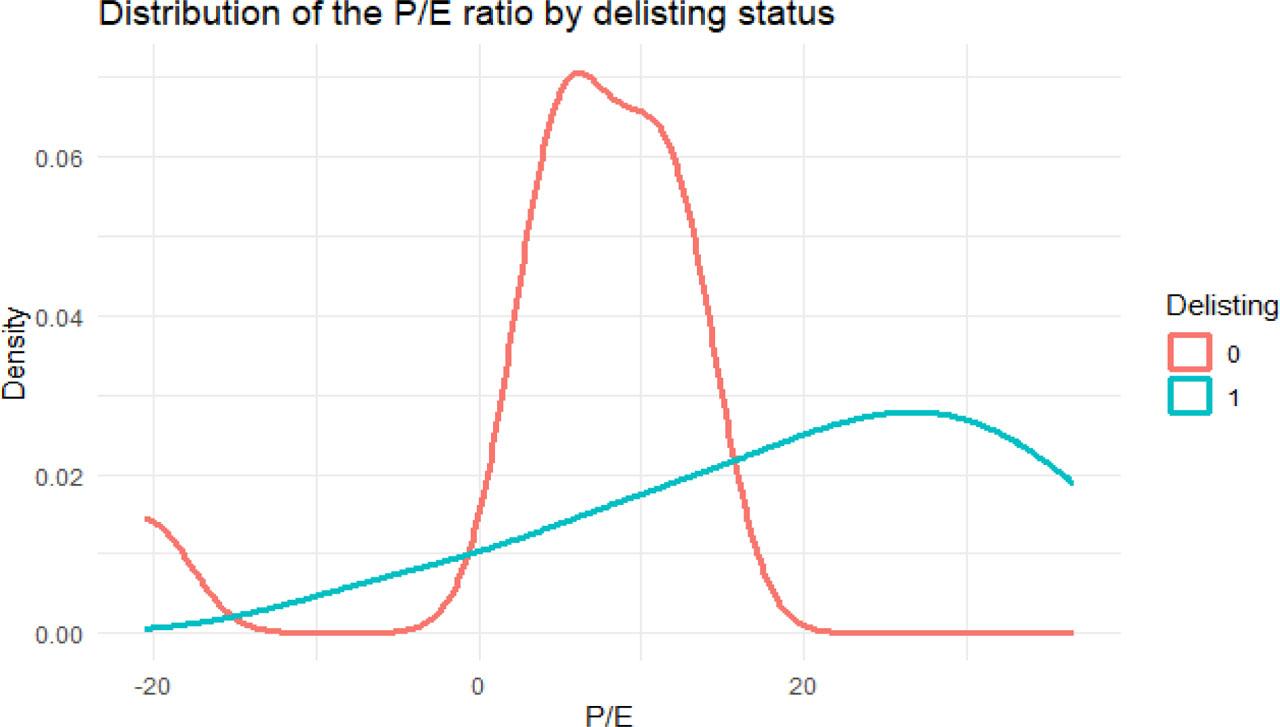

Figure 1.

Figure 2.

Non-financial characteristics of analysed cases

| Company name | Year of debut | Year of delisting | Age of company at IPO | Sector | Market capitalisation before tender offer | Share of controlling shareholder (%) | Nature of entity making tender offer | Reason for delisting |

|---|---|---|---|---|---|---|---|---|

| Ciech | 2005 | 2024 | 60 | Chemical | PLN 2.79 billion | 95.43 | Investor from outside the industry | Ability to respond more quickly and flexibly to changing conditions, facilitate decision-making, and reduce obligations and the scope of published information about the company |

| Polnord S.A. | 1999 | 2021 | 22 | Real estate development | PLN 335 million | 92.92 | Foreign industry entity | Implementation of the Cordia group’s strategy, restructuring of Polnord and consolidation of the group’s operations, which was not possible on the public market |

| STS Holding S.A. | 2021 | 2024 | 24 | Betting | PLN 3.88 billion | 99.28 | Foreign industry entity | Inclusion in the Entain group, which brings together entities from the industry |

| ‘Kruszwica’ Fat Works | 1997 | 2021 | 45 | Food | PLN 1.5 billion | 97.67 | Foreign industry entity | Acquisition by foreign industry player |

| Stelmet S.A. | 2016 | 2020 | 31 | Wooden furniture manufacturing | PLN 265.7 million | 95.37 | Polish investor | Investment in the company’s shares as a long-term investment by the caller |

| Arteria S.A. | 2006 | 2023 | 2 | Outsourcing services | PLN 40.13 million | 95.05 | Foreign industry entity | Acquisition by a foreign industry entity |

| TVN S.A. | 2004 | 2015 | 9 | Media entity | PLN 6.78 billion | 98.76 | Foreign industry entity | Acquisition by a foreign industry entity |

| Mieszko S.A. | 2000 | 2014 | 7 | Confectionery industry | PLN 161.42 million | 91.01 | Foreign investor from outside the industry | Acquisition by a foreign entity from outside the industry |

| Gekoplast | 2014 | 2018 | 47 | Packaging manufacturer | PLN 91.9 million | 99.3 | Foreign entity within the industry | Acquisition by a foreign entity within the industry |

| DZ Bank Polska | 1994 | 2011 | 5 | Bank | PLN 970.24 million | 99.87 | Foreign parent company | Complete acquisition by a foreign parent company |

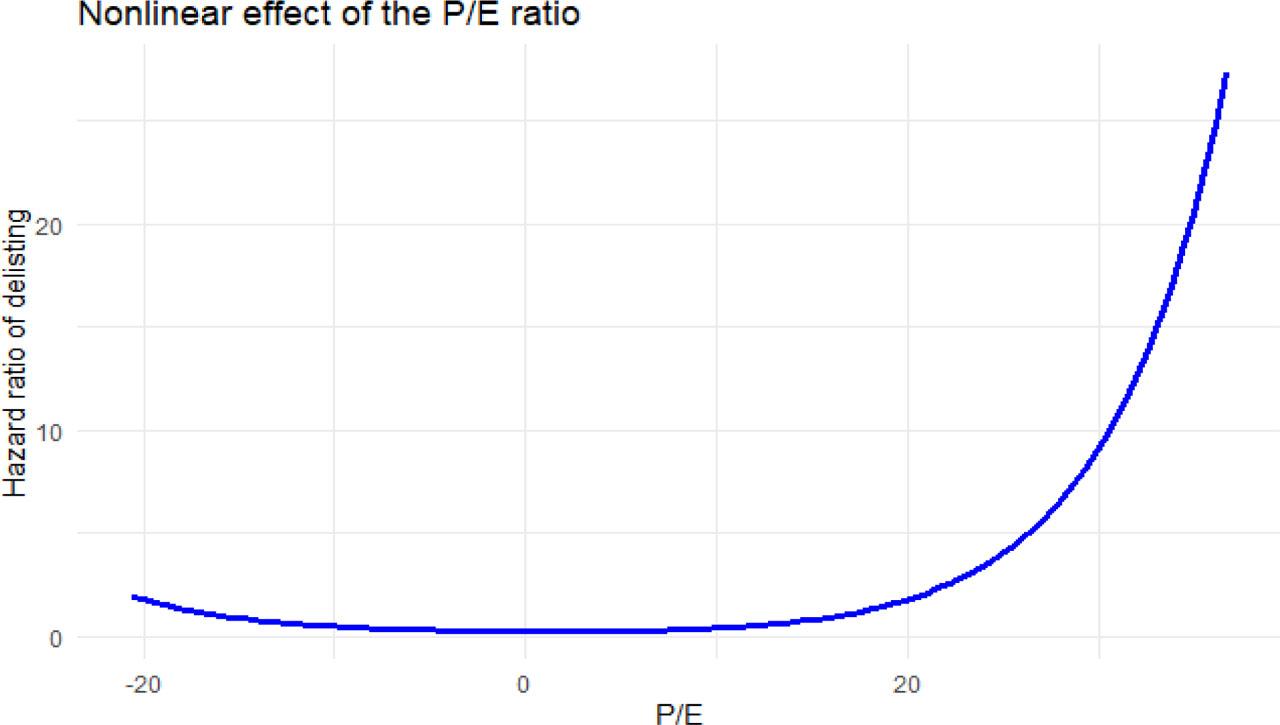

Cox proportional-hazards model results (time-varying effect)

| coef | exp(coef) | e(coef) | z | pr(> |z|) | |

|---|---|---|---|---|---|

| |ΔROE| | −0.09926 | 0.90550 | 0.08936 | −1.111 | 0.26663 |

| log_ Assets | 0.64428 | 1.90462 | 0.30941 | 2.082 | 0.03732 |

| tt(P/E_std) | 1.06830 | 2.91041 | 0.37639 | 2.838 | 0.00454 |

| Concordance = 0.857 (se = 0.086) | |||||

| Likelihood ratio test = 17.41 | |||||

| Wald test = 8.69 | |||||

| Score (logrank) test = 14.96 | |||||

Determinants of stock exchange entry by geographic and temporal perspective

| Authors | Year | Type of factor | Country | Key findings |

|---|---|---|---|---|

| Pagano et al. | 1998 | Financial | Italy | An IPO reduces the cost of debt and equity capital. |

| Carpentier and Suret | 2011 | Non-financial | Canada | Audits by reputable auditors increase the likelihood of survival in the market. |

| Mehmood, Mohd-Rashid & Ong | 2021 | Macroeconomic | Pakistan | The stock market index level, inflation, GDP growth rate, foreign direct investment and treasury bill interest rates are important for determining the IPO date. |

| Riyath and Dayaratne | 2025 | Financial | Sri Lanka | Increasing the added value of the company as a result of listing by expanding the ownership structure and creating strategic partnerships. |

Summary of results

| Case | Short existence at IPO (<5 years) | Negative average ROE | Low P/BV (<1) | PE/investment company | Mature sector | Quick delist (<5 years) | High ownership (>90%) | Low P/E (<10) |

|---|---|---|---|---|---|---|---|---|

| Ciech | ✘ (60 years) | ✘ (0.17%) | ✘ (1.1) | ✘ | ✔ (chemical) | ✘ (19 years) | ✔ (95.43%) | ✔(7.6) |

| Polnord S.A. | ✘ (22 years) | ✔(−0.16%) | ✔(0.77) | ✘ | ✔(developer) | ✘ (22 years) | ✔ (92.92%) | ✘ (31.90) |

| STS Holding S.A | ✘ (24 years) | ✔ (−79.40%) | ✘ (13.22) | ✘ | ✔ (bookmaker) | ✔ (3 years) | ✔ (99.28%) | ✘ (22.58) |

| ‘Kruszwica’ Fat Works | ✘ (45 years) | ✘ (3.87%) | ✘ (1.8) | ✘ | ✔ (food) | ✘ (24 years) | ✔ (97.67%) | ✘ (22.60) |

| Stelmet S.A. | ✘ (31 years) | ✔ (−852.84%) | ✔(0.57) | ✔ (Investment Fund) | ✔ (manufacturing) | ✔ (4 years) | ✔ (95.37%) | ✘ (27.50) |

| Arteria S.A. | ✔ (2 years) | ✔ (−193.03%) | ✔(0.89) | ✘ | ✔ (services) | ✘ (17 years) | ✔ (95.05%) | ✔(−4.76) |

| TVN S.A. | ✘ (9 years) | ✘ (7.99%) | ✘ (6.9) | ✘ | ✔ (media) | ✘ (11 years) | ✔ (98.76%) | ✘ (36.7) |

| Mieszko S.A. | ✘ (7 years) | ✘ (5.88%) | ✔(0.81) | ✔ (Investment Company) | ✔ (food) | ✘ (17 years) | ✔ (91.01%) | ✔(9.7) |

| Gekoplast | ✘ (47 years) | ✘ (16.56%) | ✘ (3.23) | ✔ (PE) | ✔ (manufacturing) | ✔ (4 years) | ✔ (99.3%) | ✘ (17.4) |

| DZ Bank Polska | ✔ (5 years) | ✘ (5.16%) | ✘ (2.67) | ✘ | ✔ (bank) | ✘ (17 years) | ✔ (99.87%) | ✘ (32.7) |

PSM matched pairs

| Study group company | Control group match | Industry sub-index |

|---|---|---|

| Ciech | Polwax S.A. | WIG-Chemia |

| Polnord S.A. | ATREM | WIG-Budownictwo |

| STS Holding S.A. | BOOMBIT | WIG-Gry |

| Zakłady Tłuszczowe ‘Kruszwica’ | PEPEES | WIG-Spożywczy |

| MIESZKO S.A. | ASTARTA | WIG-Spożywczy |

| Stelmet S.A. | KGHM | WIG-Górnictwo |

| TVN S.A. | PMPG | WIG-Media |

| Gekoplast S.A. | ODLEWNIE POLSKIE SA | WIG-Przemysł |

| DZ Bank Polska | SANPL | WIG-Banki |

| Arteria S.A. | PKP CARGO | Sektor Usługi Inne |

Determinants of stock exchange exit by geographic and temporal perspective

| Authors | Year | Type of factor | Country | Key findings |

|---|---|---|---|---|

| Morgenstern et al. | 2004 | Non-financial | USA | The crisis of confidence in the financial and regulatory sector is causing a withdrawal from the stock market. |

| Yang and Sheu | 2006 | Non-financial | Taiwan | The probability of delisting decreases with the company’s seniority at the time of IPO. |

| Marosi and Massoud | 2007 | Financial | USA | Delistings may be caused by an increase in audit fees. |

| Leuz et al. | 2008 | Non-financial | USA | The departures are the result of agency problems arising from the shareholding structure. |

| Mayur and Kumar | 2013 | Macroeconomic | India | The intensity of the phenomenon depends on the stage of the economic cycle. |

| Pour and Lasfer | 2013 | Financial | Great Britain | The shorter the listing period and the higher the costs, the greater the likelihood of delisting. |

| Tutino et al. | 2013 | Non-financial | Italy | Small companies in slow-growth industries are more likely to delist from the stock exchange. |

| Konno and Itoh | 2017 | Non-financial | Japan | The debt-to-assets ratio is not relevant when analysing delistings. The wealth transfer hypothesis, the ratio of listing costs to company profits and industry characteristics are relevant. |

| Kang | 2017 | Non-financial | Korea | There are industries with an increased likelihood of delisting: textiles and clothing, construction and trade. The important role of shareholder structure. |

| Bessler et al. | 2019 | Non-financial | Germany | The decision to delist is motivated by the desire to start trading on less liquid market segments. |

| Botha et al. | 2025 | Non-financial and macroeconomic | South Africa | The likelihood of delisting is influenced by management transparency, the level of institutional influence, the age of the company, analyst recommendations and macroeconomic factors. |

Financial characteristics of analysed cases

| Company name | P/E | P/BV | Average turnover | Free float | Premium in tender offer |

|---|---|---|---|---|---|

| Ciech | 7.6 | 1.1 | 2.802 million | 100% | PLN 53 06/11/2023 (2%) |

| 3,518,455 | 27.3% | ||||

| Polnord S.A. | 31.90 | 0.77 | 0.141 million | 100% | PLN 2.84 30/11/2021 (25%) |

| 2,494,653 | 18%–20% | ||||

| STS Holding S.A. | 22.58 | 13.22 | 2.624 million | 0% | PLN 24.6 04/10/2023 (1%) |

| 7,061,867 | 20%–25% | ||||

| ‘Kruszwica’ Fat Works | 22.60 | 1.8 | 0.464 million | PLN 65.8 26/02/2021 (1%) | |

| 442,785 | 18% | ||||

| Stelmet S.A. | 27.50 | 0.57 | 0.032 million | PLN 9.05 28/07/2020 (0%) | |

| 228,189 | 7% | ||||

| Arteria S.A. | -4.76 | 0.89 | 0.010 million | 2 | PLN 9.40 20/04/2023 (−5%) |

| 8,917 | 18% | ||||

| TVN S.A. | 36.7 | 6.9 | 5.817 million | 0% | PLN 19.92 22/09/2015 |

| Mieszko S.A. | 9.7 | 0.81 | 0.282 million | 0% | PLN 3.95 25/11/2014 |

| Gekoplast | 17.4 | 3.23 | 0.041 million | 0% | PLN 15.20 15/02/2018 |

| DZ Bank Polska | 32.7 | 2.67 | 66,331 | 0% | PLN 15.21 21/09/2010 |