Figure 1.

Characteristics of R&D tax relief

| Characteristic | Number | % Share | Comments |

|---|---|---|---|

| low level of analysis of the presented data | 6 | 25% | |

| average level of analysis of the presented data | 8 | 33% | |

| high level of analysis of the presented data | 10 | 42% | |

| obligation to conduct R&D works and their commercialization | 13 | 54% | three countries easing this requirement |

| preliminary acceptance of works by external institutions | 7 | 29% | |

| Funding for RD works work | 24 | 100% | |

| Availability of other tax incentives for applying R&D work | 22 | 92% |

Recognition of costs included as production costs and elimination of intangible assets’ costs of production on their own

| Costs included in the cost of production | Costs not included in the cost of production |

|---|---|

|

|

General materiality criteria according to ACCA

| Balance Sheet Total | Sales Revenues | Gross Profit | Net Profit | |

|---|---|---|---|---|

| Overall Materiality Value | 1–2 % | 0.5–1.0% | 5% | 5–10% |

Summary of observations of conducted research

| Hypothesis | Dependent Variable | Group Membership | Sector Affiliation | Refief in Past | Refief in the Future | Chi-Square | DF | P-Value | Hypothesis Verification | V-Cramer |

|---|---|---|---|---|---|---|---|---|---|---|

| H1 | knowledge of balance sheet law | junior accountant | ||||||||

| senior accountant | ||||||||||

| chief accountant | ||||||||||

| management of the entity (management board, supervisory board) | ||||||||||

| H2 | knowledge of tax law provisions | junior accountant | ||||||||

| senior accountant | ||||||||||

| chief accountant | ||||||||||

| management of the entity (management board, supervisory board) | ||||||||||

| H3 | the need to create a new accounting standard for R&D works | services | ||||||||

| trade | ||||||||||

| production | ||||||||||

| other | ||||||||||

| H4 | tax inspection | Yes | 7.41 | 1 | 0.006 | confirmed | 0.568 | |||

| No | ||||||||||

| H5 | expenses questioned | Yes | 2.07 | 1 | 0.150 | rejected | ||||

| No | ||||||||||

| H6 | distortion of the financial statements | Yes | 0.873 | 1 | 0.350 | rejected | ||||

| No |

Descriptive statistics by R&D beneficiaries

| Survey Questionnaire | Detailing | Category | N | % |

|---|---|---|---|---|

| Q1 | Sector | services | 15 | 46.9 % |

| production | 5 | 15.6 % | ||

| trade | 6 | 18.8 % | ||

| other | 6 | 18.8 % | ||

| Q2 | Experience | 0–1y | 12 | 37.5 % |

| 1–4y | 9 | 28.1 % | ||

| 4–7y | 2 | 6.3 % | ||

| up to 7y | 9 | 28.1 % | ||

| Q3 | Position | Junior Accountant | 18 | 56.3 % |

| Senior Accountant | 6 | 18.8 % | ||

| Chief Accountant | 2 | 6.3 % | ||

| Managing Person | 6 | 18.8 % | ||

| Q4 | Relief in Past | No | 24 | 75.0 % |

| Yes | 8 | 25.0 % | ||

| Q5 | Since Relief | from 2020 | 1 | 12.5 % |

| from 2021 | 2 | 25.0 % | ||

| from 2022 | 2 | 25.0 % | ||

| earlier than 2020 | 3 | 37.5 % | ||

| Q6 | Economic Benefits | No | 5 | 15.6 % |

| Yes | 6 | 18.8 % | ||

| No opinion | 21 | 65.6 % | ||

| Q7 | Record | small extent | 19 | 59.4 % |

| enough | 3 | 9.4 % | ||

| good | 6 | 18.8 % | ||

| very well | 4 | 12.5 % | ||

| Q8 | Provisions of the Balance Sheet Law | Yes | 5 | 15.6 % |

| No | 5 | 15.6 % | ||

| difficult to determine | 22 | 68.8 % | ||

| Q9 | Standard | No | 12 | 37.5 % |

| Yes | 20 | 62.5 % | ||

| Q10 | Tax Law Provisions | Yes | 8 | 25.0% |

| No | 14 | 43.8% | ||

| difficult to determine | 10 | 31.3% | ||

| Q11 | Tax Inspection | No | 16 | 69.6 % |

| Yes | 7 | 30.4 % | ||

| Q12 | Claim Expenses | No | 18 | 81.8 % |

| Yes | 4 | 18.2 % | ||

| Q13 | Incorrect Expenses | No | 17 | 81.0 % |

| Yes | 4 | 19.0 % | ||

| Q14 | Tax Relief | No | 14 | 66.7 % |

| Yes | 7 | 33.3 % | ||

| Q15 | Manipulation of Financial Results | No | 16 | 80.0 % |

| Yes | 4 | 20.0 % | ||

| Q16 | Making a Correction | No | 11 | 84.6 % |

| Yes | 2 | 15.4 % | ||

| Q17 | Financial Statements Distortion | No | 12 | 70.6 % |

| Yes | 5 | 29.4 % | ||

| Q18 | Creative Accounting | No | 11 | 34.4 % |

| Yes | 21 | 65.6 % |

Comparison of the provisions contained in the Accounting Act and IAS regarding RD works works

| Specification | Accounting Act | IAS |

|---|---|---|

| item | cost of completed development work | cost of research work, cost of development work |

| method of recognizing expenditure on research work | no regulation – in accordance with Art. 10 section 3 of the Accounting Act possible reference to IAS | costs of a given period |

| method of recognizing expenditure on development works | activated as active accruals | costs of the period when they do not meet the definition of assets or are capitalized in intangible assets |

Research questions and hypotheses

| Hypothesis | Research Question | Linking to the Survey Questionnaire |

|---|---|---|

| H1 | Q1 | 3 and 8 |

| H2 | Q2 | 3 and 10 |

| H3 | Q3 | 1 and 9 |

| H4 | Q4 | 4 and 11 |

| H5 | Q5 | 4 and 12 |

| H6 | Q6 | 14 and 17 |

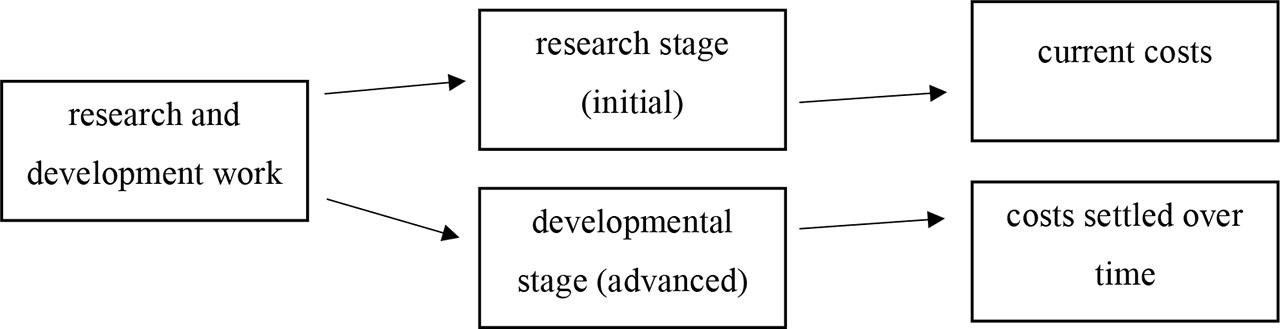

Characteristics of RD works

| Research works | Development works |

|---|---|

|

|