Wealth gaps based on gender and race represent some of the most persistent and deeply entrenched forms of economic inequality (Mahadevan, 2025). It is generally thought that disparities are not simply the result of contemporary market dynamics, but rather the culmination of centuries of structural barriers. Historical injustices — from slavery and Jim Crow segregation to redlining and employment discrimination in the United States — have denied Black Americans and other marginalized groups equitable access to wealth-building opportunities. For African American women and other intersectionally disadvantaged groups, the barriers to wealth accumulation are compounded, reinforcing cycles of economic hardship that persist across generations (Brown, 2012).

Recent research highlights the importance of utilizing historical and comparative data to better comprehend the underlying causes of these disparities and inform effective policy solutions. Researchers have shown, for instance, that the wealth gap experienced by Black women in the United States is alarmingly similar to that of post-Apartheid South Africa, with Black households in both countries holding a fraction of the wealth owned by their White counterparts (Chelwa et al., 2024). The emergence of Community Development Financial Institutions (CDFIs) in the mid-20th century was a response to the structural exclusion faced by historically underserved communities (Cherident & Gremillion, 2025). These institutions were designed to expand economic access and provide capital to communities that have been shut out of traditional financial systems. However, despite efforts aimed at economic empowerment, disparities persist.

This study presents a fresh perspective on the wealth gap experienced by Black women by examining historical risk tolerance data to gain a deeper understanding of the present-day wealth gap. Specifically, we examine patterns of risk-taking among Black women prior to the COVID-19 pandemic to better understand why the wealth gap has persisted over time, despite significant investments from CDFIs, private markets, and well-intentioned policy efforts. Using a historically informed, intersectional, and comparative framework, the study aims to uncover insights that can support the development of more inclusive economic policies — ones that effectively address systemic disparities and contribute to a more equitable financial future.

The wealth gap experienced by Black women has implications that go beyond questions of societal equality. The financial-services profession has an interest in the topic as it relates to expanding untapped markets and attracting new clientele, As highlighted by Grable and Joo (2003), Shahnaz (2021), and Walters (2007), Black women represent an underappreciated demographic within the financial-services marketplace. Despite facing systemic barriers to wealth accumulation, Black women remain a vital, yet frequently overlooked, group for financial advisors and institutions.

While scholars have explored income disparities between racial and gender groups, there is a dearth of research examining the intersectionality of race, gender, and wealth. The existing literature often treats race and gender discrimination as separate phenomena rather than as interconnected forces that jointly shape economic outcomes. This gap in the literature reflects the need for a more nuanced understanding of how Black women’s unique social and economic positions influence their ability to accumulate wealth (Brown, 2012). In this context, the present study was designed to uncover the relationships between race, gender-role attitudes, and risk tolerance (i.e., someone’s willingness to engage in a behaviour in which the outcome is uncertain and potentially negative [Rabbani & Nobre, 2022]) as factors explaining the level of wealth accumulation among Black women. We hypothesize that low levels of risk tolerance, a commonly cited factor in wealth accumulation, may disproportionately hinder Black women’s ability to build wealth, thereby contributing to the racial and gendered wealth gap. Specifically, the objectives of this study were to examine the association between racial identity and gender-role attitude, and to investigate whether risk tolerance is related to wealth-building trajectories.

The economic role of Black women in the United States has undergone significant evolution over recent decades. As Dau-Schmidt and Sherman (2013) note, Black women have entered non-traditional professions at a rate exceeding that of Black men, as well as non-Black women. However, substantial income and wealth disparities between Black and non-Black women persist. Much of the existing research on economic inequality focuses on income disparities (Hero & Levy, 2016). However, as Chang (2010) points out, the wealth gap between Black and non-Black women is an even more significant — and often overlooked — issue. Nearly half of all single Black women possess little to no wealth, with some even experiencing negative wealth (Rucks-Ahidiana & Kalu, 2023; Zaw et al., 2017). This wealth gap is exacerbated by historical and institutional factors, including unequal access to education, employment opportunities, and financial services (Chang, 2010; Elliott & Walker, 2022).

Gaining a better understanding of the relationships between race, gender, and financial risk tolerance is one way to decompose the wealth gap. Coleman (2003) was among the first to explicitly examine the role of risk tolerance in explaining differences in investment behaviour among Black, Hispanic, and non-Black households. Using data from the 1998 Survey of Consumer Finances, Coleman found that Black and Hispanic households held significantly fewer risky assets than non-Black households, contributing to a wealth gap between these groups. Coleman observed that, regardless of race, women tended to hold a lower percentage of risky assets than men, and older heads of household were also less likely to invest in higher-risk assets (Coleman, 2003, p. 43). Importantly, Coleman found that once wealth was controlled for, there were no significant racial or ethnic differences in risk tolerance, suggesting that wealth, rather than race or ethnicity, is a more prominent determinant of risk-taking behaviour.

Fisher (2019) expanded upon Coleman’s (2003) work by investigating racial differences in financial risk tolerance among Black and non-Black households. Using data from the 2016 Survey of Consumer Finances, Fisher examined how factors such as human capital (e.g., education, employment, age, and health status), financial variables (e.g., income, wealth, and financial knowledge), and life-cycle factors (e.g., marital status and family composition) explain variations in risk tolerance between Black and non-Black households. Fisher found that racial differences in risk tolerance were primarily due to disparities in human capital and financial variables. Black households were less likely to take financial risks, which Fisher attributed to the cumulative disadvantage that Black individuals experience across their course of their lives. As described by the life-course framework, this cumulative disadvantage — i.e., the process by which small initial disadvantages compound over time, leading to increasingly unequal outcomes between individuals or groups — suggests that race exacerbates economic inequalities by influencing various life opportunities and outcomes. Fisher concluded that, on average, Black households exhibit lower financial risk tolerance than their non-Black counterparts, primarily due to differences in wealth and human capital (Fisher, 2019).

A further examination of investment behaviour, specifically within African American communities, was conducted by Hudson et al. (2018), using data from the 2015 FINRA Financial Capacity Study. They found that African Americans were less likely to own higher-risk, higher-return investments like stocks, a pattern consistent with both Coleman’s (2003) and Fisher’s (2019) findings. This reluctance to invest in higher-risk assets was identified as a contributing factor to the wealth gap between Black and non-Black households. Hudson et al. (2018) applied family financial socialization theory to explain these disparities, noting that financial education, socialization, and income are positively correlated with investment in risky assets. Individuals with more financial knowledge, those whose parents financially socialized them, and those with higher incomes were more likely to purchase riskier investments. However, Hudson et al. (2018) did not find risk tolerance itself to be a significant determinant of investment behaviour among African Americans, suggesting that other factors, such as financial literacy and socialization, may play more substantial roles.

In a subsequent study, Hudson et al. (2021) investigated the factors influencing the investment behaviour of African American women. Their findings underscore the importance of factors such as financial confidence, knowledge, and attitudes toward money in shaping investment decisions. African American women who felt more confident in their ability to manage finances and had a positive attitude toward money were more likely to invest in riskier assets, including establishing brokerage accounts. Despite the importance of their findings, the study’s reliance on a convenience sample of African American women limited the generalisability of these results (Hudson et al., 2021).

In relation to the broader understanding of risk tolerance, studies have examined how education mediates the relationship between gender and financial risk-taking. For instance, the research of Cupples et al. (2013) revealed a direct negative association between identifying as female and financial risk tolerance. However, when education was included in the analysis, the gender gap in risk tolerance diminished, suggesting that higher levels of education could reduce gender-based differences in risk tolerance. Other researchers, including Bark et al. (2016), have confirmed this finding, showing that education serves as an important mediator in the relationship between gender and risk tolerance.

Fisher (2019) highlighted the role of financial literacy as a proxy for education and its relationship with risk tolerance. Fisher found that financial literacy was positively associated with risk tolerance among non-Black households, but not among Black households. This discrepancy points to the complex relationships between education, financial knowledge, and racial differences in investment behaviour. While greater financial literacy generally leads to higher risk tolerance, Fisher (2019) found that Black households did not exhibit this pattern, suggesting that racial disparities in wealth and access to financial education may limit the impact of financial literacy on risk-taking behaviour.

Gender differences in financial risk tolerance have been well-documented, with women generally exhibiting lower risk tolerance than men. Fisher and Yao (2017) explored gender differences in financial risk tolerance using data from the 2013 Survey of Consumer Finances. They found that women were generally less risk-tolerant than men, but these differences were not strictly due to gender. Instead, gender differences in risk tolerance were influenced by how other factors, such as income and wealth, interacted with gender. Specifically, they found that higher net worth was positively associated with higher risk tolerance, particularly among men. Fisher and Yao suggested that income uncertainty and financial insecurity, which disproportionately affect women, may negatively impact women’s willingness to take financial risks.

Other studies have examined the social dimensions of gender and risk tolerance. For example, Lemaster and Strough (2014) found that men who adhered to more stereotypically masculine traits were more likely to exhibit higher risk tolerance compared to women who conformed to traditional feminine standards. This finding suggests that social and cultural attitudes toward gender roles are associated with attitudes and behaviours toward risk. This perspective aligns with Lemaster and Strough’s (2013), who highlighted the role of gender-role attitudes in describing financial risk behaviours.

Despite the growing body of literature on gender and financial risk tolerance, research specifically linking gender role attitudes to financial decision-making remains scarce. White et al. (2020) showed that race and ethnicity affect financial behaviours such as saving and banking, with African Americans receiving fewer financial messages related to saving and investing. This insight suggests that the financial socialization process, particularly among marginalized groups such as African American women, may play a crucial role in shaping financial attitudes and behaviours. Hudson et al. (2017) also emphasized the importance of family financial socialization in explaining financial behaviours, noting that African Americans’ primary financial influences include parents, life experiences, and formal financial education. The messages Black women receive often reinforce traditional gender role attitudes that discourage their participation in financial decision-making (van den Horst, 2014).

The following section builds upon the review of literature by presenting the conceptual framework and models used and tested in this study. This is followed by a description of the study’s methodology and results. The paper concludes with a discussion of findings and implications for practice, research, and policy.

Racial and gender disparities in wealth accumulation are a longstanding issue that has received significant attention in economic research (Chang, 2010; Coleman, 2003; Richard, 2014). The wealth gap between Black women and non-Black women remains stark, with single Black women, in particular, having a median wealth as low as $5, compared to $42,600 for non-Black women (Chang, 2010; Elliott & Walker, 2022). This disparity is particularly concerning in the context of retirement planning, as more than 25% of Black women rely solely on Social Security for retirement income, further underscoring the challenges they face in building wealth over their lifetimes (Chang, 2007; Zaw et al., 2017). Wealth is also linked to intergenerational mobility, as it provides Black families with the resources to invest in education and pass down assets across generations (Brown, 2012; Chang, 2007).

Although wealth disparities are well-documented, less attention has been paid to the role of risk tolerance in shaping wealth outcomes for Black women. This study posits that risk tolerance may be a critical-yet-underexplored factor mediating the relationship between race, gender, and wealth accumulation. In particular, we hypothesize that the financial decision-making of Black women is shaped by unique social and economic pressures that influence their willingness to take financial risks.

While the economic outlook for Black women remains challenging, they continue to play a vital role in shaping the economy. Black women are significant economic agents within their households, often setting consumption and financial priorities for their families (Barnes, 2008). Understanding the factors that limit their wealth accumulation can provide insights into how financial services and policy interventions can better support Black women in building wealth.

As Hanna and Gutter (1998) and Grable and Joo (2004) noted, very few models or frameworks have been developed to understand the determinants of risk tolerance at the household level. Of course, theories of risk aversion, particularly as an economic consideration, are extensive and widely reported in the literature (Barsky et al., 1997; Frey et al., 2017; Viceira, 2002); these theories, however, tend to focus on the measurement and estimation of risk aversion (the opposite of which is thought to be risk tolerance), rather than on identifying the factors associated with risk aversion or in describing how risk aversion/tolerance is associated with household-level outcomes like wealth accumulation (Ahamed & Limbu, 2024). Outside of economics, finance, and financial planning, considerable effort has been devoted to identifying factors associated with a person’s willingness to take risks. Drug- and alcohol-use researchers, for example, have reported observing numerous personal and household characteristics that can be used to describe risk-tolerance attitudes and risk-taking behaviours (e.g., Watt, 2005; Wood et al., 2013).

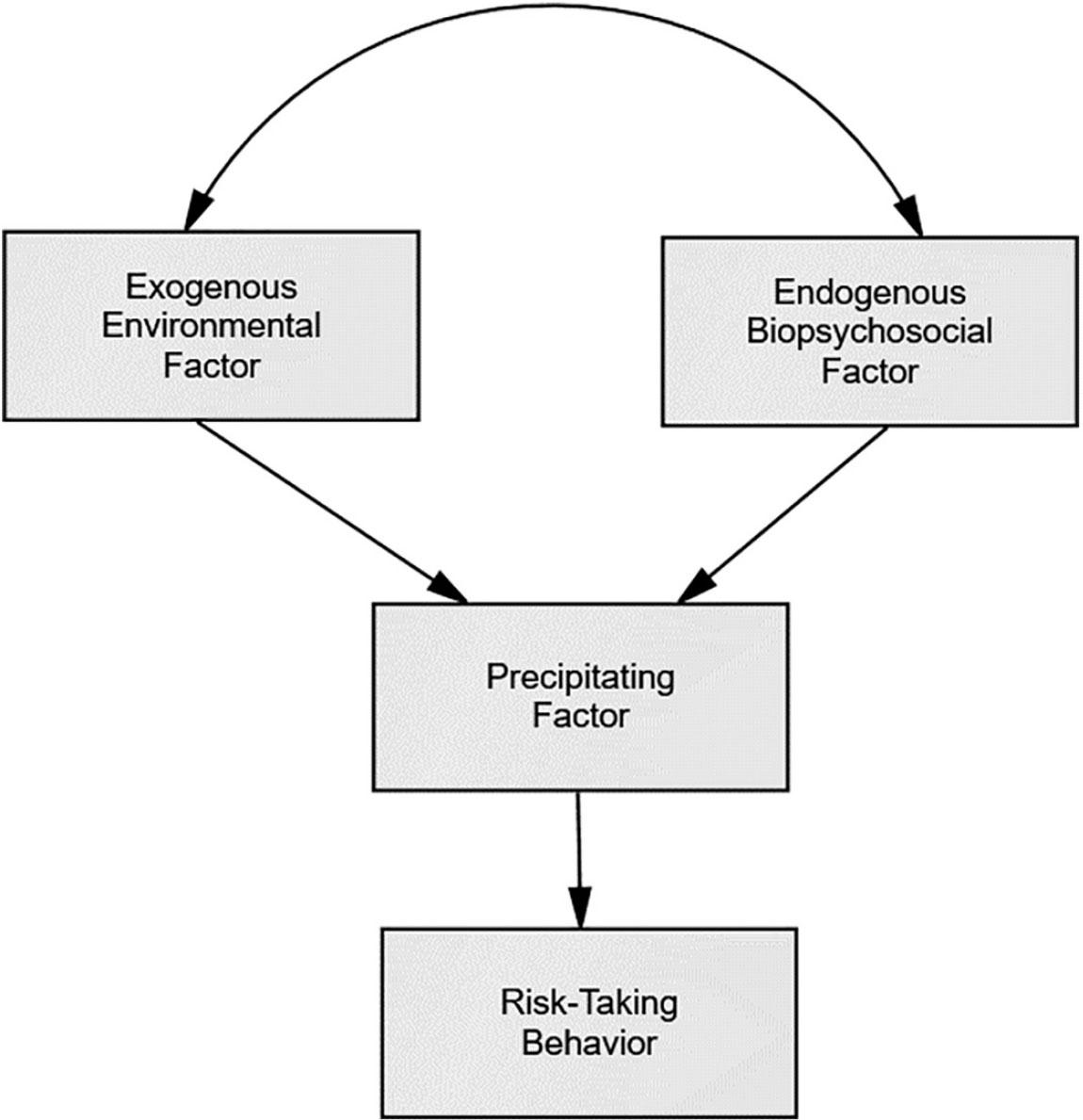

A widely used model is the biopsychosocial model of risk-taking behaviour, as proposed by Irwin and Millstein (1986) and updated by Irwin (1993). This framework was used to guide this study. The model shown in Figure 1 illustrates the framework, as conceptualized for this study:

Irwin and Millstein’s (1986) Biopsychosocial Risk-Taking Framework as Adapted for this Study.

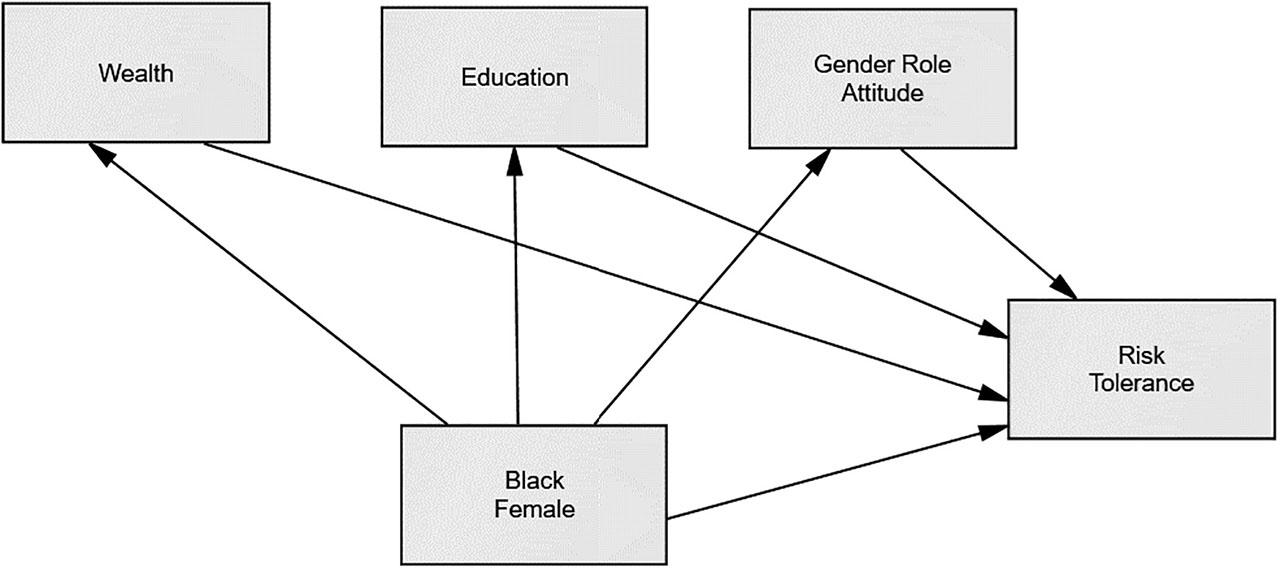

In the context of this study, wealth (i.e., household net worth) and education — an indicator of human capital — were inserted into the model as environmental factors. Race, sex, and gender role attitude were applied in the model as biopsychosocial factors, with family socialization being indicated by general role attitude. Figure 2 illustrates the path model used to test the framework. Wealth, education, and gender role attitude were hypothesized to be directly associated with risk tolerance (i.e., single-headed arrows running from each variable to risk tolerance). The variable Black Female (reference category: non-Black, non-Hispanic female) was hypothesized to be directly associated with risk tolerance. The framework differs the original conceptualization (Irwin, 1993) in that wealth, education, and gender role attitudes are hypothesized as mediating between Black women and risk tolerance.

Conceptual Framework.

Given the propositions shown in Figure 2, the following hypotheses were tested in this study:

H1: Risk tolerance is associated with being a Black female.

H2: Risk tolerance is associated with wealth.

H3: Risk tolerance is associated with attained education.

H4: Risk tolerance is associated with gender role attitude.

H5: Wealth mediates the association between risk tolerance and being a Black female.

H6: Education mediates the association between risk tolerance and being a Black female.

H7: Gender role attitude mediates the association between risk tolerance and being a Black female.

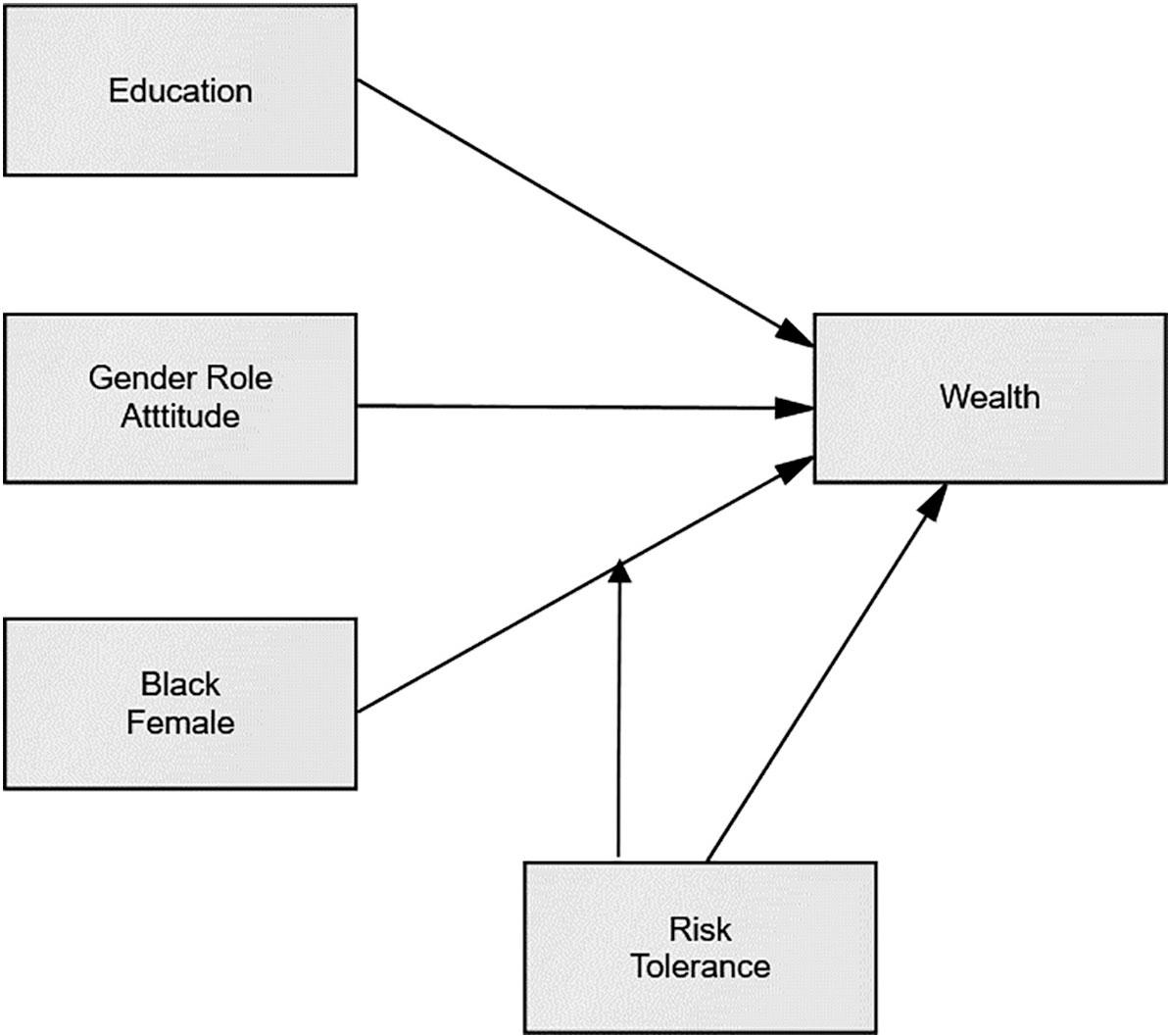

Tests of these hypotheses were used to determine the indirect, direct, and total effects of being a Black female as a biopsychosocial factor on risk tolerance. In this study, a second modification of the aforementioned conceptual framework developed by Irwin and Millstein (1986) and updated by Irwin (1993) was made and tested. The framework was modified to determine whether a relationship between wealth and race (i.e., being a Black female) is moderated by risk tolerance. The adapted framework is shown in Figure 3.

Modified Conceptual Framework.

The following hypotheses were tested in relation to the modified conceptual framework:

H8: Education is associated with wealth.

H9: Gender role attitude is associated with wealth.

H10: Being a Black female is associated with wealth.

H11: Risk tolerance is associated with wealth.

H12: Risk tolerance moderates the association between being a Black female and being wealthy.

Data for this study were obtained from the National Longitudinal Survey of Youth 1979 (NLSY79) dataset. The NLSY79, which is sponsored by the Bureau of Labor Statistics (BLS) of the United States Department of Labor, includes a set of surveys designed to gather information, at multiple points in time, on the labour-market experiences and other significant life events of a panel of men and women who were young adults in 1979 (i.e., survey respondents were ages 14 to 22 when first interviewed in 1979). The NLSY79 is a representative sample of 12,686 young men and women born from 1957 through 1964 and living in the United States when the survey began. Data were, and continue to be, gathered via interviews. At the project’s outset, data were collected annually from 1979 to 1994. Since 1994, data have been collected biennially.

Data for this study were downloaded from the NLSY79 investigator website in February 2021 and were recoded to include only women, with male respondents removed from the dataset.

While we acknowledge that using older data may be problematic in drawing contemporary conclusions, we believe the strengths offered by the NLSY79 dataset outweigh the potential limitations. Specifically, the NLSY79 includes validated measures of financial risk tolerance, but these were administered only in select waves (1993, 2002, 2004, 2006, 2008, and 2010). These data have not been replicated in newer surveys or subsequent waves of this cohort. These measures offer rare and valuable insights into individual-level behavioural and psychological traits associated with wealth accumulation, particularly when viewed through an intersectional lens. Furthermore, we believe that because risk tolerance is widely regarded in behavioural finance and psychology as a relatively stable, trait-like characteristic, especially in adulthood (e.g., Grable, 2016; Finke & Guillemette, 2016), risk attitudes do not exhibit the same volatility over time as situational factors like as market returns. Thus, relying on data from 2010 does not significantly impair our ability to draw valid inferences about long-term patterns in wealth formation or financial behaviour.

Moreover, incorporating a historical perspective is critical when attempting to understand persistent wealth disparities. The wealth gap between Black women and other demographic groups is not a recent phenomenon; it is a result of decades of cumulative disadvantage. A contemporary snapshot alone cannot fully account for the generational influences and policy contexts that shape economic outcomes over time. Using data from 2010 allows us to explore how financial attitudes and structural constraints evolve in tandem. For example, analysing risk tolerance patterns before the COVID-19 pandemic provides a rich narrative about why Black women continue to face compounded barriers to wealth accumulation, despite targeted interventions aimed at reducing the wealth gap. To provide confidence in the findings, robustness checks were undertaken for each model using the 2010 weighting variable in the NLSY79. The core findings reported in this study were observed with and without the weighting variable.

In accordance with Irwin and Millstein’s (1986) and Irwin’s (1993) biopsychosocial model of risk-taking behaviours, this study evaluated six variables: gender, race, risk tolerance, wealth, education, and gender-role attitude. Risk tolerance was used as the outcome variable in the first model, whereas wealth was used as the outcome variable in the second model. The operationalization of each variable is described in detail below.

To capture a robust measure of financial risk tolerance, this study combined two closely related NLSY79 survey items that assess general and domain-specific risk attitudes. The first item captured global risk tolerance by asking respondents to rate their general willingness to take risks: “Are you generally a person who is fully prepared to take risks, or do you try to avoid taking risks?” The second item explicitly focused on financial risk tolerance: “People can behave differently in different situations. How would you rate your willingness to take risks in financial matters?” Both items utilized an 11-point scale (0–10), allowing for methodological consistency and comparability.

Combining these two items is justified both conceptually and psychometrically. From a theoretical standpoint, prior research in behavioural economics and psychology has demonstrated that general and domain-specific risk attitudes are positively correlated, with financial risk tolerance often emerging as a stable subdimension of broader risk preferences (Grable & Rabbani, 2014; Weber et al., 2002). Psychometrically, combining these items improves reliability by reducing measurement error and capitalizing on the shared variance between general and financial risk-taking tendencies. While each question independently provides valuable information, the composite score better reflects an individual’s stable trait-level risk orientation and their context-specific financial behaviours. The combined risk-tolerance measure was developed using a principal-components factor analysis and a Promax rotation. Scores were then saved as a regression factor. The resulting factor score variable had a mean of 0, a standard deviation of 1.00, and a median of .0420. Higher scores were interpreted to indicate a greater willingness to take financial risks.

The NLSY79 measured wealth as total net family wealth, estimated by summing each respondent’s household asset values and subtracting all their debts. Given possible skewness in the variable, the log of wealth was used in all analyses. Although the nominal variable ranged from $0 to several million dollars, the log-transformed variable’s mean, standard deviation, and median were 4.8581, .8836, and 5.0201, respectively.

Education was measured with the following item: “What is the highest grade or year of regular school that you have completed and gotten credit for?” In 2010, answers ranged from two years to 20 years. The mean and median responses for 2010 were 13.34 years and 12.00 years, respectively. Education in 2008 was also estimated, with the mean and median numbers of years being 13.30 and 12.00, respectively. Given the potential endogeneity issues in the data and the relatively similar means and medians between 2008 and 2010, the 2008 education variable was used in each tested model.

Irwin (1993) noted that family socialization variables likely play a role in describing someone’s willingness to take a risk. Socialization factors may also be associated with wealth accumulation over a person’s lifespan. For this study, socialization was proxied with a variable called “gender-role attitude.” This variable was created using two items in a principal-components analysis with Promax rotation.

In 2004, the NLSY79 asked the following questions that were used in this study as indicative of gender role attitude: (1) “It is much better for everyone concerned if the man is the achiever outside the home and the woman takes care of the home and family” and (2) “Women are much happier if they stay at home and take care of their children.” Four choices were provided as response options: (1) strongly disagree, (2) disagree, (3) agree, and (4) strongly agree. For the first item, approximately 4% of respondents strongly agreed with the statement, while slightly more than 25% strongly disagreed. For the second item, more than 2% of respondents strongly agreed with the statement, while approximately 52% strongly disagreed. The resulting factor variable had a mean of 0, a standard deviation of 1.00, and a median of .2326. Higher scores were interpreted to mean that a respondent held a stronger traditional gender role attitude.

While contemporary research on gender role attitudes often draws from larger, comprehensive, multi-item scales, the use of just the two items was justified on three accounts. First, these two items represent core, canonical statements that directly tap into traditional gender ideology, specifically the separate-spheres doctrine — a foundational construct in sociological and psychological research on gender roles. This ideology posits that men and women occupy distinct and complementary domains, with men as economic providers and women as caregivers.

Decades of research — from Hochschild (1989) and Mason and Lu (1988) to Davis and Greenstein (2009) — have shown that endorsement of such beliefs is strongly predictive of broader gender attitudes and behavioural choices related to labour force participation, household division of labour, educational aspirations, and even risk preferences.

Second, these statements are not merely reflective of social views; they are normative assertions that reveal internalized expectations about gender roles and responsibilities. In a dataset where more comprehensive attitude batteries are unavailable, these items serve as valid proxies for a larger construct, which is consistent with established practice in secondary data analysis where item constraints exist (Rammstedt & Beierlein, 2014).

Third, there is precedent for the use of abbreviated gender ideology scales in large-scale social research. For example, multiple studies have used similarly worded two- or three-item scales to operationalize traditional versus egalitarian gender role attitudes. Empirical findings have demonstrated that such concise scales can possess acceptable internal consistency and are highly correlated with broader measures of gender ideology (Cotter et al., 2011; Davis & Greenstein, 2009).

Furthermore, in exploratory or preliminary scale development phases — particularly when examining intersections with race, risk tolerance, or wealth accumulation — concise item sets that reflect core ideological beliefs offer conceptual parsimony without sacrificing analytical utility.

Finally, in this study, the use of these two specific items is intentionally aligned with an intersectional framework. The goal is not to make sweeping generalizations about gender role attitudes, but to explore how adherence to traditional beliefs, as reflected in these two statements, may intersect with race, gender, and risk preferences in ways that influence long-term wealth accumulation. Their inclusion supports a focused, historically grounded examination of ideational structures that shape financial behaviours, particularly among populations for whom cultural and structural constraints have coalesced to limit wealth-building opportunities.

Several analytic techniques were used to evaluate the research hypotheses. Descriptive statistics — in the form of means, standard deviations, and correlation coefficients — were calculated to provide insights about the sample and bivariate relationships between and among the variables of interest in this study. This was followed by a series of multivariate tests.

The following ordinary least squares (OLS) regression model was used to estimate the relationship between the Black female variable and risk tolerance, controlling for a respondent’s educational level, gender role attitude, and wealth situation:

In alignment with Perry and Morris (2005), Sobel tests (Baron & Kenny, 1986) — as described by Perry and Morris (2005) — were then used to estimate the degree to which education, gender-role attitude, and wealth mediate the relationship between the variables Black female and risk tolerance. The following set of equations were used to test these mediation effects:

In the context of this study, the following features were necessary to determine a mediation effect. First, the variable Black female needed to be significantly associated with the dependent variable. Second, the variable Black female needed to be significantly related to risk tolerance. Third, the effect of education, wealth, and gender-role attitude, when risk tolerance was included as a mediator, needed to be significantly associated with the dependent variable. Fourth, the effect of Black female, in the mediated model, needed to also be statistically significant. A robustness check was made using a path model. Direct, indirect, and total effects, as well as fit index scores, were used to determine the mediating roles of wealth, education, and gender-role attitude.

The following OLS regression was estimated to determine, in an exploratory manner, the degree to which wealth for Black women is moderated by risk tolerance:

Given the possibility that an endogeneity effect may have been present in the models (as well as in general and within the dataset) between risk tolerance and wealth, a two-stage least squares (2SLS) regression was estimated. The 2SLS regression was estimated based on Equation 5:

Driving risk tolerance was chosen as the instrumental variable in the regression because the question meets the following requirements for such a variable (see Norusis, 2007): the variable is (a) free of causal influence from any of the variables in the equation; (b) correlated with the endogenous variables; and (c) not highly correlated with the outcome variable. Driving risk tolerance was assessed in the NLSY79 with the following question: “People can behave differently in different situations. How would you rate your willingness to take risks while driving?” Each respondent’s willingness to take risks was measured on a scale of 0 to 10, where zero indicated “unwilling to take any risks” and 10 indicated “fully prepared to take risks.” The variable was statistically associated with the risk tolerance variable (r = .405) but not statistically associated with wealth (r = −.002). The purpose of the regression shown in Equation 6 was to obtain an estimate of

Table 1 shows the descriptive statistics for the variables used in this study. Because risk tolerance represented a factor score, the mean was 0. Using the standardized scale, scores ranged from −1.57 to 2.50, with a standard deviation of 1.00, indicating moderate variability in risk attitudes among respondents. Gender-role attitude was also measured as a factor score, and as such, its mean score was 0. The factor scores ranged from −1.26 to 3.41, demonstrating diverse viewpoints across the sample. The analysis of educational attainment revealed that 2008 respondents had an average of 13.30 years of formal education, with a median of 12 years. The standard deviation of 2.56 suggests notable variability, with a range spanning 2 to 20 years, indicating a broad spectrum of educational backgrounds. By 2010, the average educational attainment increased slightly to 13.34 years, while the median remained at 12 years. The standard deviation increased marginally to 2.59 — reflecting continued variability — though the range remained consistent, at 2 to 20 years.

Descriptive Statistics for Variables of Interest in the Study

| Black Female | Wealth | Risk Tolerance | Gender Role Attitude | Education 2008 | Education 2010 | |

|---|---|---|---|---|---|---|

| M | 0.30 | 4.86 | 0.00 | 0.00 | 13.30 | 13.34 |

| Mdn | 0.00 | 5.02 | 0.04 | 0.23 | 12.00 | 12.00 |

| SD | 0.46 | 0.88 | 1.00 | 1.00 | 2.56 | 2.59 |

| Min | 0.00 | 0.00 | −1.57 | −1.26 | 2.00 | 2.00 |

| Max | 1.00 | 6.56 | 2.50 | 3.41 | 20.00 | 20.00 |

Total net family wealth was calculated as the sum of household assets minus debts, with nominal values ranging from $0 to several million dollars. Given the significant skewness in wealth data, the variable was log-transformed for analysis. Table 1 presents the log-transformed wealth variable’s mean, standard deviation, and median, which were 4.8581, .8836, and 5.0201, respectively. The median value indicates that approximately half of the respondents had log-transformed wealth values above 5.02 and half had values below, highlighting the substantial disparities in wealth accumulation among Black women.

The bivariate Kendall’s Tau-b estimates (Table 2) indicate that being a Black woman was negatively correlated with wealth (−.322, p < .01) and education (Education 2008, −.122, p < 0.01; Education 2010, −.114, p < .01). A small positive correlation was noted with gender role attitude (.032, p < .05). Similarly, a positive association with risk tolerance was noted (.038, p < .01). The correlations suggest that, in general, being a Black woman is associated with lower levels of education and wealth and greater risk tolerance. In this study, Black women were more likely to align with traditional gender roles when assessed in a bivariate manner. As shown in the second panel of Table 2, Spearman’s correlation estimates were similar to those of Kendall’s Tau b.

Correlation Coefficient Estimates Across the Variables of Interest in the Study

| Black Female | Wealth | Risk Tolerance | Gender Role Attitude | Education 2008 | Education 2010 | |

|---|---|---|---|---|---|---|

| Kendall’s Tau-b Correlations | ||||||

| Black Female | 1.000 | |||||

| Wealth | −.322** | 1.000 | ||||

| Risk Tolerance | .038** | .075** | 1.000 | |||

| Gender Role Attitude | .032* | −.087** | −.029* | 1.000 | ||

| Education 2008 | −.122** | .304** | .092** | −.146** | 1.000 | |

| Education 2010 | −.114** | .300** | .092** | −.142** | .864** | 1.000 |

| Spearman’s Correlations | ||||||

| Black Female | 1.000 | |||||

| Wealth | −.395** | 1.000 | ||||

| Risk Tolerance | .046** | .106** | 1.000 | |||

| Gender Role Attitude | .036* | −.119** | −.039* | 1.000 | ||

| Education 2008 | −.137** | .413** | .125** | −.186** | 1.000 | |

| Education 2010 | −.129** | .409** | .124** | −.179** | .917** | 1.000 |

Note:

p < .05,

p < .01

Table 3 shows the first multivariate test designed to determine the relationship between being a Black woman and risk tolerance. It was determined that the Black female variable was positively associated with risk tolerance. The positive coefficient suggests that, on average, Black women exhibit higher levels of financial risk tolerance compared to other women. The model was statistically significant — F(4, 1857) = 12.749, p < .01 — with approximately 3% of risk-tolerance scores explained by the model (R2 = .027).

Estimates of the Relationship between being a Black Female and Risk Tolerance

| Unstandardized Coefficients | Standardized Coefficients | t | Sig. | ||

|---|---|---|---|---|---|

| B | Std. Error | Beta | |||

| (Constant) | −.991 | .162 | −6.118 | .000 | |

| Black Female | .175 | .049 | .089 | 3.596 | .000 |

| Wealth | .104 | .029 | .096 | 3.588 | .000 |

| Education | .031 | .010 | .081 | 3.235 | .001 |

| Gender Role Attitude | −.053 | .022 | −.056 | −2.415 | .016 |

Note: Dependent Variable: Risk Tolerance.

Other significant relationships were observed. Wealth and risk tolerance were positively associated, as was the relationship with education. The association between gender-role attitude and risk tolerance was negative, indicating that those who held an affinity for traditional gender roles exhibited lower levels of risk tolerance.

Sobel mediation tests were used to further examine the relationship between being a Black female and risk tolerance. The mediating roles of wealth, education, and gender role attitude were examined. The analysis revealed that being a Black female is positively associated with risk tolerance. However, this effect was only partially mediated by wealth. The negative coefficient for “Black Female → Wealth” suggests that Black women tend to hold less wealth. The positive coefficient for “Wealth → Risk Tolerance” indicates that higher wealth is positively associated with risk tolerance. The mediated effect of being a Black female through wealth was statistically significant, suggesting that wealth was positively associated with the degree of risk tolerance exhibited by Black women. Risk tolerance was the lowest for those holding the lowest levels of wealth.

Similarly, while the results showed a positive association between being a Black female and risk tolerance, the relationship was partially mediated by education. The negative coefficient for “Black Female → Education” indicates that Black women tend to have lower educational attainment levels. Higher educational attainment was observed to be positively associated with risk tolerance. The mediated effect of being a Black woman and having more education was thus a higher level of risk tolerance. Conversely, risk tolerance was lowest for those with less formal attained education.

The last Sobel test was not significant. This finding suggests that gender-role attitude, while important in describing risk tolerance, does not mediate a Black woman’s risk attitude.

While Sobel tests indicate potential mediation across variables, the approach fails to account for the simultaneous effects of variables on an outcome. For this, reason the associations among the variables from Table 4 were retested with a path model. Results from the path model provided support for the Sobel tests, although the model did not fit the data particularly well. The chi-square statistic was significant (X2 = 502.695, df = 3, p < .001). The RMSEA, NFI, and CFI coefficients for the model were .163, .469, and .464, respectively. The key variable of non-significance was gender-role attitude; this variable was not directly associated with risk tolerance, and as such, it provided no mediation in the model. Table 5 shows the standardized coefficients from the test.

Mediation Tests of Risk Tolerance as a Function of Being Black Female

| Model | Independent Variable | Dependent Variable | Coefficients | Sig. |

|---|---|---|---|---|

| Wealth | ||||

| 1 | Black Female | Risk Tolerance | .118 | .001 |

| 2 | Black Female | Wealth | −.697 | .001 |

| 3 | Wealth | Risk Tolerance | .086 | .001 |

| 4 | Black Female | Risk Tolerance | .185 | .001 |

| Wealth | .157 | .001 | ||

| Education | ||||

| 1 | Black Female | Risk Tolerance | .118 | .001 |

| 2 | Black Female | Education | −.662 | .001 |

| 3 | Education | Risk Tolerance | .037 | .001 |

| 4 | Black Female | Risk Tolerance | .163 | .001 |

| Education | .048 | .001 | ||

| Gender Role Attitude | ||||

| 1 | Black Female | Risk Tolerance | .118 | .001 |

| 2 | Black Female | Gender Role Attitude | .059 | .107 |

| 3 | Gender Role Attitude | Risk Tolerance | −.030 | .080 |

| 4 | Black Female | Risk Tolerance | .108 | .004 |

| Gender Role Attitude | −.039 | .032 | ||

Coefficients in the Path Model

| Estimate | Standardized Estimate | S.E. | p | |||

|---|---|---|---|---|---|---|

| Wealth | <--- | Black Female | −.716 | −.373 | .038 | .001 |

| Education | <--- | Black Female | −.773 | −.138 | .096 | .001 |

| Gender-Role Attitude | <--- | Black Female | .081 | .037 | .039 | .037 |

| Risk Tolerance | <--- | Wealth | .092 | .081 | .024 | .001 |

| Risk Tolerance | <--- | Education | .034 | .088 | .006 | .001 |

| Risk Tolerance | <--- | Gender-Role Attitude | −.012 | −.013 | .017 | .459 |

| Risk Tolerance | <--- | Black Female | .228 | .105 | .044 | .001 |

Table 6 shows the total effects of each variable in the path model based on standardized direct and indirect effects. Being a Black woman was only marginally positively associated with holding a traditional gender-role attitude. However, in support of previous findings, wealth and education were negatively associated with being a Black woman. Black women, compared to other women, exhibited a higher level of risk tolerance.

Standardized Total Effects

| Black Female | Gender-Role Attitude | Education | Wealth | |

|---|---|---|---|---|

| Gender-Role Attitude | .037 | .000 | .000 | .000 |

| Education | −.138 | .000 | .000 | .000 |

| Wealth | −.373 | .000 | .000 | .000 |

| Risk Tolerance | .062 | −.013 | .088 | .081 |

Table 7 shows the direct effects from the test. Being a Black woman was directly and positively associated with risk tolerance. This means that, in a bivariate sense, the willingness to take risks among Black women was higher than that of non-Black women. This finding confirms previous reports.

Standardized Direct Effects

| Black Female | Gender-Role Attitude | Education | Wealth | |

|---|---|---|---|---|

| Gender-Role Attitude | .037 | .000 | .000 | .000 |

| Education | −.138 | .000 | .000 | .000 |

| Wealth | −.373 | .000 | .000 | .000 |

| Risk Tolerance | .105 | −.013 | .088 | .081 |

Table 8 shows the indirect effects of each variable on risk tolerance. These indirect effects consider the pathways between variables and risk tolerance. As shown in Table 8, the indirect effect of being a Black woman on risk tolerance was negative. This means that when the indirect pathways to risk tolerance were estimated jointly, Black women exhibited lower risk tolerance than other women. The indirect effect was produced by the general tendency of Black women to report lower education and wealth levels, both of which were found to be positively associated with risk tolerance and to mediate the relationship between being a Black woman and risk tolerance.

Standardized Indirect Effects

| Black Female | Gender-Role Attitude | Education | Wealth | |

|---|---|---|---|---|

| Gender Role Attitude | .000 | .000 | .000 | .000 |

| Education | .000 | .000 | .000 | .000 |

| Wealth | .000 | .000 | .000 | .000 |

| Risk Tolerance | −.043 | .000 | .000 | .000 |

Table 9 presents the results from the regression model used to estimate the association between being a Black woman and wealth status, as moderated by risk tolerance. The model was statistically significant, F(5, 1856) = 138.725, p < .001, with approximately 27% of the wealth estimates explained by the model (R2 = .272). The relationship between wealth and being a Black woman was moderated by risk tolerance. Gender role attitude was not significant in the model when the interaction term was included. This suggests that while gender role attitude appears to be a significant variable when viewed in a bivariate sense, its importance is diminished when the interaction between being a Black woman and risk tolerance is included in the model.

Estimates of the Relationship between being a Black Female and Wealth, Moderated by Risk Tolerance

| Unstandardized Coefficients | Standardized Coefficients | t | Sig. | ||

|---|---|---|---|---|---|

| B | Std. Error | Beta | |||

| (Constant) | 3.544 | .102 | 34.732 | .000 | |

| Black Female (BF) | −.600 | .036 | −.332 | −16.545 | .000 |

| Education | .115 | .007 | .327 | 15.932 | .000 |

| Gender-Role Attitude | −.027 | .018 | −.032 | −1.569 | .117 |

| Risk Tolerance | .112 | .024 | .122 | 4.585 | .000 |

| BF x Risk Tolerance | −.106 | .037 | −.075 | −2.854 | .004 |

One obvious constraint associated with the estimates presented in Table 9 is the potential endogeneity related to the relationship between wealth status and risk tolerance. While the model was premised on the assumption that risk tolerance is a predisposing factor associated with wealth accumulation, it is also possible that greater wealth levels may explain risk tolerance. If this is true, then the moderation effect observed in Table 9 may be spurious. A two-stage least squares regression was estimated to account for potential endogeneity in the model.

Driving risk tolerance was selected as the instrumental variable. It was thought that being willing to take risks whilst driving should be associated with the risk-tolerance measure used in this study, but not significantly associated with wealth (i.e., someone’s wealth status should not cause someone to take more or fewer risks when operating a motor vehicle). The variable’s mean, median, standard deviation, minimum score, and maximum score were 3.220, 2.00, 3.320, .00, and 10.00, respectively. Table 10 shows the correlations between driving risk tolerance and the other variables in the model.

Correlation Coefficient Estimates between Driving Risk Tolerance and the Variables of Interest in the Study

| Driving Risk Tolerance | Black Female | Wealth | Risk Tolerance | Gender Role Attitude | Education | |

|---|---|---|---|---|---|---|

| Driving Risk Tolerance | 1.000 | |||||

| Black Female | −.016 | 1.000 | ||||

| Wealth | .020 | −.322** | 1.000 | |||

| Risk Tolerance | .281** | .038** | .075** | 1.000 | ||

| Gender-Role Attitude | −.018 | .032* | −.087** | −.029* | 1.000 | |

| Education | .065** | −.122** | .304** | .092** | −.146** | 1.000 |

Notes:

p < .05,

p < .01.

The two-stage regression model was statistically significant, F(5, 1846) = 72.264, p < 0.001, with 27% of the wealth estimates explained by the model (R2 = .270). The test results shown in Table 11 mirrored those of the hypothesized model, suggesting that the path from the Black woman variable to wealth status is moderated by risk tolerance.

Two-stage Least Squares Analysis Robustness Check of the Moderation Model

| Unstandardized Coefficients | Standardized Coefficients | t | Sig. | ||

|---|---|---|---|---|---|

| B | Std. Error | Beta | |||

| (Constant) | 3.547 | .102 | 34.683 | .000 | |

| Black Female (BF) | −.595 | .036 | −.330 | −16.370 | .000 |

| Education | .115 | .007 | .327 | 15.872 | .000 |

| Gender-Role Attitude | −.027 | .018 | −.032 | −1.563 | .118 |

| Driving Risk Tolerance | .111 | .024 | .121 | 4.561 | .000 |

| BF x Driving Risk Tolerance | −.109 | .037 | −.077 | −2.926 | .003 |

Note: Dependent Variable: Risk Tolerance.

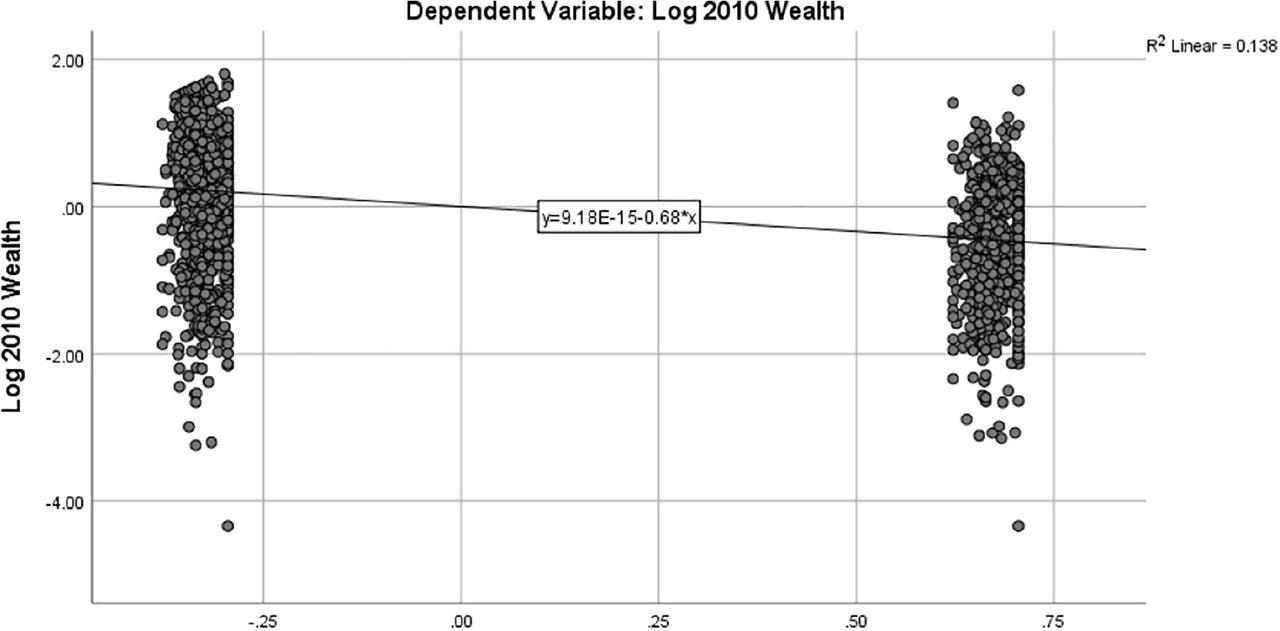

Figures 4 through 7 illustrate the general moderation effect of risk tolerance on being a Black woman and wealth status. Figure 4 shows the partial regression plot of wealth status by the Black woman variable. The fitted regression line shows the slope of the effect from non-Black women (i.e., the left side of the figure) to Black women (i.e., the right side of the figure). Black women were, on average, less likely to report high levels of wealth. Figure 5 shows the partial regression plot of the interaction term. The moderating effect of risk tolerance is evident in the reduced slope of the regression line compared to the line in Figure 4.

Partial Regression Plot Showing the Wealth Status of Black Women and non-Black Women.

Partial Regression Plot Showing the Interaction Effect of Risk Tolerance and Black Female on Wealth Status.

Interaction Effect of Risk Tolerance and Black Female on Wealth Status.

Illustration of Wealth Gap Closing as Risk Tolerance Increases.

Figure 6 illustrates the overall interaction effect of risk tolerance and being a Black woman on wealth status. As risk tolerance increases, reported wealth is shown to decrease for Black women when holding the other factors at the sample mean or median level. A separate model was estimated (not shown) that included marital status (1 = single, 0 = otherwise). The model was statistically significant, with single individuals reporting lower levels of wealth. An interaction term was created to determine whether marital status moderated the association between the Black woman variable and wealth. When this variable was included in the model, no interaction was noted. This suggests that in addition to being a Black woman, those who are single are less likely to accumulate wealth, but that the association between Black woman and marital status is not interactive.

The model was estimated again without an interaction effect. The model was statistically significant, F(4, 1857) = 90.695, p < .001, with approximately 27% of the wealth estimate explained by the model (R2 = .269). In each of the models, Black women were observed to exhibit a lower wealth status compared to non-Black women. However, the slope of the decline, as noted above, was reduced for Black women with a higher level of risk tolerance. Although risk tolerance did not reverse the wealth gap between Black women and others, it did moderate, to some extent, the degree to which the gap could be observed.

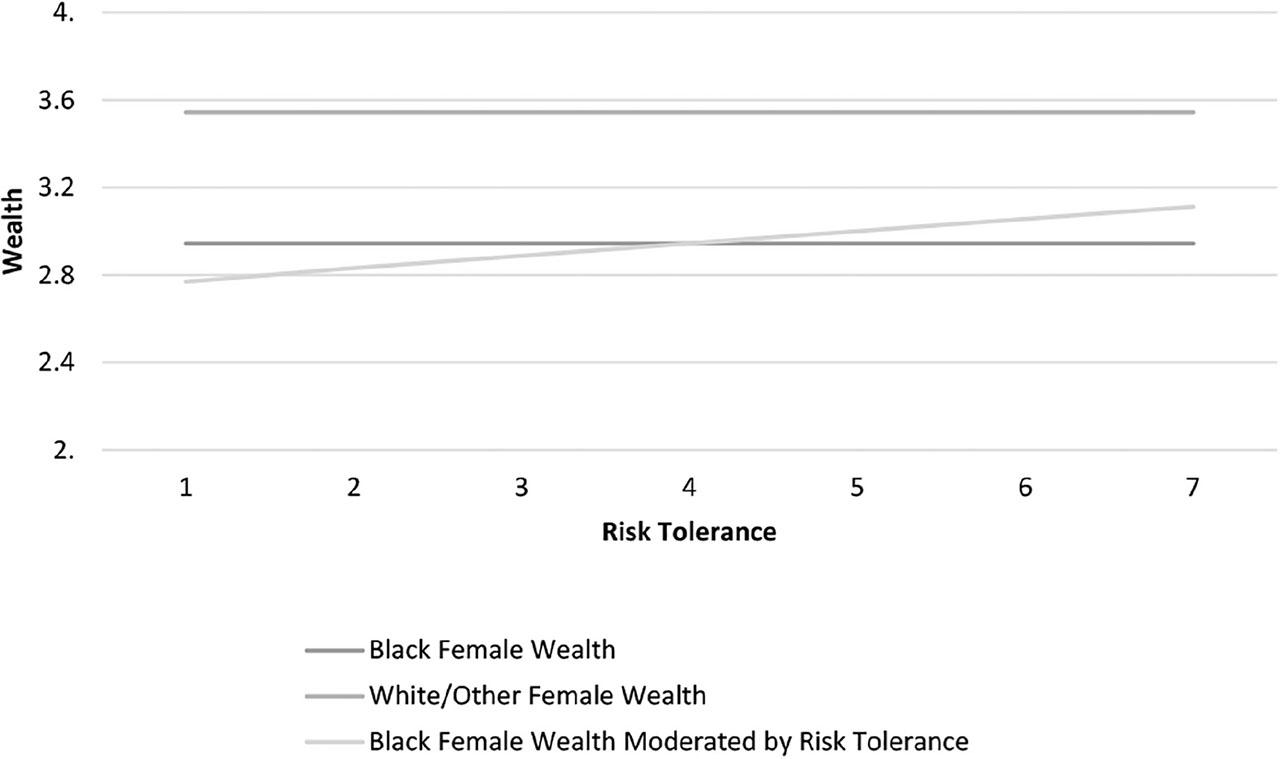

Figure 7 illustrates the moderation effect from the perspective of comparing Black women to non-Black women in terms of risk tolerance. The dark line indicates that the wealth status of Black women is lower than that of non-Black women. However, an interaction was observed when risk tolerance was taken into account (i.e., the relationship between risk tolerance and wealth is positive). This means that although Black women hold less wealth than similarly situated non-Black women, the gap between the two falls as risk tolerance increases.

The literature on race, gender, and risk tolerance underscores the complexity of wealth accumulation and financial decision-making. While research consistently finds that women, particularly Black women, exhibit lower levels of risk tolerance compared to men, the underlying causes of these disparities are multifaceted. Racial differences in wealth, human capital, and financial education interact with gender to shape financial behaviours, particularly investment decisions. The findings from Coleman (2003), Fisher (2019), Hudson et al. (2018, 2021), and others highlight the importance of considering both race and gender when examining financial risk tolerance. Understanding the intersectionality of these factors is essential for developing policies and strategies that address the financial needs of marginalized groups, particularly Black women, and promote greater financial inclusion and wealth-building opportunities. The following discussion summarizes the results of this study.

It was determined that Black women, compared to non-Black women, exhibit a greater willingness to take financial risks. This finding hints at what in this study is termed the “wealth/risk tolerance paradox.” It has been extensively documented in the literature, including in this study, that risk tolerance and wealth are positively associated. There is likely an endogeneity factor at play in the relationship. Nonetheless, those who exhibit a greater willingness to take financial risks generally report holding more wealth. This relationship, however, does not hold true for Black women when compared to non-Black women. This is a paradox that can be addressed by providing answers to the other research questions posed in this study.

Wealth was observed to have an inconsistent mediating effect between being a Black woman and risk tolerance. Those with more net wealth reported higher levels of risk tolerance. However, the opposite was also true. As wealth decreased, so did risk tolerance. Because Black women tend to hold less wealth than non-Black women, it is not surprising that wealth was observed to have an inconsistent effect in this study.

Similarly, in the mediated models examined in this study, it was determined that education had an inconsistent mediation effect on the relationship between being a Black woman and risk tolerance. The attained educational level of Black women tends to be lower than that of other women. In confirmation with the extant literature, this was observed in this study. Those with higher levels of attained education reported more risk tolerance, and individuals with lower levels of educational attainment reported a lower willingness to take financial risks. This helps explain the wealth/risk tolerance paradox. It is also worth noting that gende-role attitude was not a significant mediator in the models examined in this study. While Black women were more likely to hold traditional gender-role attitudes, this had no effect on describing higher or lower levels of risk tolerance.

It was determined that risk tolerance does moderate the association between being a Black woman and wealth. Even though Black women hold less wealth than similar non-Black women, the gap between these two groups falls as risk tolerance increases. In this respect, risk tolerance is a key factor in describing the wealth/risk tolerance paradox noted in this study. More specifically, Black women’s wealth accumulation status appears to be negatively affected by their generally lower level of education; this can be partially offset, however, by their greater willingness to engage in financial behaviours in which the outcome is both uncertain and potentially negative.

This study examined various hypotheses related to risk tolerance, wealth, education, gender role attitudes, and the experience of being a Black woman. The results confirmed a positive association between risk tolerance and being a Black woman (H1), wealth (H2), and attained education (H3). However, a negative association was observed between risk tolerance and gender role attitudes (H4). Wealth and education were found to inconsistently mediate the relationship between risk tolerance and being a Black woman (H5 and H6), while gender role attitude did not mediate this association (H7). The study also confirmed a positive association between education and wealth (H8); however, gender-role attitude was not associated with wealth (H9). Additionally, being a Black woman was negatively associated with wealth (H10). Risk tolerance was confirmed to have a positive association with wealth (H11). Additionally, risk tolerance moderated the relationship between being a Black woman and wealth, with greater levels of risk tolerance being associated with less wealth for Black women (H12).

With regard to attained education and risk tolerance, Human Capital Theory (HCT) provides an explanation for persistent wealth disparities. HCT explains how those with more education (e.g., a college degree) earn more than those with less education (e.g., a high school diploma). Income levels, as mediated by this factor, are a key driver of wealth accumulation. Income and wealth provide a degree of financial capacity that allows individuals to take more risks, which, in turn, helps them build additional wealth. Like other skills, risk tolerance is an important addition to one’s human capital. Providing Black women with information, skill-building development, and practice related to increasing risk tolerance may be the key to helping Black women bridge the wealth gap.

While noteworthy, findings associated with individual hypothesis tests do not provide enough context when attempting to decompose the association between being a Black woman and wealth status. Viewing the results across hypotheses from a holistic perspective is essential to gain a clear perspective on the association between being a Black woman and wealth status. In this regard, several insights stand out in this study:

Wealth, education, and gender-role attitude, as predisposing factors, are associated with risk tolerance;

Black women, contrary to what has been reported in much of the literature, exhibit a higher degree of risk tolerance compared to non-Black women;

Wealth and education act in a way that mediates the risk tolerance of Black women;

Black women control less wealth than comparable non-Black women, regardless of marital status); and

Risk tolerance acts as a moderator between being a Black woman and wealth status while also being directly associated with one’s wealth status.

When viewed holistically, these insights suggest that the relationship between being a Black woman and wealth status is nuanced, and that simple bivariate or linear assumptions about the relationship are likely impractical and not particularly useful. The initial tests conducted in this study showed a direct and positive association between wealth and risk tolerance, as well as education and risk tolerance, among Black women. However, the moderation test results revealed an alternative pathway in explaining the relationship between being a Black woman and wealth status. Risk tolerance was observed to be directly and positively associated with wealth status — that is, the greater someone’s willingness to take risks, the more wealth they reported at the household level.

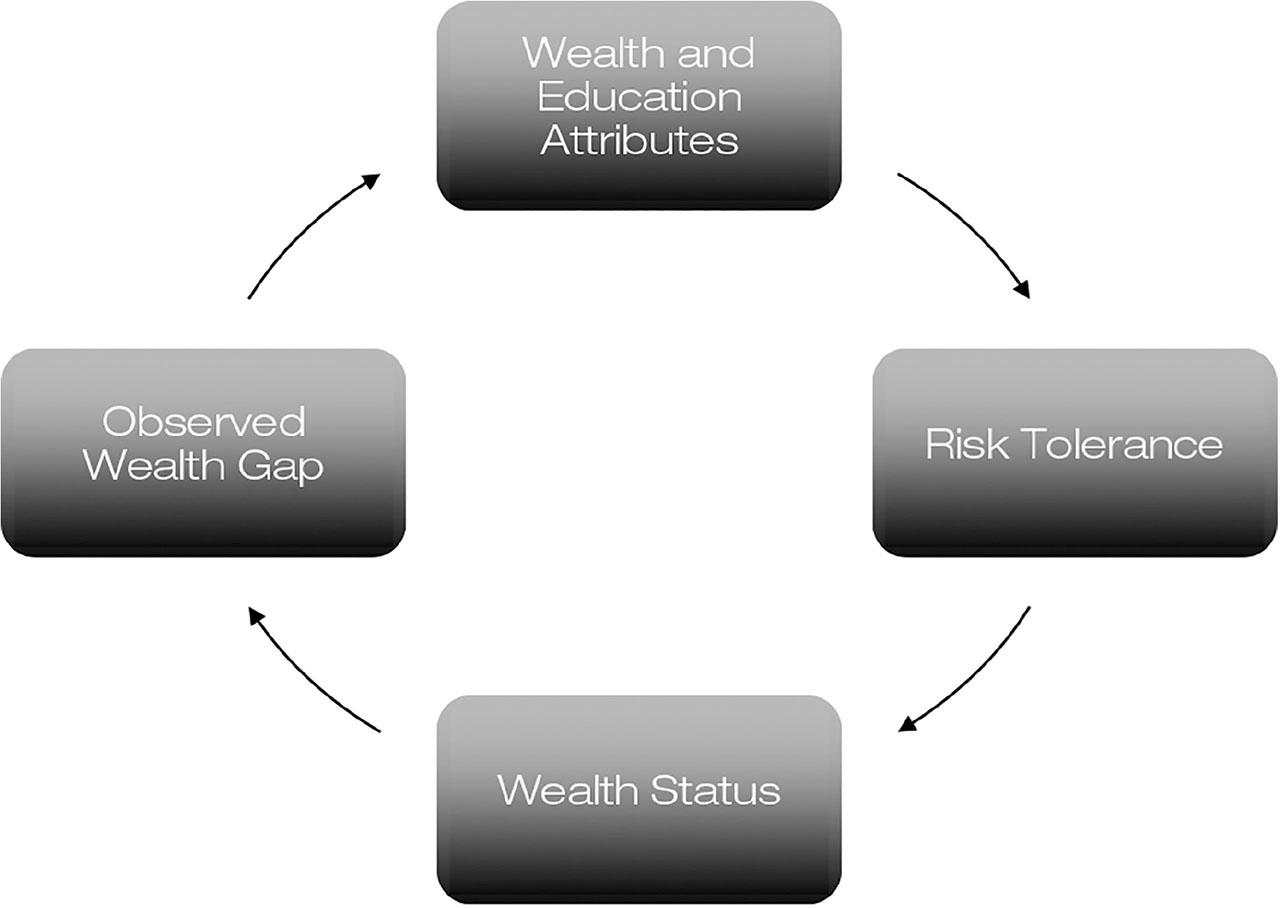

Figure 8 illustrates the apparent trends for Black women in terms of wealth status. To begin with, Black women, though they report relatively high levels of risk tolerance, tend to, on average, report lower levels of predisposing environmental attributes, such as wealth and education. In this way, Black women tend to start at a relatively weak position in terms of accumulating wealth (i.e., their capacity to take risks is lower than that of non-Black women). This results in a cycle where low levels of wealth and education dampen the effect of risk tolerance, resulting in a continued gap in wealth compared to non-Black women.

Suppose the circular relationship shown in Figure 8 is true. In that case, the interventions and policies needed to narrow the wealth gap must focus on breaking deficits in wealth and education exhibited by Black women. This implies that adjustments to one environmental factor (e.g., wealth) without corresponding adjustments to other environmental factors (e.g., education) may not be sufficient to address the ongoing wealth-gap issue.

Circular Relationship Between and Among Wealth and Education Attributes, Risk Tolerance, and the Observed Wealth Gap between Black Women and Non-Black Women.

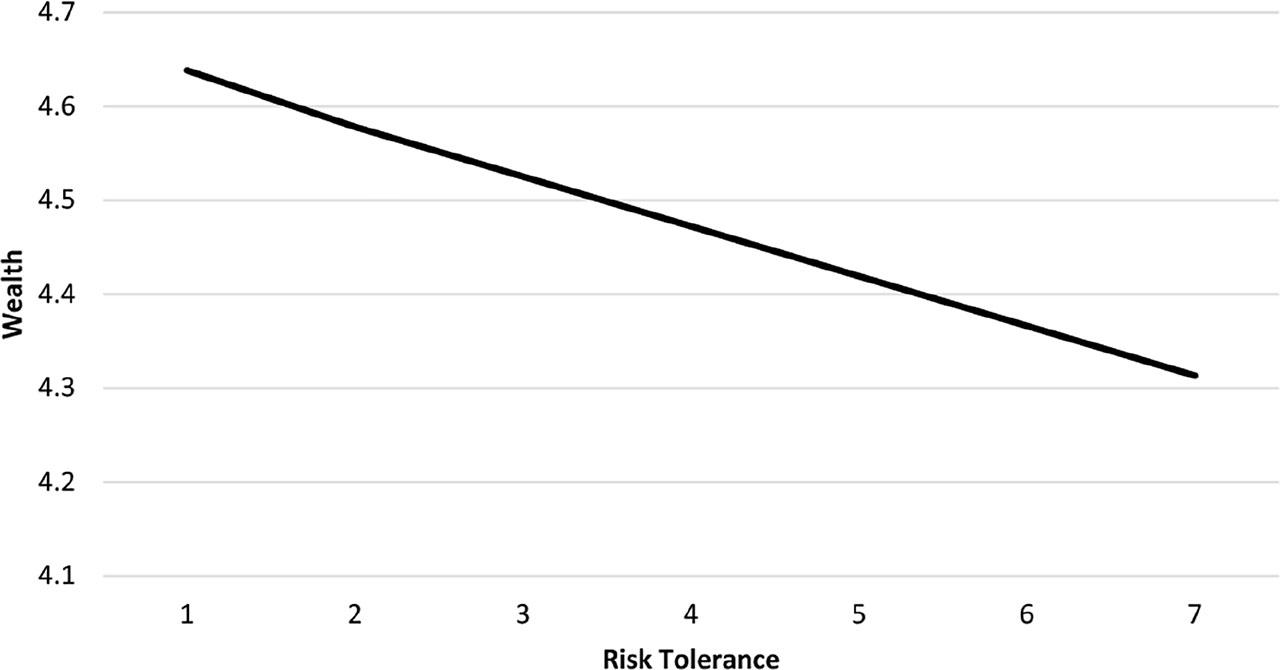

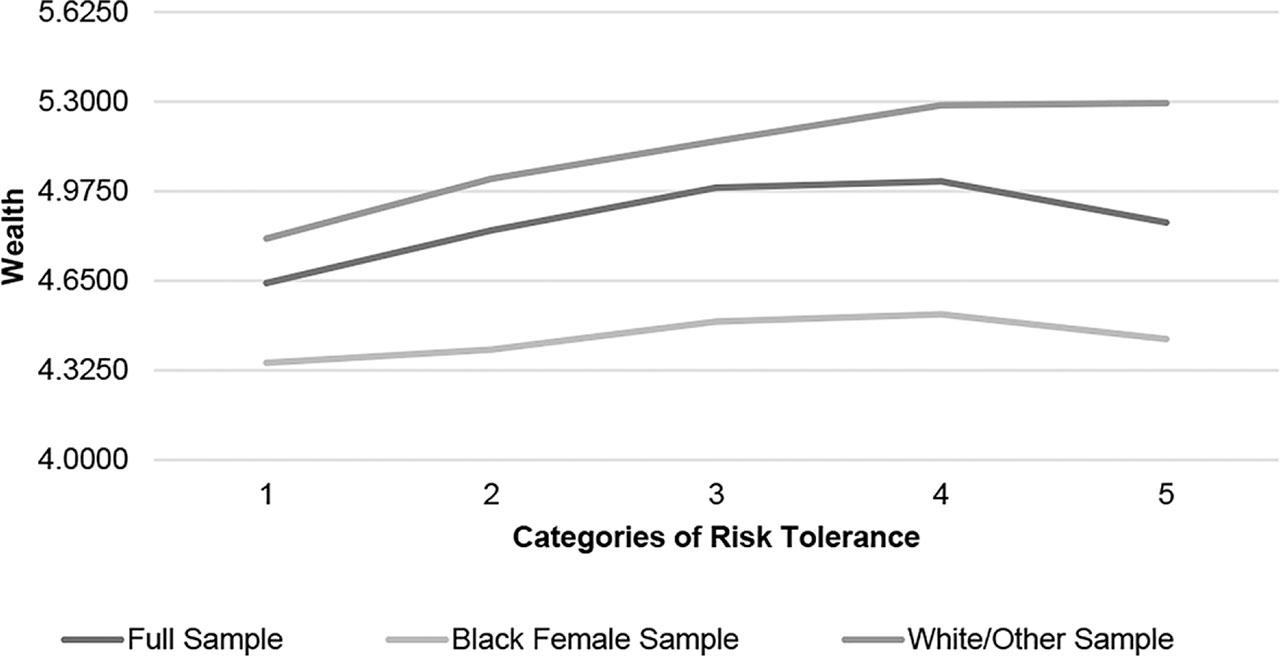

Figure 9 illustrates the role of risk tolerance in helping to explain the ongoing wealth gap between Black women and non-Black women. The horizontal categories represent risk tolerance when recoded into five equal and distinct categories from a continuous variable. The vertical axis represents wealth. Across all categories of risk tolerance, wealth is shown to increase for non-Black women (the grey line in the figure); further, the increase in wealth across categories (i.e., the slope of the line) is rather steep, suggesting that the relationship between risk tolerance and wealth status is more pronounced for non-Black women. The situation for Black women is different. Wealth is depicted in the figure as increasing to the point of “above-average” risk tolerance, and then declining at the highest level of risk tolerance. This curvilinear effect differs from the observed association between wealth status and risk tolerance seen for non-Black women.

The Association Between Categories of Risk Tolerance and Wealth Status.

The patterns of wealth status shown in Figure 9 suggest that risk literacy may play a significant role in explaining the wealth gap between Black women and non-Black women. Risk literacy refers to being more knowledgeable about the relationship between risk and return; this type of awareness can influence the financial decisions one may make (Lusardi, 2014). Those who are more knowledgeable about risks and uncertainty are more apt to save, plan for retirement, and invest in the stock market, and are less likely to take on high-interest debt (Lusardi, 2014). These factors may explain why low levels of risk literacy among Black women contribute to the observable wealth gap.

Financial planners, financial counsellors, and financial educators who work with Black woman clients can play a pivotal role in empowering them by focusing on education and risk literacy. Recognizing the historical disparities and systemic challenges that Black women face, they can tailor their approaches to address these unique circumstances. Education becomes a key tool in this process, with financial-services professionals needing to take the time to thoroughly explain financial concepts, investment strategies, and long-term planning options. By fostering a learning environment, financial-service professionals and financial educators can empower Black woman clients to make informed decisions, demystifying the complexities of the financial landscape.

Moreover, a nuanced emphasis on risk literacy is crucial. Black women, like any other demographic group, have a diverse range of risk tolerance levels and financial goals. Financial service professionals and financial educators should be willing to engage in open and honest conversations about the way risk, both real and imaginary, is perceived, tailoring their advice to align with the specific needs and aspirations of their Black woman clients. This approach goes beyond conventional financial planning, counselling, and education by recognizing the importance of addressing unique life experiences and potential obstacles. Through education and a focus on risk literacy, financial service professionals and financial educators can significantly contribute to the financial well-being and empowerment of Black woman clients, enabling them to navigate the complexities of the financial world with confidence and resilience.

To comprehensively understand the relationship between being a Black woman and risk tolerance, researchers should delve into the intricate interplay of various socio-economic factors, including wealth, education, and gender role attitudes. Wealth plays a pivotal role in describing an individual’s risk tolerance, as financial stability often influences one’s ability to absorb potential losses. Black women, who may face systemic barriers to wealth accumulation, may exhibit unique risk tolerance patterns influenced by economic disparities and distinct perspectives on what it means to be a saver and an investor. Moreover, education serves as a crucial determinant, empowering individuals with the knowledge and skills needed to navigate financial complexities. A nuanced exploration of how educational attainment intersects with being a Black woman can unveil insights into this group’s risk-taking behaviour, shedding light on whether education mitigates or exacerbates risk aversion within this demographic. In terms of specific steps researchers can take to inform educational interventions, it will be important for future studies to incorporate mediation and moderation effects in models. It would also be helpful, as illustrated in Figure 9, to account for possible curvilinear effects between risk tolerance and wealth, as well as risk tolerance and other factors.

Gender role attitudes further complicate the relationship between being a Black woman and risk tolerance. Societal expectations and cultural norms often prescribe specific gender roles that may intersect with racial identities, influencing individuals’ perceptions of risk and financial decision-making. By scrutinizing how gender role attitudes are internalized and expressed by Black women, researchers can elucidate whether traditional gender norms amplify or mitigate risk aversion. This multifaceted analysis, which considers the mediating roles of wealth, education, and gender role attitudes, is crucial for developing targeted interventions and policies that foster financial inclusion and empowerment among Black women.

To better understand the relationship between being a Black woman and risk tolerance, policymakers and researchers must examine the complex interplay of socio-economic factors, such as wealth, education, gender role attitudes, and risk-taking attitudes. Effective policy development to expand access to investing opportunities for traditionally underrepresented groups requires a nuanced approach that moves beyond surface-level solutions. Wealth, as demonstrated in the literature, is positively associated with risk tolerance, as financial stability allows individuals to absorb potential losses. Simultaneously, risk tolerance itself can contribute to wealth accumulation, creating a feedback loop. However, systemic barriers to wealth accumulation that Black women are uniquely likely to face may limit their responsiveness to traditional incentives for savings and investments. Divergent perceptions of risk and preferences for financial products, shaped by these economic disparities, must be taken into account when designing policies aimed at fostering financial inclusivity.

Policymakers should recognize that financial knowledge alone is insufficient to resolve the wealth/risk tolerance paradox experienced by Black women. As illustrated in this study, Black women already exhibit higher risk tolerance compared to non-Black women. What is critically needed is enhanced access to education and support systems that help Black women conceptualize wealth as a tool to strengthen the financial capacity of their households. Education is a key determinant that empowers individuals with the knowledge and skills to navigate financial systems and make informed, strategic decisions. A deeper exploration of how educational attainment intersects with being a Black woman can provide valuable insights into whether education mitigates or exacerbates risk aversion.

To address the challenges faced by Black women, policymakers have an opportunity to incentivize the accumulation of human capital through targeted initiatives, such as tax credits, tax subsidies, refundable tax credits, or direct tuition support for Black women who demonstrate educational need. The long-term societal and household benefits of such policies are significant. A higher level of educational attainment enhances human capital, fostering a greater willingness to take financial risks. This willingness drives wealth accumulation, further strengthening risk capacity and accelerating wealth growth. Over time, this accumulated wealth reduces reliance on government funding for health and retirement needs, creating positive economic outcomes for households and society as a whole.

In addition, gender role attitudes must be carefully considered, as they further complicate the relationship between being a Black woman and risk tolerance. Societal and cultural norms often impose traditional gender roles that intersect with racial identity, influencing financial decision-making and perceptions of risk. Understanding how Black women internalize and express these attitudes is critical for determining whether traditional gender norms amplify or mitigate risk aversion. By accounting for the mediating roles of wealth, education, and attitudes toward gender roles, policymakers can develop targeted, evidence-based interventions that foster financial empowerment and inclusivity for Black women. This multifaceted approach is essential for dismantling systemic barriers, promoting equitable access to financial opportunities, and supporting long-term economic stability.

While the findings of this study offer valuable insights, several limitations must be acknowledged to provide context and guide future research. First, this study relied on secondary data, which, while robust, has inherent constraints. Using primary data to examine the wealth-building experiences of Black women could offer a significant advantage. The collection of primary data in follow-up studies will enable the development of tailored questions that directly address the unique cultural, social, and economic factors influencing Black women’s financial trajectories — elements often underrepresented in secondary datasets like the NLSY79.

Second, the data were restricted to female respondents. While purposeful for addressing gendered wealth dynamics, this delimitation limits the generalizability of the findings to Black women. Third, the temporal scope of the financial risk tolerance measures poses an important constraint. These measures were only collected in six discrete waves between 1993 and 2010, with no subsequent updates or replications in newer waves of the NLSY79. As a result, our analysis is bound by a fixed historical period that may not fully reflect evolving attitudes shaped by recent economic or social events, such as the COVID-19 pandemic, rising student debt burdens, or post-2010 financial market shifts. While we believe that risk tolerance is a stable psychological trait in adulthood, and therefore not subject to significant temporal distortion, this assumption may not hold uniformly across all subgroups, particularly among populations exposed to chronic economic insecurity.

Additionally, reliance on retrospective data raises concerns about potential cohort effects. Respondents in the NLSY79 are part of a specific generational cohort, and their financial behaviours may be shaped by unique policy environments, labour markets, and social norms that differ markedly from those facing younger generations today. Although a historical lens is essential for interrogating the structural roots of the wealth gap experienced by Black women, especially in terms of accumulated disadvantage, caution must be exercised when extrapolating these patterns to current or future economic contexts. Another limitation deals with causality. While robustness checks using 2010 sampling weights confirm the stability of our core findings, the cross-sectional nature of the risk tolerance measures precludes definitive causal claims. Our findings should thus be interpreted as associations rather than as evidence of direct causal mechanisms.

Despite these limitations, the study provides valuable insights into the long-term relationship between psychological traits and wealth accumulation in the context of systemic inequality. The value of the NLSY79 dataset — particularly its inclusion of validated measures of financial risk tolerance — continues to provide a powerful platform for analysing enduring economic disparities and behavioural patterns. Nonetheless, future research would benefit from incorporating updated datasets or designing studies that longitudinally track changes in Black women’s financial behaviours, attitudes, and financial outcomes. Furthermore, expanding upon the biopsychosocial model of risk-taking behaviour by integrating additional endogenous, exogenous, and predisposing factors would enable a more comprehensive understanding of the variables influencing risk tolerance among Black women. This study deliberately employed a restrained model to establish foundational knowledge on this under-researched topic, but future work should expand the range of variables examined to uncover deeper insights.

Finally, while this study includes married Black women, a potential confounding effect arises from the shared nature of marital wealth. Financial outcomes within marital partnerships often reflect joint effort, making it challenging to attribute wealth accumulation solely to the individual contributions of Black women. To address this, future studies should consider focusing specifically on single Black women, as this approach would provide a more transparent lens into their economic agency and independent financial strategies. By isolating the financial decisions, investments, and entrepreneurial efforts of single Black women, researchers can better understand the challenges and opportunities they encounter in wealth-building processes. This narrower focus would mitigate the confounding influence of spousal wealth and highlight the resilience, resourcefulness, and unique financial pathways of single Black women. However, it is important to recognize that concentrating exclusively on single Black women may also introduce limitations. The Black female demographic is highly diverse, encompassing variations in educational attainment, employment opportunities, geographic location, and other socio-economic factors that impact wealth accumulation and risk tolerance. While narrowing the scope to single Black women may allow for greater specificity, doing so risks oversimplifying the broader dynamics faced by the larger population of Black women. A balanced approach — one that examines both individual financial agency and collective economic dynamics — is essential to ensure that findings represent this group’s full range of experiences. Future studies should employ data collection and methodological strategies that account for both individual and systemic factors influencing Black women’s financial outcomes. This may ultimately provide a more comprehensive and actionable understanding of wealth-building opportunities and challenges facing Black women.

As noted at the outset of this paper, the disparity in wealth accumulation between Black women and non-Black women living in the United States is a topic worthy of discussion and study. This study was conceptualized to examine the intersectionality of being Black and female in relation to risk tolerance and wealth accumulation. Specifically, the influence of education, perceived gender roles, and the willingness of Black women to tolerate risk when making household financial decisions were investigated to determine the associations across these variables with the wealth accumulation of Black women. It was determined that, contrary to popular belief, Black women are more willing to take financial risks than non-Black women. This willingness, however, has yet to result in greater wealth accumulation. To some extent, this wealth/risk tolerance paradox can be addressed by understanding how education and wealth mediate the relationship between being a Black woman and risk tolerance. The paradox can also be explained by understanding how the wealth accumulation of Black women is moderated by risk tolerance.