Functioning as a publicly listed company entails a complex trade-off between strategic benefits, such as access to capital and enhanced prestige, and significant regulatory and operational costs. In recent years, the costs of public market participation have assumed increasing prominence, as evidenced by a global trend: a declining number of enterprises choosing to debut on stock exchanges through initial public offerings (IPOs) and a simultaneous rise in voluntary delistings. While the determinants of these phenomena have been extensively documented from various temporal and geographical perspectives, existing analyses focus predominantly on developed markets characterised by stable institutional frameworks and low systemic risk.

A notable research gap concerns the systematic identification of factors influencing delisting under conditions of heightened economic uncertainty in the post-transition markets of Central and Eastern Europe (CEE). Post-transition markets are defined here as economies that have completed the primary transformation from centrally planned to market-oriented systems but still exhibit institutional, financial and organisational characteristics that distinguish them from mature developed markets (Broz, Barbić & Palić, 2018; Jankowska, Bartosik-Purgat & Olejnik, 2021). These markets tend to be characterised by higher volatility, greater sensitivity to external shocks, limited liquidity and concentrated ownership structures, all of which may modify the predictive power of traditional delisting determinants. Empirical evidence on whether the factors previously identified as critical in developed economies—ownership concentration, profitability and market valuation—retain their relevance in this more turbulent setting remains limited.

The Polish capital market serves as a representative case for this study. Poland is widely regarded as a regional leader in economic growth and market development, and despite the historical rupture caused by the transition from a planned economy, the Warsaw Stock Exchange (WSE) has established itself as a comparatively robust platform among CEE markets. The trajectory of Poland’s free-market development provides a compelling setting in which to analyse why established firms choose to withdraw from public trading.

The primary objective of this article is to identify the financial and non-financial characteristics associated with voluntary delisting decisions in post-transition markets. The study examines firms that delisted from the WSE between 2010 and 2024. The variables considered include company age at IPO, listing duration, ownership concentration (with particular attention to the share and identity of the majority shareholder), the identity of the auditor and the industry sector, alongside key financial indicators—return on equity (ROE), debt ratios and EBITDA—and the price-to-earnings (P/E) market valuation metric, all observed over the 5-year period preceding the exit. These criteria were derived from a synthesis of the existing literature and adapted to the specificities of the Polish market.

The contribution of this research lies in the integration of a post-transition market perspective into the broader delisting discourse. The paper employs a mixed-methods approach that combines a multiple cross-case study with quantitative techniques—propensity score matching (PSM) and the Cox proportional-hazards model—to provide a more comprehensive empirical examination of delisting determinants than is typically offered in qualitative-only analyses of the region. The 2010–2024 study period encompasses several episodes of substantial macroeconomic uncertainty, including the European sovereign debt crisis, the COVID-19 pandemic and the macro-financial dislocations following the onset of the Russia–Ukraine conflict. Understanding how firms in less stable institutional environments respond to such pressures is increasingly relevant as global economic uncertainty extends to markets previously regarded as stable.

The remainder of the paper is organised as follows. Section 2 reviews the literature on IPO and delisting determinants and outlines the theoretical framework drawn from Market Timing Theory. Section 3 develops the research hypotheses and describes the qualitative and quantitative methodologies employed. Section 4 presents and discusses the findings. Section 5 concludes with the principal contributions, limitations of the study and avenues for future research.

Companies pursue stock exchange listings to enhance liquidity, expand financing opportunities and access strategic partners (Pagano, Panetta & Zingales, 1998; Asker, Farre-Mensa & Ljungqvist, 2015; Riyath & Dayaratne, 2025). Historically, IPO proceeds have predominantly funded tangible and financial investments, supported working capital and reduced debt (Łukasik, 1998). Beyond these financial motives, firms also use listing to improve their image, corporate governance and competitive position, with the relative weight of these objectives varying by jurisdiction, business-cycle phase and firm age at debut (Kim & Weisbach, 2008; Mayur & Kumar, 2013). IPO volumes are procyclical: economic expansion brings rising offerings and elevated prices, and following positive macroeconomic shocks the market typically absorbs a wave of less reputable, lower-profitability entrants (Çolak, Yung & Wang, 2008). Shifts in investor sentiment provide an additional explanation for fluctuations in IPO activity (Lowry, 2003). The motives that underlie the decision to list are subsequently re-evaluated during public-market operations; when those motives no longer hold, firms begin to consider withdrawal from public trading. Table 1 summarizes the most important studies on the determinants of stock exchange entry from a geographic and temporal perspective.

Determinants of stock exchange entry by geographic and temporal perspective

| Authors | Year | Type of factor | Country | Key findings |

|---|---|---|---|---|

| Pagano et al. | 1998 | Financial | Italy | An IPO reduces the cost of debt and equity capital. |

| Carpentier and Suret | 2011 | Non-financial | Canada | Audits by reputable auditors increase the likelihood of survival in the market. |

| Mehmood, Mohd-Rashid & Ong | 2021 | Macroeconomic | Pakistan | The stock market index level, inflation, GDP growth rate, foreign direct investment and treasury bill interest rates are important for determining the IPO date. |

| Riyath and Dayaratne | 2025 | Financial | Sri Lanka | Increasing the added value of the company as a result of listing by expanding the ownership structure and creating strategic partnerships. |

IPOs, initial public offerings

Withdrawal from public markets has become a global phenomenon (Martinez & Serve, 2017), with delistings now frequently outnumbering new offerings and creating a so-called ‘listing gap’ (Doidge et al., 2017). The literature identifies two broad categories of determinants: firm-level characteristics—financial condition, ownership structure, age and industry—and external conditions, including the macroeconomic environment, regulatory regime and the structure of the private capital market.

Among firm-level characteristics, age at IPO and listing duration have received considerable attention. Firms registered for longer periods prior to going public have stronger chances of remaining listed (Yang & Sheu, 2006), and the probability of withdrawal due to regulatory violations peaks approximately 4 years after the IPO, while transfers and Mergers and Acquisitions-related (M&A-related) delistings occur on average 2 years post-IPO (Pour & Lasfer, 2013). Longer-listed firms also accumulate longer financial histories, enabling more accurate valuation and reducing information asymmetry.

Financial condition is a further important predictor. Return on Equity (ROE) has been identified as a significant variable, with sustained profitability associated with lower delisting risk (Chou, Cheng & Chien, 2011; Sokołowska, 2012). Higher financial leverage, measured by debt-to-assets, is linked to greater uncertainty and shorter post-IPO survival (Demers & Joos, 2007), and the leverage–profitability nexus underscores the complementarity of financial determinants of voluntary withdrawal (Margaritis & Psillaki, 2010). Higher absolute share prices also correlate with lower delisting probability (Fernando et al., 2004). Evidence from the Johannesburg Stock Exchange reinforces these findings: Makuvaza et al. (2025) report that the frequency of financial distress events, the duration of loss-making periods and consecutive revenue declines raise delisting risk, with profitability metrics (Return on Assets - ROA), firm size and listing duration acting in concert with macroeconomic conditions.

Firm size and industry membership shape delisting incentives. Larger entities amortise fixed listing costs more efficiently, so smaller firms tend to delist first when those costs rise (DeAngelo, DeAngelo & Rice, 1984). Firms exiting public markets are typically small and operate in mature, slow-growth sectors (Tutino, Panetta & Laghi, 2013), and frequently relocate to less liquid market segments rather than going fully private (Bessler et al., 2019). Industry affiliation matters: delistings are more common outside the technology sector, with concentrations observed in textiles and apparel, construction and retail (Kang, 2017). Underwriter and auditor reputation are also associated with post-IPO survival (Carpentier & Suret, 2011).

Ownership concentration is among the structural determinants most directly relevant to voluntary delisting. Firms with a high concentration of the largest shareholding more frequently exit public markets (Kang, 2017), as dominant shareholders find it operationally and legally easier to cross the voting-rights threshold required to execute a squeeze-out—a threshold that varies by jurisdiction. Concentrated ownership is also a recognised source of agency conflict (Leuz, Triantis & Wang, 2008), and listing-maintenance costs interact with firm-specific profitability in shaping the cost–benefit calculus of the remaining public (Pour & Lasfer, 2013; Konno & Itoh, 2017). A multifactorial analysis of the Johannesburg Stock Exchange by Lansdell, Botha and Marx (2025), using a panel probit on 302 firms, shows that liquidity and market valuation mitigate delisting risk, while governance quality and shareholder composition lower it further, with macroeconomic conditions exerting additional external pressure.

Macroeconomic and policy conditions constitute a second set of determinants. High inflation, elevated interest rates, restricted credit access, weak economic activity and high unemployment have all been linked to higher delisting probability (Botha, Lansdell & Marx, 2025), with stock-index movements, foreign direct investment and treasury bill rates providing additional explanatory power (Mehmood et al., 2021). Weak macroeconomic signals also intensify information asymmetry and raise issuance costs (Çolak, Durnev & Qian, 2017). The more diversified a firm’s ownership structure and the greater its management transparency, the lower the risk of withdrawal—primarily because no single shareholder can readily assemble the voting majority needed to execute a tender offer; wealth-transfer motives among dominant shareholders thus become a central mechanism in voluntary exit (Konno & Itoh, 2017).

The regulatory environment plays a comparable role. Krastiņš and Pētersons (2017) document that Continental European IPO firms tend to be more mature than their UK counterparts, reflecting differences in the financial-system architecture. More broadly, economic policy uncertainty and business risk are recognised drivers of voluntary withdrawal (Azevedo et al., 2024). In Poland, the 2014 dismantling of open pension fund assets and similarly disruptive episodes weakened institutional demand and contributed to declining investor confidence (Gemra & Rogowski, 2020). Regulatory tightening operates in the same direction: voluntary delistings from US exchanges rose by approximately 30% following the passage of the Sarbanes–Oxley Act (Morgenstern, Nealis & Kleinman, 2004), driven not only by formal compliance burdens but also by rising audit fees (Marosi & Massoud, 2007). The earliest systematic evidence on listing costs (DeAngelo et al., 1984) already showed that firms voluntarily leaving the market improved their profitability afterwards through cost reduction and faster decision-making.

The structure of the private capital market is a further institutional determinant. A well-developed private equity (PE) market lowers the financing cost of remaining private and weakens the incentive to publicly disclose firm-level information (Lattanzio, Megginson & Sanati, 2023). PE-backed buyouts disproportionately target small, undervalued firms with dispersed ownership—features that facilitate post-acquisition control consolidation—and the relevance of these determinants varies with the economic cycle, with free cash flow volatility playing a more substantial role than leverage (Bregneberg & Jensen, 2018). Rising firm-level operating costs unrelated to listing, such as wage growth, may further accelerate exit pressure for less established firms (Baxamusa & Jalal, 2023).

Information asymmetry and disclosure quality have also been documented as delisting determinants. Evidence from the Athens Stock Exchange indicates that delisting probability and time-to-delisting are higher for firms with larger relative offerings and observable earnings management, but lower in ‘hot issue’ periods and where audit quality, prospectus informativeness and voluntary disclosures are strong (Makrominas & Yiannoulis, 2021). Governance quality reinforces these effects: a synthetic index based on supervisory board characteristics constructed from 895 Vietnamese firms indicates that stronger governance, lower state ownership and greater foreign capital participation are associated with reduced delisting risk; although that study addresses involuntary delisting in a frontier market, the underlying governance mechanisms are equally pertinent to the voluntary case (Nguyen, Heui-Yeong Kim & Suardi, 2025).

Despite this extensive literature, empirical investigation remains concentrated in developed markets and selected emerging economies. The CEE region—and Poland in particular—has been examined less systematically, even though the WSE occupies a distinctive position among post-transition markets. As summarized in Table 2, existing evidence on the determinants of stock exchange exit is predominantly drawn from developed markets and a limited number of emerging economies, leaving the CEE region relatively underexplored. The present study addresses this gap by analysing voluntary delistings from the WSE during 2010–2024.

Determinants of stock exchange exit by geographic and temporal perspective

| Authors | Year | Type of factor | Country | Key findings |

|---|---|---|---|---|

| Morgenstern et al. | 2004 | Non-financial | USA | The crisis of confidence in the financial and regulatory sector is causing a withdrawal from the stock market. |

| Yang and Sheu | 2006 | Non-financial | Taiwan | The probability of delisting decreases with the company’s seniority at the time of IPO. |

| Marosi and Massoud | 2007 | Financial | USA | Delistings may be caused by an increase in audit fees. |

| Leuz et al. | 2008 | Non-financial | USA | The departures are the result of agency problems arising from the shareholding structure. |

| Mayur and Kumar | 2013 | Macroeconomic | India | The intensity of the phenomenon depends on the stage of the economic cycle. |

| Pour and Lasfer | 2013 | Financial | Great Britain | The shorter the listing period and the higher the costs, the greater the likelihood of delisting. |

| Tutino et al. | 2013 | Non-financial | Italy | Small companies in slow-growth industries are more likely to delist from the stock exchange. |

| Konno and Itoh | 2017 | Non-financial | Japan | The debt-to-assets ratio is not relevant when analysing delistings. The wealth transfer hypothesis, the ratio of listing costs to company profits and industry characteristics are relevant. |

| Kang | 2017 | Non-financial | Korea | There are industries with an increased likelihood of delisting: textiles and clothing, construction and trade. The important role of shareholder structure. |

| Bessler et al. | 2019 | Non-financial | Germany | The decision to delist is motivated by the desire to start trading on less liquid market segments. |

| Botha et al. | 2025 | Non-financial and macroeconomic | South Africa | The likelihood of delisting is influenced by management transparency, the level of institutional influence, the age of the company, analyst recommendations and macroeconomic factors. |

IPOs, initial public offerings

The macroeconomic and firm-level factors discussed above are consistent with the predictions of Market Timing Theory, which holds that the timing of capital market entry and exit reflects perceived divergences between market and intrinsic firm value. In its IPO-side formulation, firms time their public offerings to periods of favourable market conditions, when the ratio of market value to book value is elevated and equity is relatively inexpensive (Taggart, 1977; Chang, Chen & Dasgupta, 2019). Bear markets correspondingly depress IPO volume, as managers postpone offerings until valuations recover (Ritter & Welch, 2002), although firms with urgent financing needs may proceed regardless (Lerner, Shane & Tsai, 2003). IPO activity also rises in anticipation of cyclical upturns, as forecasts of future earnings begin to enter prevailing valuations (Batnini, 2015). The exit-side prediction has traditionally been framed in mirror-image terms: managers and controlling shareholders are expected to repurchase shares or take the firm private when the market undervalues it, capturing the resulting valuation gap (Ikenberry, Lakonishok & Vermaelen, 1995; Ater, 2017). The relationship is more nuanced, however, in markets with concentrated ownership and squeeze-out mechanisms, where the controlling shareholder’s decision balances three offsetting forces: the cost of acquiring residual minority shares (favoured by low prices), the value of the controlling stake itself (favoured by high prices) and the firm’s attractiveness to strategic acquirers (also favoured by sustained high valuations). The net direction is therefore an empirical question, particularly in post-transition markets where dominant shareholders frequently exit by transferring the firm to a strategic or industry buyer rather than by repurchasing it at a discount. The 2010–2024 period under analysis encompasses several phases of macroeconomic stress through which the market-timing channel could plausibly operate. The empirical analysis below examines this channel on the WSE under such conditions, with particular attention to the time-varying effect of market valuation on the delisting hazard. The literature review thus identifies three sets of determinants—financial condition, ownership structure and market valuation—that motivate the three hypotheses developed in the following section.

This study focuses exclusively on voluntary delistings, defined as cases in which the decision to withdraw from the stock exchange was initiated by the company or its majority shareholder rather than imposed by regulatory authorities for violations of listing requirements. Involuntary delistings—which may result from insolvency, regulatory non-compliance or exchange-mandated removal—are governed by fundamentally different determinants and are therefore excluded from the present analysis. The motivations, agency dynamics and financial characteristics associated with the two categories differ substantially (Martinez & Serve, 2017; Nguyen et al., 2025).

Drawing on the literature reviewed above and the identified gap concerning the institutional specificities of post-transition markets, the empirical investigation is centred on the most directly relevant determinants of delisting. Unlike developed Anglo-Saxon markets, the Polish capital market is characterised by a relatively short operational history, high ownership concentration and limited free float. Consequently, while several additional factors (e.g. company age at IPO, industry maturity and listing duration) are addressed in the qualitative comparative analysis, the quantitative testing is built around the following three hypotheses.

Hypothesis 1 (H1): Deteriorating and unstable financial performance is associated with an increased probability of delisting. Specifically, a high absolute variance and a negative trajectory in the ROE over the 5 years preceding the decision are expected to correlate with the firm’s withdrawal from public trading.

Hypothesis 2 (H2): High ownership concentration is a key structural determinant of voluntary delisting. In post-transition markets, agency dynamics and the regulatory architecture of squeeze-out mechanisms imply that the presence of a dominant shareholder exceeding the 90% voting-rights threshold is associated with a higher probability of exit from the public market.

Hypothesis 3 (H3): The relationship between market valuation and voluntary delisting is time-dependent. A persistently high P/E ratio is associated with an increased probability of delisting, and the strength of this association rises with listing tenure.

Case study methodology has been the dominant analytical tool in previous research on emerging and developing market delistings. Bilel and Khammassi (2024) analysed the phenomenon across selected firms from Tunisia, Morocco and Egypt, while Muyeche, Murape and Mungwini (2014) examined the financial performance preceding delisting on the Zimbabwe Stock Exchange.

Given the exploratory nature of the present research, a multiple cross-case study methodology was adopted. A single-case approach was rejected because it does not permit the generalisation of findings. The analysis encompasses 10 purposively selected companies that voluntarily delisted from the WSE between 2010 and 2024. The Polish market, as a leading post-transition economy, provides a compelling setting in which to examine the life cycle of public companies under conditions of systemic uncertainty and a recent preponderance of delistings over IPOs.

The classification of Poland’s capital market warrants explicit attention. The WSE was reclassified as a Developed Market by FTSE Russell in September 2018, making Poland the first post-communist country to achieve this status. Morgan Stanley Capital International (MSCI), however, continues to classify Poland as an Emerging Market, and several structural characteristics—relatively concentrated ownership patterns, lower market liquidity compared with Western European peers, a shorter institutional history and ongoing regulatory convergence with EU standards—indicate that the WSE retains features distinctive to post-transition markets (Fîrcescu, 2012; Adamska, Dąbrowski & Grygiel-Tomaszewska, 2016). This study therefore uses the term ‘post-transition market’ to reflect Poland’s intermediate position: an economy that has achieved significant institutional maturity while retaining structural vulnerabilities characteristic of the Central and Eastern European region. This framing is consistent with recent scholarship that treats CEE markets as a distinct analytical category rather than mapping them onto the developed/developing binary (Latinovic & Milosevic, 2019; Dodig, 2020).

Sample selection prioritised diversification across industries (chemical, real estate, banking, manufacturing, food, bookmaking, services and media), operational profiles and listing durations. Between 2010 and 2024, approximately 241 companies voluntarily delisted from the main market of the WSE, of which the 10 cases selected for this study represent approximately 4%. The selection was purposive rather than exhaustive, targeting large-scale, industry-leading entities whose delistings attracted significant market and media attention and whose financial data were sufficiently available for analysis. While this sampling strategy limits statistical representativeness, it maximises analytical depth—a recognised advantage of the multiple case study methodology (Yin, 2018). Two of the selected firms had previously been State Treasury entities, providing additional insight into the post-privatisation phase of the Polish market.

The qualitative analysis drew on WSE regulatory communications and the EMIS financial database. Each case was initially analysed independently before synthesis within a cross-case framework to identify common strategic patterns. The cross-case synthesis followed the replication logic recommended by Yin (2018), under which each case is treated as an independent experiment. After individual case analysis, the results were compared across all 10 cases using a pattern-matching approach: for each hypothesised determinant, the analysis assessed whether the predicted pattern (e.g., high ownership concentration → delisting) was consistently observed, partially supported or contradicted. Convergent findings across cases were treated as consistent patterns, while divergent outcomes prompted investigation of contextual moderators such as industry characteristics or timing relative to macroeconomic shocks.

The legal framework governing voluntary delisting in Poland is established principally by the Act of 29 July 2005 on Public Offering and the Conditions for Introducing Financial Instruments to an Organised Trading System and on Public Companies (Dz.U.2025.592 t.j.). Under this legislation, a shareholder wishing to delist a company must first conduct a mandatory tender offer (wezwanie) for the remaining shares. The critical threshold is 90% of total voting rights—once exceeded, the majority shareholder may execute a compulsory buy-out (squeeze-out) of the minority (Art. 82). The tender offer price must not be lower than the average market price of the preceding 6 months or, alternatively, the highest price paid by the offeror in the preceding 12 months. The Polish Financial Supervision Authority (KNF) oversees the process and has the power to intervene in cases of inadequate pricing or procedural irregularities. This regulatory framework creates a distinctive institutional context for voluntary delisting, in which the 90% threshold effectively determines the structural feasibility of going private—a pattern observed in all 10 analysed cases.

To complement and test the qualitative patterns, the study employs two quantitative techniques previously applied in the delisting literature—PSM and the Cox proportional-hazards model (Pour & Lasfer, 2013; Azevedo et al., 2024). Financial indicators for the 10 delisted firms, including ROE, the P/E ratio and total assets, were extracted from the EMIS and Orbis databases for the 5-year period preceding the delisting event.

To construct a comparable control group of active, non-delisted companies, PSM was applied. For each firm in the treatment group, a matched ‘twin’ company was selected from the same WSE sector sub-index. The matching used a logistic regression to estimate the propensity score as:

The Cox proportional-hazards model was then estimated to identify the factors associated with delisting risk and to capture the time-varying impact of financial variables. The general form of the model is:

The study period (2010–2024) encompasses several major macroeconomic shocks that may have influenced delisting dynamics on the WSE: the European sovereign debt crisis (2011–2012), the COVID-19 pandemic and associated market disruption (2020–2021), the onset of the Russia–Ukraine conflict in February 2022, with its acute impact on Central European energy markets and investor sentiment, and the subsequent inflationary spiral and monetary tightening cycle. Rather than treating these events as confounding factors to be controlled away, the analysis treats them as integral features of the heightened uncertainty environment that characterises post-transition markets. Given the exploratory nature of the study and the small sample (n = 10), the cross-case methodology is used to identify recurrent patterns across these varying macroeconomic conditions; the findings should accordingly be read as preliminary evidence on the determinants of delisting rather than as conclusive empirical proof.

The selected cases are examined with respect to the timing of commencement and termination of public market listing, company age at debut, sector of activity, market capitalisation prior to the tender offer, level of shareholding held by the majority shareholder, the character of the entity initiating the buy-out and the officially stated reason for delisting.

The first analysed entity is the chemical company Ciech S.A., which conducted its IPO as a mature company and remained listed on the Polish public market for 19 years. The entity initiating the buy-out, holding over 95% of shares, was an investor from outside the chemical industry. The decision to terminate listing was justified by the prospect of faster business decision-making and a reduction in the firm’s mandatory disclosure scope. Ciech operated as a European leader in its sector and had historically belonged to the State Treasury, with its privatisation process generating considerable public debate. The firm currently operates as a private company under the name Qemetica S.A., although energy price changes and environmental regulations have constrained its ability to maintain its previous scale of operations in Poland.

Polnord S.A. was a significant player in the Polish real estate development market. It listed on the WSE in 1999, having operated for over 20 years prior to its debut. Delisting was decided in 2021 following a tender offer by the majority shareholder (92.92%), a foreign industrial entity. The process formed part of group restructuring and consolidation, proceeded relatively quickly, and offered prices markedly above the last market price. The firm also attracted media attention owing to political connections and ongoing proceedings.

STS Holding S.A. was a leader in the Polish bookmaking market. Its debut was likewise conducted relatively late, as the firm had existed for over 20 years prior to listing. A foreign industrial entity held over 99% of company shares at the time of the tender offer, the stated objective being the firm’s incorporation into a group of similar entities.

Zakłady Tłuszczowe ‘Kruszwica’ (Kruszwica Fat Works) illustrates a case in which the firm was officially liquidated while its production continued under the acquiring entity. With 45 years of tradition at the time of IPO, Kruszwica had been a leader in fat production and had previously been a State Treasury company for an extended period. Following privatisation in 1997, the strategic investor—a Dutch group and one of the world’s largest oilseed processors—progressively raised its shareholding. The acquirer delisted Kruszwica in 2021 and liquidated it in 2022. The firm’s post-listing activities subsequently raised concerns with the Polish Financial Supervision Authority (KNF), which placed Kruszwica Fat Works and its owner on the KNF warning list.

In some cases, delisting forms part of the controlling shareholder’s long-term strategy from the outset. Stelmet S.A. (manufacture of wooden elements) followed this pattern, being listed for only 4 years.

In the remaining cases, withdrawal followed acquisition by foreign entities operating in outsourcing services (Arteria S.A.), media (TVN S.A.), confectionery (Mieszko S.A.), packaging production (Gekoplast) and banking (DZ Bank Polska). The relationship between company maturity at debut and listing duration is not uniform: Arteria S.A. remained listed for 17 years despite being only 2 years old at IPO, while Gekoplast, which listed after 47 years of operation, remained public for only 4 years. Across the 10 cases, only two firms listed at an early stage of development, while 6 had existed for over 20 years at the time of debut. Table 3 provides an overview of the non-financial characteristics of the analysed cases, including key attributes relevant to the delisting process.

Non-financial characteristics of analysed cases

| Company name | Year of debut | Year of delisting | Age of company at IPO | Sector | Market capitalisation before tender offer | Share of controlling shareholder (%) | Nature of entity making tender offer | Reason for delisting |

|---|---|---|---|---|---|---|---|---|

| Ciech | 2005 | 2024 | 60 | Chemical | PLN 2.79 billion | 95.43 | Investor from outside the industry | Ability to respond more quickly and flexibly to changing conditions, facilitate decision-making, and reduce obligations and the scope of published information about the company |

| Polnord S.A. | 1999 | 2021 | 22 | Real estate development | PLN 335 million | 92.92 | Foreign industry entity | Implementation of the Cordia group’s strategy, restructuring of Polnord and consolidation of the group’s operations, which was not possible on the public market |

| STS Holding S.A. | 2021 | 2024 | 24 | Betting | PLN 3.88 billion | 99.28 | Foreign industry entity | Inclusion in the Entain group, which brings together entities from the industry |

| ‘Kruszwica’ Fat Works | 1997 | 2021 | 45 | Food | PLN 1.5 billion | 97.67 | Foreign industry entity | Acquisition by foreign industry player |

| Stelmet S.A. | 2016 | 2020 | 31 | Wooden furniture manufacturing | PLN 265.7 million | 95.37 | Polish investor | Investment in the company’s shares as a long-term investment by the caller |

| Arteria S.A. | 2006 | 2023 | 2 | Outsourcing services | PLN 40.13 million | 95.05 | Foreign industry entity | Acquisition by a foreign industry entity |

| TVN S.A. | 2004 | 2015 | 9 | Media entity | PLN 6.78 billion | 98.76 | Foreign industry entity | Acquisition by a foreign industry entity |

| Mieszko S.A. | 2000 | 2014 | 7 | Confectionery industry | PLN 161.42 million | 91.01 | Foreign investor from outside the industry | Acquisition by a foreign entity from outside the industry |

| Gekoplast | 2014 | 2018 | 47 | Packaging manufacturer | PLN 91.9 million | 99.3 | Foreign entity within the industry | Acquisition by a foreign entity within the industry |

| DZ Bank Polska | 1994 | 2011 | 5 | Bank | PLN 970.24 million | 99.87 | Foreign parent company | Complete acquisition by a foreign parent company |

IPOs, initial public offerings

The analysis also examined the behaviour of selected financial indicators: ROE, the P/E ratio, the price-to-book value (P/BV) ratio, the average trading volume, the free float and the tender offer premium.

ROE was tracked for the 5 years preceding delisting to assess each firm’s financial trajectory. Substantial variation in the indicator was recorded across the sample.

The P/BV ratio, defined as the share price divided by the book value per share, was the second indicator examined. A value below 1 indicates that the market values shares below their book value, signalling a weak financial position; 4 of the 10 firms exhibited P/BV ratios below 1.

The literature suggests that the presence of PE funds or investment companies in the shareholder structure raises delisting probability. Among the analysed firms, the shareholder structure included two investment funds and one PE fund. Two of these vehicles were associated with firms that delisted before 2015; however, given the limited number of cases, no strong inference can be drawn about whether this factor was more pronounced before that date.

Among firms that delisted within 5 years of their debut, negative average ROE was observed in the pre-delisting 5-year window. This pattern is consistent with a rapid managerial response to deteriorating financial conditions through strategic withdrawal from public trading, although the small number of such firms limits the strength of this inference.

The P/E ratio at the time of delisting also varied considerably across the sample. Adopting a conventional threshold of 10 to flag low market valuation, 3 of the 10 firms exhibited P/E values below this level, including Arteria S.A., which recorded a negative P/E reflecting sustained losses. The remaining seven firms exited at higher P/E levels, indicating that the relationship between market valuation and delisting cannot be reduced to a straightforward ‘low-valuation exit’ pattern. This heterogeneity motivates the introduction of a time-varying treatment of the P/E ratio in the quantitative analysis presented below.

As presented in Table 4, the cases varied substantially in their financial profiles, with both well-performing firms and firms in evident financial difficulty represented in the sample.

Financial characteristics of analysed cases

| Company name | P/E | P/BV | Average turnover | Free float | Premium in tender offer |

|---|---|---|---|---|---|

| Ciech | 7.6 | 1.1 | 2.802 million | 100% | PLN 53 06/11/2023 (2%) |

| 3,518,455 | 27.3% | ||||

| Polnord S.A. | 31.90 | 0.77 | 0.141 million | 100% | PLN 2.84 30/11/2021 (25%) |

| 2,494,653 | 18%–20% | ||||

| STS Holding S.A. | 22.58 | 13.22 | 2.624 million | 0% | PLN 24.6 04/10/2023 (1%) |

| 7,061,867 | 20%–25% | ||||

| ‘Kruszwica’ Fat Works | 22.60 | 1.8 | 0.464 million | PLN 65.8 26/02/2021 (1%) | |

| 442,785 | 18% | ||||

| Stelmet S.A. | 27.50 | 0.57 | 0.032 million | PLN 9.05 28/07/2020 (0%) | |

| 228,189 | 7% | ||||

| Arteria S.A. | -4.76 | 0.89 | 0.010 million | 2 | PLN 9.40 20/04/2023 (−5%) |

| 8,917 | 18% | ||||

| TVN S.A. | 36.7 | 6.9 | 5.817 million | 0% | PLN 19.92 22/09/2015 |

| Mieszko S.A. | 9.7 | 0.81 | 0.282 million | 0% | PLN 3.95 25/11/2014 |

| Gekoplast | 17.4 | 3.23 | 0.041 million | 0% | PLN 15.20 15/02/2018 |

| DZ Bank Polska | 32.7 | 2.67 | 66,331 | 0% | PLN 15.21 21/09/2010 |

P/BV, price-to-book value; P/E, price-to-earnings

The application of PSM produced the treated–control firm pairs presented in Table 5.

PSM matched pairs

| Study group company | Control group match | Industry sub-index |

|---|---|---|

| Ciech | Polwax S.A. | WIG-Chemia |

| Polnord S.A. | ATREM | WIG-Budownictwo |

| STS Holding S.A. | BOOMBIT | WIG-Gry |

| Zakłady Tłuszczowe ‘Kruszwica’ | PEPEES | WIG-Spożywczy |

| MIESZKO S.A. | ASTARTA | WIG-Spożywczy |

| Stelmet S.A. | KGHM | WIG-Górnictwo |

| TVN S.A. | PMPG | WIG-Media |

| Gekoplast S.A. | ODLEWNIE POLSKIE SA | WIG-Przemysł |

| DZ Bank Polska | SANPL | WIG-Banki |

| Arteria S.A. | PKP CARGO | Sektor Usługi Inne |

PSM, propensity score matching

The matched dataset was then used to estimate the Cox proportional-hazards model. The dependent variable is a time-to-event variable rather than a simple binary indicator of delisting, and the analysis employs a survival function that incorporates both the time until the event and the event status.

The explanatory variables included:

the absolute value of the average change in the ROE ratio (|ΔROE|);

the logarithm of total assets (log_Assets) as a proxy for company size;

the P/E ratio, serving as a measure of the company’s market valuation.

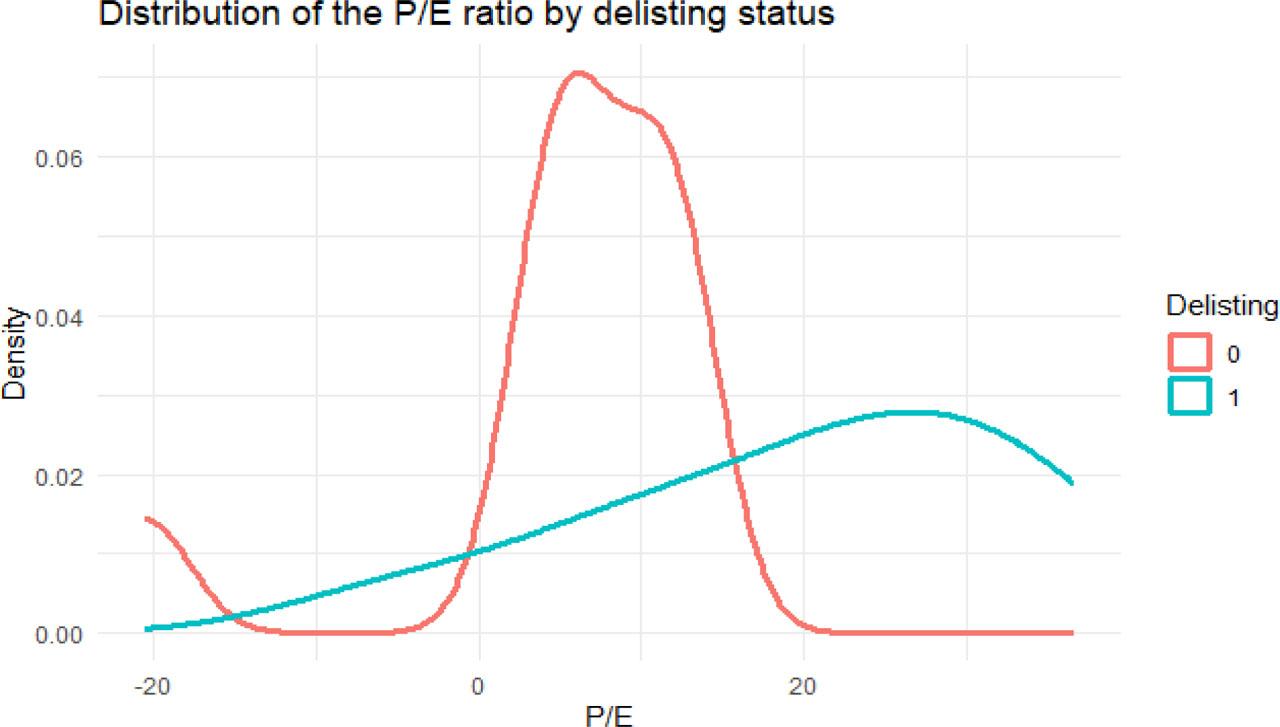

The first stage was an exploratory examination of the data. Figure 1 reports the distribution of the P/E ratio across delisted and non-delisted firms.

Distribution of the P/E ratio by delisting status. P/E, price-to-earnings

The visualisation indicates differences between the two groups and suggests that market valuation may be a relevant differentiating factor.

Three alternative Cox specifications were estimated. The first was the baseline specification with fixed (time-invariant) effects, which assumes that the impact of all variables is constant over time and that the proportional hazards assumption holds. In this specification, the P/E ratio was the only variable significant at conventional levels: a 1-standard-deviation increase in PE_std was associated with a more than fourfold increase in the estimated hazard of delisting. The change in ROE and firm size did not reach conventional significance, although firm size exhibited weak significance.

A critical limitation of the baseline specification was the violation of the proportional hazards assumption for the P/E ratio, confirmed by the Schoenfeld residuals test. This indicates that the effect of P/E is not constant over time, and the baseline specification therefore risks producing misleading interpretations.

For this reason, it was decided to alter the model specification. Next, a model with a time-varying effect for the P/E ratio was evaluated. This model allowed for the possibility that the impact of this variable changes as time progresses. For this purpose, an interaction function with time was introduced in the form of the product of the P/E variable and the natural logarithm of time.

The results indicate that the impact of the P/E ratio is statistically significant and time-dependent. The interaction coefficient is positive, meaning that the effect of P/E on the delisting hazard strengthens with listing tenure. In other words, high P/E values do not necessarily elevate short-term delisting risk, but sustained high P/E over longer periods is associated with a higher probability of delisting. This pattern is consistent with the market-timing and wealth-transfer mechanism articulated in Section 2.3: in markets with high ownership concentration, controlling shareholders may exploit sustained favourable valuation windows to execute exits, either through squeeze-out of minority shareholders or through transfer of the firm to a strategic acquirer at a premium.

In this specification, firm size also became statistically significant. The positive coefficient suggests that larger entities face a higher delisting hazard, which may reflect a higher propensity of large firms to undergo restructuring, mergers, acquisitions or strategic withdrawal from public markets. |ΔROE| remained statistically insignificant, suggesting that short-term fluctuations in profitability do not exert a decisive influence on delisting risk within the analysed sample.

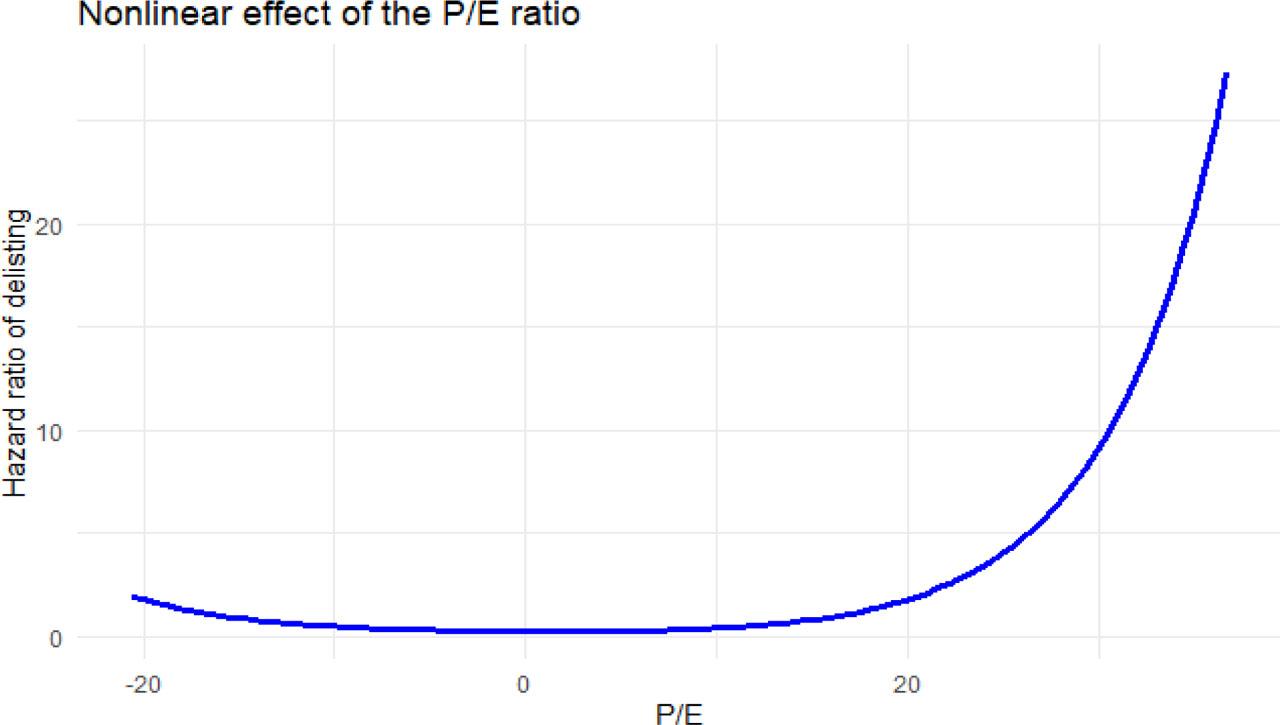

The third specification examined a non-linear effect of the P/E ratio, with the aim of capturing potential non-linearities in the relationship between valuation and the delisting hazard. The estimated relationship is illustrated in Figure 2.

Non-linear effect of the P/E ratio. P/E, price-to-earnings

The results point to a potentially complex, non-linear relationship; the estimates, however, are subject to a high degree of uncertainty, manifested in wide confidence intervals. This is most plausibly a consequence of the small sample size and the limited number of events, which constrain the stable estimation of more flexible specifications.

The proportional hazards assumption was verified using the Schoenfeld residuals test. Model goodness-of-fit was assessed using the Likelihood Ratio test, the Wald test, the Log-rank test and the concordance index (which measures the model’s ability to rank observations correctly by risk).

The comparison of the three specifications suggests that the best overall fit is achieved by the model with a time-varying effect for the P/E ratio, which adopts the following hazard specification:

This specification yields the highest concordance index in the sample (0.857), indicating a relatively strong discriminatory ability across firms with different delisting risks. The baseline specification, although it exhibits reasonable fit, violates the proportional hazards assumption and is therefore interpretatively unreliable. The non-linear specification, while theoretically more flexible, proves empirically unstable owing to the limited sample size.

The time-varying specification therefore offers the most defensible interpretation from both a statistical and an economic standpoint, given the data available. The parameter estimates and diagnostic test results are reported in Table 6.

Cox proportional-hazards model results (time-varying effect)

| coef | exp(coef) | e(coef) | z | pr(> |z|) | |

|---|---|---|---|---|---|

| |ΔROE| | −0.09926 | 0.90550 | 0.08936 | −1.111 | 0.26663 |

| log_ Assets | 0.64428 | 1.90462 | 0.30941 | 2.082 | 0.03732 |

| tt(P/E_std) | 1.06830 | 2.91041 | 0.37639 | 2.838 | 0.00454 |

| Concordance = 0.857 (se = 0.086) | |||||

| Likelihood ratio test = 17.41 | |||||

| Wald test = 8.69 | |||||

| Score (logrank) test = 14.96 | |||||

P/E, price-to-earnings

The WSE, operating since 1991, has experienced two pronounced waves of delisting since its inception: an initial wave between 2002 and 2003 and a more sustained second wave from 2019 onwards. The present study examines the determinants of voluntary delisting decisions during the latter period, drawing on a sample of 10 firms that exited the WSE between 2010 and 2024. The discussion below synthesises the qualitative cross-case findings (Section 5.1), the quantitative results (Section 5.2) and the limitations and exploratory implications of the analysis (Section 5.3).

The multiple cross-case study of 10 selected entities provided an exploratory foundation for testing the determinants of delisting in a post-socialist market context. The findings from this stage highlighted the distinct nature of the Polish market compared with developed economies. The results of the hypothesis verification are summarized in Table 7.

Summary of results

| Case | Short existence at IPO (<5 years) | Negative average ROE | Low P/BV (<1) | PE/investment company | Mature sector | Quick delist (<5 years) | High ownership (>90%) | Low P/E (<10) |

|---|---|---|---|---|---|---|---|---|

| Ciech | ✘ (60 years) | ✘ (0.17%) | ✘ (1.1) | ✘ | ✔ (chemical) | ✘ (19 years) | ✔ (95.43%) | ✔(7.6) |

| Polnord S.A. | ✘ (22 years) | ✔(−0.16%) | ✔(0.77) | ✘ | ✔(developer) | ✘ (22 years) | ✔ (92.92%) | ✘ (31.90) |

| STS Holding S.A | ✘ (24 years) | ✔ (−79.40%) | ✘ (13.22) | ✘ | ✔ (bookmaker) | ✔ (3 years) | ✔ (99.28%) | ✘ (22.58) |

| ‘Kruszwica’ Fat Works | ✘ (45 years) | ✘ (3.87%) | ✘ (1.8) | ✘ | ✔ (food) | ✘ (24 years) | ✔ (97.67%) | ✘ (22.60) |

| Stelmet S.A. | ✘ (31 years) | ✔ (−852.84%) | ✔(0.57) | ✔ (Investment Fund) | ✔ (manufacturing) | ✔ (4 years) | ✔ (95.37%) | ✘ (27.50) |

| Arteria S.A. | ✔ (2 years) | ✔ (−193.03%) | ✔(0.89) | ✘ | ✔ (services) | ✘ (17 years) | ✔ (95.05%) | ✔(−4.76) |

| TVN S.A. | ✘ (9 years) | ✘ (7.99%) | ✘ (6.9) | ✘ | ✔ (media) | ✘ (11 years) | ✔ (98.76%) | ✘ (36.7) |

| Mieszko S.A. | ✘ (7 years) | ✘ (5.88%) | ✔(0.81) | ✔ (Investment Company) | ✔ (food) | ✘ (17 years) | ✔ (91.01%) | ✔(9.7) |

| Gekoplast | ✘ (47 years) | ✘ (16.56%) | ✘ (3.23) | ✔ (PE) | ✔ (manufacturing) | ✔ (4 years) | ✔ (99.3%) | ✘ (17.4) |

| DZ Bank Polska | ✔ (5 years) | ✘ (5.16%) | ✘ (2.67) | ✘ | ✔ (bank) | ✘ (17 years) | ✔ (99.87%) | ✘ (32.7) |

IPOs, initial public offerings; P/BV, price-to-book value; P/E, price-to-earnings; PE, private equity; ROE, return on equity

The preliminary analysis allowed for the verification of the following patterns:

Ownership and Control: One of the most notable findings is the significance of high ownership concentration. All analysed entities reached the 90% ownership threshold by a single shareholder, facilitating the legal ‘squeeze-out’ process under Polish law (Act of July 29, 2005). This confirms that in transitioning markets, delisting is frequently driven by the strategic interests of dominant shareholders rather than broad market sentiment.

Financial Performance (ROE): The study confirmed that deteriorating financial health is a primary driver. A vast majority of the firms exhibited negative average ROE in the 5 years preceding delisting, supporting the thesis that sustained unprofitability encourages firms to leave the public market to reduce compliance costs and restructure privately.

Industry Maturity: All cases belonged to mature sectors with stable but slow growth rates. The limited need for further capital expansion in these industries often makes the costs of maintaining a public listing outweigh the benefits.

Other Factors: Interestingly, factors such as company age at IPO, listing duration, and the presence of PE funds were not found to be significant determinants in the Polish context. Unlike developed markets, where younger firms are often more prone to delisting due to failure, the Polish wave involved many established, former State Treasury companies where delisting resulted from privatisation or consolidation.

The second stage of the study utilised a Cox proportional-hazards model to rigorously test the three core hypotheses. The quantitative results provided a more nuanced perspective on market valuation. While the static case studies initially failed to confirm a clear link between low valuation and delisting, the time-dependent model revealed that the P/E ratio is a critical, time-varying determinant (HR = 2.91; p = 0.0045). This suggests that sustained undervaluation eventually triggers a strategic exit, as the market fails to reflect the firm’s perceived intrinsic value over time.

Furthermore, the model identified firm size (measured by total assets) as a significant factor, with larger firms exhibiting a higher hazard rate for delisting, potentially due to their attractiveness as targets for major restructuring or consolidation by international groups.

This research should be viewed as exploratory in nature. The study focuses primarily on the Polish market within a relatively narrow time horizon (2010–2024), which limits the generalisability of the findings to broader CEE markets. Most importantly, the small sample size (10 firms and 10 delisting events) imposes a significant constraint on the statistical power of the analysis and calls for particular caution in interpreting the results.

This limitation is especially relevant in the context of the Cox proportional-hazards models employed in the study. Given the small number of events, as well as the presence of non-linear specifications and time-varying effects, the estimated coefficients and hazard ratios should be interpreted as indicative rather than definitive. In particular, the results related to interaction terms and time-dependent effects may be sensitive to sample composition and model specification.

Despite these constraints, the study provides exploratory and multidimensional insights for various stakeholders:

For Investors: The identified patterns, particularly the combination of high ownership concentration and low P/E ratios, serve as a preliminary valuable early-warning system for squeeze-out risks, allowing minority shareholders to better assess the potential for mandatory buyouts at prices that may not satisfy long-term valuation expectations.

For Regulators: The findings underscore the need for enhanced protection of minority shareholders in post-transition markets, where high concentration and low liquidity can distort market mechanisms. Recommendations include ensuring more transparent valuation processes during tender offers.

For Researchers: This study highlights the necessity of using mixed-methods approaches to capture the dynamic and institutionally embedded nature of delisting in developing economies, paving the way for larger-scale comparative studies across the CEE region.