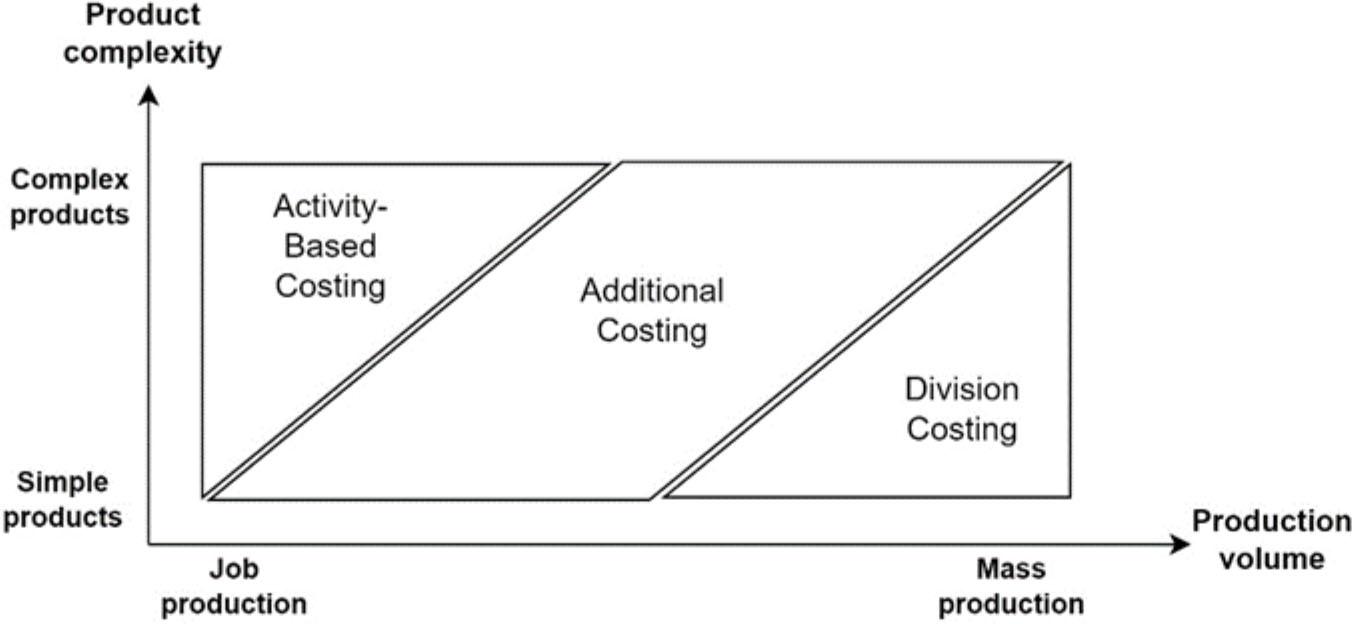

Figure 1.

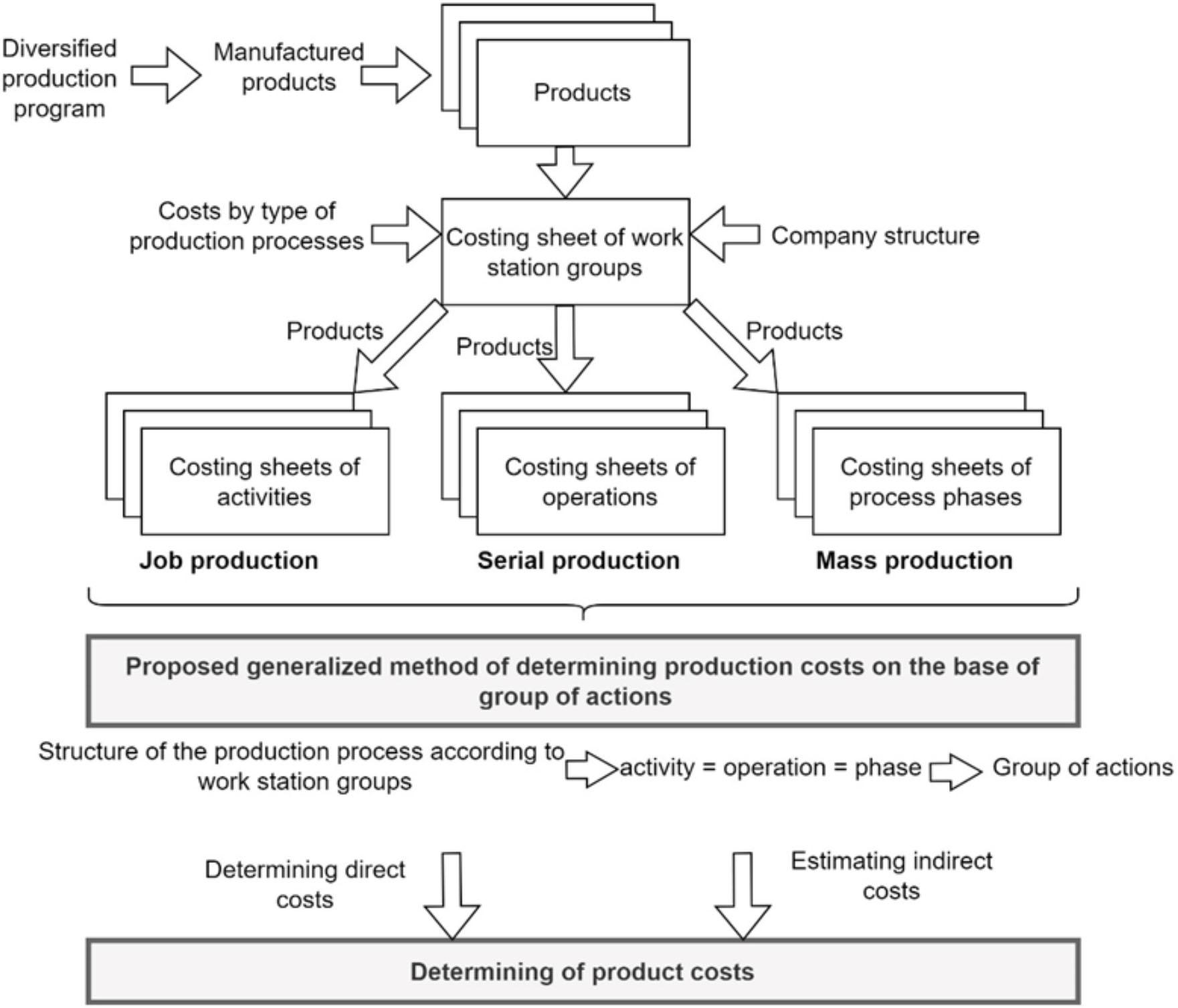

Figure 2.

Figure 3.

Figure 4.

Figure 5.

Figure 6.

Figure 7.

Figure 8.

Figure 9.

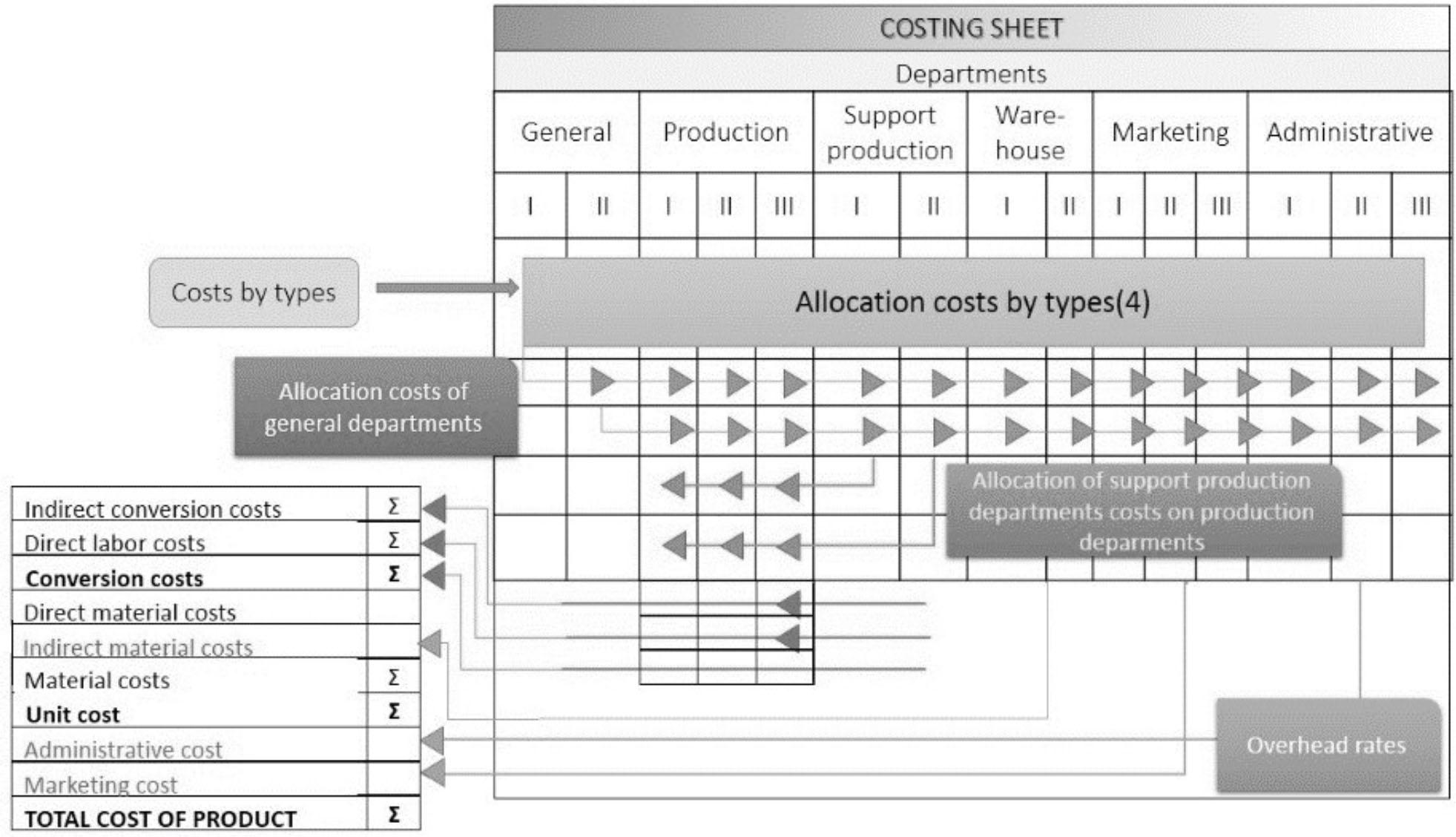

Company’s costing sheet (Source: Authors’ own research)

| Costs by types | Work stations of cutting tools production process | Work stations of sport equipment production process | Work stations of power tools production process | R&D department | Supply | Administration | Marketing and sales department |

|---|---|---|---|---|---|---|---|

| Indirect processing costs | 2.5 million PLN/year | 3.5 million PLN/year | 3.0 million PLN/year | 2.5 million PLN/year | 0.5 million PLN/year | 2.5 million PLN/year | 1.5 million PLN/year |

| Direct costs by types | 3.5 million PLN/year | 4.5 million PLN/year | 3.0 million PLN/year | 4.0 million PLN/year | 1.75 million PLN/year | 1.5 million PLN/year | 1.25 million PLN/year |

| The sum of costs by types (including direct labor costs) | 6.0 million PLN/year (1.6 million PLN/year) | 8 million PLN/year (2 million PLN/year) | 6.0 million PLN/year (1.4 million PLN/year) | 6.5 million PLN/year (1.5 million PLN/year) | 2.25 million PLN/year (0,5 million PLN/year) | 4.0 million PLN/year (1.8 million PLN/year) | 2.75 million PLN/year (1.2 million PLN/year) |

| Number of employees | 16 | 20 | 14 | 10 + 3 + 2 =15 | 5 | 18 | 12 |

| Total number of employees: | 100 | ||||||

| Total costs: | 35.5 million PLN/year | ||||||

Costing sheet of action groups (Source: Authors’ own research)

| Costs by types | Work stations of cutting tools production process | R&D department | Supply | Administration | Marketing and sales department | ||

|---|---|---|---|---|---|---|---|

| Cutting material, drilling holes | Welding, Visual control | Powder coating, quality control | |||||

| Indirect processing costs | 84 PLN | 420 PLN | 240 PLN | - | - | - | - |

| Work stations costs | 168 PLN | 700 PLN | 400 PLN | - | - | - | - |

| Labor intensity of rotor arm manufacture | 2.1 | 7 | 4 | 270 | 75 | - | - |

| The sum of labor intensity on work stations | 62 600 | 85 500 | 72 000 | 25 500 | 8 500 | - | - |

| Indirect costs by types | 2.5 million PLN/year | 3.5 million PLN/year | 3.0 million PLN/year | 2.5 million PLN/year | 0.5 million PLN/year | 2.5 million PLN/year | 1.5 million PLN/year |

| Indirect costs | 84.75 PLN | 288.25 PLN | 166.75 PLN | 24 500 PLN | 4 400 PLN | - | - |