The company is involved in contractual agreements with various parties, including stakeholders and company management. It is expected that company management will adhere to the terms of these contracts, which primarily involve enhancing investor prosperity and safeguarding the interests of creditors and other stakeholders. However, due to the separation between stakeholders and management, the latter enjoys greater autonomy in managing company operations and can adopt financial strategies that promote stakeholder wealth (Flayyih and Khiari, 2023). Unfortunately, this freedom is sometimes exploited by management. The chosen policies no longer prioritize the enhancement of stakeholder wealth but rather serve to advance personal gain. This issue is commonly referred to as the agency problem. In such cases, management no longer operates the company for the benefit of other parties, but rather for their own personal interests. Prominent examples of these agency problems include Enron and Toshiba.

Enron, recognized as the largest energy trading firm globally, was at the center of a significant scandal in the United States during the 2000s, resulting in abrupt financial losses that adversely affected various stakeholders, including investors, creditors, and the general public. A primary factor contributing to these losses was the implementation of deceptive accounting practices aimed at embellishing the company's financial reports. Similarly, Toshiba, a prominent Japanese multinational corporation, engaged in the manipulation of financial statements by artificially inflating profits starting in 2015. This situation exemplifies the repercussions of agency problems, wherein management prioritizes its own interests over those of other stakeholders.

Earnings management arises as a consequence of the agency problem. The act of manipulating financial statements is often perceived as having a favorable effect on the financial performance of a company. However, in reality, it has a detrimental impact on the users of these statements. Both Enron and Toshiba engaged in such manipulative practices with the intention of enhancing their financial performance. Nevertheless, these actions ultimately compromised the transparency of their financial statements. Consequently, numerous investors incurred significant losses as a result of these deceptive practices. Indonesia is not exempt from such manipulations, as there are several companies that resort to manipulating their financial statements in an attempt to improve their overall performance. Unfortunately, the outcomes of these manipulations often fall short of expectations, as exemplified by the case of Tiga Pilar. In this instance, the company's Board of Directors manipulated the reported financial statements, further exacerbating the issue.

To mitigate the occurrence of the agency problem, it is imperative to undertake preventive measures, and the implementation of corporate governance serves as a crucial solution. By incorporating supervisory bodies appointed by stakeholders within the company, it is anticipated that the agency problems can be effectively curbed. In Indonesia, a two-tier system is adopted for corporate organization, signifying the presence of both supervisory and executive bodies. This stands in contrast to certain countries that adhere to a one-tier system. The supervisory body in the company is referred to as the board of commissioners, while the executive body is known as the board of directors.

The agency problem can be mitigated through the effective implementation of good governance, as evidenced by (Chatterjee and Rakshit, 2023; Flayyih and Khiari, 2023; Nguyen, et al., 2024). This implementation not only ensures proper supervision but also minimizes the adverse impact on stakeholders. Nevertheless, certain countries have experienced varying outcomes, where governance measures have proven insufficient in addressing agency problems. This inadequacy is often attributed to a lack of supervision, leading to an escalation in earnings management practices. This research was conducted once again to examine the significance of governance in mitigating agency problems, as mentioned in the previous introduction. Numerous research findings have shed light on the relationship between governance and agency problems, with some asserting that governance plays a crucial role in preventing such problems within companies (Chatterjee and Rakshit, 2023; Flayyih and Khiari, 2023; Nguyen, et al., 2024). However, there are also opposing views that suggest governance has not been effective in addressing this issue (Assenso-Okofo, et al., 2021; Lukmanul, 2022; Wasan and Mul-chandani, 2020).

These disparities have piqued the interest of researchers, leading them to embark on further investigations on the same subject. The present study focuses on companies in Indonesia that have adopted a two-tier governance structure, which differs from the one-tier structure implemented in other countries. It is anticipated that the implementation of a two-tier governance system will enhance the oversight of governance and ultimately alleviate the agency problem. This research paper is structured to include an introduction to the research, a review of relevant literature, a detailed methodology, an analysis of the results, and a discussion of the findings, culminating in a conclusion that summarizes the conducted research.

Jensen is credited with the development of agency theory, which highlights the issues that arise between company management (agents) and company owners or principals. According to this theory, principals delegate authority to agents to run their companies, but there is a risk of agents misusing this authority for personal gain instead of generating additional wealth for the principals (Smulowitz, et al., 2019). This behavior leads to losses for investors and is referred to as the agency problem. It is important to note that agency problems, as discussed in this theory, extend beyond the conflicts between principals and agents. There are various types of agency problems that can arise in this context (Ghozali, 2020; Utama, et al., 2022; Flayyih and Khiari, 2023):

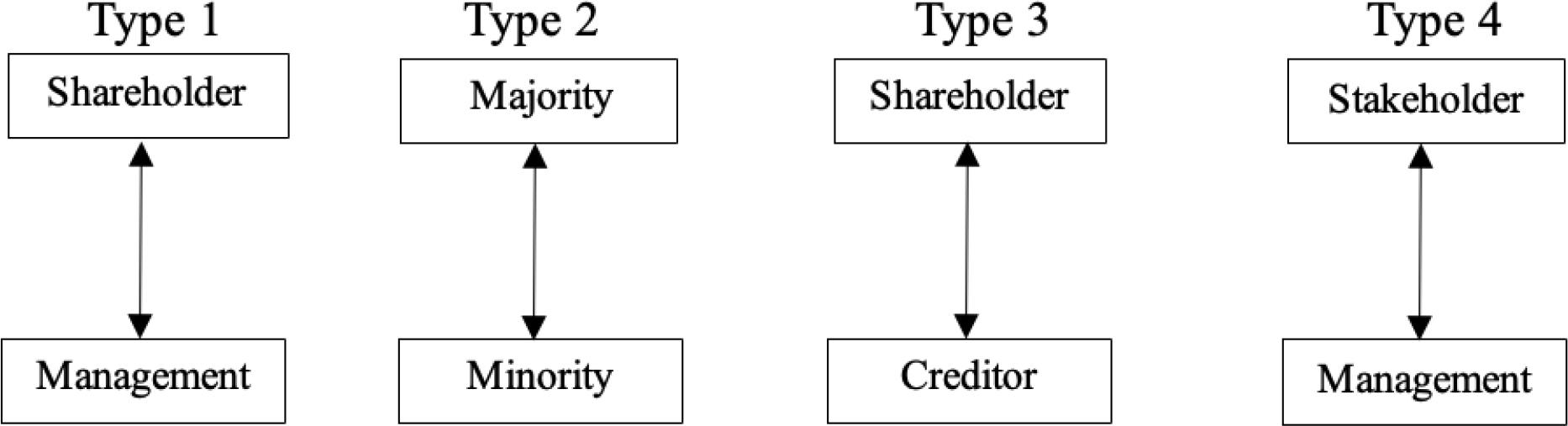

Agency problem type 1 arises from conflicting interests between owners or principals and company management or agents. The management may not always act in alignment with the desires of the owner, instead prioritizing its own self-interest by selecting accounting policies and methods that serve its own benefit. Consequently, the agent, who is not directly involved, may incur losses as a result of this behavior. The divergent goals of each party contribute to the emergence of agency problems.

Agency problem type 2 emerges when a disparity exists between majority interest holders and minority interest holders in a company. This discrepancy is evident in the unequal distribution of information, with majority interest holders typically having access to more information than their minority counterparts. Consequently, minority interest holders may suffer losses due to their lack of access to the same information as majority interest holders, leading to divergent decision-making processes that may disadvantage the minority interests.

Agency problem type 3 arises when there is a divergence of interests between investors and creditors. Both investors and creditors play significant roles in the company but have distinct objectives. Investors seek funding through shares, whereas management occasionally favors funding through loans. Opting for loans as a source of funding diminishes the benefits received by investors since the company must prioritize repayment to creditors. Consequently, this situation gives rise to agency problems.

Agency type 4 issues emerge when there are clashes between stakeholders apart from shareholders and management. These stakeholders encompass local communities, customers, employees, suppliers, and governments. Occasionally, management, while acting in the best interest of shareholders, fails to consider the concerns of other stakeholders. Stakeholders are not limited to shareholders alone but also include other entities that provide capital to agents for management purposes. For instance, employees may desire a salary raise, but management may not promptly fulfill their wishes as it would result in a reduction of profits distributed to shareholders in the form of dividends.

Various factors can contribute to agency problems, such as: individuals' inclination to prioritize their personal interests. The constraints faced by individuals in fully assessing the long-term consequences can also lead to agency problems. Discrepancies in the information exchanged between agents and principals may exacerbate agency problems. Inadequate supervision can be a significant factor in the occurrence of agency problems. In addition, individual aversion to risk-taking can further exacerbate agency problems (Ghozali, 2020; Hakim, et. al., 2022; Utama, et al., 2022).

The resemblances found in every form of agency issue lie in the conflicting interests of the involved parties within the organization and the disparities in information accessibility, also known as information asymmetry. This information asymmetry can be advantageous for parties with more information, while those lacking information may suffer losses. This research specifically delves into type 1 agency problems. Due to the lack of a precise measurement for this type of agency problem, earnings management emerges as the most suitable metric for evaluating agency problems (Flayyih and Khiari, 2023).

One approach for principals to mitigate opportunistic agency is by establishing a governance framework capable of monitoring and evaluating the actual managerial conduct, as well as implementing a structured governance system that evaluates performance according to agent behavior outcomes (Eisenhardt, 1989; Davis, et al., 2018; Ghozali, 2020). Therefore, agency issues can be addressed through the adoption of effective corporate governance practices. Governance encompasses a variety of mechanisms, processes, and relationships within the organization that facilitate the allocation of rights and responsibilities among stakeholders, ultimately overseeing decision-making processes. It is a framework of systems involving stakeholders in the organization with the primary goal of guiding and supervising the organization to ensure attainment of its objectives (Ghozali, 2020; Utama, et al., 2022).

The prevention of differences in interests can be achieved through the implementation of governance. Governance plays a crucial role in aligning the interests of principals and agents by establishing appropriate structures, systems, and processes. In cases where governance is not effectively implemented, conflicts in interests may arise, as seen in examples like Enron and World Com, where the alignment between principals and agents was lacking. The repercussions of such differences in interests can have far-reaching negative effects on various stakeholders (Ghozali, 2020; Utama, et al., 2022). Hence, it is imperative for companies to prioritize the implementation of governance to mitigate these risks.

Type of Agency Problem

(Source: Flayyih and Khiari, 2023, p.201)

There are two distinct board structures in governance, namely the one-tier system and the two-tier system. The one-tier system is predominantly utilized in Anglo-Saxon countries like the USA, England, Canada, and Australia. Under this system, both supervisors and company executives are overseen by a single entity known as the Board of Directors. However, despite being managed by a single agency, the execution and oversight are carried out by two separate parties. The executive director assumes the role of the implementer, while the non-executive director acts as the supervisor. It is important to note that one individual cannot hold both positions simultaneously (Ghozali, 2020; Utama, et al., 2022).

The two-tier system is implemented in European nations like the Netherlands and Germany. This system divides the board into two distinct entities: the supervisory board and the executive board. The supervisory board oversees the activities of the executive board, which is responsible for carrying out the company's operations. The clear separation of roles is a key feature of the two-tier system, ensuring that individuals do not hold dual positions within the organization. Every system comes with its own set of benefits (Utama, et al., 2022). In a one-tier system, decisionmaking is facilitated as implementers and supervisors are overseen by the board of directors. However, a two-tier system offers advantages in terms of organizational structure, as supervisors and implementers are distinct entities, leading to more effective supervision (Utama, et al., 2022).

Indonesia has been actively implementing governance measures since 2014, and this effort has continued to develop over time. The implementation of governance in the country is guided by the National Committee for Governance Policy (KNKG), which issues comprehensive guidelines. The most recent guidelines, known as the General Guidelines for Indonesian Corporate Governance (PUGKI), were released by KNKG in 2021 and are aligned with global standards (Utama, et al., 2022).

There are four key pillars that form the foundation of governance implementation in Indonesia. Firstly, ethical behavior is highly emphasized, with companies prioritizing honesty, fair treatment of all parties, and the preservation of moral values. In line with the principles of fairness, equality, and independence, corporations must also consider the interests of stakeholders. Secondly, accountability is a crucial aspect of governance. Companies are required to report their performance in a fair and transparent manner, ensuring that stakeholders have access to accurate and reliable information (Utama, et al., 2022).

Transparency is another essential pillar of governance in Indonesia. Corporations are expected to provide relevant information that is easily understandable and readily accessible to stakeholders. This transparency fosters trust and enables stakeholders to make informed decisions. Lastly, sustainability is a key consideration in governance implementation.

Corporations are entrusted with the responsibility of contributing to society and protecting the environment. By collaborating with stakeholders, they can promote sustainable development and ensure the long-term well-being of both society and the environment. Overall, Indonesia's governance implementation is guided by comprehensive guidelines and focuses on ethical behavior, accountability, transparency, and sustainability. These pillars serve as the framework for corporations to operate responsibly and contribute to the country's development (Utama, et al., 2022).

Indonesia's governance structure follows a two-tier system, with the board of commissioners serving as the supervisory board and the board of directors as the executive board. The division of supervisory and implementing roles is seen as an efficient measure to mitigate agency issues. As the board of commissioners does not have direct involvement in the company, the audit committee plays a crucial role in assisting with company supervision.

Effective governance serves as a mechanism to address agency issues arising from conflicting interests within a company, impacting various stakeholders. By fostering alignment and cooperation among the parties involved, governance helps mitigate agency problems, safeguarding the interests of stakeholders involved. Governance incorporates various mechanisms to ensure effective supervision. In a two-tier system, the company establishes a supervisory body known as the board of commissioners. This board acts as a supervisor over the directors, preventing them from implementing accounting policies that solely serve their own interests (Chatterjee and Rakshit, 2023; Nguyen, et al., 2024).

Research findings indicate that the supervisory board plays a crucial role in mitigating conflicts of interest and agency problems, as evidenced by the measurement of earnings management (Wasan and Mulchandani, 2020; Assenso-Okofo, et al., 2021; Lukmanul, 2022). By providing robust supervision, the board of commissioners safeguards the stakeholders' interests by minimizing detrimental management actions. It is important to note that the board of commissioners comprises both an independent board and a regular board. The independent board consists of commissioners who have no affiliations with the company, ensuring that their oversight is unbiased and free from any conflicting interests. The research further highlights that the presence of an independent board within the board of commissioners enhances the level of supervision, thereby reducing agency problems (Lukmanul, 2022; Chatterjee and Rakshit, 2023; Nguyen, et al., 2024).

In the process of supervision, the board of commissioners, who are not directly involved in the company's operations, receives assistance from the audit committee. This committee serves as a support system for the commissioners in carrying out their supervisory duties. The audit committee is selected by the commissioners and is required to possess a certain level of experience or expertise in the financial sector. This prerequisite is put in place to ensure effective monitoring of the company's financial activities and to prevent any opportunistic behaviors by the management (Feng and Huang, 2021; Hashed and Almaqtari, 2021; Lukmanul, 2022). By leveraging the oversight provided by the audit committee and its financial expertise, it is anticipated that agency problems can be mitigated. According to recent research, audit committees with financial backgrounds have the potential to reduce agency problems, particularly in terms of earnings management (Franklin and Guerber, 2020; Komal, et al., 2023). Furthermore, external sources such as external auditors, can also contribute to corporate governance. These auditors play a crucial role in instilling confidence among stakeholders regarding the accuracy of the financial information disclosed by the company's management. The competence of the external auditor appointed by the company is inversely related to the occurrence of fraudulent activities (Feng and Huang, 2021; Hashed and Almaqtari, 2021; Komal, et al., 2023).

Based on the formulation of the hypothesis and the findings from previous studies, the following hypotheses are formulated:

- H1

The presence of a board of commissioners decreases agency problems within the company.

- H2

The presence of an independent board of commissioners decreases agency problems within the company.

- H3

The existence of audit committees decreases agency problems within the company.

- H4

The expertise of audit committee members decreases agency problems within the company.

- H5

The use of high-quality auditors decreases agency problems within the company.

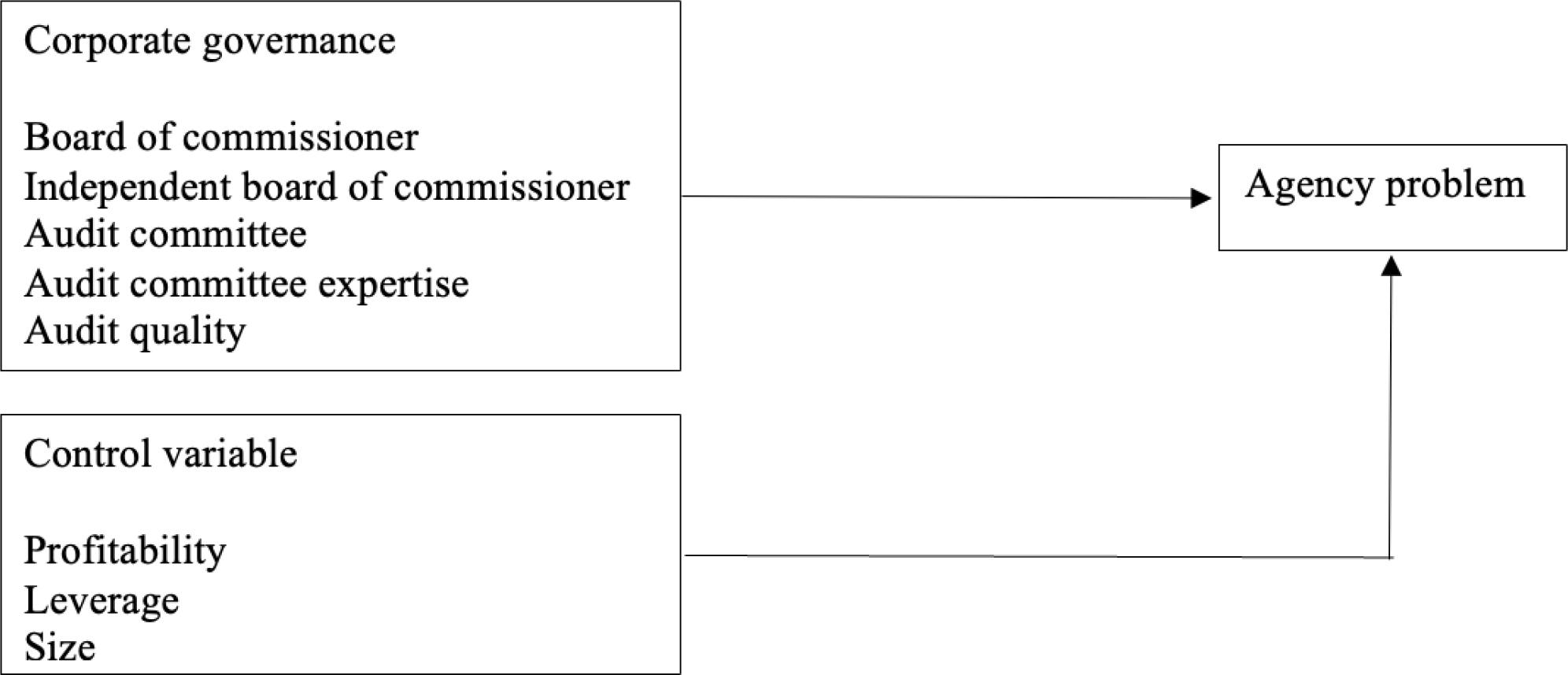

This study utilizes control variables including profitability, leverage, and size. Profitability is effective in addressing agency conflicts by aligning the interests of stakeholders within the company through increased profits. Leverage assists in reconciling conflicting interests between shareholders and creditors, especially when the leverage levels are moderate. In addition, company size can help mitigate agency problems by virtue of larger companies having more intricate organizational structures, potentially reducing opportunistic managerial actions.

The research framework is shown in Figure 2.

Research Framework

(Source: Author’s own research)

The study employed consumer cyclical and consumer non-cyclical sector companies that were listed on the Indonesia Stock Exchange between 2020 and 2022 as the research subjects. Companies classified as consumer cyclical are those whose operations are influenced by economic fluctuations, encompassing industries such as automotive, mining, real estate, oil and gas, airlines, and entertainment. In contrast, consumer non-cyclical companies operate in sectors that remain relatively insulated from economic changes, including food and beverages, retail, and household goods. Given that these two categories encompass all sectors represented on the Indonesia Stock Exchange, this study focuses exclusively on these two sectors. A total of 66 companies were chosen as research samples through the purposive sampling method. Table 1 shows the research sample selection procedure.

Sample Selection Procedure (Source Author’s own research)

| No | Description | Total |

|---|---|---|

| 1. | During the research period, companies in the consumer cyclical and consumer non-cyclical sectors that were listed on the Indonesia Stock Exchange were examined. | 191 |

| 2. | Companies that do not present financial reports as of December 31 | (16) |

| 3. | Companies that do not to use the Rupiah currency | (13) |

| 4. | Companies that experience losses | (96) |

| Total number of companies | 66 | |

| Research period | 3 years | |

| Total number of samples | 198 | |

Variable Measurement (Source: Author’s own research)

| Variable | Definition | Measurement |

|---|---|---|

| Agency problem (AP) | Agency conflicts stem from misaligned incentives between the principal and the agent. In this study, agency conflicts are assessed through the lens of earnings management as proposed by Dechow in 1995. The evaluation of agency conflicts can be conducted by examining earnings management. Thus, this study aims to utilize framework for measuring earnings management. (Dechow, et al., 1995) | |

| Board of commissioners (BOC) | The board of commissioners serves as the overseeing body within a company that operates under a two-tier system. Its primary role is to supervise and offer guidance to the board of directors. | ∑ Number of commissioners |

| Independent commissioners (IND) | Independent commissioners are individuals serving on the board of commissioners without any ties to the company. | |

| Audit committee (AC) | The audit committee functions as an additional supervisory entity selected by the board of commissioners. | ∑ Number of audit committees |

| Audit committee expertise (EXP) | Audit committee members are chosen based on a specific criterion, which is possessing proficiency and practical knowledge in finance. | |

| Audit quality (AQ) | External auditors are individuals who are not affiliated with the company and are designated to ensure the reliability and accuracy of the financial statements. | Audit quality can be assessed by utilizing a binary variable, assigned a value of 1 when the external auditor of the company is affiliated with one of the Big 4 firms, and 0 otherwise. |

| Profitability (PROF) | The profitability of a company demonstrates its capacity to generate a net income | |

| Leverage (LEV) | Leverage refers to the assessment of the proportion of debt to equity within a company. | |

| Firm size (SIZE) | The size of a company is determined by the quantity of assets it possesses. As the number of assets owned increases, so does the magnitude of the company. | Natural logarithm (Total assets) |

To examine the research hypothesis, panel data regression was employed using views. Panel data regression refers to a statistical technique that employs panel data, which integrates both cross-sectional and time series data (Ghozali and Ratmono, 2017, p.193). The dataset utilized in this research is characterized as balanced, comprising three time periods and 66 cross-sectional observations. Within the framework of panel data regression, various models are evaluated to determine the most suitable one for this analysis, specifically the common effect, fixed effect, and random effect models.

The findings of this study indicate that the common effect model is the most appropriate, leading to the application of the Common Ordinary Least Squares (OLS) method for estimation. The research utilized various measurements for each variable under investigation.

The descriptive statistics for each variable is presented below Table 3.

Descriptive Statistics (Source: Author’s own research)

| Maximum | Minimum | Mean | Std. deviation | |

|---|---|---|---|---|

| AP | 0.8393 | - 0.2282 | 0.0045 | 0.1075 |

| BOC | 10 | 2 | 4.1818 | 1.6912 |

| IND | 0.8333 | 0.3333 | 0.4389 | 0.1141 |

| AC | 3 | 3 | 3.0151 | 0.1224 |

| EXP | 1 | 0 | 0.5795 | 0.2503 |

| AQ | 1 | 0 | 0.4595 | 0.4996 |

| PROF | 0.4930 | 0.0002 | 0.0799 | 0.0705 |

| LEV | 7.5853 | 0.0004 | 0.9304 | 0.9918 |

| SIZE | 259,692,979,111 | 180,433,300,000,000 | 14,557,693,746,764 | 27,683,481,766,119 |

AP = Agency Problem, BOC = Board of Commissioners, IND = Independent Board of Commissioners, AC = Audit Committee, EXP = Audit Committee Expertise, AQ = Audit Quality, PROF = Profitability, LEV = Leverage, SIZE = Firm Size (in IDR)

Findings from the descriptive statistics indicate that the supervisory boards, specifically the board of commissioners in consumer cyclical and consumer non-cyclical companies, have an adequate number of supervisors with an average of four individuals. The Independent Board of Commissioners comprises an average of 43%, slightly exceeding the mandated requirement of having at least 30% of commissioners being independent. On average, there are three audit committee members, with 57% of them possessing a financial background. Only approximately 45.95% of consumer cyclical and consumer non-cyclical companies are audited by reputable public accounting firms.

Before testing the research hypothesis, it is advisable to conduct correlation analysis for each research variable to assess the presence of multicollinearity issues. Table 4 shows a correlation analysis of the research variables.

Correlation Results (Source: Author’s own research)

| EM | BOC | IND | AC | EXP | AQ | PROF | LEV | SIZE | |

|---|---|---|---|---|---|---|---|---|---|

| AP | 1 | - | - | - | - | - | - | - | - |

| BOC | - 0.078 | 1 | - | - | - | - | - | - | - |

| IND | - 0.030 | - 0.130 | 1 | - | - | - | - | - | |

| AC | - 0.016 | 0.060 | 0.393 | 1 | - | - | - | - | - |

| EXP | - 0.186 | 0.202 | - 0.150 | - 0.163 | 1 | - | - | - | - |

| AQ | - 0.159 | 0.441 | - 0.022 | - 0.114 | 0.321 | 1 | - | - | - |

| PROF | 0.331 | 0.003 | 0.209 | - 0.124 | 0.215 | 0.146 | 1 | - | - |

| LEV | - 0.137 | 0.214 | 0.315 | 0.409 | 0.007 | 0.118 | - 0.134 | 1 | - |

| SIZE | 0.046 | 0.506 | 0.072 | - 0.111 | 0.176 | 0.470 | 0.058 | 0.157 | 1 |

AP = Agency Problem, BOC = Board of Commissioners, IND = Independent Board of Commissioners, AC = Audit Committee, EXP = Audit Committee Expertise, AQ = Audit Quality, PROF = Profitability, LEV = Leverage, SIZE = Firm Size

It can be inferred according to the findings of the correlation analysis that there is a negative association between corporate governance and agency problems as indicated by discretionary accruals. This suggests that effective governance can lead to a reduction in agency problems within the organization.

Consistent with established theories on agency problems and governance, it is evident that the more robust the governance practices are within the company, the lower is the incidence of agency problems.

The correlation table presented above indicates that multicollinearity is not an issue among the variables, as evidenced by the correlation values that remain below 1. To further validate these findings, the results of the multicollinearity assessment utilizing the Variance Inflation Factor (VIF) are provided in Table 5.

Multicollinearity Results (Source: Author’s own research)

| Variable | VIF |

|---|---|

| BOC | 1.646 |

| IND | 1.522 |

| AC | 1.492 |

| EXP | 1.164 |

| AQ | 1.531 |

| PROF | 1.167 |

| LEV | 1.412 |

| SIZE | 1.620 |

The analysis of the table indicates that multicollinearity is not an issue, as evidenced by the VIF values remaining below the threshold of 10. Alongside the assessment of multicollinearity issues, the Durbin-Watson test is employed to examine autocorrelation, thereby mitigating potential bias in the regression outcomes. The findings from the Durbin-Watson test indicate that the research model under consideration does not exhibit any autocorrelation concerns. The results of this analysis are detailed in Table 6.

Autocorrelation Results (Source: Author’s own research)

| Durbin – Watson | 1.883 |

The outcomes of the autocorrelation assessment conducted via the Durbin-Watson statistic yielded a value of 1.883, surpassing the upper Durbin (DU) threshold as outlined in the Durbin-Watson table. This finding suggests the absence of autocorrelation issues within the research model.

However, to mitigate potential bias, it is essential to address the issue of heteroskedasticity. The present study employs the Breusch- Pagan- Godfrey test, which reveals that the data under investigation exhibit heteroskedasticity concerns. The results of this analysis are detailed in the Table 7.

Heteroskedasticity Results (Source: Author’s own research)

| F-statistic | 11.9135 | Prob. F | 0.0000 |

| Obs*R2 | 66.3754 | Prob. chi-square | 0.0000 |

With a prob. chi-square value below 5%, it shows that there is a heteroskedasticity problem in the research data. With this heteroskedasticity problem, the results of the research conclusions will be incorrect and biased (Ghozali and Ratmono, 2017; Mehmetoglu and Jakobsen, 2017). One way to correct for this problem is to use White's-Heteroskedasticity-Consistent Variance and Standard Error. Standard error correction is done to obtain valid results and will statistically show true parameter values (Ghozali and Ratmono, 2017; Mehmetoglu and Jakobsen, 2017). Therefore, the results of hypothesis testing will use White's approach so that the heteroskedasticity problem does not mislead the research conclusions.

The findings of the study in Table 8 indicate that the independent board of commissioners has the ability to mitigate agency issues type 1 within the organization. This suggests that implementing a two-tier system or separating the roles of supervisors and executives can help alleviate agency problems between investor and management (agency problem type 1). The independent board of commissioners plays a crucial role in overseeing the board of directors to prevent any selfserving accounting practices that may harm the principal. The inherent independence of this commissioner, devoid of any vested interests in the company, enhances the effectiveness of oversight compared to commissioners who possess a stake in the organization. This aligns with (Wasan and Mulchandani, 2020; Feng and Huang 2021; Chatterjee and Rakshit, 2023), and which highlights the importance of effective supervision by the supervisory board in reducing agency problems.

Hypothesis Results (Huber-White) (Source: Author’s own research)

| Variable | Predicted Sign | Coefficient | t-Statistic | Prob. |

|---|---|---|---|---|

| Constanta | - | - 0.567556 | - 2.684904 | - |

| BOC | - | - 0.003839 | - 0.994104 | 0.3214 |

| IND | - | - 0.129492 | - 1.790326 | 0.0750* |

| AC | - | 0.072867 | 1.437175 | 0.1523 |

| EXP | - | - 0.105775 | - 3.045734 | 0.0027* |

| AQ | - | - 0.044776 | - 2.688230 | 0.0078* |

| PROF | -/+ | 0.660226 | 2.272222 | 0.0242* |

| LEV | -/+ | - 0.007082 | - 0.761935 | 0.4470 |

| SIZE | -/+ | 0.015775 | 3.365222 | 0.0009* |

Significant at 1%, 5%, 10%

AP = Agency Problem, BOC = Board of Commissioners, IND = Independent Board of Commissioners, AC = Audit Committee, EXP = Audit Committee Expertise, AQ = Audit Quality, PROF = Profitability, LEV = Leverage, SIZE = Firm Size

Moreover, the research results demonstrate that having an audit committee with a financial background can also help address agency problems. Despite the size of the audit committee not being extensive, the financial expertise within the committee enables them to identify policies that may be detrimental to the principal. Therefore, the financial acumen of the audit committee plays a significant role in mitigating agency problems. This finding is consistent with Franklin and Guerber, 2020; Komal, et al., 2023, and Lukmanul, 2022, which emphasizes the role of audit committee expertise in curbing opportunistic behaviors by the management.

The function of external auditors is instrumental in alleviating type 1 agency problems, which highlight the conflicts between corporate management and investors. By engaging reputable external auditing firms such as PwC, Deloitte, EY, and KPMG, investors can effectively diminish these agency issues. The auditors' role in offering assurance regarding financial statements serves to mitigate this agency problem by decreasing the likelihood of misstatements and fraudulent activities perpetrated by the management (Feng and Huang, 2021; Hashed and Almaqtari, 2021; Komal, et al., 2023).

In addition, the study reveals that variables such as board of commissioners and audit committee alone may not be sufficient in addressing agency problems. The presence of a limited number of board of commissioners and audit committees hinders the effective supervision that can be conducted. Given their crucial role in corporate governance, it is imperative for companies to prioritize the establishment and functioning of independent commissioners and audit committees. From the study's outcomes, it can be inferred that the implementation of good governance practices is essential in reducing agency problems in line with agency theory. Effective supervision is crucial in mitigating agency conflicts between agents and principals.

The findings derived from the test results that incorporate control variables indicate that both profitability and the size of the company are likely to exacerbate agency issues between management and investors. In large corporations, investors often harbor elevated expectations for substantial returns on their investments, which may incentivize management to engage in deceptive practices within financial reporting to satisfy shareholder demands. Consequently, this dynamic intensifies the agency problems present within the organization.

The objective of this study is to gather empirical data on the impact of governance on agency problems. Governance serves as a mechanism to safeguard the principal's interests from the opportunistic behaviours of agents. Findings from the research conducted on consumer cyclical and consumer non-cyclical sector firms in Indonesia indicate that the division of roles between supervisors and executives can mitigate agency problems. This suggests that the implementation of a two-tier system can enhance oversight. In addition, the research findings reveal that the financial expertise of the audit committee can decrease agency problems. However, the presence of an independent board of commissioners, audit committee, and audit quality does not have a significant effect on agency problems.

The study is subject to various constraints, particularly the absence of a definitive measurement tool for agency problems. In addition, the research did not include a comparative analysis with countries utilizing a one-tier system, which could have provided more diverse and conclusive findings. The study is limited by the lack of a precise measurement for agency problems and the absence of a comparative analysis with countries employing a one-tier system. These limitations highlight the need for further research to enhance regulatory frameworks related to corporate governance in Indonesia.