How general is managerial human capital? Market-based views on managerial compensations explain high CEO compensation in the U.S. as resulting from the competition to employ scarce managerial talent (e.g., Gabaix and Landier, 2008; Terviö, 2008). However, the validity of these theories critically depends on the answer to this question. This question is also related to the sensitivity of managerial turnover to poor performance by a firm (e.g., Eisfeldt and Kuhnen, 2013). Thus, it is one of the most important empirical questions in the literature on corporate governance.

The empirical studies on the retention of managers after M&As may provide some evidence to assist in answering this question. Although several theories of takeovers presume that top managers in a target firm must be replaced after a takeover (1) , there is increasing evidence that the retention of a management group is important to the new firm (2) . This evidence suggests that there are important skills held by executives of a target firm that a new management group in an acquiring company cannot easily replace.

Interestingly, the existing literature finds that the tenure of a CEO does not have any significant effect on his/her probability of retention after takeover (e.g., Buchholtz et al., 2003; Wulf and Singh, 2011). Given that experience in a firm is assumed to result in the development of firm-specific skills, the lack of such an effect places doubt on the hypothesis that firm-specific skills are required to manage a newly merged firm after a merger and acquisition (M&A).

It appears that managers’ tenures may have a negative impact on their retention rate after an M&A. If it is expected that managers with long tenures will have difficulty adapting to the new environment - on the basis that the smaller number of firms in which their experience is gained reduces their opportunity to improve their general human capital - a newly merged firm may not want to employ a manager with a long tenure (e.g., Buchholtz et al., 2003). Therefore, this could offset the positive effect of tenure on the retention rate.

This paper examines how the tenure of managers influences the retention rate of a management group after M&As in Japanese companies during the period 1990–2006. It attempts to separate the two different hypotheses regarding the effect of tenure on separation probability. We show that negative and positive effects of tenure on the managers’ separation rate coexist in the case of Japanese M&As.

The main challenge to achieving our goal is developing a way to cope with the limitations of the data. Ideally, we need a fairly rich dataset, which includes the random assignment of target managers and their history afterward, including not only their career paths, but also wage payments and obtained skills. Unfortunately, it is not possible to obtain such data for Japanese firms. These data restrictions force us to develop a new model and a new method that can extract meaningful information from the restricted dataset. We develop a general equilibrium model that is designed to analyze the separation of target-firm managers after M&As. It is shown that our structural model can be approximately estimated by a stratified Cox proportional hazards model. In addition, we propose a novel method to correct for selection biases arising from unobserved heterogeneity of managers.

Equipped with the constructed theoretical model and the new estimation method, we conduct survival analyses of Japanese titled directors, who are considered to be the top executives in Japanese companies (3) . Because the Japanese promotion system is known to encourage investment in firm-specific human capital, we expect that the advantages and disadvantages of long tenure can be more accurately measured and investigated in Japanese companies than is the case for other countries.

We consider two sources of managerial human capital in this paper: experience as employees and managerial experience, which is measured by experience as a board member. Our empirical analyses show that an increase in a manager's tenure as an employee in a target company increases both the probability of being appointed to the board in a merged firm and the subsequent separation probability after this appointment. However, a longer tenure as a board member within the target firm does not have any significant impacts on either appointment probability or separation probability. Through the lens of our theory, we can interpret these findings as follows: 1) Japanese firms after M&As value both the target firm-specific human capital and the general human capital of managers; 2) experience as an employee increases firm-specific skills, but at the expense of the accumulation of general human capital; and 3) Managerial experiences are likely to be more general than those as an employee.

There have been many attempts to understand the retention of managers after M&As (4) . This paper makes two main contributions to the literature. First, to the best of our knowledge, ours is the first paper that constructs a structural model of managers’ retention after M&As. Second, we propose a novel method to correct for selection biases arising from the unobserved heterogeneity of managers, which does not require a random sample from the population. These two contributions are discussed in detail below.

We develop a structural model to disentangle the several mechanisms underlying the causal effects of tenure on the separation of target managers after M&As given several data limitations. However, in contrast to the standard structural estimation approach of, for instance, Rust (1987) and Hotz and Miller (1993), we do not attempt to estimate all structural parameters. Instead, we focus on particular parameters of interest, namely the coefficients of the effects of tenure on the separation rates. Our model is designed to clarify the conditions under which we can obtain economically meaningful interpretations from these parameters. Given the data limitations that we face, this strategy allows us to utilize weaker parametric assumptions for our identification, resulting in greater transparency of the source of variations for the identification (5) .

Let us describe the intuition on how to identify some mechanisms from the coefficients of the estimated effect of tenure on turnover in conditions where the data are constrained. In particular, we are concerned about two data problems: the lack of data about skills and the lack of data about compensation. First, because we cannot observe skills, we must differentiate two different hypotheses regarding the length of tenure and the separation probability of managers. Our identification strategy is built on the recognition that, although target-specific human capital is important as an input for current production, employment of managers with the ability to learn in a new environment is an investment in future production. More concretely, on the one hand, because managers in an acquiring firm do not have much knowledge of the target firm's organization, the acquirer initially regards the specific skills held by the target firm managers as highly valuable in managing and restructuring the target firm. On the other hand, because target managers accumulate knowledge of the new firm over time, the difference between the amount of knowledge accumulated by a manager who learns quickly and one who is a slow learner becomes larger as time goes by (6) . It is shown that the timing of separation reflects the relative importance of each type of human capital.

This seemingly intuitive argument requires nontrivial theoretical consideration of learning capability. Although the argument in the previous paragraph implicitly assumes that a newly merged firm is willing to employ managers with high learning capability, this may not be true. Because the ability to learn in a new environment is a general ability, the market competition can raise the compensation of able managers, which may make the firm reluctant to employ them. Therefore, the validity of the above argument depends on the structure of the external labor market for managers. Because we developed a general equilibrium model, we can discuss how the frictions in the managerial external labor market influence the coefficients of the effects of tenure on the separation probability.

In addition, the coefficients of the effects of tenure might be influenced by the second data problem: the lack of compensation data for Japanese managers. It is not obligatory for publicly traded companies to provide information on the compensation of managers in Japan. As suggested in the literature (e.g., Wulf, 2004, Hartzell et al., 2004, and Bargeron et al., 2009), this might cause several biases if managers in target firms can negotiate the compensation and severance pay in the newly merged firm during the process of an M&A. Our theoretical model shows that if it is impossible to make a complete contract on treatment of the new managers in the new firm during the M&A and there are some explicit or implicit transfers after the new firm starts as a result of ex post bargaining, then the separation probability does not depend either on the compensation or on the severance pay of managers. That is, the model provides a theoretical condition under which we can extract meaningful information from the coefficients of the impact of tenure on the separation rate even when compensation data are not available.

Next, we explain the second main contribution to the literature. In fact, this second contribution can be considered the more important contribution because it has a broader relevance than the post-M&A managerial retention literature. Note that because managers in a target company are not randomly assigned, the coefficient of tenure can be contaminated by another effect. If a talented person is promoted to a management position faster than is usually the case, the short tenures observed in our data may simply indicate that a manager has a high unobserved ability.

In order to deal with these selection biases, we propose a novel method to extract information about the unobserved heterogeneity of workers from the data on managers. Intuitively, if a talented person is promoted to a management position faster, the length of tenure prior to becoming a manager must contain useful information about their unobserved ability. We utilize this information to identify and control for unobserved ability to estimate the causal effects of tenure.

Compared with the standard sample selection models that have appeared in econometrics textbooks (e.g., Wooldridge, 2002; Cameron and Trivedi, 2005), our approach has three advantages. First, because we utilize the timing of selection in a selected sample to correct for selection bias, we do not need to access a random sample from the population. We are not aware of any other papers that provide a tractable method to correct a selection bias inherent to personnel data using only the selected sample. Second, because the timing of observations is generally different from the timing of promotions, we can find several exclusive variables that are required to identify parameters and obtain reliable estimates. Finally, although a standard two-step estimator makes distributional assumptions to correct selection biases, we rely on an extreme value theory to obtain robust results against misspecifications of distributional assumptions. Gabaix and Landier (2008) argue that an extreme value theory can provide a nice approximation for the upper tail of a large class of continuous distributions. We apply their argument and derive an explicit solution to the conditional expectation of unobserved ability under a selected sample, which is used to determine unbiased estimates of parameters under a selected sample.

As discussed before, this methodology is applicable to a broader literature than that of managerial retention after M&As. Although it is recognized that the characteristics of CEOs change the strategies of firms (e.g., Bertrand and Schoar, 2003), researchers face difficulties in examining the causal role of CEO characteristics in a firm because publicly available data on top managers typically involve selected samples. We propose a method to deal with this problem. Moreover, our methodology can be applied to data on internal promotions, when researchers are not able to access data on employees’ whole careers. We hope that this novel approach can help researchers struggling with data limitations to evaluate the role of leaders.

In addition to these two main contributions to the literature, our results contribute to several streams of literature, including those on managerial compensation and Japanese M&As. We clarify the contribution of our results to these fields in Section 8.

The paper is organized as follows. Section 2 presents a general equilibrium model of the separation of target managers after M&As. It shows how target firm-specific human capital and general human capital can influence the separation decision after M&As. Section 3 links the length of tenure and each type of human capital and provides a number of testable conditions that distinguish several hypotheses on managerial human capital based on the evidence of the effect of tenure on separation probability. Section 4 introduces our empirical model and discusses how to correct a selection bias using our selected dataset. Section 5 describes our Japanese dataset and Section 6 presents our estimation model and our results, interpreted through the lens of our theory. Section 7 discusses whether the moral hazard of managers could influence the interpretation of our results. Section 8 relates our results to several streams of literature that cover managerial compensation and Japanese M&As. Section 9 concludes the paper.

In this section, we construct a general equilibrium model that is designed to examine the separation of target managers after M&As using the following procedure. First, we discuss the assumptions on the production functions, which describe how target firm-specific human capital and general human capital influence the production process. Second, using the production functions, we model the separation of a manager from a target firm after an M&A by taking the outside values of managers as given. Third, we model an external managerial labor market, which allows us to determine the outside values of the managers. Finally, we show how our structural model can be approximately represented by the proportional hazards model and discuss how target firm-specific human capital and general human capital influence the parameters of the proportional hazards model.

Suppose that when a firm is merged with another firm, managers from the target firm must learn new skills and/or new routines to manage the merged firm in its new environment. We assume that all learning takes place at time t = 0 and that normal firm operations start after time t = 1, where the analysis time t is the length of time of operation after the year in which the new firm was created by the M&A. Assume that a manager in a target firm has general human capital hG and human capital specific to the target firm, hT. Suppose that the productivity of the manager with human capital h = {hG, hT} is described by pt(h):

The production technologies fGs and fTs depend on the state s. We use s = l to denote a learning state, whereas s = n denotes the normal operation state. We assume that

The assumption of

The assumption of

The assumption of

Now, we construct a model of managerial separation. The present value of the expected profit sequences from employing a particular manager, Jt(h) at t ≥ 1, can be described as follows:

We assume that firms review their managers every period. Assuming that the manager prefers to stay, which means that

Similarly, the present values of the sum of the expected income flows of managers in the firm at the analysis time t, Wt(h), can be described as follows:

We assume that:

We define the joint surplus of the manager and the new firm by

Suppose that the manager and the firm can negotiate

Proposition 1 shows that the separation decision does not depend on

In addition, Proposition 1 shows what determines the joint surplus. For any t, maintaining the relationship brings a joint instantaneous surplus of

Assume that ɛt is exponentially distributed with a parameter λ. The separation probability, qt, is shown to be a function of St(h), as follows:

This suggests that increases in the joint surplus, St(h), reduce the probability of separation.

Given this distributional assumption, the expected gain from separation is shown to be proportional to the separation probability.

Inserting the expected gain from separation into the dynamics of the joint surplus, we can rewrite equation (1) and summarize how the two types of human capital influence the separation probability using the following equations:

Note that both target firm-specific and general human capital influence the separation through an increase in productivity, pt(h). The general human capital has additional effects on the separation through a change in outside value, b(hG). Therefore, without knowing the structure of function b(hG), we cannot make any clear theoretical prediction on the impacts of general human capital on the separation probability.

We model an external labor market and endogenize

Suppose that managerial talent is a scarce resource and all firms competitively post an initial wage to attract a manager as long as profits are positive. Because of the price competition,

Similarly, the present values of the sum of the expected income flows of a manager who has a general skill hG at the state

We define the surplus under a normal operation as

Note that

Because

Using this result, we can summarize the separation probability derived from our general equilibrium model of the managerial separation after an M&A in the following proposition.

The separation probability of a target manager after an M&A is characterized by the following equations:

The proposition shows that not only the production function but also the hiring cost function influences the separation productivity of the target manager after an M&A.

We show how our structural model can be approximately represented by the proportional hazards model. The advantage of the proportional hazards model is that we do not need any parametric assumption on the basic hazard and, therefore, the model does not make any assumptions on the shape of the hazard over time. It is shown that without making any assumption on ζ(t: X), we can conduct our empirical analysis.

We assume that after the merger, a new firm faces a transition period and eventually converges to an operation state that is similar to those of other firms that did not experience an M&A. We derive an approximate solution of St(h). We decompose X and ζ(t: X) into two parts: X = (XZ, XV), νs (XV) and z (t:Xz) so that ζ(t: X) = νs (XV) + z (t: Xz), where s = {l, n}. Taking a first-order approximation of

Similarly, the present value of the stream of instantaneous joint surpluses at time 0, S0(h) can be expressed as:

Therefore, using the same approximation, we can show that:

The following proposition summarizes the results.

Separation probability can be estimated using the following proportional hazards model:

B (t: (XZ) = e−λZ(t:XZ) and I(t = 0) = 1 when t = 0 and I(t = 0) = 0 otherwise.

We assume that the acquiring firm appoints the manager in the target firm to the board of the new firm at the beginning of t = 0. Because the probability of being appointed a manager is equivalent to 1 − q0, investigating the separation probability in the initial period provides information about the appointment probability as well. As we discussed, we derive the basic hazard B(t: Xz) as a function of z(t + τ: Xz). Therefore, without making any parametric assumption on z(t + τ: Xz), we can conduct the estimation of this proportional hazards model.

Let us examine how target firm-specific and general human capital influence the parameters on the proportional hazards model. Because, for x = G or T,

The impacts of target firm-specific human capital and general human capital on the proportional hazards model can be analyzed by the following equations:

The impacts of target firm-specific human capital:

\matrix{ {\;\;\;\;\;\;\;\;\;\;\;{{\partial - \lambda {\Pi ^n}\left( {\bf{h}} \right)} \over {\partial {h^T}}} = {{ - \lambda f_{Tn}^{\prime}\left( {{h^T}} \right)} \over {1 - \beta \left( {1 - \hat q} \right)}} \le 0} \hfill \cr {\,\;\;\;\;\;\;\;\;\;\;{{\partial - \lambda \Delta \pi \left( {\bf{h}} \right)} \over {\partial {h^T}}} = - \lambda \left[ {f_{Tl}^{\prime}\left( {{h^T}} \right) - f_{Tn}^{\prime}\left( {{h^T}} \right)} \right] \le 0} \hfill \cr {{{\partial - \lambda \left[ {\Delta \pi \left( {\bf{h}} \right) + {\Pi ^n}\left( {\bf{h}} \right)} \right]} \over {\partial {h^T}}} = - \lambda \left[ {f_{Tl}^{\prime}\left( {{h^T}} \right) + {{\beta \left( {1 - \hat q} \right)f_{Tn}^{\prime}\left( {{h^T}} \right)} \over {1 - \beta \left( {1 - \hat q} \right)}}} \right] \le 0} \hfill \cr } 2. The impacts of general human capital:

\matrix{ {\;\;\;\;\;\;\;\;\;\;\;{{\partial - \lambda {\Pi ^n}\left( {\bf{h}} \right)} \over {\partial {h^G}}} = - \lambda \left[ {f_{Gn}^{\prime}\left( {{h^G}} \right) - f_{Gl}^{\prime}\left( {{h^G}} \right) + F'\left( {{h^G}} \right)} \right] \le 0} \hfill \cr {\,\;\;\;\;\;\;\;\;\;\;{{\partial - \lambda \Delta \pi \left( {\bf{h}} \right)} \over {\partial {h^G}}} = - \lambda \left[ {f_{Gl}^{\prime}\left( {{h^G}} \right) - f_{Gn}^{\prime}\left( {{h^G}} \right)} \right] \ge 0} \hfill \cr {{{\partial - \lambda \left[ {\Delta \pi \left( {\bf{h}} \right) + {\Pi ^n}\left( {\bf{h}} \right)} \right]} \over {\partial {h^G}}} = - \lambda F'\left( {{h^G}} \right) \le 0} \hfill \cr }

The first result in Proposition 4 shows that a rise in hT increases Πn(h) and Δπ(h) + Πn(h), and, therefore, always decreases the separation probability of managers. That is, because target firm-specific human capital always improves productivity,

The impacts of general human capital are more complicated. Because of the competition for general human capital, a rise in this type of human capital increases not only productivity, but also the cost of employing managers. Therefore, how general human capital influences the separation probability appears to be unclear. However, the second results in Proposition 4 provide clear theoretical predictions. That is, a rise in hG increases Πn(h) and Δπ(h) + Πn(h), and, therefore, always decreases the separation probability of managers. A rise in hG increases Δπ(h) + Πn(h) and, therefore, reduces q0 if it is difficult to find more able managers

In this section, we explain how we utilize the timing of separation to obtain information to distinguish two hypotheses on managerial human capital in a firm (i.e., an increase in target firm specific human capital and a reduction in the general ability to learn in a new environment) from the coefficients of the effect of tenure on separation probability. For this purpose, we propose testable hypotheses to interpret the relationship between tenure and separation probability.

Taking a first-order approximation, it is shown that:

Let τb and τe denote the manager's tenure as a board member and as an employee in the target firm, respectively. Following the tradition of labor economics, we assume that the target firm's firm-specific human capital is an increasing function of these tenures.

We assume that ηx ≥ 0 for x = b or e, which means that increases in both types of tenures assist in the accumulation of firm-specific human capital (8) .

On the other hand, as hG is a general skill, labor economists typically assume that hG increases not only as a result of experience in the target firm, i.e., as a result of both τb and τe, but also as a result of the duration of other experiences, τ0. Therefore, we have:

The parameters ωx − μ (x = b,e) capture the relative productivity of tenure for the accumulation of general human capital compared with other experiences. Buchholtz et al. (2003) argue that longer tenure may hamper the accumulation of general skills that are needed for adaptation to a new environment. This implies that ωx − μ < 0. Although this might be a reasonable assumption, we also allow for the possibility that ωx − μ > 0: i.e., that experience in a target firm can assist in improving general human capital. Several studies on spin-off effects suggest that previous experience in incumbent firms can be an important source of experience in establishing new firms (e.g., Klepper, 2001). It would be possible to apply a similar reasoning in this context. This possibility is captured by ωx − μ > 0.

The following proportional hazards model can be derived:

Using this derived hazard function, the theoretically predicted effects of tenure on separation probability are summarized as follows:

Investigating equations (7), (8), and (9) provides the following propositions that we wish to reject in our empirical study. The first proposition below shows the set of conditions under which a newly merged firm does not value any specific skills of employees in the target firm and/or any ability to learn in a new environment, and under which a market friction does not depend on the general human capital.

We assume that ηx ≥ 0 for both x = b and e.

Suppose that

f_{Gl}^{\prime}\left( {{h^G}} \right) \le f_{Gn}^{\prime}\left( {{h^G}} \right) F'\left( {{h^G}} \right) \ge 0 {\tilde \alpha _G} \ge {\bar \alpha _G} \ge 0 f_{Tn}^{\prime}\left( {{h^T}} \right) = f_{Tl}^{\prime}\left( {{h^T}} \right) = 0 {\tilde \alpha _T} = {\bar \alpha _T} = 0 (10) {\rm{sign}}\left[ {{{d\left( { - \lambda {\Pi ^n}\left( {\bf{h}} \right)} \right)} \over {d{\tau _x}}}} \right] = - {\rm{sign}}\left[ {{{d\left( { - \lambda \Delta \pi \left( {\bf{h}} \right)} \right)} \over {d{\tau _x}}}} \right] = {\rm{sign}}\left[ {{{\partial \left[ { - \lambda \left( {\Delta \pi \left( {\bf{h}} \right) + {\Pi ^n}\left( {\bf{h}} \right)} \right)} \right]} \over {\partial {\tau _x}}}} \right]. Suppose that

f_{Tl}^{\prime}\left( {{h^T}} \right) \ge f_{Tn}^{\prime}\left( {{h^T}} \right) \ge 0 {\bar \alpha _T} \ge {\tilde \alpha _T} \ge 0 - (a)

If

f_{Gl}^{\prime}\left( {{h^G}} \right) = f_{Gn}^{\prime}\left( {{h^G}} \right) {\bar \alpha _G} = 0 (11) {{d\left( { - \lambda \Delta \pi \left( {\bf{h}} \right)} \right)} \over {d{\tau _x}}} \le 0 - (b)

If

F'\left( {{h^G}} \right) = 0 {\tilde \alpha _G} - {\bar \alpha _G} = 0 (12) {{\partial \left[ { - \lambda \left( {\Delta \pi \left( {\bf{h}} \right) + {\Pi ^n}\left( {\bf{h}} \right)} \right)} \right]} \over {\partial {\tau _x}}} \le 0 - (c)

If

f_{Gl}^{\prime}\left( {{h^G}} \right) = f_{Gn}^{\prime}\left( {{h^G}} \right) F'\left( {{h^G}} \right) = 0 {\tilde \alpha _G} = {\bar \alpha _G} = 0 (13) {{d\left( { - \lambda {\Pi ^n}\left( {\bf{h}} \right)} \right)} \over {d{\tau _x}}} \le 0,{{d\left( { - \lambda \Delta \pi \left( {\bf{h}} \right)} \right)} \over {d{\tau _x}}} \le 0,{{\partial \left[ { - \lambda \left( {\Delta \pi \left( {\bf{h}} \right) + {\Pi ^n}\left( {\bf{h}} \right)} \right)} \right]} \over {\partial {\tau _x}}} \le 0

- (a)

The intuition behind equation (10) in Proposition 5 is explained as follows. If target firm-specific human capital does not increase productivity,

Similarly, we can explain the intuition behind equations (11) (12) and (13) in Proposition 5 as follows. If there are no benefits from learning capability

If the cost of hiring a new manager does not depend on the general human capital of the manager,

If there are no benefits from learning capability

Note that Proposition 5 requires that equations (10) and (11) are jointly satisfied by the coefficients for both the tenure as a board member, x = b, and the tenure as an employee, x = e. Because an acquiring firm does not care about how a target manager obtains a skill, if the skills are not profitable within the merged firm, the coefficients of tenure as a board member and as an employee will be influenced in a similar way. In other words, if the derived conditions are not satisfied for either x = b or x = e, we can reject the hypotheses in Proposition 5.

On the other hand, the difference between the coefficients for the two types of tenure, x = b and x = e, provides us with information about the differences in skills obtained as a result of experience gained as a board member or as an employee. The following proposition summarizes the hypotheses about specific human capital and experience that we wish to reject.

Suppose that

Equation (14) looks very similar to equation (10). The only difference is that Proposition 5 requires that equation (10) must be jointly satisfied for both x = e and x = b, whereas Proposition 6 states that we can separately use equation (14) for x = e and x = b. The intuition behind equation (14) is the same as that behind equation (10). However, by separately applying the same logic to the coefficients for the tenure as a board member and the tenure as an employee, we can determine differences in skills obtained from experience as a board member compared with experience as an employee.

Finally, the following proposition summarizes the hypotheses about general human capital and experience that we wish to reject.

Suppose that

If ωx ≥ μ, which means that a long tenure during x, where x = b or e, does not hamper the accumulation of general human capital relative to other experiences, then:

{{d\left( { - \lambda {\prod ^n}\left( {\bf{h}} \right)} \right)} \over {d{\tau _x}}} \le 0,{{\partial \left[ { - \lambda \left( {\Delta \pi \left( {\bf{h}} \right) + {\prod ^n}\left( {\bf{h}} \right)} \right)} \right]} \over {\partial {\tau _x}}} \le 0. If ωx ≤ μ, which means that a long tenure during x, where x = b or e, does not assist in the accumulation of general human capital relative to other experiences, then:

{{d\left( { - \lambda \Delta \pi \left( {\bf{h}} \right)} \right)} \over {d{\tau _x}}} \le 0.

If ωx ≥ μ, an increase in tenure assists in the accumulation of general human capital. Because an increase in tenure also increases valuable human capital specific to the target firm, a long tenure is valued by the newly merged firm and, therefore, it lowers the separation probability at all times.

However, if ωx ≤ μ, the opposite effect occurs. Because the human capital specific to the target firm is initially more highly valued, and because limited learning abilities do not initially cause any problem, the initial value of tenure is larger than its subsequent value. Therefore, a definite prediction of our theory is that the coefficient of tenure interacted with the t = 0 dummy must be negative. Equipped with the theoretical predictions outlined in this section, we now conduct our empirical study.

Suppose that XV can be decomposed into the characteristics of the target-firm manager and those of the firm to which the manager belongs. To analyze the determinants of the retention rate of target managers in a newly merged firm, we use the following stratified Cox proportional hazards model, which summarizes our theory:

This equation depends on the individual unobserved heterogeneity of a manager j at firm f, χfj. This unobserved heterogeneity may be the result of unobserved capabilities, or it may be the relationship with the founding family, main bank, or parent company. We do not know the cause of this heterogeneity, but we assume that the parameter χfj can summarize the effect of these heterogeneities. Without controlling for χfj, our estimates might be biased. As explained in footnote 3, we focus on titled directors in Japanese companies. However, talented workers may be appointed to titled director positions with less experience than less talented workers. Hence, χfj and τb,fj can be correlated.

In order to deal with this bias, we estimate unobserved abilities from our data and control for them in our survival analysis. The following argument explains how to estimate χfj.

Suppose that a person is appointed to a management position (titled director) in Japan if and only if:

From the definition of

Let us define a function R such that:

Given the estimates of

Hence, we seek to obtain unbiased estimators of

We define the deviation of the unobserved ability from the firm-level average in year

Note that

Therefore, if we know a functional form of

In order to implement this idea, we need to estimate

We need to estimate

Unfortunately, a random sample from the population is not available in our case. However, note that our conditional expectation of unobserved ability,

The remaining concern is determining what is a plausible distribution of

Our appendix proves the following lemma.

Suppose that

The assumption in Lemma 8 requires that the ability distribution has a finite upper bound, Q(0). Gabaix and Landier (2008) provide empirical evidence that supports this assumption using data on U.S. compensation of CEOs.

We assume that a function Q may differ across firms f and across years

In sum, we can obtain unbiased estimates of

Using

Below, we test the propositions outlined in the previous sections, focusing on M&As during the period 1990–2006 in Japan. We identify Japanese M&As in this period from the Delisting dataset, which is manually constructed from various sources of information, including Kaisha Nenkan 1969–2006, Kaisha Shikiho 2000–2006, and Tosho Yoran 1972–1973 and 1975–2007. This dataset contains information on delisted firms in exchange markets throughout Japan from 1968 to 2007. The information includes the stock code and name of the delisted firm, the listed market, dates of listing and delisting, the reason for delisting, and the name and the stock code of the new firm, when the reason given for delisting was a merger or an acquisition.

From the database, we selected those firms that had been delisted because of a “merger” or a “full-ownership acquisition” during the sample period (10) . When the firms that were delisted as the result of M&As involve a consolidation of assets and liabilities under a company with a stock code, we can observe who is retained in the new firm after the M&A as a board member. We select these types of delisted firms, and refer to them as “target firms”. In most M&As, one of the merging firms survives as the same firm with the same stock code. In other cases, mergers result in a new company with a new stock code. Our dataset includes both cases, and we refer to the post-merger firms in both cases as “new firms” in this paper. When we discuss surviving firms with the same stock codes after M&As, we refer to them as “acquirers” and we refer to all premerger firms that transacted with target firms during M&As as “other merged firms”.

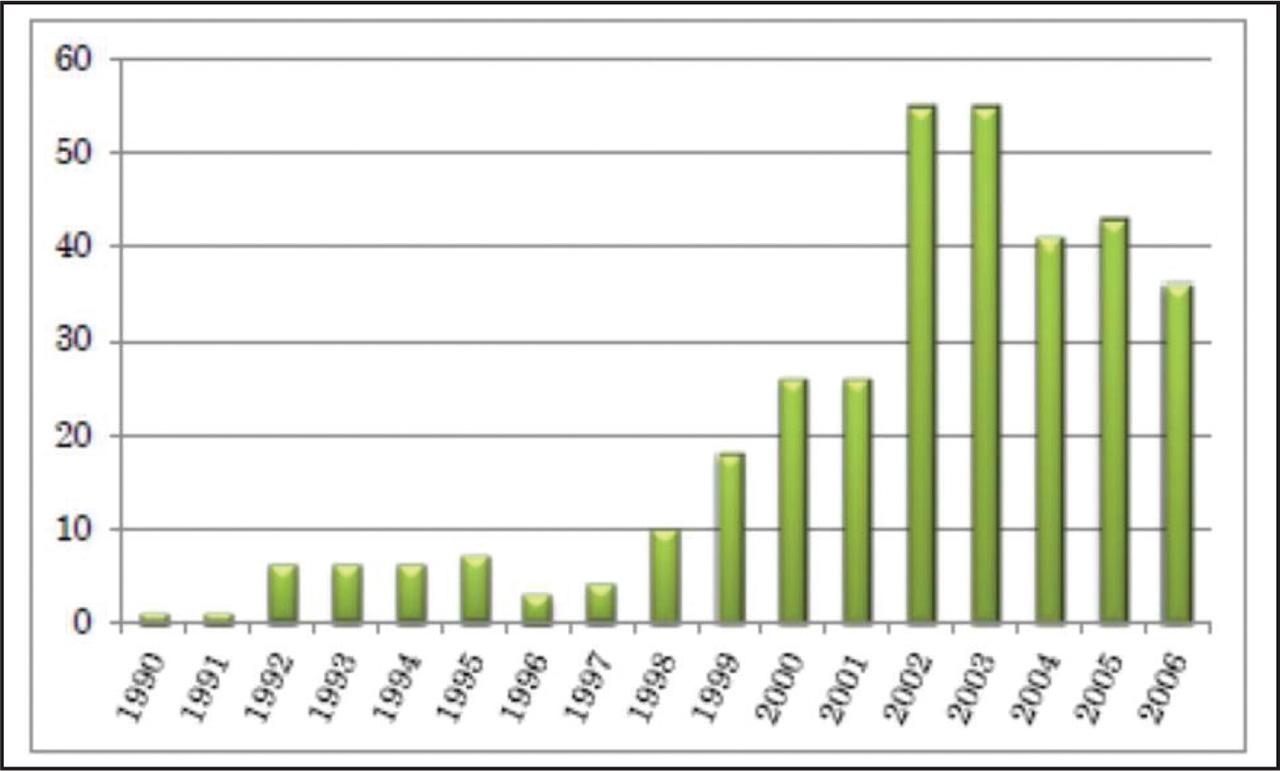

Our sample contains 344 M&A cases, comprising 123 mergers and 221 full-ownership acquisitions. Only mergers between listed firms are included. Figure 1 depicts the number of sample M&As over the study period. We can see that the number of M&As rapidly increased after 1998.

Number of M&As each year during the period 1990–2006.

The exchanges on which the target firms are listed include the Tokyo, Osaka, Nagoya, and other local stock exchanges, as well as emerging and over-the-counter markets. However, we exclude cases in the JASDAQ market because director-level data for these firms are available only after 2000.

We merge data on firm characteristics for the target firms and the new firms with the above M&A data. The data on firm characteristics are from the Nikkei NEEDS database. We first merge the three-digit Nikkei industry code for each target and new firm.

Table 1 presents the numbers of target and new firms in our sample, based on a two-digit industry classification (11) . The second column shows the number of target firms by industry, whereas the third column shows the number of new firms by industry. The fourth column shows the number of M&A cases where the target and new firms are from the same industry. We can see that M&As within the same industry occurred most often in the electronics industry.

Numbers of mergers and acquisitions by industry

| Industry | No. of target firms | No. of new firms | Both |

|---|---|---|---|

| Food | 15 | 16 | 14 |

| Textile | 7 | 8 | 5 |

| Pulp | 13 | 13 | 10 |

| Chemical | 19 | 21 | 14 |

| Pharmaceutical | 6 | 3 | 2 |

| Petroleum | 3 | 6 | 3 |

| Rubber | 2 | 1 | 1 |

| Ceramic | 14 | 13 | 10 |

| Iron ore | 7 | 13 | 7 |

| Nonferrous metal and metal | 15 | 18 | 10 |

| Machinery | 24 | 24 | 16 |

| Electronics | 27 | 46 | 24 |

| Shipbuilding | 0 | 1 | 0 |

| Automobile | 9 | 9 | 4 |

| Transport machinery | 6 | 0 | 0 |

| Precision instruments | 2 | 2 | 1 |

| Other manufacturers | 10 | 9 | 6 |

| Marine products | 1 | 0 | 1 |

| Mining | 4 | 2 | 2 |

| Construction | 26 | 26 | 16 |

| Trade | 43 | 32 | 22 |

| Retail | 27 | 31 | 21 |

| Other financial businesses | 2 | 4 | 2 |

| Real estate | 11 | 1 | 1 |

| Rail and bus | 2 | 12 | 2 |

| Land transportation | 2 | 4 | 2 |

| Marine transportation | 7 | 6 | 6 |

| Air transportation | 1 | 3 | 1 |

| Telecommunications | 4 | 2 | 2 |

| Electricity | 0 | 2 | 0 |

| Service | 35 | 15 | 13 |

| Total | 344 | 344 | 218 |

Next, we merge the financial characteristics in the Nikkei NEEDS database with our sample. More specifically, we merge operating income, sales, number of full-time employees, personnel expenses, total assets, and the stock share of the top ten stockholders for each target firm. These variables are explained in detail below. We also merge operating income, total assets, and the stock share of the top ten stockholders of the acquirer of the target firm in the year prior to the M&A if there is a surviving firm with the same stock code. For cases of M&As without any surviving firm, we use the average value of these variables for all other merged firms instead to represent those of the acquirer.

Next, we merge the firm-level data with the director-level data. The data for board members are taken from the Directors data published by Toyo Keizai. This database contains information on the directors of all listed firms in Japan from 1990 to 2007. The information includes the title, the date the person entered the firm, and a personal history of the board member, along with the name and date of birth.

Because we are interested in the retention of Japanese executives after M&As, we focus our analysis on directors with titles in the sample target firms (12) . Therefore, our sample comprises all directors with titles at target firms in the year of the M&A (13) . As explained in footnote 3, following the arguments by Kaplan (1994) and Saito and Odagiri (2008), we consider titled directors to be the top executives in Japanese companies. In the following sections, we analyze whether executives in target firms are retained as board members in the new firms after M&As.

We have 1520 observations (titled directors) for 343 targets, with an average of 4.43 titled directors per target. We specify the date of birth, title, the date a person entered the firm, and her/his history as a board member. We also identify the number of other firms (including the target firm itself) in which target-firm managers served as board members in the year of the M&A.

From the Directors data, we determine whether a target manager was retained as a board member (with or without a title) in the new firm after the M&A and, if so, how many years he/she stayed on the board after the M&A (14) . In addition, we identify whether a target-firm manager served as a board member of the acquirer before the M&A.

Table 2 provides summary statistics of the managers’ retention characteristics. The first variable (retained) takes a value of one if the target manager became a board member of the new firm after the M&A and is zero otherwise. The second variable (years of survival if retained) is the number of years that the retained target manager served as a board member of the new firm after the M&A. The table shows that only 38.7% of the target managers were retained as board members after M&As and that the retained managers kept their positions for an average of less than five years.

Characteristics of target directors

| Variable | No. of observations | Mean | S.D. | Min. | Max. |

|---|---|---|---|---|---|

| Retained | 1520 | 0.387 | 0.487 | 0 | 1 |

| Years of survival if retained | 588 | 4.117 | 2.190 | 1 | 16 |

Using the dataset explained above, we first conduct a GMM estimation using equations (19), (20), and (21) to obtain the unobserved individual ability defined in equation (22).

The summary statistics of the variables used in the GMM estimation can be found in Table 3. The first four variables are those of the manager's tenure history, which determine his/her human capital at

Summary statistics

| Variable | No. | Mean | S.D. | Min. | Max. |

|---|---|---|---|---|---|

| Tenure as a board member at

| 1520 | 2.70 | 2.91 | 0.00 | 20.92 |

| Tenure as a board member at

| 1520 | 8.50 | 7.41 | 0.25 | 56.42 |

| Tenure as an employee (years) | 1520 | 11.82 | 13.59 | 0.00 | 43.17 |

| Outside experience (years) | 1520 | 40.35 | 15.62 | 15.17 | 71.17 |

| Age (years) | 1520 | 60.67 | 5.54 | 35.08 | 90.92 |

| Variables in

| |||||

| Negative operating income at

| 1520 | 0.15 | 0.36 | 0.00 | 1.00 |

| Negative operating income at

| 1520 | 0.21 | 0.41 | 0.00 | 1.00 |

| Direct | 1520 | 0.20 | 0.40 | 0.00 | 1.00 |

| No. of employees at

| 1520 | 1.70 | 2.65 | 0.006 | 23.87 |

| No. of employees at

| 1520 | 1.53 | 2.24 | 0.006 | 16.35 |

| Wage at

| 1520 | 4.25 | 3.37 | 0.08 | 28.39 |

| Wage at

| 1519 | 5.03 | 3.89 | 0.21 | 25.57 |

| Median tenure as a titled director at

| 1520 | 4.89 | 4.00 | 0 | 33.17 |

| Median tenure as a titled director at

| 1520 | 4.61 | 3.19 | 0.50 | 24.67 |

| Median age of titled directors at

| 1520 | 55.35 | 4.34 | 27.58 | 69.17 |

| Variables in

| |||||

| Sales (1000 million yen) | 1520 | 146.78 | 256.95 | 0.68 | 2877.40 |

|

| |||||

| Median value of tenure as a board member at

| 1520 | 7.48 | 4.17 | 0.25 | 32.42 |

| Median value of tenure as an employee (years) | 1520 | 10.84 | 12.17 | 0.00 | 35.83 |

| Median value of outside experience (years) | 1520 | 40.20 | 13.66 | 20.42 | 68.42 |

| Manager characteristics | |||||

| No. of firms as a board member | 1520 | 1.14 | 0.51 | 1.00 | 10.00 |

| Board member in the acquirer before the M&A | 1520 | 0.15 | 0.35 | 0.00 | 1.00 |

| Upper | 1520 | 0.31 | 0.46 | 0.00 | 1.00 |

| Target ROA | 1520 | 0.00 | 0.06 | −0.43 | 0.52 |

| Firm characteristics | |||||

| Log target assets | 1520 | 11.07 | 1.35 | 6.92 | 14.61 |

| Board size | 1520 | 5.77 | 2.73 | 1.00 | 15.00 |

| Log stock share of top 10 | 1520 | −6.89 | 1.35 | −8.39 | −0.14 |

| Target firm's relative size in assets | 1520 | 0.27 | 0.23 | 0.00 | 0.99 |

| Related | 1520 | 0.48 | 0.50 | 0.00 | 1.00 |

| Acquisition | 1520 | 0.61 | 0.49 | 0.00 | 1.00 |

| Acquirer or others ROA | 1520 | 0.00 | 0.06 | −0.68 | 0.60 |

| Log top 10 share of acquirer or others | 1520 | −7.09 | 1.56 | −8.89 | 0.00 |

For the variables that determine the human capital level required for appointment to a managerial position (a titled director position),

Direct is an indicator variable that takes a value of one if the manager is hired from outside the firm. We control for this variable because the required human capital level may differ depending on whether the manager is selected from among the employees of the firm or is hired from outside. We control for the number of employees to estimate the required human capital level because more employees may mean there is more intense competition to become a manager on the board. Therefore, we expect that the number of employees will have a positive effect on the required human capital level. Similarly, a higher average wage may imply that employees of the firm have a higher average human capital level. Therefore, a greater level of human capital may be required for appointment to a titled director position. The average wage is calculated using the number of employees and the personnel expenses of the target firm.

We include the median length of tenure as a titled director within a firm and consider the turnover rate of titled directors to be low if the tenure length as a titled director is high, on average. In such cases, it is more difficult to become a titled director. We also control the median value of age in the merger year. If a firm has the high median age, it is likely that the firm set a high requirement to become a titled director. Therefore, we expect its coefficient to be positive.

For a variable in a vector

Once we obtain the unobserved individual ability,

For the variables in the vector XD,f,j, we use the manager's age at the time of the M&A (Age), the number of firms in which the target manager served as a board member (No. of firms as a board member), whether the target manager was a board member in the acquirer before the M&A (Board member in the acquirer before the M&A), and whether the target manager was the president or chairman of the board of directors (Upper). These variables are calculated from the Directors data, as explained in the previous section. We include the target firm's performance as a manager characteristic to measure the manager's ability. To represent the target firm's performance, we use the return on assets (ROA) in the year prior to the M&A, where the ROA is defined as operating income divided by assets, measured using the deviation from the industry median. Note that this measure is at the firm level, even though we consider it as a manager characteristic, as suggested by Wulf and Singh (2011).

The target firm's characteristics in XF,f include firm size and the board size of target firms. To control for the target firm's size and its board size, we include the logarithm of the target firm's assets in the year prior to the merger (Log target assets) and the number of board members (Board size). The previous literature has considered the target firm's size to be important because larger and more complex firms may require managers with unique skills, which may increase the retention rate of managers (Finkelstein and Hambrick, 1989) (17) . We include the board size of the target firm because an increase in the number of managers may reduce the productivity of managers in a target firm. The board size of the target company is also important for another reason: between 1990 and 2006, many companies reduced the size of their boards. If we do not control for board size, the coefficient on tenure may capture this effect as well. Our theory is based on the presumption that there are some explicit or implicit transfers that have to be negotiated after the M&A. Although we believe that this is a plausible assumption, some may argue that this may not be true. If so, the initial contracts resulting from the ex ante strategic bargaining during the M&A can influence the separation probability. To estimate the importance of ex ante strategic bargaining, Bargeron et al. (2009) control for a measure of the ownership structure, specifically, the level of insider ownership in a target firm. Following this idea, we include the logarithm of the stock share of the top 10 stock holders (log stock share of top 10) in XF,f, so that we can minimize the bias even if our assumptions are not valid. We expect that the impact of strategic retention would be smaller if the value of this variable were larger because large shareholders have more incentive to monitor managers under a concentrated ownership structure.

The transaction characteristics in XF,f include the relative size of the target firm. If the firm is large, the postmerger integration may be more difficult and, therefore, we would expect the likelihood of manager retention to be higher (Zollo and Singh, 2004). To measure relative firm size, we calculate the ratio of the target firm assets to the acquirer assets if there is a surviving firm with the same stock code. For cases of M&As without any surviving firm, we use the total assets of all other merged firms in place of the acquirer assets. Following the previous literature, including Walsh (1989) and Buchholtz et al. (2003), we include a dummy variable that represents whether the target and the new firm operate in the same industry as a transaction characteristic. More specifically, we create an indicator variable that is equal to one if the new and target firms operate in the same three-digit Nikkei industry code (i.e., medium industry classification) and is zero otherwise (Related). We also include a full-ownership acquisition dummy to observe whether mergers and full-ownership acquisitions have different effects on the retention rate (Acquisition).

We control for the governance characteristics of the other merged firms. Specifically, we control for the ROA and the stock share of the top 10 stock holders of the acquirer if there is a surviving firm with the same stock code. For cases of M&As without any surviving firm, we use the average value of these variables for all other merged firms in place of the acquirer values (“Acquirer or others ROA” and “Log top 10 share of acquirer or others”).

The summary statistics of these variables, which appear exclusively in the stratified Cox proportional hazards estimation, are shown in the last two groups in Table 3. In addition to these variables, we need tenure as a board member at

In addition, for the vector Xz,f in equation (23), we include two-digit industry codes for a new firm and a target firm and the year of the M&A. This means that we allow the baseline hazard functions to differ for these groups. Note that because hazard rate depends on year after M&A, controlling the year of the M&A helps avoiding the impact of economic conditions. Finally, we construct an initial dummy that assigns a value of one for the initial year (t = 0) and zero for any other separation time (18) .

Table 4 shows the results of our GMM estimation using equations (19), (20), and (21). In addition to the variables explained in the previous section, we include two-digit industry dummies and decade dummies in

GMM estimation

| Variable | Coef. | Std. Err. |

|---|---|---|

| Negative operating income | −0.636 | 0.404 |

| Direct | −1.964 | 1.030 * |

| No. of employees | 0.000 | 0.000 |

| Wage | 0.242 | 0.049 *** |

| Median tenure as a titled director | 0.025 | 0.028 |

| Median age | 0.801 | 0.253 *** |

| Constant

| 73.183 | 13.474 *** |

| Tenure as an employee (ϕe) | 0.400 | 0.230 * |

| Outside experience

| 0.382 | 0.224 * |

| 1/(ζ + 1) | 0.663 | 0.051 *** |

| Sales | 0.000 | 0.000 * |

| Industry code dummy | Yes | |

| Decade dummy | Yes | |

| Number of observations | 1519 | |

1. Instruments for the equation: negative operating income, direct no. of employees, wage, median tenure as a titled director, median age as a titled director, median tenure as a board member, median tenure as an employee, median outside experience, sales, and decade and industry dummy for both

2. ***, ** and * denote statistical significance at the 1%, 5%, and 10% significance levels. Standard errors are calculated using bootstrap methods.

We can see in Table 4 that the signs of the coefficients of the variables in the R function in equation (20) are all as expected. That is, a higher number of employees, higher wages, higher median tenure as a titled director, and higher median age seem to make it more difficult for a director to be appointed as a titled director, whereas poor performance of the current management makes it easier. The coefficient of Direct is negative, indicating that the human capital level required to be appointed to a titled director position is lower for managers from outside the firm. The coefficients for Direct, Wage, and Median age are statistically significant.

The results show that the coefficients for both tenure as an employee and outside experience are positive, implying that these variables raise individuals’ human capital. However, because the values of these coefficients are smaller than one, their effect on human capital is smaller than that of tenure as a board member, i.e., experience as a board member seems to be more important for promotion to a management position than is experience as an employee. We estimate 1/(ζ + 1) and obtain a value such that 0 < 1/(ζ + 1) < 1 without imposing any restrictions on estimation. This is consistent with the assumption of ζ > 0 in Lemma 8. The coefficients of the variables that affect the manager's human capital are all statistically significant. The coefficient of sales that appears in

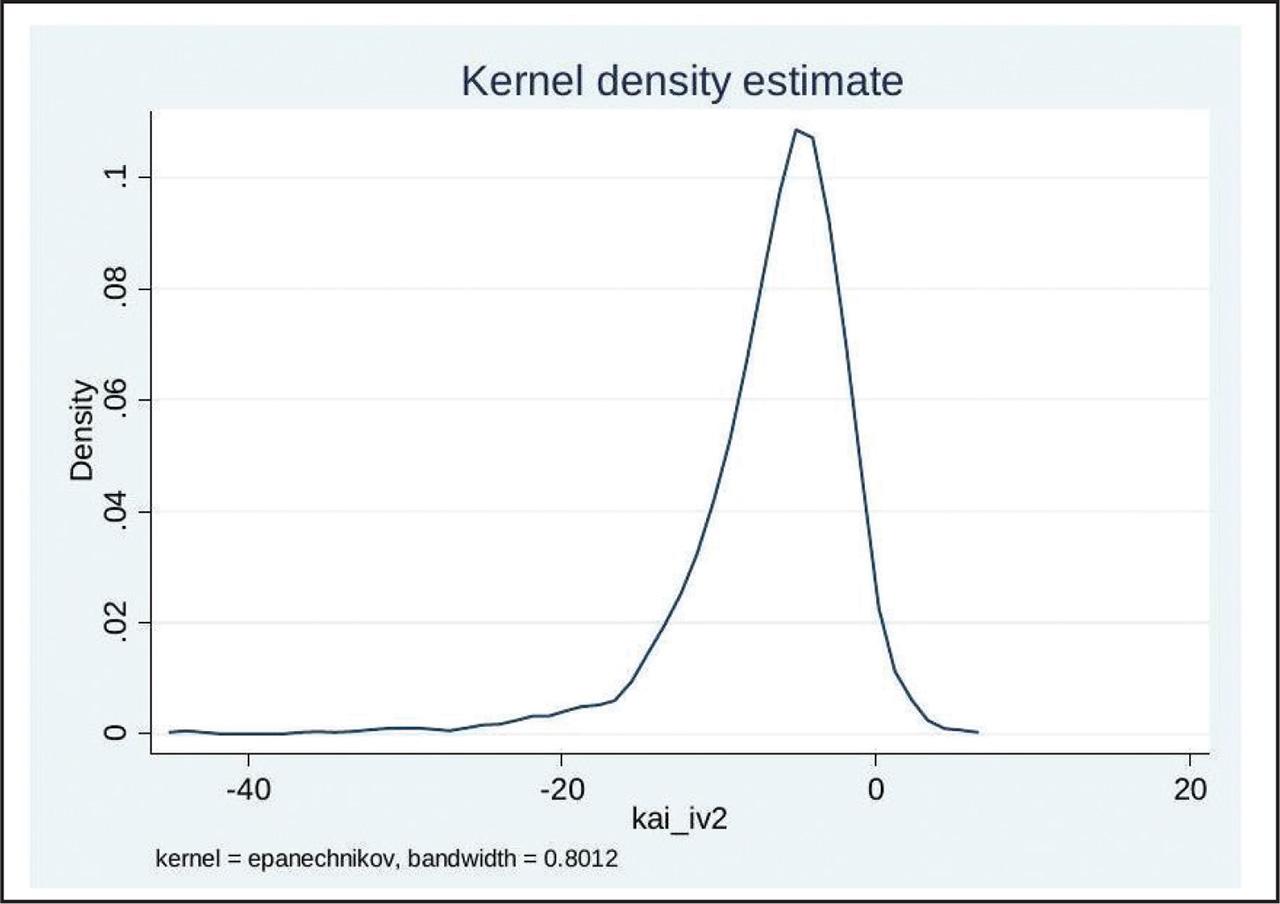

Using the estimated parameters, we obtain the unobserved ability,

Estimated unobserved skill

| Obs. | Mean | Std. Dev. | Min. | Max. | |

|---|---|---|---|---|---|

|

| 1520 | −6.606 | 5.104 | −44.191 | 5.654 |

Kernel density of estimated unobserved skill.

Tables 6 and 7 show the results of our stratified Cox proportional hazards model estimation using equations (23), (24), and (25). All results pass the test of the proportional hazards assumption, based on the test of nonzero slope in a generalized linear regression of the scaled Schoenfeld residuals on a natural log of the analysis time at the 5% level. For equations (1) and (3), the standard errors are obtained using 1000 bootstrap samples.

Stratified Cox proportional hazards model estimation

| Variable | (1) | (2) | ||

|---|---|---|---|---|

| Coef. | Std. Err. | Coef. | Std. Err. | |

| 1: Tenure as a board member | 0.006 | 0.024 | −0.010 | 0.009 |

| 2: Tenure as an employee | 0.011 | 0.007 * | 0.011 | 0.005 ** |

| 3: Tenure as a board member × initial dummy | −0.012 | 0.024 | 0.002 | 0.010 |

| 4: Tenure as an employee × initial dummy | −0.014 | 0.007 ** | −0.014 | 0.005 *** |

| Age | 0.112 | 0.031 *** | 0.100 | 0.016 *** |

| Board size | 0.097 | 0.081 | 0.105 | 0.049 ** |

| No. of firms as a board member | −0.166 | 0.215 | −0.179 | 0.137 |

| Board member in the acquirer before the M&A | −0.106 | 0.479 | −0.108 | 0.308 |

| Acquisition | −0.025 | 0.797 | 0.003 | 0.495 |

| Target ROA | −11.913 | 7.626 | −11.335 | 3.860 *** |

| Related | 0.117 | 0.562 | 0.034 | 0.374 |

| Target firm's relative size in assets | −0.990 | 0.530* | −0.942 | 0.433 ** |

| Log target assets | −0.026 | 0.216 | −0.066 | 0.133 |

| Upper | −0.277 | 0.198 | −0.264 | 0.132 ** |

| Log stock share of top 10 | −0.460 | 0.355 | −0.455 | 0.194 ** |

| Acquirer or others ROA | −3.164 | 6.143 | −2.214 | 3.368 |

| Log top 10 share of acquirer or others | 0.134 | 0.265 | 0.092 | 0.162 |

|

| 0.044 | 0.039 | ||

| Age × I(t = 0) | −0.072 | 0.031 *** | −0.061 | 0.017 *** |

| Board size × I(t = 0) | −0.073 | 0.082 | −0.080 | 0.051 |

| No. of firms as a board member × I(t = 0) | −0.293 | 0.248 | −0.281 | 0.184 |

| Board member in the acquirer before the M&A × I(t = 0) | −0.114 | 0.482 | −0.116 | 0.312 |

| Acquisition × I(t = 0) | 0.729 | 0.819 | 0.702 | 0.525 |

| Target ROA × I(t = 0) | 11.813 | 7.691 | 11.198 | 3.910 *** |

| Related × I(t = 0) | −0.383 | 0.577 | −0.300 | 0.388 |

| Target firm's relative size in assets × I(t = 0) | −0.210 | 0.567 | −0.257 | 0.464 |

| Log target assets × I(t = 0) | 0.012 | 0.220 | 0.054 | 0.138 |

| Upper × I(t = 0) | −0.007 | 0.207 | −0.017 | 0.143 |

| Log stock share of top 10 × I(t = 0) | 0.504 | 0.357 | 0.503 | 0.200 ** |

| Acquirer or others ROA × I(t = 0) | 5.533 | 6.241 | 4.636 | 3.577 |

| Log top 10 share of acquirer or others × I(t = 0) | −0.161 | 0.269 | −0.120 | 0.165 |

|

| −0.037 | 0.039 | ||

| Wald Test | Coef. | Chi2(1) | Coef. | Chi2(1) |

| 1 + 3 | −0.006 | 1.28 | −0.008 | 5.31 ** |

| 2 + 4 | −0.003 | 2.71 * | −0.003 | 3.74 * |

| Number of observations | 2108 | 2108 | ||

Stratified by year, acquirer industry code, and target industry code.

***, **, * denote statistical significance at the 1%,5%, and 10% significance levels.

Standard errors are calculated by bootstrap methods.

Stratified Cox proportional hazards model estimation

| Variable | (1) | (1) | ||

|---|---|---|---|---|

| Coef. | Std. Err. | Coef. | Err.ef. | |

| 1: Tenure as a board member | −0.002 | 0.022 | −0.016 | 0.009 |

| 2: Tenure as an employee | 0.010 | 0.006 * | 0.010 | 0.005 * |

| 3: Tenure as a board member × initial dummy | −0.005 | 0.022 | 0.007 | 0.010 |

| 4: Tenure as an employee × initial dummy | −0.013 | 0.006 ** | −0.012 | 0.005 *** |

| Age | 0.116 | 0.026 *** | 0.107 | 0.016 *** |

| Board size | 0.036 | 0.020 * | 0.039 | 0.046 ** |

| No. of firms as a board member | −0.358 | 0.094 *** | −0.361 | 0.082 *** |

| Board member in the acquirer before the M&A | −0.229 | 0.074 *** | −0.232 | 0.064 *** |

| Acquisition | 0.579 | 0.156 *** | 0.578 | 0.139 *** |

| Target ROA | −0.466 | 1.000 | −0.463 | 4.068 |

| Related | −0.244 | 0.106 ** | −0.252 | 0.097 *** |

| Target firm's relative size in assets | −1.016 | 0.437 ** | −1.006 | 0.374 *** |

| Log target assets | −0.036 | 0.053 | −0.040 | 0.049 |

| Upper | −0.279 | 0.059 *** | −0.275 | 0.133 *** |

| Log stock share of top 10 | −0.009 | 0.057 | −0.008 | 0.195 |

| Acquirer or others ROA | 1.223 | 1.439 | 1.370 | 1.219 |

| Log top 10 share of acquirer or others | −0.028 | 0.047 | −0.035 | 0.043 |

|

| 0.036 | 0.033 | ||

| Age × I(t = 0) | −0.076 | 0.026 *** | −0.069 | 0.017 *** |

| Board size × I(t = 0) | ||||

| No. of firms as a board member × I(t = 0) | ||||

| Board member in the acquirer before the M&A | ||||

| Acquisition × I(t = 0) | ||||

| Target ROA × I(t = 0) | ||||

| Related × I(t = 0) | ||||

| Target firm's relative size in assets × I(t = 0) | −0.294 | 0.484 | −0.289 | 0.414 |

| Log target assets × I(t = 0) | ||||

| Upper × I(t = 0) | ||||

| Log stock share of top 10 × I(t = 0) | ||||

| Acquirer or others ROA × I(t = 0) | ||||

| Log top 10 share of acquirer or others × I(t = 0) | ||||

|

| −0.027 | 0.034 | ||

| Wald Test | Coef. | Chi2(1) | Coef. | Chi2(1) |

| 1 + 3 | −0.006 | 1.18 | −0.009 | 5.58 ** |

| 2 + 4 | −0.003 | 2.95 * | −0.003 | 4.08 ** |

| Number of observations | 2108 | 2108 | ||

Stratified by year, acquirer industry code, and target industry code.

***, **, * denote statistical significance at the 1%,5%, and 10% significance levels.

Standard errors are calculated using bootstrap methods.

Specification (1) in Table 6 is our benchmark specification. The result for specification (1) shows that the coefficient of tenure as a board member is not significant, whereas the coefficient of tenure as an employee is positive and significant. The coefficient of tenure as a board member with an initial dummy is not significant, whereas the coefficient of tenure as an employee with an initial dummy is negative and significant. The sum of tenure as a board member and that with an initial dummy is negative, as is the sum of tenure as an employee and that with an initial dummy. A Wald test shows that the latter summed variable is statistically significant, whereas the former is not. The results indicate that, whereas the tenure as a board member has no impacts on the separation probability after M&As, irrespective of timing, a longer tenure as an employee increases the separation rate and the probability of appointment as a board member in a new firm, with statistical significance.

The coefficient for age is positive and significant, whereas that for age with an initial dummy is negative and significant. The sum of these variables is positive. Therefore, older managers are less likely to be retained either in the initial year after an M&A or in the years after.

Because many other control variables are insignificant in Specification (1), we suspect that there may be some multicollinearity among variables. Hence, we drop the variables with initial dummies for which both the level and interaction terms are insignificant in Specification (1). The result is shown as Specification (3) in Table 7. It is shown that the results on tenures are the same and, therefore, are robust.

The coefficients of many other control variables become significant in Specification (3). Specifically, the coefficient of board size is positive and significant. This may imply that the productivity of managers decreases with the number of managers. The results also indicate that managers who serve as board members in different companies have a lower separation rate. We can see that managers who were in the acquirer before the M&A and managers who belonged to a target firm in the same industry as the new firm are likely to be retained on the board of the new firm. This may imply that acquirer-specific knowledge and industry-specific knowledge are appreciated by the new firm. We can also see that the target managers are less likely to be retained in cases of acquisition and that higher-level managers (Upper) are more likely to be retained.

Specifications (2) and (4) are the same as Specifications (1) and (3), respectively, except that the former do not include the estimated unobserved skill,

Now, we wish to interpret the results using our theory. We first apply Proposition 5 to interpret the results of our estimation. Because the conditions in Proposition 5 must be satisfied by the coefficients of both tenure as a board member and tenure as an employee, if the coefficients of either type of tenure can reject the conditions, then the corresponding hypothesis in Proposition 5 is rejected. First, let us test hypotheses 1 and 2 in Proposition 5 using the result for tenure as an employee. Our estimated results on the coefficient of tenure as an employee, the coefficient of tenure as an employee with the initial dummy, and the sum of these two coefficients correspond to

Next, we separately investigate the role of tenure as a board member and that of tenure as an employee after M&As. Let us first apply Proposition 6 to the estimated results for the tenure as an employee. It shows that the evidence for tenure as an employee,

On the other hand, the relevant coefficients for tenure as a board member are not statistically significant, and we are not able to reject the hypothesis that experience as a board member does not increase firm-specific skills and does not have a larger influence on the accumulation of general human capital relative to other experiences. Without rejections of any null hypotheses, we cannot make a strong argument in relation to the effects of experience as a board member. However, our result seems to be consistent with the argument that experience as a board member does not involve firm-specific human capital and does not hamper the accumulation of general human capital. Hence, it is likely that managerial experiences are more general than those as an employee.

In summary, we can interpret our results as follows. 1) After an M&A, Japanese firms value both the target firm-specific human capital and the general human capital of managers. 2) Experience as an employee increases firm-specific skills, but at the expense of the accumulation of general human capital. 3) Managerial experiences are likely to be more general than those as an employee.

In this section, we discuss whether the moral hazard of managers could influence our interpretation. In line with the literature, including Wulf (2004), Hartzell et al. (2004), and Bargeron et al. (2009), we note that managers with long tenures in target firms may become very powerful and attempt to protect “their position” as much as possible in the event of M&As.

As this paper shows, as long as ex post bargaining is possible without any costs, we do not need to be concerned about this possibility. In fact, although we control for a measure of the ownership structure using the logarithm of the stock share of the top 10 stock holders, it does not have any significant impacts on the separation rate. This strongly suggests that the entrenchment story may not be a serious problem for M&As in the Japanese context.

Of course, this may not be taken as conclusive evidence to justify our presumption. If the ex post negotiation is costly, these managers would remain very powerful in the initial period and the acquiring firms would find it difficult to fire them. However, eventually, the power of these managers would be eroded such that, finally, it would become possible for the new firms to fire them. Thus, this kind of entrenchment story may be able to explain the coefficient of tenure in our survival analysis.

To the extent that the power of these managers is the source of their productivity, there is no reason to distinguish their power from their target firm-specific skills. In this case, the above story can be consistent with the story that we have presented. However, it is possible that a powerful manager could be unproductive. Unfortunately, we do not have conclusive evidence that can reject this kind of entrenchment story. Nevertheless, there are at least three reasons to consider that the entrenchment of powerful but unproductive managers is not important for our results. First, the entrenchment argument is consistent with our coefficient of tenure as an employee, but it is inconsistent with the coefficient of tenure as a board member. These results are peculiar because we would expect that tenure as a board member would be a more appropriate measure of power in a firm than tenure as an employee. Second, because it is impossible, in reality, to write an explicit contract for all possible contingencies, powerful managers should anticipate that they will eventually lose their power. If so, it is not theoretically clear why they would initially agree to a merger. Most mergers in Japan are friendly and, therefore, if the managers are very powerful, they could potentially oppose them. This suggests that managers do not possess the degree of power required to support the entrenchment argument. Finally, senior people typically have more authority in Japanese society than do younger people. Hence, it is possible that power in a firm could be captured by age rather than tenure. In fact, the coefficient of age is significantly positive, the interaction with the initial dummy is significantly negative, and the sum of the two coefficients is significantly positive, which indicates that senior managers are less likely to be appointed as board members of a new firm. This is to be expected when these managers are less productive, despite their power in the initial years. Therefore, we expect that, after controlling for age, the entrenchment story will have little effect on the coefficient of tenure.

In addition to our methodological contributions to the literature, our results have a number of important implications for several streams of literature, including those on managerial compensation and Japanese M&As. This section discusses how our results contribute to these fields.

First, evidence about the transferability of managerial skills between Japanese firms can provide a useful basis and comparison for the discussion of sources of high compensation for U.S. CEOs. As Bertrand (2009) and Frydman and Jenter (2010) show, some researchers consider the high compensation of U.S. CEOs to be the result of powerful managers setting their own pay rates, whereas others consider it to be the result of a competitive market for managerial talent. One of the key presumptions behind the market-based view (e.g., Gabaix and Landier, 2008; Terviö, 2008) is that important managerial skills are transferable across firms. Indeed, Murphy and Zábojník (2004) and Frydman (2005) argue that a rise in the importance of a CEO's general skills relative to his/her firm-specific skills can explain not only the increase in CEO compensation but also the increase in the turnover rate that has occurred since 1970. Kaplan et al. (2012) investigate a proprietary dataset for executives and provide evidence that general skills are important managerial skills. Our results, focusing on the Japanese context, provide evidence that complements this U.S.-based literature; the transferability of managerial human capital depends on the source of managerial human capital. We find that whereas managerial human capital accumulated through experiences as an employee is firm specific, managerial experiences are likely to be more general than those gained as employees, even though the promotion structure of Japanese firms is considered to facilitate the accumulation of firm-specific skills to a particularly large extent (e.g., Mincer and Higuchi, 1988).

It should be noted that Japanese managers receive far less cash compensation than do their U.S. counterparts (19) and that Japanese CEOs have very long tenures at their firms relative to CEOs in U.S. firms (20) . This suggests that, even if managerial experience in Japan is transferable across firms, such an appointment does not immediately imply high compensation and a high turnover rate. Accounting for the differences in the market for managers between the U.S. and Japan is beyond the scope of this paper. However, together with our evidence that experience gained as an employee is firm specific and is required to manage a newly merged firm, a plausible conjecture is that Japanese managers must conduct not only tasks that require managerial experiences, but also those that require the type of experience gained as an employee (21) , which make it more difficult to hire managers from outside the firm in Japan.

Finally, this is the first paper that examines the retention of managers after M&As using a Japanese dataset. The number of M&As in Japan has dramatically increased since the late 1990s. Although there are several attempts to understand Japanese M&A waves (e.g., Fukao et al. 2005), few papers investigate the separation of workers after M&As. Notable exceptions are Kubo (2004) and Kubo and Saito (2012), which analyze the effect of mergers on employment and wages. In particular, Kubo (2004) analyzes the personal characteristics of employees who separated from firms before and after mergers using firm personnel data. However, neither work discusses the retention of top managers. Although the impacts of mergers on employees are interesting in their own right, the reasons for the separation of managers from the boards of newly merged firms would differ from the reasons for the separation of employees. Hence, the evidence in our paper provides valuable new information to understand how Japanese firms adapt to merger waves.

This paper examines how the tenure of managers influences the retention rate of management groups after M&As in Japanese companies. It develops a general equilibrium model of managerial separation after M&As that distinguishes several hypotheses about the effect of tenure on separation, given several data limitations. Our empirical results show that acquiring firms obtain benefits from skills that are specific to the target firm and from skills that are specific to the new firm, which must be acquired by managers from the target firm following an M&A. We also show that experience as an employee in a target firm, prior to becoming a manager, increases valuable specific skills but at the expense of the accumulation of managers’ general human capital.

To confirm the external validity of the empirical results found in data-rich countries such as the U.S., it is important to analyze managerial human capital in multiple countries, including data-poor countries such as Japan. However, it is likely that the data availability would impose several limitations on such a study, as they have in our case. This paper provides useful methods to overcome these possible data limitations. In particular, we provide a novel method to correct for selection biases by utilizing the timing of selection in a selected sample, which does not require a random sample from the population. We hope that our approach can assist in accumulating empirical evidence in countries with limited data.

Of course, the development of the model is based on several assumptions. Hence, we do not claim to provide conclusive evidence on the retention rate of managers after M&As. However, because the importance of human capital in understanding the retention of managers cannot be denied, we believe that our results provide a reasonable explanation of the otherwise puzzling evidence on the retention rate of managers after M&As. Moreover, because our model is flexible and amendable, it can provide a sound basis for the development of a more complete theory of retention in the future.

Some research considers takeovers as a disciplinary device (e.g., Martin and McConnell, 1991). Alternatively, Shleifer and Summers (1988) argue that a takeover causes a breach of trust with stakeholders and transfers rent from them to shareholders. Jovanovic and Rousseau (2002) emphasize that a takeover can reallocate capital to better manage a firm. All of these theories presume that top managers in a target company must be replaced after a takeover. On the other hand, the synergy view of takeovers, which is supported by McGuckin and Nguyen (1995) and Matsusaka (1993), does not predict the replacement of top managers.

Matsusaka (1993) finds that the retention of managers in a firm targeted for takeover increases the bidder's return, and Cannella and Hambrick (1993) and Zollo and Singh (2004) find that the departure of executives from acquired firms is harmful to postacquisition performance.

Comparing U.S. CEOs and Japanese presidents, Kaplan (1994) argues that, because decisions in a Japanese firm are made on a consensus basis, it is important, for the sake of accurate comparison, to include other directors, not only presidents. Saito and Odagiri (2008) argue that, because there is heterogeneity among directors, not all directors are important decision makers and, therefore, they choose to focus on directors with titles as the important decision makers in Japanese firms. We follow Saito and Odagiri (2008) and identify directors with titles as the relevant executives in the sample target firms.

Walsh (1988), Walsh (1989), and Walsh and Ellwood (1991) investigate several factors that influence the turnover of top managers after M&As. More recently, Wulf (2004), Hartzell et al. (2004), and Bargeron et al. (2009) focus on the power of target CEOs to negotiate benefits, which includes a position in a new firm, as an expense borne by shareholders. Finally, Mateos de Cabo et al. (2014) investigate how individual characteristics, including gender or membership of a minority group, influence appointments to directorships after M&As.

Similar to our empirical strategy, Chetty (2009) and Heckman (2010) discuss the benefits of estimating wellfocused parameters rather than full structural parameters.

This intuition may not be true if the amount of total knowledge that must be learned is so little that a quick learner can immediately understand everything and if an acquiring firm can wait until a slow learner catches up. However, this case is less likely to be important for our empirical studies. First, the literature on the learning curve (e.g., Jovanovic and Nyarko, 1995) suggests that a rise in productivity continues for a long time, especially if tasks are complex, which is likely to be the case for management jobs. Second, as most firms are subject to seasonal events, it is less likely that every operation can be understood without spending at least one year in the firm. Therefore, we focus on one year as the period over which extensive learning occurs in our empirical study. Third, because, as Kaplan (1994) argues, the decisions in many Japanese firms (the focus of our empirical studies) are made on a consensus basis, it is important to learn what people think about a particular strategy. As suggested by the literature on higher-order beliefs, learning about the beliefs of other people on random objects is more difficult than learning about the random objects themselves (see Veldkamp, 2011). Hence, it is likely that a target-firm manager needs time to learn the consensus views held by the managers in the new company. Finally, there is no economic reason for an acquiring firm to keep a slow learner until they start to catch up.

Although we construct a model under a stationary environment in this paper, macroeconomic shocks can be easily incorporated by multiplying all variables by A(x), which denotes macroeconomic shocks in year x. Given this specification, we can show that the introduction of A(x) does not change the results at all.

Our human capital accumulation functions are linear if they do not change positions. Since a more general production function would greatly complicate our empirical predictions, we made the linear assumption in order to derive a meaningful interpretation from the empirical results. This assumption can be thought of as a linear approximation to the general human capital accumulation function.

Our human capital accumulation function is consistent with the following human capital accumulation function. For any year t

Other reasons given for delisting include “stock transfer”, “bankruptcy”, “insolvency”, “window-dressing settlement”, and “business suspension”. There was a single case of stock transfer in our sample, but we excluded it because the target firm was in the JASDAQ market.

We exclude financial institutions such as banks, stock companies, and insurance companies because of the difference in accounting systems.

Auditors are excluded.