interest (Korean Ministry of the Health and Welfare, 2019b).

This study uses survey data collected from SSP participants in South Korea. The sample was created using two-stage cluster systemic random sampling. At the first stage of sampling, the first author selected local self-sufficiency centers based on a sampling frame provided by the Korea Association of Local Self-Sufficiency Centers. The sampling frame includes every local Self-Sufficiency Center in Korea. In consideration of regional differences, the first author divided the centers on the list by region and selected every fifth center from each region. Forty-eight local Self-Sufficiency Centers were selected out of 249 on the list. At the second stage, the first author invited the selected 48 centers to the research project, of which 38 centers agreed to participate and provide lists of all SSP participants at each respective center. Using the participant lists, the first author selected every second participant into the survey sample.

The survey was conducted between June 24 and September 19, 2019. Data were collected through in-person interviews, using the survey questionnaire developed by the first author. Either a caseworker or an administrator at each Self-Sufficiency Center interviewed each study participant. Accordingly, interviewers had prior relationships with study participants. The research team decided to rely on caseworkers and administrators for data collection because of budgetary limitations. To minimize undue influence, the research team trained interviewers about research ethics and requested they did not force SSP participants into the study. Out of 1,344 SSP participants who were invited, 1,023 completed survey interviews, a 76% response rate. We excluded three respondents from analysis because their surveys were incomplete. The final analysis sample consisted of 1,020 respondents. The design of the study was reviewed and approved by the Institutional Review Board at the first author’s university (IRB ID: NSU-201905-004).

The dependent variable of this study was self-reported saving outcomes. The survey asked the savings amounts, if any, deposited by the respondent in the previous month into IDAs and non-IDA private accounts. Based on answers to these two questions, we created a nominal variable with four distinct categories: (1) no savings (zero savings into both types of accounts), (2) IDA only (positive savings amount into an IDA and zero savings into private accounts), (3) private accounts only (zero savings into an IDA and positive savings amount into non-IDA private accounts), and (4) both IDA and private saving accounts (positive savings amounts into both types of accounts). We decided to use a categorical variable of saving outcomes, instead of a continuous measure (e.g., total savings amount) because TAs only allow two monthly savings amounts: $50 or $100 every month. In addition, TA participants are required to make a deposit every month unless they have a program-defined excuse. Accordingly, there existed little variation in saving amounts in IDAs, which were the principal interest of this study. In addition, the nominal variable measures different saving decisions and behaviors of study participants. By categorizing savings outcomes into four categories, this measure shows whether a study participant saves and if so, what type(s) of account(s) they use.

The main independent variable was the length of SSP participation. As described above, SSP participants become automatically eligible for TAs. Therefore, the duration in SSP is the same as the period eligible for TAs. We hypothesized that the longer a study participant has participated in SSP and (therefore) been eligible for TAs, the more likely they were to take advantage of savings incentives and to save in IDAs. The survey questionnaire asked the calendar year and month when the study participant first participated in SSP. Using these answers, we calculated the number of months in SSP. We divided study participants into five groups as follows: 1–12 months (first year in SSP), 13–24 months (second year), 25–36 months (third year), 37–48 months (4th year), and 49 months or longer (fifth year). We chose duration in SSP participation as the main independent variable, not participation in TAs, because those who join TAs programs likely differ from those who do not in terms of unobserved characteristics (e.g., motivation to save). Because we rely on observation data, we cannot control for these unobserved characteristics between TAs participants and non-participants in estimating the effects of IDAs on savings outcomes. We decided to use eligibility as the main independent variable to estimate whether and how access to TAs is associated with savings outcomes among low-income SSP participants.

This study had three types of control variables: individual, family, and program characteristics. First, individual characteristics included a study participant’s gender, age, education, future orientation, financial capability, financial conflict, and history of debt default. Gender was a dichotomous variable (female versus male). Age was an ordinal variable consisting of the following categories: 29 years old or younger, 30 to 39 years old, 40 to 49 years old, 50 to 59 years old, and 60 years old or older. Education indicated formal educational attainment with three categories: less than a high school diploma, a high school diploma, and a college degree or higher.

Future orientation was defined as “the ability to behave in ways that support long-term goals” (Monahan, King, Shulman, Cauffman, & Chassin, 2015, p.1,267). In this study, future orientation was created with an eight-item measure developed for the Pathways to Desistance study: The Future Outlook Inventory (FOI) (Monahan et al., 2015). The FOI asks questions about study participants’ values, attitudes, or behaviors related to planning and preparing for the future (e.g., “I will keep working at difficult, boring tasks if I know they will help me get ahead later,” “I would rather save my money for a rainy day than spend it now on something fun”). The FOI’s reliability and validity were tested and verified (Monahan et al., 2015). Each question has five possible answers from “never true” (value of 1) to “always true” (value of 5). This study created the future orientation variable by averaging answers to the eight FOI questions. The values of the future orientation variable ranged from 1 to 5, with a higher value indicating being more future oriented.

The financial capability scale measured an individual’s financial management behaviors and confidence in dealing with financial matters. This scale included six questions (e.g., "Do you currently have a personal budget, spending plan, or financial plan?" and "How confident are you in your ability to achieve a financial goal you set for yourself today?") based on the scoring guide provided by the Center for Financial Security (Collins & O’Rourke, 2013). The potential range of this scale lay between 0 and 8, with a higher value indicating a higher level of financial capability.

In measuring financial conflict, this study used questions from a financial strain survey, an 18-item instrument recording “the cognitive, emotional, and behavioral response to the experience of financial hardship” (Aldana & Liljenquist, 1998, p. 11). From that instrument we selected four questions related to relationships (e.g., “Financial problems hurt my relationships”) (Aldana & Liljenquist, 1998). We created the financial conflict measure by averaging answers to the four questions. The potential value range of this variable lay between 1 and 5, with a higher value indicating more severe relational conflicts caused by financial difficulties. Debt default status indicated whether an individual was currently registered as a defaulting debtor in banking or credit institutions.

Family characteristics consisted of family size, marital status, family income, and housing type. Family size indicated the number of people in the family and consisted of three categories: 1 person, 2 people, and 3 or more people. Marital status was a nominal variable with four categories: currently married, never married, divorced, and widowed. Family income was a continuous variable: monthly income of the previous month. Housing type consisted of five categories: Owning a home, Jeonse rent, Wolse rent, public housing, and other housing arrangement. Jeonse is a unique rental system in Korea that requires a large lump sum initial deposit but no monthly rent. A landlord’s rental income comes from interest on the initial deposit. Wolse is a rental system common in the United States and Europe that requires a small initial deposit and monthly rent.

Program-related factors included the type of Self-Sufficiency Program and public assistance beneficiary status. The type of SSP has two categories: social service job programs versus market-entry job programs. Public assistance beneficiary status is a dichotomous variable indicating whether a study participant is a beneficiary of public assistance or not.

This study used multinomial logit regressions because the dependent variable was a nominal variable consisting of four categories: no savings (the reference category), IDA savings only, private savings only, and both IDA and private savings. Multinomial logit regression is a common statistical approach in analyzing unordered categorical response variables (Powers & Xie, 1999).

The regression analysis model had length of participation in SSP as the main independent variable. Since the association between the length of participation and savings outcomes may not be linear, this study used five dummy variables: 12 or fewer months (the reference category), 13–24 months, 25–36 months, 37–48 months, and 49 or more months.

Because the dependent variable consists of four categories, the multinomial logit regressions generated three sets of coefficients. First, the regression coefficients of the length in SSP were expected to be significantly positive for one’s chance of saving only into an IDA. As explained above, we hypothesized that program participants’ chances of learning about and taking advantage of TAs’ saving incentives increased as their time in the SSP increased because SSP participants automatically became eligible for TAs. Second, the direction of the relationship between length in SSP and one’s chance of saving into “private savings only” is unclear. It may be negative if SSP participants shifted their savings from private savings accounts to their IDAs. Otherwise, it may not be different from zero. Third, the impact of the IDA program on the chances of saving in both types of accounts was not obvious. If the IDA program increased only savings into IDAs, the coefficients of the length in SSP would not differ much from zero. If IDAs encouraged participants to manage finances prudently and to save as much as possible overall, the coefficients of the length in SSP would be positive.

The regression model controlled for the measures of individual, family, and program characteristics noted above. To account for potential non-linear relationships with savings outcomes, we used dummy variables for age and the log of family income in the regression analysis. Based on regression results, we estimated predicted probabilities to show how one’s saving outcomes change over the duration of SSP participation. In calculating predicted probabilities, we set the values of control variables at their means.

Table 1 presents our sample’s characteristics. In terms of length in SSP, about one in three study participants had been in SSP for 12 months or fewer, 17.4% were in the second year, 16.7% in the third year, 12.8% in the fourth year, and 16.9% in the fifth year.

Sample Characteristics of SSP Participants

| Variable | Statistics | |

|---|---|---|

| Program Duration (%) | ||

| 12 months or less | 36.2 | |

| 13-24 months | 17.4 | |

| 25-36 months | 16.7 | |

| 37-48 months | 12.8 | |

| 49 months or more | 16.9 | |

| Female (%) | 58.7 | |

| Age: (%) | ||

| 29 or younger | 4.9 | |

| 30-39 | 6.7 | |

| 40-49 | 18.9 | |

| 50-59 | 38.3 | |

| 60 or older | 31.2 | |

| Education (%) | ||

| Less than High School | 39.0 | |

| High School degree | 47.4 | |

| College or above | 13.6 | |

| Future Orientation, Mean (SD†) | 3.31 | (0.63) |

| Financial Capability, Mean (SD†) | 3.27 | (1.92) |

| Financial Conflicts, Mean (SD†) | 2.43 | (1.11) |

| Credit Default (%) | 17.4 | |

| Family Size (%) | ||

| 1 person | 47.4 | |

| 2 people | 25.6 | |

| 3 or more people | 27.0 | |

| Marital Status (%) | ||

| Never married | 23.5 | |

| Divorced/separated | 38.5 | |

| Widowed | 12.0 | |

| Currently married | 26.0 | |

| Family Income KRW†† | ||

| Mean | 1,300,000 | |

| Median | 1,200,000 | |

| Housing (%) | ||

| Homeowner | 14.0 | |

| Rent, Jeonse | 10.2 | |

| Rent, Wolse | 34.0 | |

| Public housing | 29.4 | |

| Others | 12.4 | |

| Program Characteristics (%) | ||

| Market-ntry Job (%) | 30.0 | |

| Public Assistance Recipient (%) | 63.0 | |

Note. N = 1,020;

Standard Deviation;

1,000 KRW is approximately 1 USD.

In terms of individual characteristics, the majority are female (58.7%) and older (69.5% are 50 years of age or older). Study participants’ educational attainment is relatively low: 39% do not have a high school degree, 47% have a high school degree, and 14% have a college degree. In the Korean adult population in general, these levels of educational attainment are 9%, 38%, and 53%, respectively (OECD. 2023). The mean value of future orientation is 3.3, suggesting that study participants, on average, chose a neutral answer (potential range: 1–5) to questions about their future orientation. The mean for the financial capability scale is 3.3 out of a 0–8 potential range, implying that study participants’ financial management and their confidence in handling financial matters is low. Study participants’ level of financial conflict is also low, with a mean value of 2.4 (1-5 potential range), indicating that study participants on average answered “somewhat not true” to financial conflict questions. About 20% reported that they were in default on some debt.

In terms of family characteristics, almost half of our survey respondents lived alone, about a quarter resided in families of two, and another quarter in families with three or more people. Among study participants, 24% had never married, 39 % were divorced, 12% were widowed, and 26% were currently married. Family monthly income was low, with a median of $1,200. Comparable statistics for Korean families are around $2,875 in 2019 (Statistics Korea, n.d.). Answers relating to housing type show study participants’ unstable economic situations. Only 14% owned their own house, 10% lived in “Jeonse” rent with a large initial deposit, 34% resided in “Wolse” rent, 29% in public housing, and 12% have other types of housing conditions. Program characteristics are also reported in Table 1. 30% were in the marketentry job program whereas 70% were in the social-service job SSP. At the same time, two out of three respondents received public assistance.

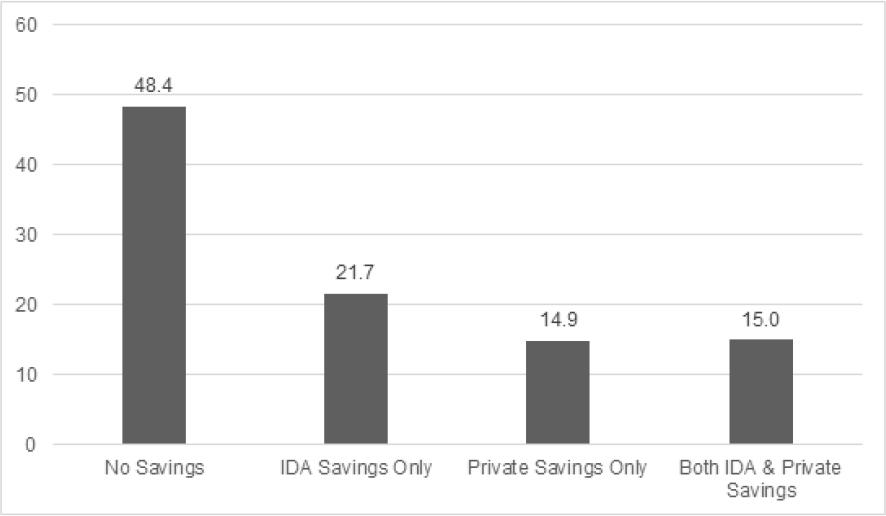

Figure 1 shows the distribution of savings outcomes. About half of respondents did not save at all in the month prior to the survey. One out of five participants saved only in an IDA. A small but substantial portion (15%) saved only in private accounts and gave up savings incentives offered by the IDA program. The remaining 15% saved in both types of accounts.

Savings Outcomes among SSP Participants

Table 2 presents results from multinomial logit regression analysis. Our control variables have the expected results. Among individual characteristics, financial capability has a significantly positive association with savings in private account only and in both types of accounts (p<0.05). Future orientation has a significant and positive association with savings in private account only (p<0.01). Credit default has a significantly negative association with savings in IDA only and private account only (p<0.05). Female, older, and more educated study participants are significantly more likely to save in both types of accounts (p<0.05). Among family characteristics, larger family size is associated with a higher chance of saving in both types of accounts (p<0.05). Among program characteristics, participation in a market-entry job program has significantly positive associations with savings in IDA only and both types of accounts (p<0.05).

Results of Multinomial Logit Regression Examining Savings Patterns of SSP Participants

| Variable | IDA Savings Only | Private Savings | Both IDA and | |||

|---|---|---|---|---|---|---|

| Coef. | SE | Coef. | SE | Coef. | SE | |

| Program Duration | ||||||

| 13-24 months | 0.43 | (0.28) | -0.10 | (0.29) | 0.56 | (0.30) |

| 25-36 months | 1.07** | (0.27) | 0.22 | (0.29) | 1.36** | (0.29) |

| 37-48 months | 1.48** | (0.28) | 0.34 | (0.32) | 1.21** | (0.33) |

| 49 months or more | 1.80** | (0.26) | 0.07 | (0.32) | 0.96** | (0.32) |

| Individual Characteristics | ||||||

| Female | 0.25 | (0.20) | 0.13 | (0.23) | 0.54* | (0.24) |

| Age | ||||||

| 30-39 | -0.30 | (0.54) | 1.12 | (0.63) | 1.78* | (0.74) |

| 40-49 | 0.05 | (0.44) | 1.02 | (0.59) | 1.54 | (0.70) |

| 50-59 | -0.11 | (0.44) | 0.38 | (0.59) | 1.51 | (0.70) |

| 60 or older | -0.10 | (0.48) | 0.72 | (0.62) | 1.55** | (0.73) |

| Education | ||||||

| High School degree | 0.31 | (0.21) | -0.27 | (0.24) | 0.50* | (0.24) |

| College or above | 0.49 | (0.30) | 0.11 | (0.32) | 0.75** | (0.33) |

| Future Orientation | 0.22 | (0.15) | 0.46** | (0.18) | 0.11 | (0.18) |

| Financial Capability | 0.09 | (0.05) | 0.34 | (0.06) | 0.37** | (0.06) |

| Financial Conflicts | -0.09 | (0.09) | 0.07 | (0.10) | 0.11 | (0.10) |

| Credit Default | -0.52* | (0.26) | -1.14** | (0.36) | -0.06 | (0.27) |

| Family Characteristics | ||||||

| Family Size | ||||||

| 2 people | 0.15 | (0.24) | 0.22 | (0.27) | 0.58* | (0.27) |

| 3 or more | 0.35 | (0.28) | 0.02 | (0.34) | 0.77* | (0.32) |

| Marital Status | ||||||

| Never married | 0.22 | (0.33) | 0.28 | (0.39) | 0.38 | (0.38) |

| Divorced/separated | 0.29 | (0.25) | 0.26 | (0.30) | 0.33 | (0.28) |

| Widowed | -0.03 | (0.33) | 0.39 | (0.36) | 0.13 | (0.38) |

| Family Income (Log) | -0.52 | (0.42) | 0.23 | (0.48) | 0.08 | (0.46) |

| Housing | ||||||

| Rent, Jeonse | -0.09 | (0.35) | -0.33 | (0.41) | -0.04 | (0.43) |

| Rent, Wolse | -0.37 | (0.28) | -0.23 | (0.32) | 0.15 | (0.34) |

| Public Housing | 0.04 | (0.29) | 0.04 | (0.33) | 0.33 | (0.34) |

| Other | -0.40 | (0.35) | -0.32 | (0.38) | -0.36 | (0.42) |

| Program Characteristics | ||||||

| Program Type: Market-Entry | 0.55** | (0.20) | 0.23 | (0.22) | 0.45* | (0.22) |

| Public Assistance Recipient | -0.19 | (0.20) | -0.11 | (0.22) | -0.31 | (0.22) |

| Constant | -0.27 | (2.22) | -5.80* | (2.58) | -6.91** | -2.51 |

Note. N = 1,020. Coef. = coefficient output of multinomial logit regression. SE = standard error‥

* p < 0.05

** p < 0.01

Multinomial logit regression shows that length of time in SSP (length of time for being eligible for TAs) is strongly associated with one’s chance of savings in an IDA. Every dummy variable for program duration has a positive and statistically significant coefficient for savings in IDA only and both IDA and private accounts at the 0.01 level, except for the 13–24 month category. These results suggest that the longer a study participant has stayed in SSP and been eligible for the TAs program, the higher his/her chance of saving in an IDA or both types of accounts. In contrast, length of time in the program is not significantly associated with one’s chance of saving in a private account only.

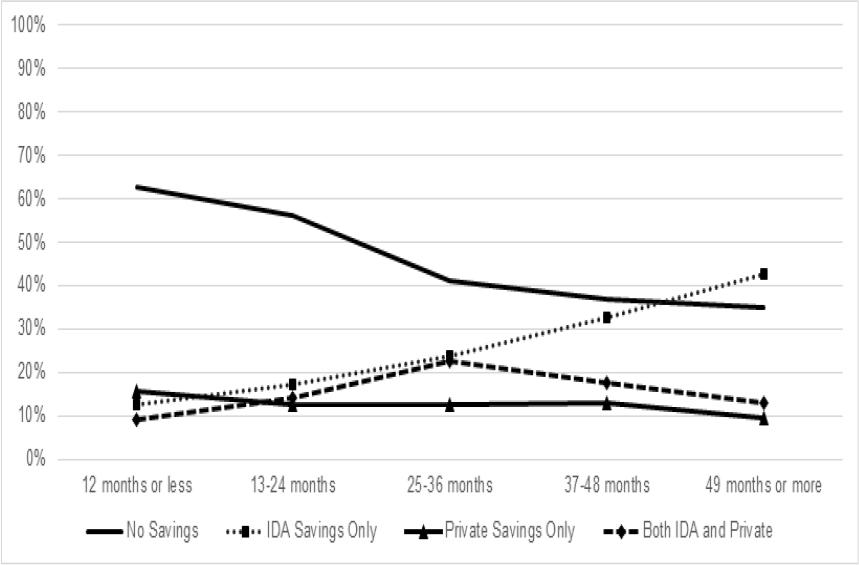

Predicted probabilities clearly show the associations between savings outcomes and the length of SSP participation. As mentioned above, predicted probabilities were estimated based on the results of the multinomial logit regression reported in Table 2. As shown in Figure 2, the estimated probability of no savings is 63% during the earliest period of the program (the first year). It declines to 56% in the second year, 41% in the third year, 37% in the fourth year, and 35% in the fifth year. A participant’s chance of saving only into an IDA increases as one’s time in SSP (being eligible for TAs) rises. The predicted percentage of program participants who save only in an IDA was 13% in the first year, but increased to 17% in the second year, 24% in the third year, 32% in the fourth year, and 43% in the last year. Participants’ chances of saving only in private accounts declined slightly (not statistically significant in the multinomial logit regression) over time: 16% in the first year, 13% in the next three years, and 9% in the fifth year. Study participants’ chances of saving in both types of accounts increased for the first three years (9% to 23%) and then declined for the last two years (18% and 13%).

Predicted Probabilities of Savings Outcomes by SSP participation length

This study investigates how access to IDAs affects saving among low-income participants in Korea’s Self-Sufficiency Program. Despite increased global interest in asset-building policies for low-income populations, empirical research on IDAs has mostly concentrated on programs in the United States. Few existing studies evaluated IDA policies outside the United States. Considering the variety of distinct economic, social, and cultural environments of low-income populations across different countries, it is imperative to study IDAs outside the United States. As mentioned earlier, Korea has adopted multiple nationwide and local IDAs policies over the last two decades, making it a suitable location in which to evaluate IDAs policies. The present study fills some of the gaps in our knowledge about IDAs using data collected from a probability sample of SSP participants in Korea.

The results of this study suggest that access to Tomorrow Accounts (TAs), one of Korea’s IDAs policies, has a positive association with savings into IDAs among low-income SSP participants. Since SSP participants become automatically eligible for TAs upon enrollment in SSP, this study uses the length of SSP participation to estimate whether and how TAs affect low-income SSP participants’ saving.

Multinomial regression analysis and predicted probabilities show that access to IDAs has a positive and significant association with one’s chances of saving in an IDA only. As length of SSP participation increases, the percentage of participants without savings decreased dramatically from 63% in the first year to 35% in the fifth year. At the same time, the proportion of study participants who saved only in IDAs increased considerably (13% to 43%) for the five years in SSP. These results imply that low-income individuals can save and accumulate assets if appropriate supports and incentives are provided.

Analysis results also show challenges in saving among low-income SSP participants. Although the proportion without any saving dropped considerably for the five years in SSP, a substantial portion (35%) did not save even at the end of the program. This study also found that a substantial minority of study participants saved only in private savings accounts and forewent strong saving incentives offered by IDAs. As shown in Figure 2, 9 to 16 percent of study participants are predicted to save only in private accounts for the five years in SSP. Considering the Tomorrow Accounts’ generous savings incentives, this result is unexpected. Some study participants may have been unaware of the IDAs program. Strict program rules may have discouraged participants from joining the IDAs program. As described above, SSP participants are required to exit public assistance programs in order to receive savings incentives. Low-income public assistance beneficiaries, especially those with multiple labor market barriers, may feel uncomfortable with leaving public assistance programs and view the generous saving incentives as unattainable. It is also plausible that some study participants save in this way to maximize their economic interests. Because the SSP and IDAs have different time limits for participation (5 years and 3 years, respectively), study participants are able to stay on these two programs for the longest period by joining IDAs later than the SSP. These explanations are, however, hypothetical. Further research is warranted to test these hypotheses empirically.

This study is not free from limitations. Because it relies on observation data, not experimental data, we cannot rule out the possibility that the significant association found between the length of SSP participation (being eligible for IDAs) and savings in IDAs may be explained by other factors. This study cannot establish causality without doubt. In addition, the cross-sectional data used in this study do not allow us to examine changes in savings and other characteristics over time. Accordingly, this study is unable to look at the dynamic process of how the SSP and IDA programs influence participants’ attitudes and behaviors related to saving and asset-building.

Our findings have the following implications for future policy and research. First, asset-building policies should be maintained and strengthened for the low-income population in Korea. As shown in Figure 1, more than half of low-income SSP participants do save, despite their low income and other challenges in their lives. Furthermore, multinomial logit regression and predicted probability analyses show that as the period of time of being eligible for IDAs increases, the chances of saving into IDAs increased and probability of not saving at all declined. These results suggest that asset-building programs have positive impacts on low-income individual’s savings, confirming the need for continued government investment into asset-building programs for low-income populations.

Second, targeted interventions are necessary for those with difficulties in saving. As shown above, a substantial percentage of study participants save in neither account. We should develop policies and programs to remove barriers to savings among these individuals after identifying challenges they face.

Third, further research is warranted for an in-depth understanding of whether and how IDAs affect low-income individuals. New and innovative studies may utilize various types of data (both qualitative and quantitative) and answer whether and how IDAs have influenced low-income participants over time. Future studies may ask why some participants give up the benefits of IDAs and choose to save in private accounts. More in-depth investigation on the topic would improve program design and implementation.