Socio-economic conditions are undergoing rapid transformation. It is influenced by globalisation along with the accompanying development of technology. Technology, on the one hand, improves the day-to-day functioning of organisations by improving the efficiency of operations and employees' work (Moll et al., 2019). On the other hand, it is seen as a threat to eliminating humans from many professional and social areas (Frey & Osborne, 2017). The turning point of the progressive change was the fourth industrial revolution, I4.0, along with its advanced smart technology and further development of Industry 5.0 (Ghobakhloo et al., 2023). This is reflected in the manufacturing sector, specifically in creating smart factories (Lee & Lee, 2015). Smart factories define efficient, agile, and flexible manufacturing using the latest Internet of Things and Industrial Internet technologies, consisting of smart sensors and sensing, computing and predictive analytics, and resilient control technologies. These technologies must be integrated to transmit, interpret, and analyse data and control the production process as intended (Lee, 2015; Moll et al., 2019). Smart factories define efficient, agile, and flexible manufacturing using the latest Internet of Things and industrial Internet technologies, consisting of smart sensors and sensing, computing and predictive analytics, and resilient control technologies. Smart factories or, more broadly, smart organisations must become integral to smart economies, smart governments, or smart cities (Gupta et al., 2023). The smart economy is driven by innovation, creating an ecosystem to foster an entrepreneurial spirit in society. It should provide productivity and labour market flexibility and have its brand globally. Smart economies must have a smart administration, that is, open to information sharing and cooperation, with transparency in decision-making, and systematically improving the efficiency of its services through smart technological solutions. Smart economies cooperating with the smart government are an environment for smart people, i.e., a society ready for lifelong learning characterised by open-mindedness, flexibility to adapt to the transformations of the environment, and creativity. Smart economy, smart companies, and smart management cannot progress without the integration of knowledge management, which helps to respond to the challenges of Industry 5.0 faster and more efficiently (Caputo et al., 2019; Cilo et al., 2022).

Adamik and Fernandez-Sikora (2021) pointed out that the smart economy should create smart solutions to complex strategic problems to ensure human functioning and be more demanding of smart organisations and their environment. The smart economy must be based on a solid future-oriented foundation, so not only the technological innovations that are the main component of the Industry 4.0 concept (digital solutions, robotics, real-time processing of big data, internet connectivity, artificial intelligence, neural networks), but also the so-called soft innovations, i.e., social justice, the rule of law, transparency, accountability, social cohesion, people's wisdom, sustainability, and shared visions and goals (Kramer & Pfitzer, 2016). Thus, in the smart economy, the pillar is the integration and cooperation based on knowledge and innovative solutions of smart people, machines, and systems, leading to changes on its various levels to increase their quality, speed, and, therefore, the efficiency of different processes and activities and create added value in the long perspectivity (Fonseca, 2018).

The smart economy requires specific competence and creates technological and organisational challenges for companies (Moll et al., 2019). It means the creation by organisations of smart workplaces of human resources to implement smart work. Hassan (2016) states that smart work refers to a new approach to work made possible by advanced technological solutions integrated with the economic, environmental, and social spheres. Smart work means working more efficiently, increasing cost-effectiveness, and effectively combining employee roles. Smart work also requires smart employees characterised by smart competencies. This refers to the managerial function, which determines the development of the business and its various areas, and individual specialists with whom the functioning of the company and effective management is possible. Smart work in Industry 4.0 requires the integration of artificial intelligence (AI) tools (Del Giudice et al., 2023).

Given that in smart conditions, knowledge and information are a “key currency” in various human interactions, machine interfaces, or negotiations, and that is a pillar of smart management and decision-making. Management accountant is a generator of relevant information for the need to support management, improve its efficiency, and ultimately improve profitability and create value for the organisation. In turn, increasingly developed technological solutions foster his role as a business partner in cooperation with managers and other business partners inside and outside the organisation (Järvenpää, 2007).

The new environment is challenging for management accountants and requires identifying new skills and competencies in the scope of SMART management. The current literature is focused mainly on general requirements for the new generation of managers. Industry 4.0 is characterised by integrating digital technologies, automation, standardization, and data analytics into all business operations. Managers need to understand and harness these technologies to make informed decisions. They must go beyond spreadsheets and financial reports to work with data from the Internet of Things devices, AI-driven systems, and blockchain, allowing them to provide real-time insights and support strategic choices (Chatterjee et al., 2020; Hallem et al., 2022; Ribeiro et al., 2021).

In smart management and Industry 4.0, data takes centre stage. Managers must be skilled in collecting, processing, and interpreting vast data. They should be able to transform data into actionable insights for executives, aiding in better decision-making and helping companies stay competitive in rapidly changing markets (Akter et al., 2016; Duan et al., 2019; Dubey et al., 2020). Traditional risk management focuses on financial risks. However, in Industries 4.0 and 5.0, managers must address new risks related to cybersecurity, data privacy, and technological disruptions. Understanding these risks and developing strategies to mitigate them is essential (Lezzi et al., 2018).

The article aims to identify the characteristics and traits of management accountants operating in a smart environment.

Our research employed a multifaceted methodology, beginning with a foundational theory of change to guide our exploration. We conducted a comprehensive literature review, examining existing research on management accountants' evolving role in emerging SMART technologies. This review provided the foundation for a deeper conceptualization of the topic, allowing us to identify key themes and trends. Building on this foundation, we developed several propositions that capture the unique challenges and opportunities facing management accounting professionals in the rapidly changing SMART economy. By integrating these methodological components, we aim to provide a well-rounded analysis that sheds light on the evolving landscape of management accounting.

The paper is structured as follows: literature review tracked by methodology, the core section devoted to developing the conceptual framework for SMART management accountants, and the article is closed with conclusions and limitations. The article contributes to developing the theoretical background for studying management skills and competencies in the SMART era.

Filos (2006) defined the smart organisation “as the threshold for distinguishing winners from losers in the digital economy”. The European Commission juxtaposed the smart organisation with one that is knowledge-driven, learning, connected to the global Internet, dynamically adapting to new organisational practices and forms, and agile in creating and exploiting opportunities offered in the digital environment (Filos, 2006). A smart organization is a dynamic entity adept at generating, obtaining, organizing, and disseminating both codified and non-codified knowledge. It harnesses this knowledge to enhance operational efficiency, promote sustainability, and bolster competitiveness within the global marketplace. It has a clear strategic vision, culture, and a supportive incentive system for attaining achievements of a social and environmental nature (Matheson et al., 1998; Stępień et al., 2023). Smart organisations are equated with success, the fulfilment of successfully intended goals, and this is due to the creation and selection of information from their own and external. The professional vision thus obtained is used to modify organisational behaviour and build internal structures to transfer and apply the accumulated knowledge effectively. Adamik (2020) defined a smart organisation as “a continuous process of organisational improvement in structure and method of operation, implemented through methodical acquisition and application of knowledge to survive and grow sustainably”.

A smart organisation, however, cannot just be an “island unto itself”. It is a network of other organisations forming alliances with suppliers, customers, employees, and competitors. As a rule, an organisation in a network or cluster is characterised by flat hierarchies, dynamic structures, empowerment of individuals, and high respect for individual capabilities, intellect, and knowledge (Filos, 2006). Carley (2001) stressed that one of the essential skills of this type of organisation in the era of Industry 4.0. is precisely the creation and development of business networking. It is fostered by a knowledge environment formed by ICT hardware, software, human resources, data, and information (Adamik & Sikora-Fernandez, 2021). As a result, smart organisations include three components: the ICT, the organisational, and the knowledge dimensions. Networking at the ICT level enables organisations to move to extended or virtual organisational forms and, within them, build cross-functional teams. The knowledge dimension refers to sharing information of people working in different teams, which is related to the integration and complementarity of competencies. The organisational dimension is associated with the flexibility and agility of teams, which, through cooperation, shape partnerships to effectively achieve strategic goals and create added value (Filos, 2006). Goldman et al. (1995) identified four strategic dimensions of agile behaviour that are key to smart organisations. These are customer focus, commitment to intra- and inter-organisational collaboration, organising to master change and uncertainty, and leveraging the influence of people (entrepreneurial culture) and knowledge (intellectual capital).

In addition to the network structure promoted for smart organisations, a hierarchical structure is still visible in the market. Therefore, viewing this entity as a hyper-connected organisation is the best solution. According to Nonaka and Takeuchi (1995), it can maximise (hierarchical) efficiency at the corporate level and network teams as scale and complexity increase while maintaining the ability to create value.

Smart organisations require smart management along with smart methods for them to fulfil the role they are called to play. Smart management has a link to active management theory grounded in finance. According to it, smart management requires the manager to manage the organisation and its areas flexibly and efficiently to ensure competitive advantage and profitability despite risks and constraints. Although such an explanation can be considered common to management, smart management requires a change in mechanisms that will allow more efficient use of resources, including modern methods and technologies for analysing and processing information, and ensure cooperation between advanced technology and human capital.

In the literature, references can be found to specific areas of smart management, i.e., in transportation or supply chain (Stefansson & Lumsden, 2008; Wu et al., 2016). These cases emphasise smart management's importance in adding value and identifying key elements that fulfil this direction. Big data, Internet of Thing infrastructure, advanced analytics, data mining and business intelligence, automation, digitization, standardization, streamlining, openness to data exchange, integration, process, and product innovation (Wu et al., 2016). Stefansson and Sternberg (2007), on the other hand, pointed out that close cooperation with partners, mutual exchange of data and information through shared and decentralized databases, and, thanks to the technologies supporting this process, practical application of information for planning, control, and real-time decision-making are the keys to the success of smart management. Associated with smart management is the achievement of goals, which should be by the SMART concept, i.e., specifiable, measurable, achievable, relevant, and time-bound (MacLeod, 2012). By formulating goals using the SMART concept, one can be sure of achieving organizational success, which will be reflected in high performance. This includes nonfinancial perspective, i.e., performances in the sphere of environment and society. However, it is impossible to shape smart organizations and implement smart management to achieve SMART goals without smart human resources and smart work. Smart prospects are the result of the development of technology, including the application of advanced smart solutions flowing from the concept of Industry 4.0. (Cascio & Montealegre, 2016).

The competitive advantage of companies will depend not only on the adaptation of innovative technologies but also on changes in labour, work environment, and human resource strategies. The placement of human beings in the environment of Industry 4.0 has given rise to the smart human resource, where smart human manifests itself in the critical treatment of the human, the intangible. In contrast, resources point to human knowledge, know-how, and their application to achieve greater productivity and self-esteem (Abellán-Sevilla & Ortiz-de-Urbina-Criado, 2023). The idea of smart human resources in business, in turn, has defined the smart worker or smart worker 4.0 (Abellán-Sevilla & Ortiz-de-Urbina-Criado, 2023; Pillai & Srivastava, 2022; Errichiello & Pianese, 2018). The main intention of operating an employee in a technology environment is to support and maximize his or her potential, thus making him or her do his or her job more smartly. This may also involve eliminating operational, repetitive activities with low added value. According to Meindl et al. (2021), smart working refers to employees' use of advanced technological solutions (artificial intelligence (AI), cloud, big data, automation, standardization) to support decision-making processes, manage knowledge, stimulate creativity, and design and enhance employee safety and satisfaction. All these skills are the foundation for the development of Industry 5.0, which assumes high use of robotics and AI, focusing more on human-machine collaboration, sustainability, and social responsibility. A smart employee is an employee who performs work differently, using digital tools, but also possesses specific skills and abilities (Dornelles et al., 2022). According to Errichiello & Pianese, (2018), smart work manifests itself in flexibility, that is, doing work regardless of time and place, translating into remote work. Smart work means flexible schedules, locations, and forms of employment (Hassan, 2016). Flexibility at work is fostered by the following elements: the redesign of physical workspaces along with information and communication technologies for employees and significant changes in employees' work procedures and traditional management (Clapperton & Vanhoutte, 2014). These are called the three levers: bricks of Bytes and Behavior, which refer to the physical, technological, and behavioural dimensions (Clapperton & Vanhoutte, 2014; De Kok, 2016). Orlikowski (1992) also pointed out that smart work is based on a combination of at least two elements: institution, location, and technology. According to the researcher, smart work is carried away from offices and factories, where employees communicate with others through new technology.

Smart working, in effect, can mean an atypical style of work that does not fit into the standard form of employment, i.e., telecommuting, telework, e-work, mobile work, but is expected to generate benefits for both parties (Robertson & Vink, 2012; Rudolph & Schröder, 2003). Hassan (2016) defined a conceptual framework for smart work. These include work policy change, application, managerial support, measurement, and feedback. Smart working responds to changing economic and social transformations, including adopting family-friendly solutions and work-life balance. Smart working is more effective for assessing and monitoring workload and achievements. In addition, employees have a better sense of well-being, resulting in more effective cooperation (Coffey et al., 2016). This is also supported by the research of Golden (2012), who emphasises that smart working improves employees' health and well-being and gives work or life satisfaction without raising ongoing labour costs and even improving work efficiency. Smart working is bound by autonomy, which is referred to as backbone. It is intended to proactively foster strategic goal achievement (Boute & Van Mieghem, 2019).

Smart working creates opportunities to work more efficiently and effectively, increasing organisational performance. It refers to “new ways of working made possible by technological advances and made necessary by economic, environmental, and social pressures” (Hassan, 2016). It appears to be, as Morsi (2002) (as cited in Hassan, 2016) states, “the best way to face rapidly changing business demands and remain competitive”. Smart working defines smart workers who have flexible skills. They are well-informed and well-connected through technology, and they do not work under strict director supervision but more as partners, which promotes self-actualisation, better self-perception, and satisfaction, thus leading to business growth (Hassan, 2016).

Smart working for competent workers means adapting advanced and innovative technologies by organisations and using them with soft skills, namely flexibility, openness, partnership, willingness to self-development and continuous learning, and emotional intelligence. This means that socio-emotional skills are essential for the formation of smart workers.

Organisations that want to achieve the smart title must ensure that working conditions are adapted to a smart environment through technology and that employees are retrained or upgraded. Employees operating in smart organisations and working conditions should have specific characteristics and approaches. In particular, they emphasise lifelong learning, open-mindedness, creativity, and elasticity in adapting to change and good decision-making (Kumar, 2017), and enhancing work productivity. Adamik and Fernandez-Sikora (2021) stressed that smart employees working under the conditions of concept Industry 4.0 should have the following competencies and skills: subject matter knowledge, ability to learn, ability to work in a team, ability to work in a multicultural environment, ability to work remotely, knowledge of foreign languages and IT, ability to share knowledge, and in attitudes they see such as attitude to continuous development, goal orientation, openness to new experiences, creativity, flexible thinking, agility, high tolerance for uncertainty and sociability. Writing about competencies and skills, it is worth recalling Barbar and Plucker (2002), according to whom such labels as intelligence, expertise, ability, and talent inhibit the evolution and contextual nature of the individual-environment relationship (social, cultural, ecological, relational). According to the researchers, these constructs can be described more as functional relationships acquired, updated during various transactions, through which individuals appear to possess knowledge and skills. In addition, some traits are established within the individual, in a sense “innate”. If correctly grasped and guided during transactions, they can shape an individual with the given labels of intelligence or expertise, which were previously perceived differently. In this regard, the characteristics of smart workers, who rely mainly on networking and interaction in their work, should be described through traits, attitudes, or nature/disposition.

In addition to the traits that define smart workers, personality and its components are expressed in behaviour and interactions with others and a given situation. Tupes and Christal (1961) grouped five traits of smart human beings, which also translates to workers. These are flexibility, extroversion and openness, emotional stability, awareness (dependability), and culture and intellect. The same characteristics were indicated by McCrae & Costa (1991), i.e., extraversion of neuroticism, agreeableness, conscientiousness, emotional stability, and openness. Based on the indicated personality types, (Kumar, 2017) set a specific framework for the characteristics and roles of smart people in smart cities. This model can be transferred to smart workers in smart organisations.

As a result, the extrovert dimension of personality implies better interpersonal skills, readiness for change, and proactive decision-making, which translates into better leadership, teamwork, and willingness to take on new projects. Under agreeableness is understood as the development of cooperation, organisation, confidence, contentment, and harmony. Conscientiousness stands for focus, responsibility, dependability, interest in novelty, skating better organisation, and success. Emotional stability is expressed through satisfaction with life and work, low stress levels, calmness, confidence, and optimism. These traits influence better control of emotions, while an optimistic attitude and composure alleviate conflictual and unclear circumstances. The last dimension is openness to experience, creativity, curiosity, sensitivity, or innovation. Each dimension is conducive to fulfilling roles in a smart environment. For example, the first dimension of personality translates into better performance and smarter use of ICT infrastructure and services, respectively; the second dimension allows the formation of a friendly and satisfying work environment; the third dimension boils down to improving work organisation and following a plan, the fourth dimension enables one to go through difficulties in a “painless” way.

In contrast, the fifth dimension contributes to developing innovation and creating a sustainable work environment (Kumar, 2017). As a result, it can be concluded that a smart personality is a personality with a positive attitude, empathy, and support. It can be possessed by both an extrovert and an introvert (Montag & Elhai, 2019). In the latter's case, it is worth adding that technology that enables long-distance communication can influence increased openness so that smart organisations can favour introverts in presentations and discussions in the broader group. On the other hand, considering the four types of temperaments and their characteristics, i.e., choleric, sanguine, phlegmatic, and melancholic, it can be concluded that sanguine is the most appropriate for a smart environment. It is a confident, extroverted (outward-facing), relatively stable person whose main characteristics include being sociable, open, talkative, sensitive, relaxed, full of life, and a leader. It is a strong, balanced type but simultaneously empathetic and self-distant (Strelau, 1985).

Smart workers are not only associated with intellect and possession of textbook knowledge. Smart workers are a certain kind of personality predisposition, character, and abilities, which together translate into the ability to, among other things, perform different tasks, enter different roles and different cooperations, and work both independently and in a group. A smart worker should have non-spiritual abilities and social-emotional skills, such as conscientiousness or emotional stability (Bergner, 2020; He et al., 2019). Salgado et al. (Salgado-Gálvez et al., 2013) position that higher cognitive abilities lead to tremendous success at work and are more critical when significant intellectual challenges characterise the job. In contrast, Seibert et al., (1999) emphasise that under conditions of greater individual freedom of action, such conditions are created by smart working, social-emotional, or character-related skills that are crucial. The researchers point out that they perform well in unpredictable and challenging situations. So, they can be instrumental in today's dynamic, changing, unexpected business and economic conditions. Berger (2020) confirmed this thesis in her research, pointing out that social-emotional skills, particularly openness, go beyond cognitive ability in the context of predictive entrepreneurship. In her view, more than intelligence in terms of intellectual wisdom is needed to become an entrepreneur, for example. However, an individual must also be open-minded, curious, and like unconventional ideas and viewpoints (i.e., openness).

A smart worker is an agile worker embedded in a smart environment identified with elements of Industry 4.0, i.e., can quickly adopt and understand new technology and work with it effectively. A smart worker is also a business partner who can talk to co-workers and contractors, i.e., has his arguments and listens. A smart worker is also a “lifelong employee” who, although he knows that the company's high achievements are essential, such a perspective does not blind his eyes to observing the world and society and using his own experiences to improve the business and professional environment. A smart worker is different from the best or ideal employee, including not making mistakes but being a practical, sustainable, and social human being. Smart workers are best reflected by the statement (Kumar, 2017), “A person may have a brilliant mind and an outstanding intelligence, but with certain personality traits, a person cannot be one of the smart people”.

Considering the ideas of smart organisation, smart management, and smart workers, a suitable example is the silhouette of a management accountant. A management accountant plays an important role in the organisation, as he is most generally predisposed to support business activities. This factor distinguished him from the general profession of the accountant, who books and deals with taxes and financial reporting (Riahi-Belkaoui, 2018). The role lof the management accountant has also been and continues to be subject to change due to the evolution of economies and socio-business trends. Initially, they were responsible for planning and controlling economic processes; in the long run, their function was seen as holistic management support (Byrne & Pierce, 2007). At the same time, it was mainly reduced to preparing internal reports and analyses without active involvement in management and decision-making. Management accountants were perceived as aloof professionals confined to their department and, in many cases, as a certain “enemy” to other employees due to the constant pressure to reduce costs to ensure business profitability - an operational orientation (Burns & Vaivio, 2001; Parker, 2000). In recent years, the image of management accountants has been “warmed up” due to the emphasis on its business approach, that is, actively supporting the management and decision-making process (Granlund & Lukka, 1998; Taylor & Scapens, 2016). The management accountant has thus changed his image from the so-called “bean counter” to “business partner” or even “change agent” (Byrne & Pierce, 2007; Granlund & Lukka, 1998). The new perception of the specialist in question signifies a growing emphasis on a more strategic, forward-looking perspective of the organisation, whose goals can be realised through internal and external collaborative efforts (Wadan et al., 2019). Mistry et al. (2014), as well as Albelda (2011), have paid particular attention to the role of management accounting practice toward the development and support of sustainability, which involves expanding reporting and analysis, new tools and metrics for measuring achievements, i.e., not only targeting financial, but also non-financial aspects, and orienting management and decision-making toward environmental and social aspects, not just economic, and therefore value rather than exclusive profitability. Opinions and studies, for example, by CIMA or Adams and Frost (2008), show that management accounting practices have been and continue to be guided by the core values of economic prosperity.

As a result, several rationales are being presented (regulations, greater expectations for managers to orient management toward sustainability, voices of accounting professionals), emphasising the need for management accountants to engage in sustainability actively (Mistry et al., 2014; Wijethilake et al., 2017). Perhaps such a perspective will emerge in a new role for the management accounting professional, such as a “social partner”. Thus, the practice of management accounting is further evaluated in the direction of value and strategic management, and this trend may be fostered by the smart environment, which is based on the concept of I4.0., i.e., advanced and smart technologies. Its framework assumes the availability of necessary information in real-time thanks to integrating various network links that circulate value or value chains (Wadan et al., 2019). Structural changes require management changes, and thus, changes in the role and perception of the management accountant being an active link in management. Jedrzejka (2019) stresses that accounting shows significant potential for automatisation and robotisation, which will translate into a change like tasks from specialists in this field towards business consulting and automation management or management consultant. The transformation in the sphere of tasks, where even tighter integration of management accounting with financial accounting and management, more intensive coordination of internal and external processes and data thanks to technology, and the need to share knowledge will affect the emergence of new roles and a new walkthrough of qualities and competencies that the “new” management accountant should possess in the so-called digital environment (Schäffer & Weber, 2015). Yazdifar and Tsamaney (2005) now emphasise the importance of coordination competencies, strategic thinking, systems knowledge and IT scope, business knowledge, and interpretive skills. However, the Industry 4.0 environment will deepen their essence and form new characteristics of management accountants. For example, Gänßlen et al. (2013) highlight the importance of knowledge in statistics (regression, time series, or clustering) and computer science, social and communication skills, and a holistic understanding of business. Sauter et al. (Sauter et al., 2015), on the other hand, assume the importance of skills in forecasting and predictive analytics of management accountants, resulting from the development of Big Data and automation of temporal management accounting tasks. Practice representatives have a similar outlook, claiming that the idea of Industry 4.0, of which automation is a part, promotes transparency and optimisation of management accounting processes. According to them, management accountants will not have to focus on reporting but on analysis, interpretation, and the essence of communication and partnership, i.e., soft skills will increase. The analysis results of job advertisements for the management accountant position provide similar trends. There is a decrease in the importance of data collection and reporting tasks and an increase in the importance of budgeting, decision-making, and communication. In addition, MS Excel, VBA, and SQL skills dominate over SAP ERP/R3 (Wadan et al., 2019). According to Wadan et al. (2019), management accountants are not fully prepared to work in the Industry 4.0 environment, so they pointed out some predispositions that the specialist should have to be effective in the new environment. These include IT handling, Data warehousing, programming, coding, MS Excel with VBA, SQL, Data Mining, predictive and static analysis and forecasting, budgeting, decision-making partnership, communication, sure appearance, and project management. Industry 5.0 requires supporting societal goals beyond jobs and growth (Garrido et al., 2024), which means that requirements for smart management accountants will also change in this respect. The involvement of management accountants in implementing and assessing sustainability and corporate social initiatives will increase. The need to combine skills that require working closely with high-level IT tools, including AI, while maintaining the high standards of human centrism and resilience, shape the future portrait of the smart management accountant Industry 5.0.

Taking into account the current consideration of the new role of management accountants, which is indicated in the literature mainly by its two designations, i.e., “business partner” or “change agent”, one can ask whether this is sufficient to be a practical management accountant in the new conditions defined by digitalisation, automation, robotisation, and artificial intelligence. It may be closer to describing the specialist in question as management accountant 4.0. The answer is complex, as one can view these roles differently. In a sense, the management accountant has always been a partner, only in the hitherto targeted narrow audience, and today, adopting a more open attitude. In addition, only some management accountants are necessarily predisposed to be a business partner, as certain character traits of an individual may limit this role for it to be performed effectively. The management accountant was also an agent of change, as he identified bottlenecks in the business and the need to reduce them, but this was more of a passive role rather than an active one. On the other hand, management accounting 4.0 and 5.0 may have too technical an overtone. What term most reflects the future management accountant and his role in the organisation? Considering the dynamically developing idea of a smart environment in conjunction with the era of Industry 4.0 and sustainability, it would be most adventurous to see the management accountant as a SMART specialist.

We used the explorative theory of change approach to develop a conceptual framework for SMART management accountants. According to Dale et al. (2023) “theory of change describes the causal relationships between the events linked to an intervention that aims to meet a set of stated scheme objectives. In doing so, it seeks to consider context and any likely changes to this that can be foreseen”. A Theory of Change (ToC) approach guides the course of an evaluation by first pinpointing the theoretical basis that clarifies the mechanisms through which an intervention is anticipated to realise its intended outcomes. Subsequently, this can be empirically verified by assessing indicators for each anticipated stage along the causal path from implementation to impact. De Silva et al. (De Silva et al., 2014) believes that “a ToC is a theory of how and why an initiative works which can be empirically tested by measuring indicators for every expected step on the hypothesised causal pathway to impact”. Researchers believe that ToC can be applied in any field and adjusted to any change (Kubisch, 1998; Mackenzie & Blamey, 2005; Sullivan et al., 2002; Yatirajula et al., 2022). A ToC delineates the pathway through which a series of actions will result in short- and long-term effects. It additionally aims to recognise environmental factors that could influence these effects. This process assists in constructing and reinforcing an evidence-based rationale. It allows those implementing the intervention to attribute alterations in the outcomes (compared to the initial state) to the activities integrated into the initiative. This is why ToC is suitable for developing the conceptual framework of SMART management accountants.

The logical framework of our approach is presented in Table 1.

Methodological approach to the development of the conceptual framework of SMART management accountant

| Component | Characteristics |

|---|---|

| Literature review | Conduction of an extensive literature review covering various sources related to Industry 4.0, smart management, and the concept of smart work. Analyse academic research, industry reports, books, and other relevant publications. |

| Conceptual framework development | Based on your literature review, smart management accountants must develop a conceptual framework that outlines skills and competencies. Identification of key concepts, relationships, and variables within the literature that pertain to the skills of management accountants in the context of Industry 4.0 and smart management. |

| Theoretical synthesis | Synthesise the theoretical insights from the literature into a coherent framework that highlights the interplay between skills, smart management practices, and Industry 4.0. Consideration how the concepts and theories from different fields (management accounting, Industry 4.0, smart management) intersect and influence one another. |

| Gap identification | Identify gaps in the existing literature where your research can make a valuable contribution. Determining which aspects of smart management accounting skills have not been sufficiently explored requires further theoretical development. |

Source: developed by authors

A ToC is crucial for constructing a conceptual framework for SMART management accountants. It offers a structured pathway to define objectives and the steps to achieve them, facilitating goal clarity (Blamey & Mackenzie, 2007). ToC emphasises identifying causal links between inputs, activities, outputs, and outcomes, helping establish how specific traits lead to desired results in the context of SMART management accountants. Moreover, ToC considers contextual factors that may influence outcomes, ensuring adaptability to different organisational environments (Kirshner et al., 2021). This approach aligns the framework with the overarching objectives of SMART management, emphasising technology, analytics, and innovation. It provides flexibility for ongoing refinement as the field evolves. ToC enhances stakeholder communication and fosters engagement, promoting an understanding of the framework's rationale and expected outcomes (Penuel et al., 2011). Ultimately, a ToC-based conceptual framework offers a holistic view of skills and competencies vital for SMART management accountants, contributing to the broader knowledge base and guiding further research and practice in this dynamic field.

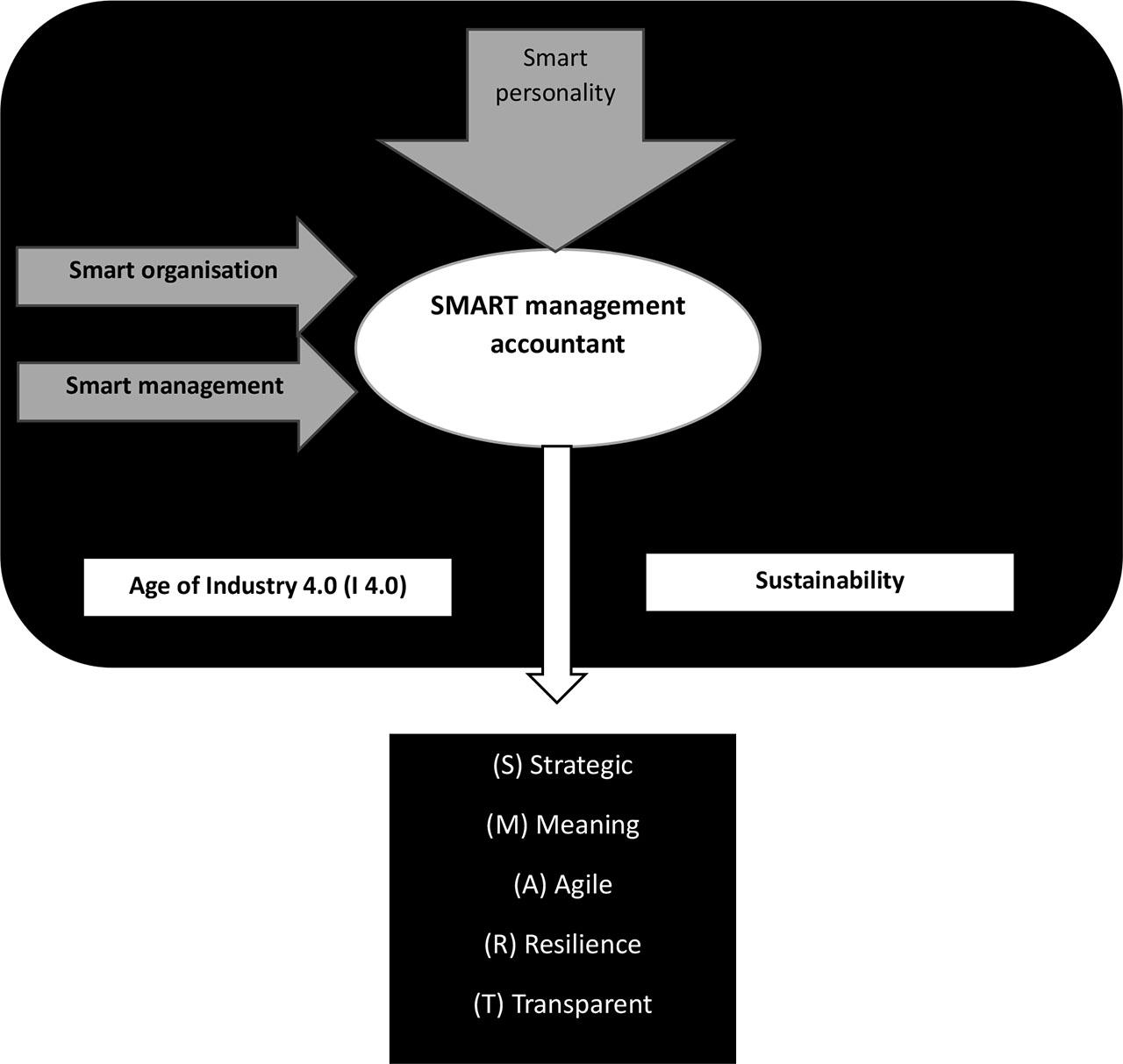

SMART management accountants result from the impact of the characteristics and features of smart organisations, smart management, smart workers, smart working and smart personality, which more broadly, from a macro perspective, is identified with smart economies, smart governments, smart cities, or smart people/humans. These plateaus are conditioned by the development of the Industry 4.0 era, smart and advanced technology, and sustainable development (see Fig. 1).

Determinants for SMART management accountant

According to the dictionary, “smart” means, in context, to be quick in an individual's actions or to possess or exhibit sharp intelligence or ready mental abilities (Smart, 2023). Considering smart ideas broadly, SMART management accountants can be defined by the following characteristics: (S) Strategic, (M) Meaningful, (A) Agile, (R) Resilient, and (T) Transparent.

A management accountant in a smart environment should demonstrate a strategic approach to work and carry out activities to support the organisation's strategic management (Wijethilake et al., 2017). It means taking a long-term view, the centre of which is the profit or profitability category and value. Value that considers the needs of various stakeholders, i.e., owners, employees, suppliers, customers, society, and the environment. Therefore, the indicated characteristic corresponds closely to sustainable development. At the same time, the smart management accountant should seek, together with the manager, a balance between performances in the economic, social, and environmental spheres using the “win-win” principle and a high correlation between the operational and strategic perspectives of the organisation's operation. Thanks to automation, robotization, and digitalization, efficiency in this area can be achieved quickly, provided one has the knowledge and ability to use advanced and intelligent technologies of Industry 4.0 and Industry 5.0. Intuitiveness will also be a valuable trait for a management accountant.

A management accountant should be focused on something other than his role and achievements but must exhibit a partnership approach and see himself as an integrated unit of larger or smaller teams. This characteristic can be realised by certain traits and attributes: openness, open-mindedness, empathy, understanding, assertiveness, and communication. Therefore, the first category (S-Strategic) can be associated with budgeting, forecasting, predictive analysis, or decision-making (Wadan et al., 2019).

The second component (M-Meaningful) lays behind the flat meaning of sense-seeking, or so-called sense-making. A management accountant should seek and indicate the meaning of his actions and decisions but also relate in the same respect to the managers with whom he must work closely and other stakeholders, such as owners. Based on experience and observation, the management accountant verifies the meaning of the current situation with a view to strategy implementation and value creation, and in the case of inconsistencies, gives new meaning or seeks new meaning. Indeed, the skillful use of artificial intelligence, which will enhance management accountants' search for meaning, is helpful in this regard. In addition, big data plays an important role. Accountants need to use many kinds of different data sources in real-time, which is made possible by Industry 4.0 and Industry 5.0 technologies such as sensors or digital twins (Moll & Yigitbasioglu, 2019). A management accountant in a smart environment, therefore, has to assess whether given resources solutions have a further grounding in functioning, and this, he/she can be helped by a new, “fresh” outlook, as reflected in the quote, “The real voyage of discovery consists not in seeking new landscapes but in having new eyes”. (Ancona, 2012). It means seeking order, even if the management accountant still determines if it exists. Sense-making is an emergent activity, that is, the management accountant's ability to move between heuristics and algorithms, intuition and logic, inductive and deductive reasoning, the constant search for and provision of evidence, and the generation and testing of hypotheses, all of which should be done in real-time (Ancona, 2012). The qualities that are conducive to the realisation of this plateau by a management accountant in a smart environment are having emotional intelligence, self-awareness, flexibility to move from “what is” sensemaking and “what could be”, having a holistic view of various issues, but also being communicative and intuitive. Sensemaking is a collective action, not an independent proceeding, requiring negotiations and conversations based on critical and analytical thinking. It can be pointed out that “what distinguishes the smart management accountant from the average management accountant is their ability to perceive the nature of the game and the rules by which it is played when they play it”.

Agility is also related to the plateaus outlined above. The management accountant can react quickly to the changing situation of the company and the market and the changing needs of managers and other stakeholders. It means quick action and quick decisions and suggests collaboration inside and outside the organisation to increase its competitiveness and create value chains. Being agile is a beneficial trait in uncertain and turbulent environments. In addition to responding quickly to change, the key is proactively anticipating change and looking for emerging opportunities (Ambe, 2010). It refers to changes in management accounting processes, in agile use of advanced technology offered by the smart organisation, and dynamism in co-decision-making and co-management. For a management accountant to act this way, smart conditions must emerge, i.e., real-time data flow, credibility, process integration, and networking (Kisperska-Moron & Swierczek, 2009). The predisposition of agility makes it possible to quickly adapt the information for the need of strategic management, including, for example, skilful directing of activities realisation with different intensity of economic, social, and environmental goals depending on the environment's expectations. Management accounting with this trait can add value, be quality-oriented and proactive, use technology flexibly, and shape an effective combination of “soft” and “hard” organisational techniques and resources. The qualities that help in being an agile management accountant are openness, flexibility, communication, critical and analytical thinking, but also emotional intelligence.

The fourth dimension of the smart management accountant is resilience. This characteristic means surviving or quickly overcoming difficulties. Management accountants are exposed to various unpredictable situations, sometimes critical incidents. In addition, they have to cooperate on an ongoing basis with other activities and business partners, where this is accompanied by different goals and expectations, thus generating conflations and, therefore, stressful situations. It is worth noting that management accountants have focused mainly on financial goals; nowadays, they have to look for solutions leading to realising goals in three spheres simultaneously, generating a considerable amount of data to collect, process, and analyse. Thus, the management accountant is pressured to fulfil the company's strategy and managers' intentions. Indeed, a smart organisation and its advanced technology can make it easier for a management accountant to achieve resilience. However, personal qualities, i.e., self-esteem, self-regulation, and optimism, may be decisive. External factors, on the other hand, include, for example, the resources mentioned above of the smart organisation, but appropriate support and appreciation from the environment can further enhance resilience (Southwick et al., 2014). The long-term experience of a management accountant can also increase the resilience of management accountants. A professional who has encountered many difficulties on his professional path acquires a kind of resilience that allows him/her to approach successive crises or chaos in a balanced way. Moreover, he knows the approaches and techniques to deal with them so that they do not cause negative consequences for himself but those around him (Herrman et al., 2011). As a result, management accountants' emotional intelligence, mental strength, and flexibility are gaining importance. They make it possible to adapt the management accountant's approach to the situation to minimise negative consequences for the organisation.

The last property of smart management accountants, i.e., transparent, can be controversial. Transparency most generally means clarity. This characteristic can be attributed to the clarity and transparency of management accounting processes, which can be supported by advanced technology. In turn, authenticity and ethicality are regarded here in the context of the specialist in question, especially in unclear situations. This means that the management accountant can make a clear argument, i.e., to be assertive, if, for example, the manager is wrong or his actions may deteriorate the company's efficiency. However, this is to work together to find a quick, favourable solution for the company, to motivate each other in this regard, and not to “criticise”. They understand what is ethical and what is not and can address this appropriately because they are communicative and open-minded. They are also flexible, i.e., they can act with a plan but also spontaneously. A management accountant with such qualities is a trustworthy, sincere employee, and with such a personality, one works effectively and achieves the organisation's success faster.

In this case, personal qualities can also promote transparency in the role of management accountant. These include mental stability, self-esteem, emotional intelligence, morality, and integrity. Complex competencies, i.e., solid knowledge of management accounting and understanding of ethical principles, are also crucial, as they translate into an ethical approach using advanced technology in management accounting tasks. Thus, a smart management accountant on this plateau is a transparent employee with their strengths and weaknesses.

Table 2 presents a summary of the characteristics and traits of SMART management accountants as a response to the challenges of the current SMART economy.

Characteristics and traits of SMART management accountants in SMART economy

| Challenges of the SMART economy | Characteristics of Management Accountants (MA) | Traits of the Management Accountants (MA) |

|---|---|---|

| Integration of digital technologies, automation, and data analytics into all business operations causes the need to understand and harness these technologies to make informed decisions. The pressure to go beyond spreadsheets and financial reports to work with data from IoT devices, AI-driven systems, and blockchain, allowing MA to provide real-time insights and support strategic choices | Strategic, Meaningful, Agile, Resilient | Openness, open-mindedness, understanding, assertiveness, communication, critical and analytical thinking, emotional intelligence, self-awareness, flexibility, mental strength, trustworthy |

| Big data pressure. MA must be skilled in collecting, processing, and interpreting vast data. They should be able to transform data into actionable insights for executives, aiding in better decision-making and helping companies stay competitive in rapidly changing markets | Strategic, Meaningful, Agile, Resilient | Openness, open-mindedness, communication, critical and analytical thinking, emotional intelligence, flexibility, mental strength |

| The need to address new risks related to cybersecurity, data privacy, and technological disruptions. Understanding these risks and developing strategies to mitigate them is essential | Strategic, Meaningful, Agile, Resilient, Transparent | Openness, open-mindedness, empathy, understanding, assertiveness, emotional intelligence, self-awareness, flexibility, mental strength, trustworthy |

| The pace of change in Industry 4.0 is rapid. MA must continuously update their skills to stay relevant. This includes understanding emerging technologies, regulatory changes, and evolving industry standards. | Agile, Resilient | Openness, open-mindedness, understanding, assertiveness, communication, critical and analytical thinking, emotional intelligence, self-awareness, flexibility, mental strength, trustworthy |

| Need to combine digital solutions, robotics, real-time processing of big data, internet connectivity, artificial intelligence, and neural networks with social justice, the rule of law, transparency, accountability, social cohesion, people's wisdom, sustainability, and shared visions and goals | Strategic, Meaningful, Agile, Resilient, Transparent | Openness, open-mindedness, empathy, understanding, assertiveness, communication, critical and analytical thinking, emotional intelligence, self-awareness, flexibility, mental strength, trustworthy |

Source: developed by authors

SMART management accountant refers to a professional who, using the facilities of a smart organisation, i.e., advanced Industry 4.0 technology and Industry 5.0, and considering the intentions of sustainable development, can effectively improve the management accounting function, interact directly with management, making it smarter, and as a result create added value for various stakeholders. SMART management accountant is characterized by strategic thinking and approach, constant search for meaning and its creation, agility, resilience, and authenticity. SMART management accountant does not mean an ideal employee and is not associated only with wisdom, and therefore typical intellect, but more with soft skills and emotional intelligence. Due to his personality and specific traits, a SMART management accountant can adapt to different situations and conditions, including in the era of Industry 4.0 and the development of Industry 5.0. He is interested and prepared for continuous learning and can concentrate and communicate.

Several vital attributes emerge as defining qualities in identifying the characteristics and traits of management accountants operating in the SMART economy. These attributes collectively encapsulate what it means to be a SMART (Strategic, Meaningful, Agile, Resilient, Transparent) management accountant. In the context of SMART management accountants, the term “smart” extends beyond mere intelligence; it encompasses a set of qualities that align with the dynamic demands and challenges of contemporary business environments. SMART management accountants are characterised by their ability to navigate and excel in smart organisations enabled by Industry 4.0 and Industry 5.0 technologies.

Strategic. SMART management accountants adopt a strategic approach to their work, actively contributing to an organisation's strategic management. They prioritise long-term value creation over mere profitability, considering the needs of various stakeholders, including society and the environment. Automation and digitalisation enhance efficiency, provided they possess the knowledge to harness these technologies effectively.

Meaningful. These accountants are dedicated to making their actions and decisions meaningful. They excel at sense-seeking and sense-making, aligning their activities with the organisation's strategy and value creation. They use artificial intelligence and big data to discern new meanings and verify existing ones, fostering a fresh perspective on complex issues.

Agile. Agility is a hallmark trait, enabling SMART management accountants to respond swiftly to evolving business landscapes. They adapt to changing circumstances, collaborate seamlessly within and outside the organisation, and proactively anticipate shifts in the market, fostering a competitive edge in turbulent environments.

Resilient. Resilience is critical, as management accountants often encounter unpredictable situations and stress-inducing scenarios. SMART management accountants thrive in the face of challenges, utilising personal qualities like self-esteem, self-regulation, and optimism. They are adaptable and equipped to manage crises effectively, minimising negative repercussions for the organisation.

Transparent. Transparency and authenticity define the actions of SMART management accountants. They foster clarity in management accounting processes, are supported by advanced technology, and prioritise ethical considerations. Openness, flexibility, communication, and ethical principles guide their conduct, establishing trustworthiness and effectiveness.

These traits collectively equip SMART management accountants to address the challenges of the SMART economy, where digital technologies, data analytics, and automation are seamlessly integrated into business operations. They excel in harnessing these technologies for informed decision-making and providing real-time insights. Additionally, they navigate the complexities of big data, cybersecurity risks, and the rapid pace of change in Industry 4.0 and Industry 5.0.

Continuous learning and adaptability are central to their approach, allowing them to stay current with emerging technologies and industry standards. SMART management accountants excel in combining digital solutions, artificial intelligence, and data processing with principles of sustainability, transparency, accountability, and social responsibility.

This paper has several limitations, including its reliance on a conceptual framework without empirical validation, which may necessitate future research for validation. Additionally, the traits outlined may only encompass part of the full spectrum of skills required in diverse SMART management accountant roles, and their relative importance may vary across industries. Furthermore, the study needs more specific case examples or quantitative data to illustrate the practical application of these traits. To address these limitations, future research can involve empirical studies to validate the framework's effectiveness in real-world scenarios, considering industry-specific nuances. Incorporating case studies and surveys among SMART management accountants can provide quantitative insights into trait significance and practical utility.