In the Polish economy, the sectors of micro, small and medium-sized enterprises are developing dynamically despite the numerous challenges in recent years including the COVID-19 pandemic, issues with the component availability, parts for the production of machines, cars, inflation, and other factors (Łupicka & Konecka, 2022). Currently, these enterprises constitute over 99% of business units operating in Poland. Competition among these entities is very high, prompting their managers to look for innovative solutions and utilize Research and Development works (RD works) activities to optimize finances and taxes (Hołda & Łojek, 2022).

RD works provide ample room for maneuvering and manipulating accounting data. Several factors may contribute to this state of affairs, ranging from understatement or overstatement of the financial result. Consequently, the monetary value of data on the balance sheet or entities may make numerous attempts to create financial and tax benefits resulting from tax laws.

The article examines the current perception of RD works by accountants and managers. It may serve as a foundation for further research in the area, assuming a larger research sample is utitlized.

The aim of this article is to test research hypotheses through a chi2 independence test to assess the need to create a new national accounting standard for RD works and the level of respondents’ knowledge about balance sheet and tax law. The article also raises issues related to potential questioning of the costs of RD works. The assumed issues led to the formulation of the following research questions:

Q1: Is there a relationship between the group of individuals representing the entity’s accounting in the research sample and the level of understanding of the provisions of accounting law regarding RD works? Q2: Is there a relationship between the group of individuals representing the entity’s accounting in the research sample and the level of understanding of tax law provisions in the field of RD works? Q3: Is there a statistically significant relationship between membership in a given group representing an entity’s accounting in the research sample and the need to create a new national accounting standard for RD works? Q4: Is there a statistically significant relationship between the use of RD works tax reliefs and the risk of audits by fiscal institutions? Q5: Is there a statistically significant relationship between the use of RD works tax reliefs and the risk of control by co-financing institutions building assets? Q6: Is there a statistically significant relationship between performing RD works and the tendency to manipulate financial results?

The authors test the research hypotheses presented below based on these research questions. To achieve this, chi-square tests of independence were conducted, with the questions included in the survey questionnaire available upon request to the authors of the article.

H1: Groups representing the entity’s accounting differ from each other in the level of understanding of the provisions of the balance sheet law in the field of RD works. H2: Groups representing the entity’s accounting differ from each other in the level of understanding of tax law provisions in the field of RD works. H3: There is a statistically significant relationship between belonging to a group representing the entity’s accounting and the need to create a new national accounting standard in the field of RD works. H4: There is a statistically significant relationship between the use of tax reliefs in the field of RD works and the risk of control by fiscal institutions. H5: There is a statistically significant relationship between the use of tax reliefs in the field of RD works and the risk of control by co-financing institutions building assets. H6: There is a statistically significant relationship between the performance of RD works and the tendency to manipulate the financial results.

The article consists of both a theoretical and empirical part. At the end of the study, the authors included a list of questions and possible answers that were posed to the respondents. This article utilized an anonymous online survey to collect research results. The survey was conducted online and sent to accountants from various sectors, as well as to the authors’ students.

Observations were conducted from May 2023 to the end of February 2024. Requests to complete surveys were sent to approximately 100 people included in the research sample, but only 32 people responded, which constitutes 32% of observations.

The analyzed issue has been the subject of interest of the authors (Annique, Cuervo-Cazurra & Asakawa, 2010; Becker & Dietz, 2004; Hołda & Łojek, 2022, 2023; Kalka, 2013; Kleinknecht & Rejinen, 1992; Klimczak, 2012; Merrifield, 2015; Mishra, 2011; Okamuro, 2007; Oktaba & Grzywińska-Rąpca, 2023; Piekut, 2012; Piersiala, 2014; Surmacz & Garata, 2014; Tokarski, 1994; Wasiluk & Białek-Jaworska, 2020). Furthermore, based on the authors’ experiences, statutory auditors examine the expenditure incurred by enterprises on RD works. All authors agree on the conclusion of the studies that RD works have a positive impact on the entrepreneurship of business entities and also improves the quality of products manufactured in innovative ways, compared to traditional methods.

The concept of RD works activities is quite broad. In simple terms, it is a production activities that encompass scientific research and/or development work conducted in a systematic manner. (Act, 1991). Its primary goal is to create an innovative solution or a needed item that is not yet available, often serving as a prototype. Conducting RD works in business entities increases their intellectual capital (Kwiecień & Piotrowska, 2007). However, RD works work are sometimes abandoned at the final stage for financial reasons, such as the inability to complete the project for economic reasons.

Scientific research, in its simplest terms, refers to exploratory, experimental or theoretical work that is aimed at acquiring new knowledge (Act, 1992; Act, 1991). Development works benefit from the acquired knowledge because as they extend the research stages. During them, the discovered and innovative technology is developed after the discovery work is completed.

According to the definition of the Central Statistical Office (GUS), RD works encompass all activities (development, financial, commercial) undertaken by an enterprise with the aim creating innovative technology (Frascati Book, 2015). This definition also covers RD works activities conducted by an enterprise, regardless of its purpose. The abbreviation used refers to the RD works relief used in Poland.

There is no definition of RD works in Polish balance sheet law, i.e. in the Accounting Act and KSR. However, it is approximated by International Accounting Standard (IAS) 38, “intangible Assets”. In this international standard, research is defined as the search for new solutions combined with the simultaneous acquisition of technical and scientific knowledge. Development works is the practical application of discoveries resulting from previous research. Therefore, two stages can be distinguished: initial and advanced, for RD works, respectively. The characteristics of these works are presented in Table 1.

Characteristics of RD works

| Research works | Development works |

|---|---|

|

|

Source: own study based on Hołda & Łojek, 2022

Pursuant to IAS 38, if an entity is unable to determine whether a given stage concerns research or development work, it should be assumed that all expenditures were incurred solely for research purposes. Table 3 presents the main differences between the provisions of the Accounting Act and IAS in the field of RD works. Pursuant to the Accounting Act, Article 10 Section 3, entities applying Polish balance sheet law may apply the provisions of IAS in the absence of solutions in the Accounting Act.

Comparison of the provisions contained in the Accounting Act and IAS regarding RD works works

| Specification | Accounting Act | IAS |

|---|---|---|

| item | cost of completed development work | cost of research work, cost of development work |

| method of recognizing expenditure on research work | no regulation – in accordance with Art. 10 section 3 of the Accounting Act possible reference to IAS | costs of a given period |

| method of recognizing expenditure on development works | activated as active accruals | costs of the period when they do not meet the definition of assets or are capitalized in intangible assets |

Source: own work based on Hołda, 2022

Although the basic normative act, the Accounting Act, does not define the concept of RD works, it can be found in the Higher Education Act (Act, 2018). It also states that scientific research is an activity that includes:

- 1)

basic research understood as empirical or theoretical work aimed primarily at acquiring new knowledge about the basis of phenomena and observable facts without direct commercial application,

- 2)

applied research understood as work aimed at acquiring new knowledge and skills, aimed at developing new products, processes, or services or introducing significant improvements to them.

Development works—in accordance with the above-mentioned normative act—is an activity involving the acquisition, combination, shaping, and use of currently available knowledge and skills, including in the field of IT tools or software, for planning production and designing and creating changed, improved or new products, processes or services, excluding activities that involve routine and periodic changes thereto, even if such changes are of the nature of improvements.

The approach to RD works presented so far included an approach to the issue from the perspective of balance sheet law (Accounting Act, IAS, US GAAP). However, the legislator in Poland also recognizes a tax approach in the form of a relief called R&D works, where the taxpayer can obtain a tax benefit of up to 200% of the possible deduction and thus recognize “tax costs,” which, in principle, result in a reduction of the tax liability (fiscal burden).

Globally, it is also possible to benefit from RD works relief. For example, a comparison of 24 countries from different continents shows that 25% of them are assessed as having a relatively low level of analysis of the presented data. Conversely, 10 countries from this sample are rated as having a very high level of review of the data presented. Poland was classified in the first of the mentioned groups. More than half of the analyzed sample assumes that all RD works must be carried out in a given country, as well as the commercialization of their results. Pre-approval is required in only 7 countries out of the analyzed research sample. Selected data are presented in Table 3.

Characteristics of R&D tax relief

| Characteristic | Number | % Share | Comments |

|---|---|---|---|

| low level of analysis of the presented data | 6 | 25% | |

| average level of analysis of the presented data | 8 | 33% | |

| high level of analysis of the presented data | 10 | 42% | |

| obligation to conduct R&D works and their commercialization | 13 | 54% | three countries easing this requirement |

| preliminary acceptance of works by external institutions | 7 | 29% | |

| Funding for RD works work | 24 | 100% | |

| Availability of other tax incentives for applying R&D work | 22 | 92% |

Source: own study based on Tax Credits for RD works, company guide Ayming; https://www.ayming.pl/analizy-i-aktualnosci/raporty/ulga-br-malymi-krokami-do-wiekszej-innowacyjnosci/, Warsaw 2022, access date: 7.01.2024

External institutions provide funding for RD works, with the highest values estimated among European countries and the lowest in Australia. Interestingly, it is worth emphasizing that as many as 92% of the analyzed countries attempt to encourage taxpayers to launch and commercialize the results of the mentioned effects of RD works through various tax incentives.

The concept of innovative activity also has a broader definition, it includes RD works activities, engineering and design work, marketing activities related to intellectual property, employee training, software development, and the purchase and lease of tangible assets, as well as innovation management. Innovative activity may end in success (it is postponed), be discontinued (without the intention to continue), or be continued (Barge-Gil & Lopez, 2014).

Deception can be defined as knowingly misleading someone to gain personal benefits (Polish dictionary, 2024). Accounting also distinguishes the possibility of fraud in cases of theft and embezzlement of data in financial statements, which can lead to tangible benefits from the perspective of stakeholders (Łojek, 2021). The aforementioned issues have been the subject of research by many authors (Andrzejewski, 2016; Argenti, 1976; Hołda, 2020; Hołda, 2006; Jurkowska-Zeidler, 2020; Łojek, 2021; Maćkowiak, 2015; Parker, 1995; Rutkowska-Tomaszewska, 2020; Wells, 2002; Wiktorow & Monkiewicz, 2020; Wójtowicz, 2010; Zack, 2009).

Accounting manipulation is defined as: “taking advantage of the trust, loyalty or ignorance of an individual (group) to gain full control over it in an unnoticeable way and achieve one’s own goals” and as “one of the techniques of exercising power; inducing or provoking an individual (group) to take specific actions in good faith, and then, by discrediting them, discredit the individual (group) in the eyes of public opinion and use it to achieve one’s own political benefits” (PWN, 2024). This definitione may seem somewhat trivial but is reflected in everyday economic life as accounting fraud.

Research conducted in 2010–2020 by ACFE (Association of Certified Fraud Examiners) proved that the most common type of fraud is misappropriation of assets—over 80% of cases, while falsification of financial statements alone did not exceed 10% of frauds (ACFE, 2010, 2012, 2014, 2016, 2018, 2020).

However, it all depends on the level of materiality that affects the financial situation in the eyes of stakeholders (Micherda, 2010). Table 4 presents the materiality criteria according to the Association of Chartered Certified Accountants (ACCA). The general level of materiality should be included in the accounting policy of the economic entity (Stępień, 2019). When setting this level, you should use common sense so that the company does not make profits and maintains an appropriate level of financial liquidity (Łojek, 2021). There are instances when a negative financial result does not affect cash flow (Wędzki, 2021).

General materiality criteria according to ACCA

| Balance Sheet Total | Sales Revenues | Gross Profit | Net Profit | |

|---|---|---|---|---|

| Overall Materiality Value | 1–2 % | 0.5–1.0% | 5% | 5–10% |

Source: Łojek, 2020

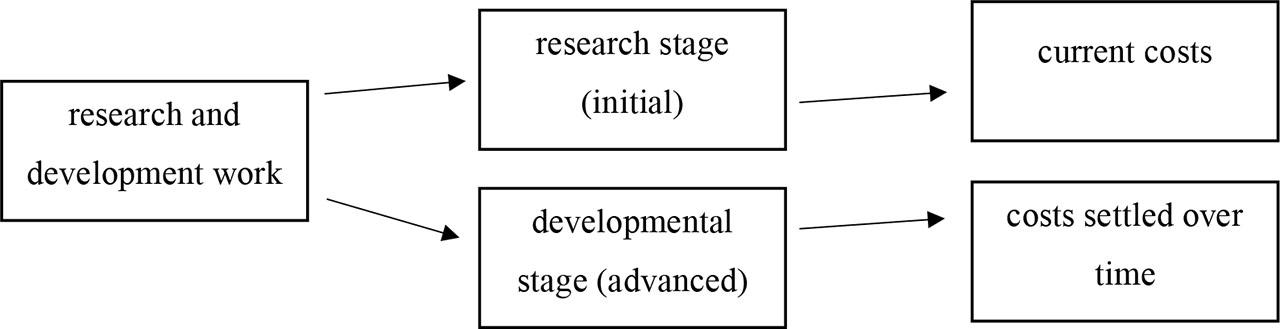

RD works work in accounting records

Source: own study

However, a creative approach to RD works can also be recognized. This issue should be understood as conduct within the limits of the law (Micherda, 2012). The aforementioned creative (positive) accounting means innovative use of knowledge and acquired skills (Łojek, 2021).

If an entity wants to start RD works activities, it should appropriately modify the provisions of its accounting policy and supplement them with provisions regarding RD works activities (Stępień, 2019). The basic categories include: measurement, valuation, presentation in financial statements, procedures for identifying ongoing projects, and the rules for making depreciation write-offs. These provisions should be applied continuously (Piotrowska, 2008).

As mentioned earlier, the Accounting Act does not directly define the concept of RD works; however, when analyzing its provisions, attention should be paid to the accounting records of RD works. Figure 1 illustrates the accounting treatment of the discussed issue. Costs incurred in the initial stage are the costs of current reporting periods, costs incurred in the advanced stage—development work—should be settled over time, and therefore suspended on the accounts of Team 6 (active accruals) in correspondence with the accounts of other teams in the chart of accounts. Due to the nature of research costs, these are not amortized over time (Act, 1994).

According to the Accounting Act, the costs of successfully completed development works (commercialization, sale, use for internal needs) should be classified as intangible assets. It should be noted here that this approach is recommended when the production or use of the technology has not previously occurred, the cost value has been estimated reliably, and the costs incurred will be covered by revenues from the sale of the product or implementation of the technology.

The positive result of completed development work should also be recognized and recorded in the balance sheet as intangible assets for the entity when the following conditions are met:

- 1)

the product or production technology is precisely determined and the development costs related to it are reliably determined,

- 2)

the technical suitability of the product or technology has been adequately documented by the taxpayer and, on this basis, the taxpayer has made a decision to produce these products or use the technology,

- 3)

the documentation regarding development works shows that the costs of development works will be covered by the expected revenues from the sale of these products or the use of technology.

When the intended economic benefit is achieved, the expenditure accumulated in the accruals account is reclassified to intangible assets. Accounting involving cost reduction and activation of intangible assets should be conducted through internal turnover accounts to tighten the cost circle. At this point, there is no longer a need to maintain detailed accounts for the project because, as mentioned, it has been completed. The unit can only keep records according to the cost center.

Documentation of completed development work should include a precise description of: how the product or technology was created; proof of the technical suitability of the created product or technology, e.g., by indicating the group of potential recipients for these products; estimating the expected profits from sales using the new technology; indicating the method of assigning given costs to activated costs of completed development works resulting from the component documents (salaries, depreciation, expenditure of materials) (Ball, Thomas & Grath, 1991, Canage, Jackson, Ma & Zimberlman, 2022).

If a decision is made to activate development works, the costs of their implementation using own or external resources until their completion are initially collected on analytical accounts regarding active settlements of accrued costs. If the costs of development work are not expected to be activated, the costs of these works are charged to current costs and affect the financial result for the period. After the development work has been completed and it has been determined that they have brought results, and the production of new or significantly improved products or the use of new or significantly improved technologies to which the work relates will be implemented on an industrial scale, the values accumulated on the analytical accounts of active prepayments are transferred to the accounts intangible assets—in the amount of the production costs of works performed using own resources or the actual costs of purchasing works performed using external resources (possible recoveries and costs covered by the subsidy must be reduced).

The mentioned subsidies in the form of subsidies are posted to accounts relating to deferred income (in Poland, most often according to Set 8 of the company’s chart of accounts) and are settled in proportion to the expenditure incurred during development work before the decision is made to complete or, in the event of sucessful project completion, are accepted as an intangible asset on the balance sheet. The postings should be proportionally written off as revenues in parallel with the asset’s amortization in the following years in accordance with the principle of matching.

The provisions of IAS 38 clearly state that an intangible asset resulting from development work may be recognized only if the entity is able to prove (IAS 38):

- 1)

the technical feasibility of completing the intangible asset in such a way that it is suitable for use or sale,

- 2)

the intention to complete a given asset or prepare it for sale,

- 3)

ability to use or sell the ingredient,

- 4)

how the asset will be able to generate future economic benefits, including: prove the existence of market needs for the products created thanks to the mentioned ingredient, or for the ingredient itself,

- 5)

availability of technical, financial and other means used to complete development work as well as to use or sell the intangible asset,

- 6)

the possibility of reliably determining the expenditure incurred during development work that can be attributed to this intangible asset.

During the implementation of development works, the entity is often unable to determine whether it will be successful and, consequently, whether the costs will be activated in the balance sheet. The costs of RD works that do not fully or partially meet the conditions for their activation, whether carried out using the entity’s own resources or external, are written off against other operating costs or the cost of products sold.

It should be added that US GAAP standards do not require the separation of RD works (current and capitalized costs) but require the recognition of all expenses incurred for ongoing activities as current costs.

An entity should disclose the total RD works expenditure recognized during the accounting period as an expense in the profit and loss account on an accrual basis. Moreover, the provisions of the basic normative act of Polish accounting law, which is the Accounting Act, specify that the costs of completed development works are valued at the actual incurred costs related to the construction of new or improved products and production technologies. Typically, they include:

- 1)

remuneration of employees involved in development work;

- 2)

costs of materials and services used in the course of development work;

- 3)

depreciation of tangible fixed assets in the part corresponding to their use during development works. It should be emphasized that the entity should reliably determine the settlement keys to ensure the reliability of the data and determine the extent to which a given asset was used for RD works purposes.

The cost of internally generated intangible assets includes all expenses that can be directly attributable to the activities of designing, creating, producing, testing, and adapting the asset for use in the manner intended by management. Expenditures are recognized in the value of an asset from the moment it meets the recognition criteria for development work until it is in a condition that allows it to be used in accordance with management’s intentions (despite the lack of use or no decision to use it). Table 5 shows the costs that can be included in the manufacturing cost and those that cannot be classified as manufacturing costs.

Recognition of costs included as production costs and elimination of intangible assets’ costs of production on their own

| Costs included in the cost of production | Costs not included in the cost of production |

|---|---|

|

|

Source: own study

To properly verify the presented data, the entity should conduct reconciliation work. The entity should adopt and implement internal procedures that will verify the proper classification of costs in addition to the aforementioned separate accounting records and the adopted appropriate provisions of the accounting policy.

In a situation where an entity obtains funding for RD works, it is relatively simple to analyze the level of funding in relation to the expenditures incurred. For this purpose, it is necessary to annex the accounting policy, open a new synthetic account, and, as a result of the horizontal division of accounts, make appropriate analytical entries, based on accounting evidence.

Salary costs may cause minor difficulties in estimating the actual working time of employees in relation to the total working hours of a given individual. In other words, an economic entity conducting RD works should keep additional records showing the actual working time spent in the settlement period. It should be emphasized that this condition applies to employees closely related to the RD works project. From the perspective of the institution controlling the progress of work, these records may affect the amount of funding approved for payment.

The research sample consisted of observations in one hundred entities applying the provisions of accounting law in the field of RD works. These entities primarily belonged mainly to the production sector, specifically economic units producing certain goods. The survey was targeted employees of accounting departments responsible for the accounting of the above-mentioned entities and managers. Only 32% of respondents participated, resulting in 32 observations being collected. The research was conducted from May 2023 to the end of February 2024. An online survey was created and made available to a group of 100 accountants and managers of enterprises related to the entity’s accounting. The questions asked were included in the Appendix.

This article employs research methods such as the chi2 independence test, statistical analysis, criticism of the literature, scientific research results, and statistical inference.

A statistical analysis of the survey responses was performed, as shown in Table 6.

Descriptive statistics by R&D beneficiaries

| Survey Questionnaire | Detailing | Category | N | % |

|---|---|---|---|---|

| Q1 | Sector | services | 15 | 46.9 % |

| production | 5 | 15.6 % | ||

| trade | 6 | 18.8 % | ||

| other | 6 | 18.8 % | ||

| Q2 | Experience | 0–1y | 12 | 37.5 % |

| 1–4y | 9 | 28.1 % | ||

| 4–7y | 2 | 6.3 % | ||

| up to 7y | 9 | 28.1 % | ||

| Q3 | Position | Junior Accountant | 18 | 56.3 % |

| Senior Accountant | 6 | 18.8 % | ||

| Chief Accountant | 2 | 6.3 % | ||

| Managing Person | 6 | 18.8 % | ||

| Q4 | Relief in Past | No | 24 | 75.0 % |

| Yes | 8 | 25.0 % | ||

| Q5 | Since Relief | from 2020 | 1 | 12.5 % |

| from 2021 | 2 | 25.0 % | ||

| from 2022 | 2 | 25.0 % | ||

| earlier than 2020 | 3 | 37.5 % | ||

| Q6 | Economic Benefits | No | 5 | 15.6 % |

| Yes | 6 | 18.8 % | ||

| No opinion | 21 | 65.6 % | ||

| Q7 | Record | small extent | 19 | 59.4 % |

| enough | 3 | 9.4 % | ||

| good | 6 | 18.8 % | ||

| very well | 4 | 12.5 % | ||

| Q8 | Provisions of the Balance Sheet Law | Yes | 5 | 15.6 % |

| No | 5 | 15.6 % | ||

| difficult to determine | 22 | 68.8 % | ||

| Q9 | Standard | No | 12 | 37.5 % |

| Yes | 20 | 62.5 % | ||

| Q10 | Tax Law Provisions | Yes | 8 | 25.0% |

| No | 14 | 43.8% | ||

| difficult to determine | 10 | 31.3% | ||

| Q11 | Tax Inspection | No | 16 | 69.6 % |

| Yes | 7 | 30.4 % | ||

| Q12 | Claim Expenses | No | 18 | 81.8 % |

| Yes | 4 | 18.2 % | ||

| Q13 | Incorrect Expenses | No | 17 | 81.0 % |

| Yes | 4 | 19.0 % | ||

| Q14 | Tax Relief | No | 14 | 66.7 % |

| Yes | 7 | 33.3 % | ||

| Q15 | Manipulation of Financial Results | No | 16 | 80.0 % |

| Yes | 4 | 20.0 % | ||

| Q16 | Making a Correction | No | 11 | 84.6 % |

| Yes | 2 | 15.4 % | ||

| Q17 | Financial Statements Distortion | No | 12 | 70.6 % |

| Yes | 5 | 29.4 % | ||

| Q18 | Creative Accounting | No | 11 | 34.4 % |

| Yes | 21 | 65.6 % |

Source: own study

The table above presents the results of a survey on various aspects of the accountants’ work, including their sectors, experience, positions and opinions on various tax practices and regulations. The first part of the table shows the distribution of respondents by the sector in which they work. The largest group comprises accountants working in the services sector (46.9%), while the remainder are distributed among production (15.6%), trade (18.8%), and other sectors (18.8%). In terms of professional experience, most respondents have 0 to 1 year of experience (37.5%), while the rest have 1 to 4 years (28.1%), 4 to 7 years (6.3%), and over 7 years (28.1%).

The second part of the table focuses on the positions held by respondents. Most of them were junior accountants (56.3%), while a smaller number were senior accountants (18.8%), chief accountants (6.3%), and managers (18.8%). The table also analyzes whether respondents took advantage of tax breaks, with 75% responding affirmatively. Moreover, the survey examines how long they have been using tax breaks, with responses divided among different years; the largest group of respondents declared tax breaks before 2020 (37.5%).

The last part of the table includes respondents’ opinions on economic benefits, quality of record keeping, knowledge of balance sheet regulations, tax standards, and tax inspections. For example, 65.6% of respondents have no opinion on the economic benefits, and 68.8% have difficulty identifying the balance provisions. The table also contains data on declaring and manipulating financial results, with most respondents indicating that they do not engaged in such practices. Moreover, 65.6% of respondents admit to using creative accounting. Overall, the table provides a comprehensive insight into the practices and opinions of accountants regarding various aspects of their work.

Such behaviour may results from the lack of transparent solutions developed by the creative accounting system in this context. The authors recognize the need to create certain solutions, but this is an issue for a separate study.

The connection between research questions and hypotheses, as well as questions from the survey questionnaire, is presented in Table 7.

Research questions and hypotheses

| Hypothesis | Research Question | Linking to the Survey Questionnaire |

|---|---|---|

| H1 | Q1 | 3 and 8 |

| H2 | Q2 | 3 and 10 |

| H3 | Q3 | 1 and 9 |

| H4 | Q4 | 4 and 11 |

| H5 | Q5 | 4 and 12 |

| H6 | Q6 | 14 and 17 |

Source: own study

The results obtained are summarized in Table 8. To better illustrate these results, subsequent cross-tabulations present the individual questions and research hypotheses. Below the table, there is a description of each hypothesis along with the authors’ comments.

Summary of observations of conducted research

| Hypothesis | Dependent Variable | Group Membership | Sector Affiliation | Refief in Past | Refief in the Future | Chi-Square | DF | P-Value | Hypothesis Verification | V-Cramer |

|---|---|---|---|---|---|---|---|---|---|---|

| H1 | knowledge of balance sheet law | junior accountant | ||||||||

| senior accountant | ||||||||||

| chief accountant | ||||||||||

| management of the entity (management board, supervisory board) | ||||||||||

| H2 | knowledge of tax law provisions | junior accountant | ||||||||

| senior accountant | ||||||||||

| chief accountant | ||||||||||

| management of the entity (management board, supervisory board) | ||||||||||

| H3 | the need to create a new accounting standard for R&D works | services | ||||||||

| trade | ||||||||||

| production | ||||||||||

| other | ||||||||||

| H4 | tax inspection | Yes | 7.41 | 1 | 0.006 | confirmed | 0.568 | |||

| No | ||||||||||

| H5 | expenses questioned | Yes | 2.07 | 1 | 0.150 | rejected | ||||

| No | ||||||||||

| H6 | distortion of the financial statements | Yes | 0.873 | 1 | 0.350 | rejected | ||||

| No |

Source: own study

The first research question related to the verification of the first hypothesis is: Is there a relationship between the group of people representing the entity’s accounting and the level of understanding of the provisions of the balance sheet law in the field of RD works?

To verify the first hypothesis, a chi-square test of independence was performed. The test results indicate that there is no statistically significant relationship between experience and knowledge of the provisions of the balance sheet law: chi2 (6 = 2.67; p = 0.849), which means that this hypothesis should be rejected.

One might argue that greater attention needs to be paid to the detailed provisions of the balance sheet law, as the Act on Accounting Act itself only briefly signals the existence of RD works. However, it should be noted that this issue is described in greater detail in IAS regulations, specifically IAS 38. From the author’s experience, few individuals utilize these standards, and many mistakenly believe that the provisions of the balance sheet law are limited to the Accounting Act. This observation be serve as an impetus for further research by the authors in this area.

Ultimately, the aforementioned approach of accountants to balance sheet law in Poland may vary and depends on many factors; however, it can be expected that accountants will appreciate its importance for the reliability and transparency of financial statements while attempting to cope with its complexity and variability.

The second research question that can be asked in connection with the verification of the first hypothesis is: Is there a relationship between the group of people representing the entity’s accounting and the level of understanding of tax law provisions in the field of RD works? Therefore, a research hypothesis regarding the examined relationships was formulated.

In order to verify the second hypothesis, a chi-square test of independence was performed. The test results indicate that there is no statistically significant relationship between experience and knowledge of tax law provisions: chi2 (3 = 4.25; p = 0.236), which means that this hypothesis should also be rejected.

As in the case of the previously tested hypothesis, no relationship between the variables was demonstrated here. While there are no similar studies in the literature, this result should be considered unsurprising; according to the authors of the article, if a person does not understand the solutions provided by accounting law in the field of RD works, it will be difficult to navigate the tax regulations, not to mention knowledge required regarding legal solutions or the possibilities of obtaining financing for the relevant RD works.

Indeed, knowledge of tax law is as important as knowledge of balance sheet law, even for individuals just starting work in financial and accounting departments (Wolff & Reinthaler, 2008). The constant changeability of regulations, the addition of subsequent paragraphs and points do not facilitate the education of the above-mentioned groups in this area.

It should be emphasized, however, that the solutions of the balance sheet law are stable in the context of RD works (Becker, 2014). This includes recognition, valuation, records, and presentation. The situation is slightly different in tax law. On average, new provisions appear every year, but certain aspects remain unchanged, such as the right to use a tax relief. This, in turn, is quite complicated for individuals just starting their careers in finance and accounting departments. It should be added that from January 1, 2022, the Polish tax system allows for additional tax relief related to the relief for RD works (Hołda & Łojek, 2023).

The issue of RD works in business practice is not common. The authors anticipated this result from the test of the previously formulated hypotheses.

Continuing, the third research question was posed: Is there a statistically significant relationship between membership in a given group representing an entity’s accounting and the need to create a new national accounting standard for RD works?

In order to verify the third hypothesis, a chi-square test of independence was performed. The test results indicate that there is no statistically significant relationship between the sector and the need to create a new accounting standard: chi2 (3 = 1.56; p = 0.667). This hypothesis is rejected.

So far, authors in the literature have not examined the relationship between the two mentioned variables, so it is difficult to refer to historical data. Only the authors can indicate the desired direction of development of the mentioned issue by accountants. Their experience shows that accountants signal the need to create a new, national accounting standard for RD works works. However, the problem lies in the accountant’s lack of awareness regarding the existence of IAS 38, which details the issue analyzed in the article. This situation may be due to the fact that this standard does not explicitly indicate that it pertains to RD works in its title (“intangible assets”).

However, the results of the research conducted by the authors indicate that, regardless of the sector, there is no need to create a new accounting standard in terms of valuation, recognition, and presentation of RD works.

According to the authors of the study, this result is relatively surprising, because if the respondents show no correlation between their knowledge of balance sheet law in this context, they should signal a greater need to create the necessary accounting standard. Consequently, another new standard could be introduced, perhaps more extensive than the previously mentioned IAS 38, incorporating more detailed aspects.

Independently, the authors decided to formulate the fourth research hypothesis regarding the use of tax relief for R&D works and the frequency of inspections by tax authorities. Therefore, the fourth research question was posed: Is there a statistically significant relationship between the use of tax reliefs in the field of RD works and the risk of control from fiscal institutions?

To verify the fourth hypothesis, a chi-square test of independence was performed. The test results indicate that there is a statistically significant relationship between the use of the relief and the risk of control by fiscal institutions (tax audit): chi2 (1 = 7.41; p = 0.006). The value of the V-Cramer statistic indicates a moderate strength of the relationship; CV = 0.568. This hypothesis should be accepted. Unfortunately, it was not possible to find a reference point for the conducted research in the literature.

Economic practice shows that almost always, when an enterprise takes advantage of any income tax relief, tax control by fiscal institutions always occurs. It can be conducted remotely or at the taxpayer’s office.

Tax audit is a process in which tax authorities analyze and verify the compliance of financial data and tax payments declared by taxpayers with the provisions of tax law (Dinh, Sidhu, & Yu, 2019). It may have various causes such as reported irregularities, random selection, risk analysis, lack of consistent data in the files submitted, or suspicion of income concealment (Zalewski, 2021).

Similarly, the hypothesis regarding the relationship between the use of tax relief and the occurrence of questionable expenses by the institution co-financing the construction of the asset could be verified. Therefore, a fifth research question should be posed: Is there a statistically significant relationship between the use of tax reliefs in the field of RD works and the risk of control from co-financing institutions building assets?

To verify the fifth hypothesis, a chi-square test of independence was performed. The test results indicate that there is no statistically significant relationship between the use of tax reliefs in the field of RD works and the occurrence of expenses that need to be questioned by the institution co-financing the construction of the assets: chi2 (1 = 2.07; p = 0.150). It is advisable to reject this hypothesis.

The research conducted indicates that the respondents have little knowledge of the provisions of accounting and tax law regarding RD works. In the light of previous observations, the result of the fifth test of independence of the indicated variables is surprising from the authors’ perspective.

As mentioned, these institutions primarily focus on obtaining funds for asset construction; however, in addition to this function, they are expected to maintain proper accounting records, including tax records.

It would seem that a low level of knowledge of accounting and tax law solutions would result in questionable expenses. However, the result is contrary to what was expected. Therefore, it can be concluded that these institutions fulfill their function, and that accounting people are good at properly classifying the expenses necessary for asset construction.

The tax solutions indicated in the acts may present tempting “proposals” for individuals keeping the entity’s accounting. The authors mean higher limits on expenses and tax deductions to minimize them. Therefore, the sixth and final research question should be posed: Is there a statistically significant relationship between the performance of RD works and the tendency to manipulate the financial result? This sixth hypothesis will be verified.

To verify the sixth hypothesis, a chi-square test of independence was performed. The test results indicate that there is no statistically significant relationship between the commencement of planned future RD works and the risk of data manipulation in the accounting records and financial statements: chi2 (1 = 0.873; p = 0.350). This hypothesis is rejected.

Such relationships have not been previously studied in the literature. However, the result is not surprising. There has always been a risk of manipulation of accounting data (in records and/or financial statements), as well as taxes, in order to obtain benefits and maximize profit while minimizing taxation.

Manipulation of accounting data, also refered to as book fraud or, more commonly, accounting fraud, can occur for a variety of reasons, some of which may be more prevalent or complex than others. The most common reasons include tax avoidance, improvement of financial results, maintaining market position, obtaining financing, internal pressure, lack of sufficient internal control, bonuses, and employee motivations (Hołda, 2020).

Among these, the most common are improving financial results and tax avoidance (Zielińska, 2022). However, the other reasons mentioned above are also prevalent in business practice. Manipulation of accounting data is prohibited by law and violates the principles of professional ethics and legal provisions. This leads to loss of investor confidence, legal and reputational consequences, and can be detrimental to the long-term success of the company. There may also be a risk of insolvency if a tax audit begins (Białek – Jaworska, Budlewska & Hałatek, 2024). Therefore, it is crucial for companies to employ fair accounting practices and ensure appropriate controls are in place to prevent data manipulation.

In summary, three of the six hypotheses (numbers 1, 2, and 3) were rejected because they did not show statistically significant differences between the groups. However, hypothesis 4 was accepted, indicating a significant difference between the groups, with Cramer’s V value indicating a moderate relationship between the variables. Hypotheses 5 and 6 were also rejected because they showed no significant differences between the groups.

Most of the obtained results should be classified as revealing due to the lack of research in this area to date. Firstly, people involved in the entity’s accounting should pay more attention to their knowledge of accounting and tax law in the field of RD works. Active accountants or those just starting their professional careers in similar positions should recieve more detailed education at the initial stage of their educational path. In the opinion of the authors, this approach should be standard practice. However, as mentioned in the theoretical part, the issue of RD works is relatively complex compared to other issues that accountants encounter on a daily basis (such as simple costs and settlement records).

It may be beneficial to consider support for education and training in RD works regulations. This issue may be crucial for ensuring understanding and compliance with regulatory requirements in the context of accounting and tax law. Training programs for entrepreneurs, scientists, and regulators can help increase awareness and competence in this area.

Regarding the unification of regulations in force in Poland, in the context of RD works, it is worth considering the introduction of a new national accounting standard in terms of their recognition, valuation, and presentation in the financial statements. The conducted research suggests that the respondents do not feel such a need; however, if the research was carried out among a different target group (such as only managers or only accountants), the results obtained could indicate the need to create such a standard.

On the other hand, the lack of such a need on the part of the respondents may indicate that, in their opinion, the regulations are transparent. Therefore, it is not possible to clearly ascertain what criteria guided the respondents. The authors express the need to conduct such research in a separate study.

Last but not least, it should be noted that additional research on regulatory needs among various target groups, such as managers and accountants, should be carried out. This research will allow us to better understand whether there is a genuine need to introduce new regulations or accounting standards for RD works or to clarify existing ones.

Moreover, it was pointed out that almost always when entrepreneurs decide to use reliefs for RD works, there is an increased risk of control by tax authorities and institutions co-financing the construction of the asset. In fact, this control by authorized bodies occurs, which may cause some anxiety on the part of entrepreneurs.

It is important to ensure sustainable supervision over the use of tax relief for RD works, understood as a process that requires consideration of both the needs of entrepreneurs and research institutions, as well as public and fiscal interests. Potential controls can also prevent accounting fraud and sometimes deter accounting crimes. Particular vigilance is required for smaller companies where internal controls may be limited.

At the beginning of this article, a review of the literature and definitions related to RD works was performed. Moreover, the theoretical part discusses and presents the classification of expenses related to the titular issue.

In conclusion, the article analyzes current trends in the field of balance sheet law, both at the national and international level. Tax law solutions were also presented in terms of the correct classification of expenses related to RD works. The impact of changes in regulations on business practice and the need to adapt to international standards through accounting standardization may be considered. Unfortunately, making such a classification under tax law would be problematic due to its territorial scope of operation (each country has adopted different regulations in this respect).

In the context of national balance sheet law and its adaptation to international solutions, an analysis was made of the degree of compliance between Polish balance sheet law and the international standard IAS 38. Areas of convergence and differences were identified, which may lead to the need to adapt or interpret Polish regulations in relation to international requirements.

The article proposes a classification of RD works in the context of balance sheet law, taking into account various methodological approaches and thematic areas. Works aimed at the interpretation and analysis of applicable regulations were distinguished, as well as those focused on innovations and new concepts in the field of accounting. The need for further research was also emphasized to improve the legal system related to balance sheet law and to adapt to changing economic conditions and international standards.

In the empirical part, statistical analysis of the data was performed. Observations were collected through surveys, with descriptive and statistical interpretation of the data presented in the diagrams. In addition, a chi-square test of independence in the research hypotheses was conducted. Most hypotheses had to be rejected due to the lack of a statistically significant relationship in the conducted research. Only one of the six hypotheses can be classified as acceptable, provided that the strength of the relationship is moderate.

The results obtained through statistical analyses should not be surprising, as the initial assumptions of the authors of the article were confirmed. The accountants and managers indicated in the research sample do not have specific knowledge of the provisions of the balance sheet and tax law regarding RD works, which was verified using the first and second hypotheses. The obtained results did not indicate a statistically significant relationship between membership in a given group representing the entity’s accounting and the level of understanding and knowledge of the provisions of balance sheet and tax law in the field of RD works. The chi-square test results were (6 = 2.67; p = 0.849) and (3 = 4.25; p = 0.236), respectively. It may be suggested that numerous courses conducted by organizations educating accountants and managers should emphasize this issue, as a potential enterprise may experience significant economic benefits from the use of the titular topic.

It should be emphasized, however, that not only the aforementioned groups have an impact on the development of the company. It is true that accountants can only influence indirectly, but managers and employees (often employed in specialized RD departments) should be innovators who see the need to build a new asset that will meet the definition and qualify as RD works, contributing to the creation of innovative goods.

It is also important to follow numerous financial and substantive support programs for the construction of assets classified as RD works. There are many institutions that provide such support.

As mentioned, work experience in the accounting department does not prove knowledge of the provisions of accounting and tax law in this context. Moreover, the observations conducted indicate that there is a possibility of incorrect classification of RD works expenses, which may lead to distortions in financial statements, possibly also in tax aspects.

Further analysis of the results of the conducted research showed that there is almost always a risk of control from fiscal institutions during RD works and/or after the completion of the construction of an asset. In this aspect, hypothesis No. 4, set in the introduction of the article, was verified, which showed a strong statistical relationship between the use of reliefs for RD works in enterprises and the risk of tax audit. This statement is confirmed by the result of the chi-square independence test (1 = 7.41; p = 0.006). However, the result of the V-Cramer test was 0.568, indicating a moderate strength of the relationship between the use of reliefs for RD works and fiscal control.

In the opinion of the authors of the article, this behavior is absolutely justified and prevents abuses in business entities using RD works. On the other hand, however, it may discourage entrepreneurs from taking action in this area and encourage them to use creative accounting, and unfortunately, sometimes also its aggressive form. However, the verification of the authors’ initial assumptions was not confirmed in the selected research sample, as evidenced by the verification of the sixth hypothesis (chi2 (1 = 0.873; p = 0.350)) adopted at the beginning of this article. Perhaps conducting studies with more observations could show a different result.

Less often, such inspections are carried out by institutions co-financing the construction of enterprise assets, as demonstrated by verifying the fifth hypothesis (result of the chi2 test (1 = 2.07; p = 0.150). The relationship between the use of reliefs for RD works and verification activities aimed at checking the correctness of the institution co-financing the project was not statistically significant.

In the course of the research conducted by the authors, it was found that the respondents do not see the need to create a new national accounting standard for RD works, as demonstrated by verifying the third hypothesis (the result of the chi-square test was (3 = 1.56; p = 0.667)). It can be conclude that this behavior is not justified, as this issue is only partially described in the Act, and IAS 38, which describes this aspect of the entity’s accounting, was issued in 2008. Over the course of 16 years, there have been numerous changes in the provisions of the balance sheet law, and this could be considered here in creating a document that would be adapted to the current needs of economic units, where the added value could also be the organization and systematization of knowledge in the field of RD works.

As mentioned, RD works has been the subject of research by many authors. However, the research results contained in the article indicate a low level of knowledge among the respondents regarding balance sheet and tax law in the field of RD works. Moreover, the analysis shows that the respondents do not indicate the need to create a new national accounting standard in the field of RD works. It should also be noted that taxpayers almost always have to take into account tax control when applying tax reliefs, but not always from co-financing institutions. It is also important to point out the potential manipulation of the financial result in the scope of RD works.

All the goals and hypotheses set in the introduction were achieved. The article may constitute a basis for further research in the discussed aspect. It was not decided to conduct a tax analysis of the solutions adopted in individual countries due to the geographically different tax systems. Particular attention should be paid to the solutions of the balance sheet law in the field of RD works and the attempt to standardize them to international regulations.