Figure 1

Figure 2

Figure 3

Figure 4

Figure 5

Figure 6

Figure 7

Figure 8

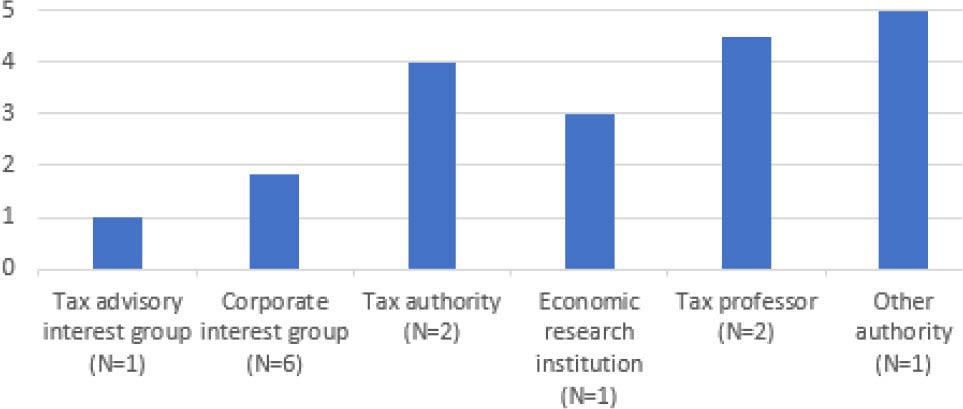

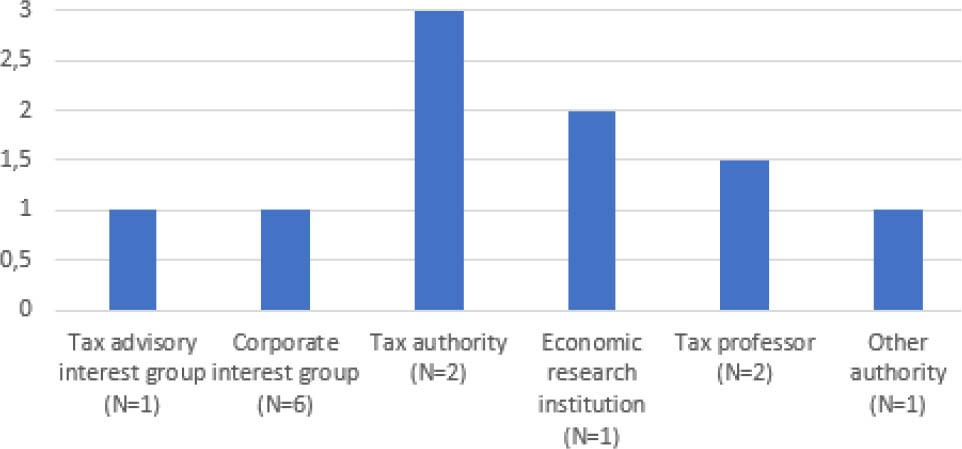

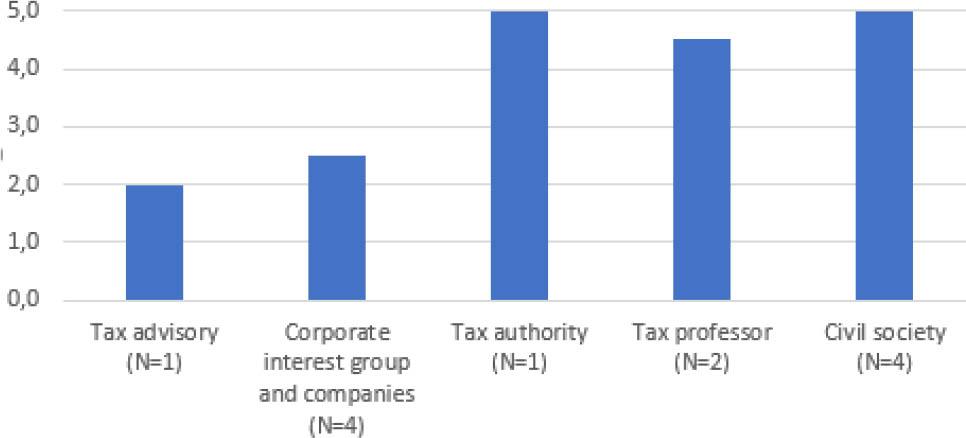

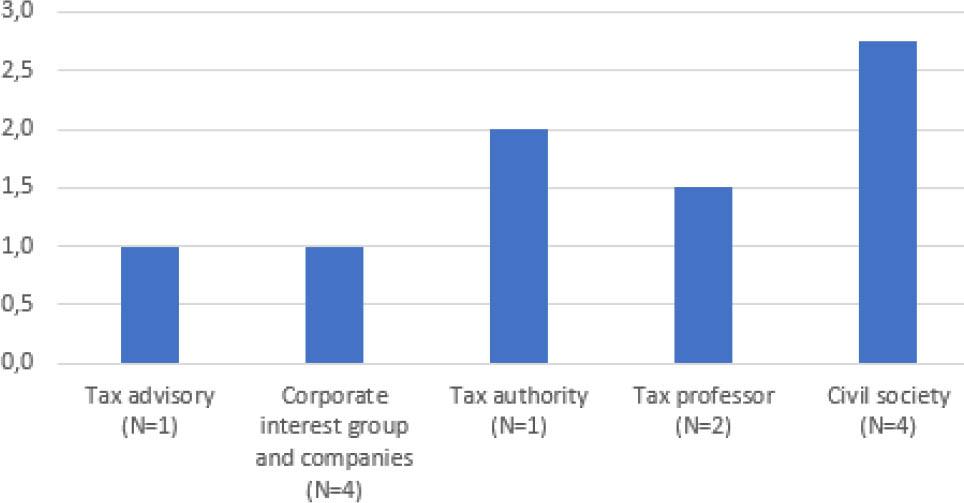

Statements in the 2012 September consultation_

| Statement | Stakeholder | Stakeholder group | View | Type | Specific public entity |

|---|---|---|---|---|---|

| 1. | Confederation of Finnish Industries | Corporate interest group | 1 | 1 | 0 |

| 2. | Finance Finland | Corporate interest group | 2 | 1 | 1 |

| 3. | Finnish Chamber of Commerce | Corporate interest group | 3 | 2 | 0 |

| 4. | Finnish Energy | Corporate interest group | 1 | 1 | 0 |

| 5. | RAKLI - The Finnish Association of Building Owners and Construction Clients | Corporate interest group | 3 | 2 | 0 |

| 6. | The Family Business Network Finland | Corporate interest group | 1 | 1 | 0 |

| 7. | Association of Finnish Local and Regional Authorities | Municipalities interest group | 3 | 3 | 1 |

| 8. | The Finnish Pension Alliance TELA | Pension funds interest group | 3 | 3 | 1 |

| 9. | The Central Organisation of Finnish Trade Unions SAK | Trade union | 5 | 4 | 0 |

| 10. | The Finnish Tax Administration | Tax authority | 5 | 3 | 0 |

| 11. | Marjaana Helminen | Tax professor | 3 | 4 | 0 |

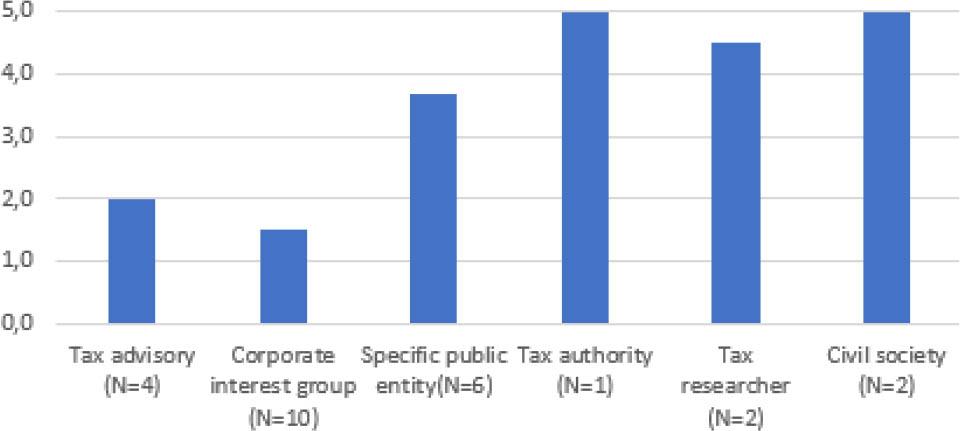

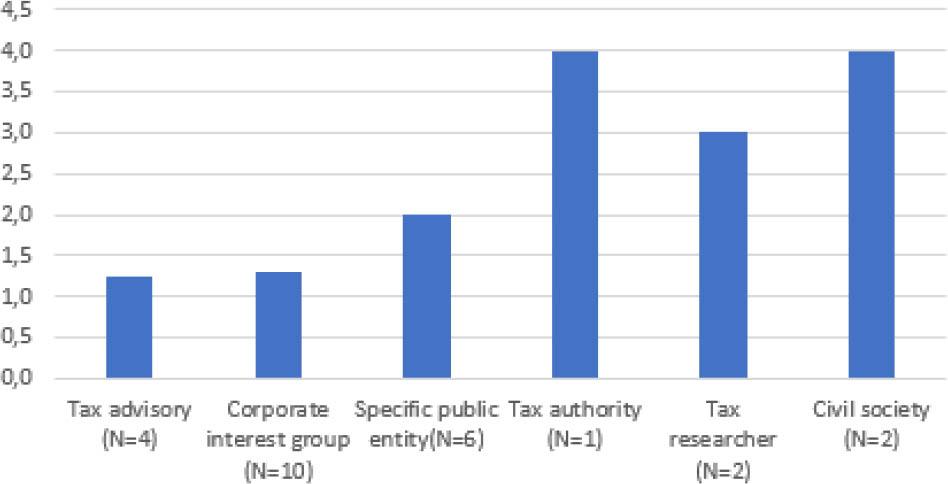

Statements in the 2018 spring ministry consultation_

| Statement | Stakeholder | Stakeholder group | View | EER ex |

|---|---|---|---|---|

| 1. | Technology Finland | Corporate interest group | 1 | 1 |

| 2. | INFRA — Infra Contractors Association in Finland | Corporate interest group | 1 | 1 |

| 3. | The Finnish Real Estate Federation | Corporate interest group | 2 | 3 |

| 4. | Finnish Energy | Corporate interest group | 1 | 1 |

| 5. | Federation of Finnish Enterprises | Corporate interest group | 1 | 1 |

| 6. | Finnish Chamber of Commerce | Corporate interest group | 1 | 1 |

| 7. | Finnish Venture Capital Association FVCA | Corporate interest group | 1 | 1 |

| 8. | Finance Finland | Corporate interest group | 1 | 1 |

| 9. | Confederation of Finnish Industries | Corporate interest group | 1 | 1 |

| 10. | The Family Business Network Finland | Corporate interest group | 1 | 1 |

| 11. | Taxpayers Association of Finland | Corporate interest group | 1 | 1 |

| 12. | The Finnish Wind Power Association (FWPA) | Corporate interest group | 2 | 3 |

| 13. | RAKLI - The Finnish Association of Building Owners and Construction Clients | Corporate interest group | 1 | 1 |

| 14. | Paikallisvoima ry | Corporate interest group | 1 | 1 |

| 15. | Kepa ry | Human rights based NGO | 6 | 5 |

| 16. | Finn watch ry | Human rights based NGO | 6 | 5 |

| 17. | Helsinki Region Environmental Services Authority HSY | Joint municipal authority | 3 | 3 |

| 18. | Pohjolan voima Oyj | Mankala company | 3 | 3 |

| 19. | EPV Energy Ltd | Mankala company | 3 | 3 |

| 20. | Teollisuuden Voima Oyj | Mankala company | 3 | 3 |

| 21. | Association of Finnish Local and Regional Authorities | Municipalities interest group | 3 | 5 |

| 22. | City of Vantaa | Municipality | 2 | 3 |

| 23. | TA Companies | Non-profit housing association | 3 | 3 |

| 24. | SOA — The Finnish Associations of Student Housing Organisations | Non-profit housing association | 3 | 3 |

| 25. | Association for Advocating Affordable Rental Housing — KOV | Non-profit housing association | 3 | 3 |

| 26. | Suomen Asumisoikeusyhteisöt ry. | Non-profit housing association | 3 | 3 |

| 27. | The Ministry of Economic Affairs and Employment | Other authority | 3 | 3 |

| 28. | The Ministry of Transport and Communications | Other authority | 3 | 3 |

| 29. | Ministry of the Environment | Other authority | 3 | 1 |

| 30. | The Finnish Transport Infrastructure Agency | Other authority | 3 | 3 |

| 31. | Kassiopeia Finland Oy | Other private company | 1 | 1 |

| 32. | Fortum Plc | Other private company | 1 | 1 |

| 33. | OP Financial Group | Other private company | 1 | 3 |

| 34. | Social Democratic Parliamentary Group | Political party | 6 | 5 |

| 35. | Municipality Finance Plc | Public Authorities' Finance company | 3 | 3 |

| 36. | Senate Properties | Public Real Estate Company | 3 | 3 |

| 37. | The Association of Finnish Tax Advisors | Tax advisory interest group | 1 | 1 |

| 38. | The Finnish Bar Association | Tax advisory interest group | 1 | 1 |

| 39. | The Finnish Tax Administration | Tax authority | 5 | 5 |

| 40. | Juha Lindgren | Tax Professor | 2 | 3 |

| 41. | Tomi Viitala | Tax Professor | 4 | 3 |

| 42. | Seppo Penttilä | Tax Professor | 2 | 2 |

| 43. | Reijo Knuutinen | Tax Professor | 4 | 3 |

| 44. | Marjaana Helminen | Tax Professor | 2 | 2 |

| 45. | The Central Organisation of Finnish Trade Unions SAK | Trade Union | 6 | 5 |

Statements in the 2018 fall parliamentary consultation_

| Statement | Stakeholder | Stakeholder group |

|---|---|---|

| 1. | The Finnish Real Estate Federation | Corporate interest group |

| 2. | Finnish Energy | Corporate interest group |

| 3. | Federation of Finnish Enterprises | Corporate interest group |

| 4. | Finnish Chamber of Commerce | Corporate interest group |

| 5. | Finnish Venture Capital Association FVCA | Corporate interest group |

| 6. | Finance Finland | Corporate interest group |

| 7. | Confederation of Finnish Industries | Corporate interest group |

| 8. | Taxpayers Association of Finland | Corporate interest group |

| 9. | VATT Institute for Economic Research | Economic research institution |

| 10. | Finnwatch ry | Human rights based NGO |

| 11. | Pohjolan voima Oyj | Mankala company |

| 12. | Teollisuuden Voima Oyj | Mankala company |

| 13. | Fennovoima Oy | Mankala company |

| 14. | Association of Finnish Local and Regional Authorities | Municipalities interest group |

| 15. | Financial Supervisory Authority (FIN-FSA) | Other authority |

| 16. | Municipality Finance Plc | Public Authorities' Finance company |

| 17. | Senate Properties | Public Real Estate Company |

| 18. | Juha Lindgren | Tax Professor |

| 19. | Tomi Viitala | Tax Professor |

| 20. | Seppo Penttilä | Tax Professor |

| 21. | Heikki Niskakangas | Tax Professor |

| 22. | The Central Organisation of Finnish Trade Unions SAK | Trade Union |

Statements in the 2016 parliamentary ATAD consultations_

| Statement | Stakeholder | Stakeholder group | View | Type |

|---|---|---|---|---|

| 1. | Confederation of Finnish Industries | Corporate interest group | 1 | 1 |

| 2. | Federation of Finnish Enterprises | Corporate interest group | 3 | 1 |

| 3. | Finnish Chamber of Commerce | Corporate interest group | 2 | 1 |

| 4. | Taxpayers Association of Finland | Corporate interest group | 4 | 1 |

| 5. | Finnwatch ry | Human rights based NGO | 5 | 3 |

| 6. | Kepa ry | Human rights based NGO | 5 | 3 |

| 7. | The Association of Finnish Tax Advisors | Tax advisory interest group | 2 | 1 |

| 8. | The Finnish Tax Administration | Tax authority | 5 | 2 |

| 9. | Marjaana Helminen | Tax professor | 5 | 2 |

| 10. | Tomi Viitala | Tax professor | 4 | 1 |

| 11. | The Finnish Confederation of Professionals STTK | Trade union | 5 | 2 |

| 12. | The Central Organisation of Finnish Trade Unions SAK | Trade union | 5 | 3 |

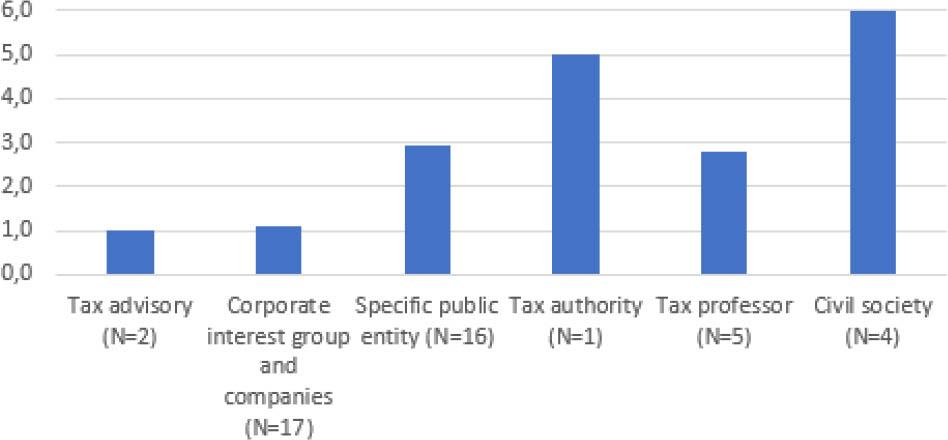

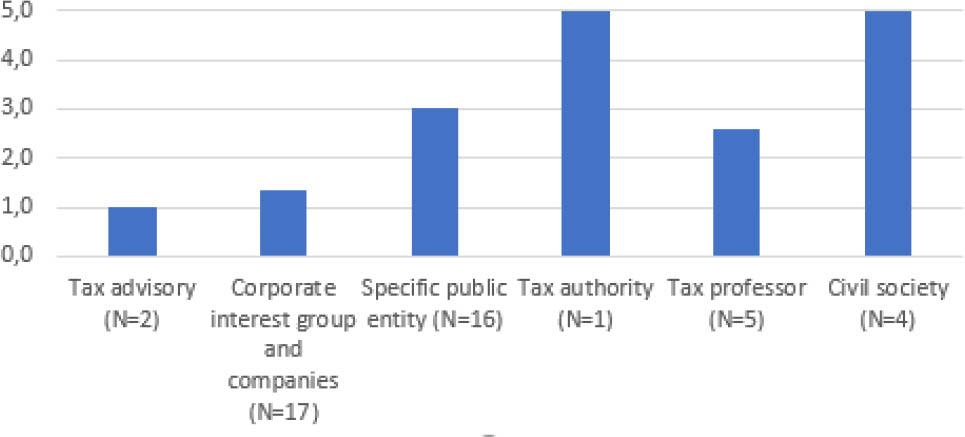

Statements in the 2012 April–June consultation_

| Statement | Stakeholder | Stakeholder group | View | Type | EER Ex | Delay | Real estate ex | Specific public entity |

|---|---|---|---|---|---|---|---|---|

| 1. | Confederation of Finnish Industries | Corporate interest group | 1 | 1 | 1 | 1 | 1 | 0 |

| 2. | Federation of Finnish Enterprises | Corporate interest group | 2 | 2 | 0 | 1 | 0 | 0 |

| 3. | Finance Finland | Corporate interest group | 1 | 1 | 1 | 0 | 1 | 0 |

| 4. | Finnish Chamber of Commerce | Corporate interest group | 1 | 1 | 1 | 1 | 0 | 0 |

| 5. | Finnish Energy | Corporate interest group | 1 | 1 | 1 | 1 | 1 | 0 |

| 6. | Finnish Venture Capital Association FVCA | Corporate interest group | 1 | 1 | 1 | 1 | 0 | 0 |

| 7. | INFRA - Infra Contractors Association in Finland | Corporate interest group | 3 | 2 | 0 | 0 | 0 | 0 |

| 8. | RAKLI - The Finnish Association of Building Owners and Construction Clients | Corporate interest group | 1 | 1 | 0 | 1 | 1 | 0 |

| 9. | Taxpayers Association of Finland | Corporate interest group | 3 | 2 | 0 | 0 | 0 | 0 |

| 10. | The Family Business Network Finland | Corporate interest group | 1 | 1 | 1 | 1 | 0 | 0 |

| 11. | Attac Finland | Economic democracy NGO | 5 | 4 | 0 | 0 | 0 | 0 |

| 12. | Tieyhtiö Valtatie 7 Oy | Public infrastructure company | 2 | 2 | 0 | 0 | 0 | 1 |

| 13. | Association of Finnish Local and Regional Authorities | Municipalities interest group | 5 | 2 | 0 | 0 | 0 | 1 |

| 14. | City of Helsinki | Municipality | 5 | 2 | 0 | 0 | 0 | 1 |

| 15. | The Finnish Transport Infrastructure Agency | Other authority | 3 | 2 | 0 | 0 | 0 | 1 |

| 16. | The Finnish Pension Alliance TELA | Pension funds interest group | 3 | 2 | 0 | 0 | 0 | 1 |

| 17. | Municipality Finance Plc | Public Authorities' Finance company | 4 | 2 | 0 | 0 | 0 | 1 |

| 18. | PWC Finland | Tax advisory company | 3 | 2 | 0 | 0 | 1 | 0 |

| 19. | The Association for Authorized Public Accountant (KHT-yhdistys ry) | Tax advisory interest group | 2 | 1 | 0 | 0 | 1 | 0 |

| 20. | The Association of Finnish Tax Advisors | Tax advisory interest group | 1 | 1 | 1 | 1 | 1 | 0 |

| 21. | The Finnish Bar Association | Tax advisory interest group | 2 | 1 | 1 | 1 | 0 | 0 |

| 22. | The Finnish Tax Administration | Tax authority | 5 | 4 | 0 | 0 | 0 | 0 |

| 23. | Marjaana Helminen | Tax professor | 5 | 4 | 0 | 0 | 0 | 0 |

| 24. | Pauli K. Mattila | Doctor in tax law | 4 | 2 | 0 | 1 | 0 | 0 |

| 25. | The Central Organisation of Finish Trade Unions SAK | Trade union | 5 | 4 | 0 | 0 | 0 | 0 |

Statements in the 2009 consultation_

| Statement | Stakeholder | Stakeholder group | View | Type |

|---|---|---|---|---|

| 1. | Confederation of Finnish Industries | Corporate interest group | 1 | 1 |

| 2. | Family Business Network Finland | Corporate interest group | 3 | 1 |

| 3. | Federation of Finnish Enterprises | Corporate interest group | 1 | 1 |

| 4. | Finance Finland | Corporate interest group | 1 | 1 |

| 5. | Finnish Chamber of Commerce | Corporate interest group | 2 | 1 |

| 6. | Taxpayers Association of Finland | Corporate interest group | 3 | 1 |

| 7. | VATT Institute for Economic Research | Economic research institution | 3 | 2 |

| 8. | Financial Markets Department of the Ministry of Finance | Other authority | 5 | 1 |

| 9. | Association of Finnish Tax Advisors | Tax advisory interest group | 1 | 1 |

| 10. | Finnish Tax Administration | Tax authority | 4 | 3 |

| 11. | Large Taxpayers' Office | Tax authority | 4 | 3 |

| 12. | Marjaana Helminen | Tax professor | 5 | 1 |

| 13. | Seppo Penttilä | Tax professor | 4 | 2 |

Statements in the 2012 November parliamentary consultation_

| Statement | Stakeholder | Stakeholder group |

|---|---|---|

| 1. | Confederation of Finnish Industries | Corporate interest group |

| 2. | Federation of Finnish Enterprises | Corporate interest group |

| 3. | Finance Finland | Corporate interest group |

| 4. | Finnish Chamber of Commerce | Corporate interest group |

| 5. | Finnish Energy | Corporate interest group |

| 6. | RAKLI - The Finnish Association of Building Owners and Construction Clients | Corporate interest group |

| 7. | Taxpayers Association of Finland | Corporate interest group |

| 8. | The Family Business Network Finland | Corporate interest group |

| 9. | Attac Finland | Human rights based NGO |

| 10. | Association of Finnish Local and Regional Authorities | Municipalities interest group |

| 11. | City of Helsinki | Municipality |

| 12. | The Finnish Pension Alliance TELA | Pension funds interest group |

| 13. | Municipality Finance Plc | Public Authorities’ Finance company |

| 14. | The Association for Authorized Public Accountant (KHT-yhdistys ry) | Tax advisory interest group |

| 15. | The Association of Finnish Tax Advisors | Tax advisory interest group |

| 16. | The Finnish Bar Association | Tax advisory interest group |

| 17. | The Finnish Tax Administration | Tax authority |

| 18. | Marjaana Helminen | Tax professor |

| 19. | Heikki Niskakangas | Tax professor |

| 20. | The Central Organisation of Finnish Trade Unions SAK | Trade union |