The world faces growing challenges related to climate change and environmental protection (Atif et al., 2023). Greenhouse gas emissions have increased climate risks, leading to extreme weather, biodiversity loss, and environmental imbalance (Hu et al., 2025). Measures such as habitat conservation and pollution reduction are vital for addressing these impacts (Folqué et al., 2021; Kolawole & Iyiola, 2023). These challenges have changed the financial system. Now, investments must align with the Sustainable Development Goals and support responsible capital allocation (Beisenbina et al., 2023; Fiordelisi et al., 2023; Infante et al., 2024; Koellner et al., 2005).

Sustainable investment began with socially responsible investing (SRI), which grew in the 20th century, especially among religious and ethical groups (Escrig-Olmedo et al., 2017; Soler-Domínguez et al., 2021). The idea became prominent between 1970 and 1980 as Corporate Social Responsibility (CSR) gained attention (Avramov et al., 2022). This growth came from rising societal expectations, regulatory pressures, and greater awareness of the social and environmental effects of organizations (Betakova et al., 2023). Sustainable investment now encompasses strategies to integrate environmental, social, and governance (ESG) factors into decision-making (Avramov et al., 2022; Paulsy & Lal, 2025).

Kraussl et al. (2024) indicated that investor commitment to responsible investment has grown significantly during the last 15 years. The United Nations Principles for Responsible Investment (UN PRI) has catalyzed this change by increasing the number of responsible investment signatories and asset holders. This development has enhanced investors' interest in ESG investments (Folqué et al., 2021) and has significant valuation consequences, with risk premiums and term structures increasingly dependent on investor preferences (Kubalek & Kudej, 2025).

Pakistan is highly vulnerable to climate change, making sustainable investment crucial (GCF, 2023). Climate shocks hurt agriculture, stall economic growth, and raise financial risks, exacerbated by carbon-intensive funding (Farooq et al., 2023; Lamperti et al., 2021). Green investment is needed to boost financial, economic, and environmental sustainability in Pakistan (Hasan et al., 2022).

Most studies on sustainable investment focus on uniform preferences and assume all ESG investors share similar goals (Lim et al., 2025; Meng & Wang, 2020). Yet, in practice, investors have diverse preferences for ESG factors (Qasem et al., 2025). Some focus on specific dimensions (Kraussl et al., 2024). While moral and ethical factors are important for societal responsibility (Belás et al., 2020a), much of the literature addresses the Western context (Zvarikova et al., 2023; Belás et al., 2024b). Non-Western contexts are understudied (Bashir et al., 2025). Psychological and social influences on these preferences remain poorly studied (Paulsy & Lal, 2025), especially given that recent research has mainly used quantitative methods (Yucel et al., 2023; Gutsche et al., 2023; Paulsy & Lal, 2025).

VBN theory (Stern et al., 1999) provides a relevant framework to understand heterogeneous perceptions. By relating values, beliefs, and norms to pro-environmental behavior, the theory helps explain how self-enhancement and self-transcendent values shape sustainable investment decisions (Andersson et al., 2005; Jansson & Biel, 2014).

Based on the above context, this study addresses the following research question: RQ1: “What are the heterogeneous perceptions and drivers of individual investors regarding sustainable investment decisions?” By answering this question, the research highlights the variety of investor motivations and enables financial product strategies tailored to each investor's values.

Sustainable investment means investment practices that consider both financial returns and ESG factors (Cunha et al., 2020; Cubas-Díaz & Martinez Sedano, 2018; Elahi et al., 2023; Klumpes, 2024). Sustainable investment is linked to CSR and reflects calls for firms and investors to help achieve broader societal and environmental goals, not just profits (Carroll, 1999). The field grew due to awareness of long-term risks from environmental damage, social inequality, and weak governance (Hafenstein & Bassen, 2016; Carlsson Hauff & Nilsson, 2023). Thus, investors now assess how companies handle ESG risks and seek long-term profit while avoiding liabilities (Beckmann et al., 2014; Talan & Sharma, 2019). The degree of ESG integration still varies (Camilleri, 2021).

VBN Theory (Stern et al., 1999) helps explain the drivers of sustainable investment at the individual level. The theory holds that values shape environmental beliefs, which in turn create personal norms for pro-environmental acts (Whitley et al., 2018). Self-enhancement values, such as materialism, achievement, and power, focus on the self and may harm the environment. Self-transcendent values such as universalism and benevolence link to caring for others and the environment (Jansson & Biel, 2014). People with strong self-transcendent values feel a duty to oppose environmental harm (Kim & Hall, 2021; Perera, 2024; Whitley et al., 2018).

Cultural values influence both investment decisions and societal expectations. In societies with strong sustainability values, investors prefer companies that match these ideals (Delsen & Lehr, 2019). For example, Scandinavian investors support firms with fair labor and strong environmental practices (Gainulina & Setiawan, 2017). Across the globe, cultural values are shaping business conduct as investors seek firms that reflect social ethics (Fehrenbacher et al., 2018). Ethical values also drive sustainable investment by discouraging harm and prioritizing long-term social and environmental gains over short-term profit (Robin & Angelina, 2020).

Behavioral biases significantly impact sustainable investment decisions, often leading to suboptimal choices that fail to align with long-term sustainability goals. Shah & Hussain (2024) indicated that herding bias occurs when individuals react similarly to their peers, especially in complex or uncertain situations. In sustainable investing, herding bias can lead investors to follow the crowd, investing in popular sustainable funds or stocks without thoroughly evaluating their sustainability criteria. Robin & Angelina (2020) indicated that it can lead to the overvaluation of green investments, as they are widely endorsed rather than rigorously evaluated for their true social or environmental impact.

Status quo bias refers to the tendency to prefer the status quo rather than making changes that lead to better outcomes (Rehman et al., 2024). In sustainable investing, the bias often prevents investors from shifting away from traditional, less sustainable investments to green alternatives. The reluctance to change investment portfolios, even when provided with clear evidence of sustainable options, is hindered by comfort with familiar assets, which comfort-driven benefits hinder progress toward sustainable financial practices (Bednarz & Matasova, 2024; Korteling et al., 2023).

The study comprises two cases involving mutual fund investors and stock market investors. The research follows an interpretive approach and employs a multiple-case study design. Multiple cases are useful for comparing results across cases to study contemporary phenomena beyond the setting of a single case (Nguyen et al., 2023).

The study employs a multiple-case study design to evaluate modern phenomena in their actual life settings, using multiple evidence sources (Eisenhardt & Graebner, 2007). Krishnan et al. (2025), Kahraman and Kazancooglu (2019), Nguyen et al. (2023), and Reim, Sjodin, and Parida (2021) have used this approach in their research on sustainable and circular business models. The paper examines real-world sustainable investment decisions by modeling heterogeneous preferences and drivers across cases. Two scenarios are considered: mutual fund investors (Case A) and stock market investors (Case B). Although the focus on stock market investors is quite common (Chowdhury, Mahdzan, & Rahman, 2024; Ahmad & Wu, 2023), incorporating mutual fund investors has previously addressed a significant research gap.

Data was collected through face-to-face semi-structured interviews with eight respondents, comprising five mutual fund investors (Case A) and three stock market investors (Case B). The sample size is justified because qualitative research focuses on data saturation instead of the number of respondents (Creswell, 2013), which is also consistent with studies, e.g., Ahmad & Wu (2023) (five participants) and Chowdhury et al. (2022) (thirteen participants). Participants were recruited through personal contacts and LinkedIn, and interviews were conducted in three rounds until saturation was reached. The eligibility criteria included a bachelor's degree in business and an age of 24 or older. The interviews took 20–25 minutes, were conducted in English and Urdu, and were transcribed using Sonix and NVivo. The research was conducted in Pakistan (an emerging economy).

Interview details

| Participant | Age | Gender | Education | Investment Platform | Employment Status | Interview Duration |

|---|---|---|---|---|---|---|

| R1 | 24 | Male | BBA | Stock market | Account Payable Manager | 25 minutes |

| R2 | 25 | Male | BS (Business) | Mutual Funds (Bitcoins also) | Freelancer | 27 minutes |

| R3 | 28 | Male | MBA | Mutual Funds | Analyst | 23 minutes |

| R4 | 27 | Male | BBA | Stock market | Marketing Manager | 19 minutes |

| R5 | 28 | Male | BS (Finance) | Mutual Funds | Analyst | 24 minutes |

| R6 | 28 | Female | BBA | Mutual Funds | Small scale entrepreneur | 19 minutes |

| R7 | 24 | Female | BS | Mutual Fund | Student | 29 minutes |

| R8 | 27 | Male | BS | Stock market | Marketing Manager | 23 minutes |

The transcripts were analyzed using thematic analysis using NVivo. The study has adopted the approaches of Nguyen et al. (2023) and Santa-Maria, Vermeulen, and Baumgartner (2022), and has developed first-order categories from codes generated from quotes in transcripts using NVivo. These first-order categories were then analyzed for relationships, resulting in clustering into theoretically distinct groups, known as the second-order themes. Finally, aggregate themes or dimensions were identified.

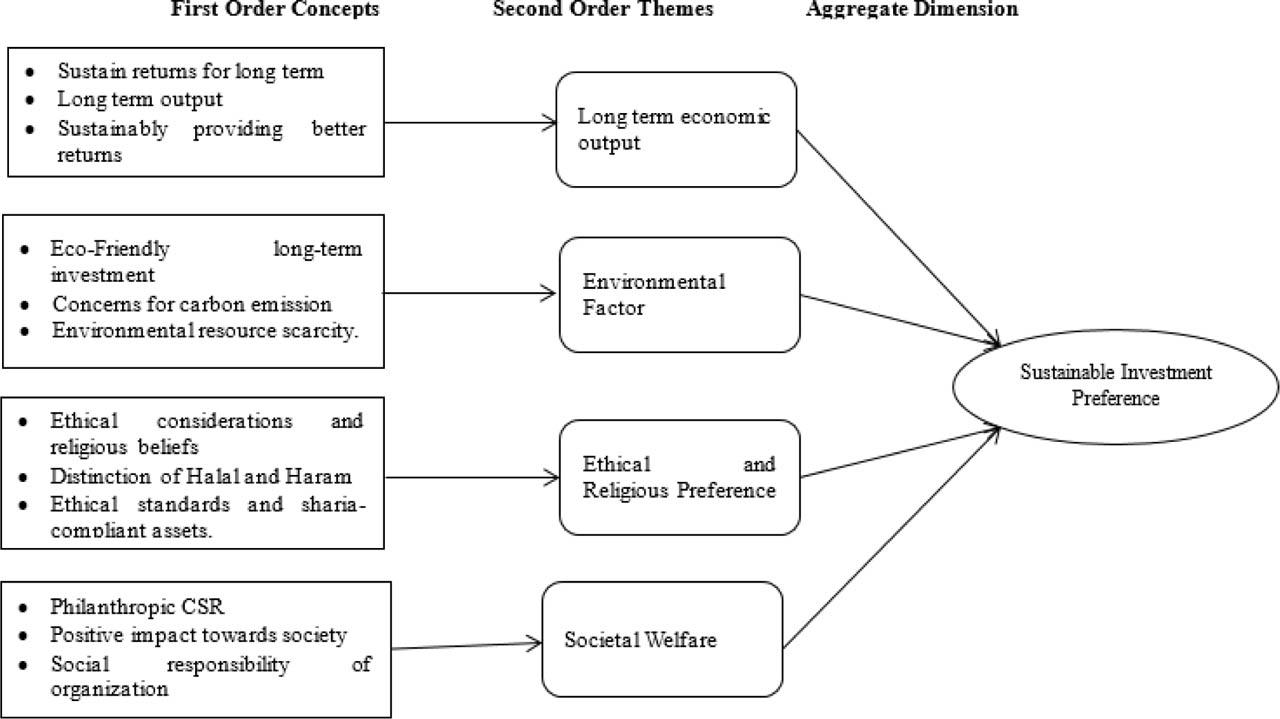

Figure 1 shows a word cloud that reflects the diverse perceptions and motivations that shape sustainable investment decisions among individual investors in emerging economies.

Word cloud

Respondents held various perceptions of sustainable investment, shaped by their awareness and definitions of sustainability. The four dimensions were long-term economic output, environmental factor, religious preferences, and societal welfare. Most respondents preferred maintaining long-term returns, indicating that long-term economic output is a sustainable investment. In this context, R1 indicated that;

“[………] My investment should sustain the returns for the long term. [……..] long term output is important to obtain sustainability […..]”.

R2 indicated that;

“[…] the investment that is sustainably providing me with better returns is what sustainability is.”

The second dimension was the environmental factor, indicating that the asset's environmental friendliness is an important sustainability aspect. They indicated that the organization where they invest must focus on environmentally friendly practices. R3 indicated that;

“[…] it is sustainable, such as in environmental concerns. It does not emit any carbon emissions. That is what I believe is sustainability investment.”

R6 indicated that;

“[….] Like, my investment does not have such practices that will be harmful for the environment or society and can impact the resource scarcity of the future.”

The third dimension was religious preferences, as respondents focused on their investment being ethical and aligned with their religious beliefs. Ethical and religious investments are part of socially responsible investment, as per Avramov et al., (2022). In this respect, R1 indicated that;

“The return on investment is one thing, but if it is a company that I consider is ethically wrong, I wouldn't invest, no matter how high the returns are. Ethical considerations and religious beliefs are very important in my investment choices.”

R4 indicated that;

“One of the most important factors for me, aside from returns, is whether the investment is sharia-compliant.”

Hence, religious factors are important for sustainable investment. Furthermore, the fourth factor was the societal welfare. Sustainable investment emerged through social responsibility, which is important for sustainability (Paulsy & Lal, 2025). The respondents indicated that CSR practices must have a positive impact on society. In this respect, R2 reflected that;

“Social factors are very important. It plays a significant role in my investment decisions. My investments should not harm society.”

R3 further emphasized that;

“[…..] But yes, I do have a say in the social aspect of companies that make good profits. But if it is not socially viable, I do not make my investment there otherwise.”

Hence, the social factors are significant for sustainable investment. However, it is not important for many investors as well, e.g., R1 indicated that;

“It's not a deal-breaker for me, but if a company is doing CSR, it's a good initiative. You never know, maybe a government program or scholarship might come your way in the future, and I'll be thankful for the company's CSR contributions.”

Hence, it indicated four dimensions shaping sustainable investment, including long-term economic output, environmental factors, religious preferences, and societal welfare. Investors prioritize long-term returns, with many focusing on environmental sustainability and ethical considerations, especially religious compliance. While social welfare is significant, it is not a primary factor. It indicates varying sustainability perceptions, where financial returns, ethical alignment, and social responsibility play significant roles. Figure 2 below shows the framework for their heterogeneous preferences.

Heterogeneous preferences for sustainable investment decisions

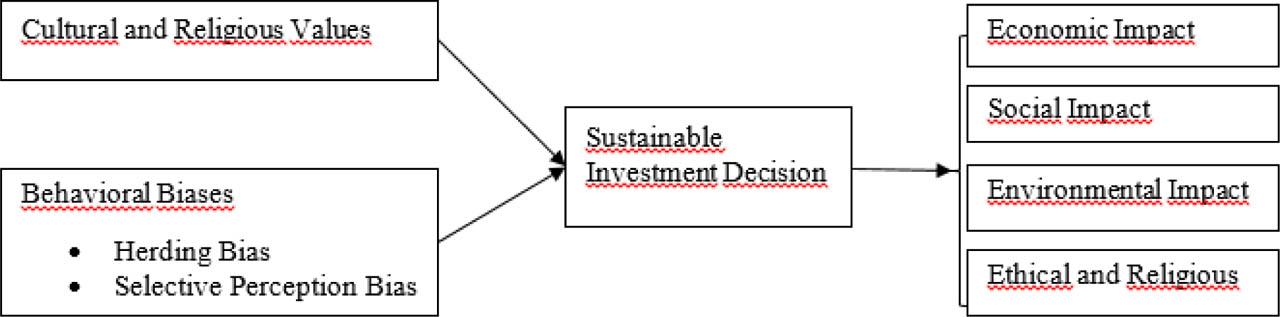

The research further evaluated the social and psychological drivers for sustainable investment decisions. The key drivers are cultural and religious values, herding bias, selective perception bias, and status quo bias. Cultural and religious values are important drivers. Gainulina and Setiawan (2017) indicated that culture and values are important for investment decisions. Individuals base their decisions on their cultural values, norms, and beliefs. It also aligns with VBN theory, indicating that self-transcendent values are an important aspect of decision-making (Whitley et al., 2018). A Respondent indicated that;

“If a company's values contradict my cultural beliefs, it would affect my decision-making. If it doesn't align with my values, it would affect my feelings towards the company.”

It indicates that cultural values and beliefs are important for sustainable investment decisions. Ethics is also a significant factor.

“I do care about ethics. I wouldn't invest in companies or sectors that go against my religious principles, such as those involved in alcohol, gambling, or things that are considered haram.”

In this regard, religious factors are also significant sustainable investment drivers. An Islamic country with a Muslim majority indicates religion as an important aspect, as these respondents avoid earnings considered Haram in their religion. In this regard, one respondent indicated that;

“[…..] I only invest in sharia-compliant assets. I avoid any industry that involves activities that are not permissible in Islam, such as alcohol or any such thing. I also avoid businesses that exploit workers or engage in unethical practices [.....] my focus is always on aligning my investments with my religious and ethical values.”

Furthermore, herding bias significantly drives sustainable investment decisions. Robin and Angelina (2020) found that herding behavior significantly influences investment decisions, as investors are influenced by their surroundings and peers. The respondent in this context reflected;

My peers' opinions are very important to me. I seek their guidance based on their experiences, and I share my opinions with them as well. So, in some ways, they can have an influence on my decision”.

However, not everyone is affected by peers, and some conduct their independent research as well. Respondent indicated that;

“[…..] When I'm making an investment decision, I mostly trust my own judgment and expertise, especially because I have a strong understanding of investment valuation. I believe in doing my own research and maintaining a good record of my investments.”

Furthermore, selective perception bias also affects sustainable investment decisions. Respondents do not prioritize environmental issues but consider them as linked to long-term benefits. The respondent indicated;

“[…..] when it comes to long-term investments, if I'm putting a portion of my money into long-term investments, like for 5 or 10 years, with the expectation that it will grow over time, the environmental factor also plays a role.”

Furthermore, status quo bias also impacts investment decision-making. Rehman et al. (2024) indicated that status quo bias refers to investors' preference for traditional investments over new alternatives. Respondents agree that they prefer traditional investments over new alternatives, as one respondent stated.

“I tend to stick with what I know. I've invested in mutual funds, and I'm comfortable with that approach because it provides me with a balanced risk and aligns with my long-term strategy.”

However, another respondent contends that they also consider new alternatives in their investment decision.

“I would explore new options. It's important to keep learning and stay updated. Even if it doesn't benefit you immediately, expanding your knowledge is valuable.”

The analysis indicates that cultural and religious beliefs strongly shape investment choices, with many prioritizing alignments with ethical and religious principles. Herding bias and selective perception bias elaborate on the impact of peer opinions and personal focus on long-term outcomes, respectively. Status quo bias indicates a preference for traditional investment approaches, though some investors are open to new alternatives.

The conceptual framework (Figure 4) has been developed from the above analysis.

Drivers of sustainable investment decision

Framework to evaluate sustainable investment decision

The study assesses the heterogeneous preferences and motivations that underline individual investors' decisions to invest sustainably in a developing economy. The results indicate that four prevailing dimensions influence sustainable investment decisions: long-term economic output, environmental factors, religious orientations, and societal welfare. The salience of long-term economic output is consistent with the previous research that financial performance is a fundamental determinant of investment choices, even in the context of sustainability (Beckmann et al., 2014; Kraussl et al., 2024). This finding is closely related to those in Central Europe, particularly in Slovenia, where energy efficiency is ranked second after price in property-related investments (Lakić et al., 2020). Just like the Slovenian homeowners and homebuyers, investors in the current study are more likely to focus on sustainability because it is closely associated with long-term economic gains, which supports the claim that financial rationality and sustainability are not necessarily mutually exclusive.

Another important dimension that can be identified is environmental consideration, yet its significance seems relative rather than absolute. In the current study, environmental factors become more salient when they lead to long-term economic consequences, suggesting a strong selective perception bias. This observation is partly at odds with results from Slovenia, where environmental and energy-efficiency characteristics are highly valued even beyond direct financial benefits, especially among environmentally conscious people and women (Lakić et al., 2020). The divergence implies that although Central European investors and consumers are highly inclined to incorporate environmental values as a separate decision criterion, investors in the developing world might continue to conceptualize environmental sustainability in an economic context. This disparity could be due to differences in institutional trust, income stability, and market maturity across Central European and developing-economy settings.

An especially relevant dimension that makes this research different from Central European literature is the presence of ethical and religious orientations. The high-ethical-and-religious investors in this study prefer investments grounded in moral and religious values. Such an observation is in line with the Value-Belief-Norm (VBN) theory, which posits that self-transcendent values trigger personal norms that direct prosocial and pro-environmental behavior (Stern et al., 1999; Jansson & Biel, 2014). Ethical considerations can also be observed in Central Europe, but in a more generalized form, in terms of CSR and ESG awareness, rather than in the form of religious motivations. For example, a Czech study on Millennials' awareness of CSR and socially responsible investment found that 57 percent of respondents are willing to forgo a portion of their financial gains to invest in socially responsible instruments (Formánkova et al., 2019). Although the two settings emphasize ethics-based investment conduct, the current study builds on this body of literature by showing that religious values, which are mostly absent or underemphasized in Central European studies, are determinants of sustainable investment decisions in non-Western and developing-economy contexts.

The fourth important preference dimension is societal welfare, which strengthens the increasing appreciation of the social aspect of ESG. This observation aligns with results from Slovakia and other EU member countries, where young consumers and investors consider socially responsible corporate practices a competitive edge and are willing to patronize responsible companies despite paying a premium (Blahušiaková, 2025). Nonetheless, although Central European literature tends to focus on societal welfare through institutionalized CSR reporting mechanisms and regulatory innovations such as the Non-Financial Reporting Directive and the Corporate Sustainability Reporting Directive, the current study postulates that considerations of societal welfare among individual investors are less regulation-based and more value- and norm-based. This comparison highlights the effects of institutional maturity to determine the avenues through which social responsibility affects investment behavior.

The cultural and religious values are revealed as major motivators of sustainable investment decision-making, advancing the previous literature, which is predominantly Western and Central European in its settings, where secularization tends to diminish the importance of religion (Belás et al., 2020a; Dubcová et al., 2025). The prominence of religion underscores the situational specificity of ESG motivations and suggests that Western-designed ESG frameworks may not align fully with investors' interests in emerging markets. Also, behavioral biases, including herding, selective perception, and status quo bias, are present, which supports the behavioral finance knowledge (Robin & Angelina, 2020; Rehman et al., 2024). Value-based sustainability narratives seem more successful than normative strategies in developing economies.

This study contributes by incorporating ethical, religious, and cultural factors into sustainable investment decisions, recognizing that investors make decisions shaped by diverse values, beliefs, and motivations. It is consistent with the VBN theory as it demonstrates the role of self-enhancement and self-transcendent values in environmental decision-making. It also highlights cultural norms and societal values that promote socially responsible investment behavior.

Fund managers must be aware of the increasing demand for sustainable portfolios that reflect investors' ethical, religious, and cultural interests and devise strategies that support long-term returns. The study focuses on integrating four sustainability dimensions into investment decision-making to align with investor values and financial objectives. Policymakers must promote sustainability through clear reporting policies and incentives. Also, financial and educational institutions should collaborate to sensitize people to sustainable investing by educating, using the media, and leveraging community programs to promote responsible investment and sustainable development.

The research has various limitations as well. The sample of participants is not very diverse in terms of age and background. Future research must involve more diverse groups to capture a broader range of sustainable investment preferences. Second, sustainable investment literacy was not investigated in the study, influencing investors' preferences and their behavior. Future research should evaluate the influence of literacy on decision-making. Lastly, credibility, transparency, and greenwashing in sustainable investment portfolios were not discussed and warrant further research. This research mainly focused on the Global South Asian context (Pakistan). Future scholars may explore Central European regions to understand ESG from the Global North region.