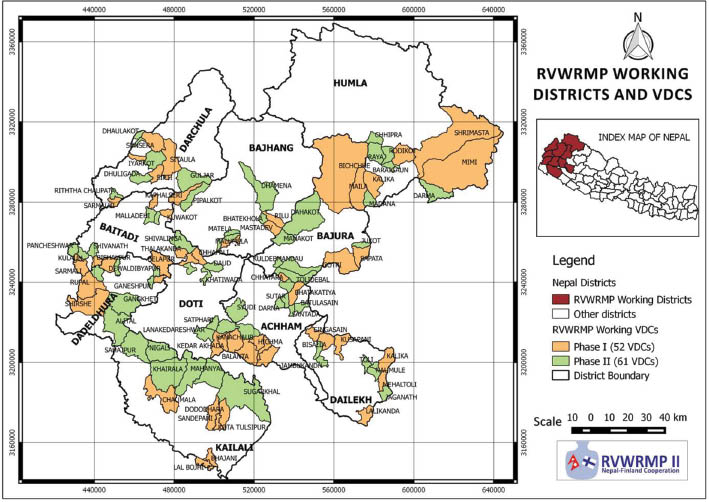

Figure 1

Map of Nepal and the project districts. (Provided with the permission of RVWRMP).

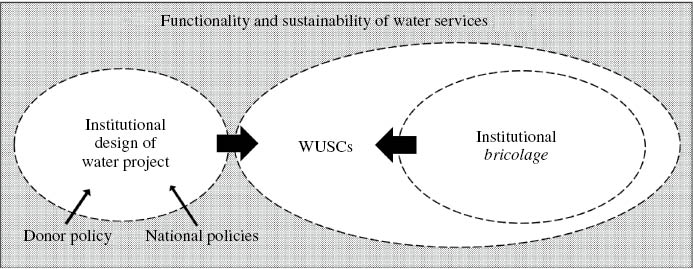

Figure 2

Analytical framework.

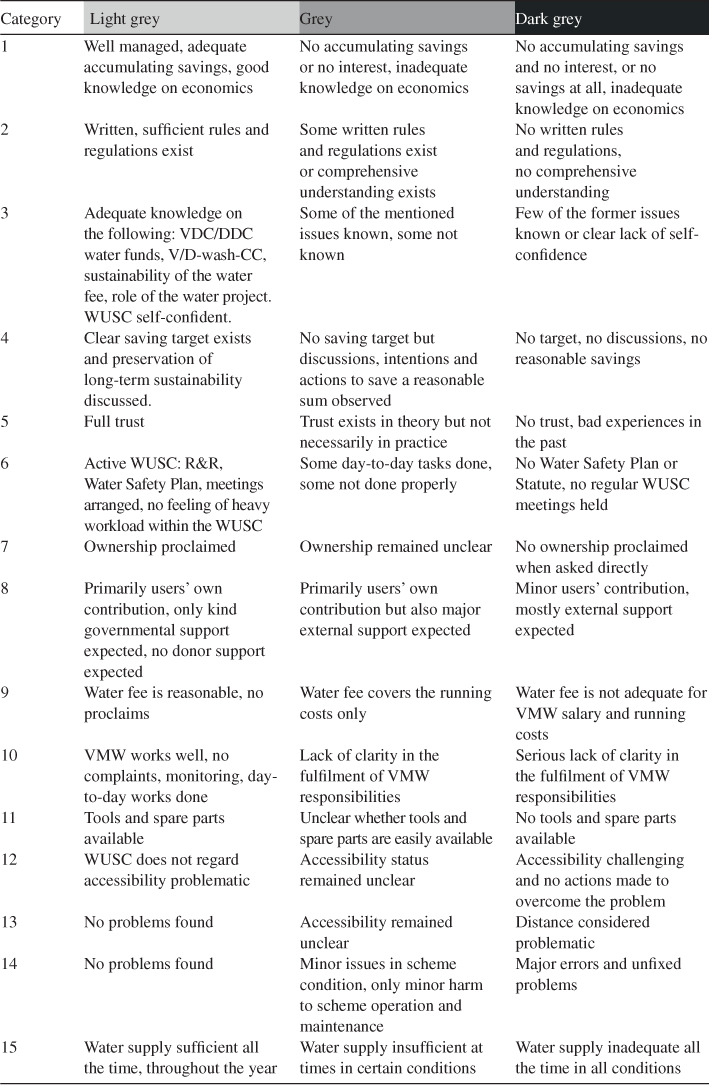

Table 1:

Implementation of institutional design principles within project operations.

| Design principle | Implementation in practices of WUSCs | Difficulties sometimes encountered |

|---|---|---|

| 1. Well-defined boundaries | Institutional: WUSC responsible for managing the infrastructure Users/beneficiaries: Water fee payers Physical: Scheme infrastructure and immediate watershed above the water source Users groups operational and legal boundaries defined in the local self-governance act | Sometimes, due to water scarcity, water is taken from a neighbouring Village Development Committee (VDC) – this carries some risk for continuing supply |

| 2. Match between appropriation and provision rules and local customs | WUSC Statute: defined rules, regulations, shared costs

WUSC registration under Water Act: establishing rights to water and responsibilities (water source). Women's meeting held to decide tap locations. | Potential conflict as traditionally community members consider water to be free. Risk of elites taking water for production and depriving some households |

| 3. Collective-choice arrangements | Election of WUSC members from the water users; familiarity and continuous interactions between water users and WUSC members; transparency principle in operation and maintenance and management | Risks of elite capture, exclusion of disadvantaged groups/women |

| 4. Monitoring | Participatory systematic monitoring embedded into the Step-By-Step approach. Public hearings and mass meetings are an aspect of the monitoring practice stipulated in the project guidelines. Transparency and accountability principles of the project. Operational scheme monitoring: VMW Responsibility: WUSC | Requires initial facilitation by project and regular collection of adequate water tariff to pay VMW. Water tariff set often too low to pay for continuing maintenance |

| 5. Graduated sanctions | WUSC Statute: rules and regulations Follow-up with sanctions by WUSC | Sometimes not written down. Sanctions may not be well understood or may be applied unfairly. |

| 6. Conflict-resolution | WUSC Statute, Water Safety Plan Public audits and public hearings, transparency, accountability as established during the planning and implementation phase through Step-by-Step approach | Requires initial support from project. Risk of corruption leading to conflict. |

| 7. Recognition of rights | Legal status (Local Self Governance Act 2055; 2068; Water Act) | Registration must be renewed |

| 8. Nested enterprises | Supportive roles of VDCs, V-WASH-CCs, DDCs, District WASH Coordination Committees and line agencies. | Sometimes limited support available (e.g. VDC Secretaries overloaded) |

Note: Village Development Committees (VDCs) constitute the lowest tier of the governance hierarchy. District Development Committees (DDCs) are the second lowest tier of the governance, comprised of multiple VDCs. The project works with VDC-wide Village Water, Sanitation, and Hygiene Coordination Committees (V-WASH-CC). The VDC WASH Coordination Committees (V-WASH-CCs) in the RVWRMP area cover all water resources management issues, livelihoods and micro-finance. The establishment and role of V-WASH-CCs is defined in the Nepal National Sanitation and Hygiene Master Plan (GoN 2010). The role of District WASH Coordination Committees D-WASH-CCs corresponds at District level with the role of V-WASH-CCs. VMW; village maintenance worker is a trained person, responsible for day-to-day maintenance of a water scheme.

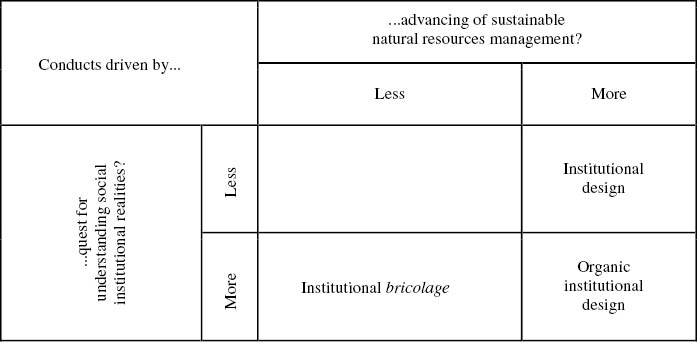

Figure 3

Linking institutional design and bricolage.

Table A:

Characteristics of scrutinised WUSCs.

| Scheme number | Interviewees | Water tariff | Collected water tariff, total | VMW salary | Regularly deposited savings | Savings, total | Source-wise saving/credit interest rates | Average distance to village market | Distance from village market to district HQ | Date of interview | District | Scheme age in years | Number of households | Estimated population | Number of water supply taps |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| I | Chair, treasurer, 1 beneficiary | 20 NPR/hh/m | 180 NPR/m | 90 NPR/m | 10 NPR/hh/m | Bank: NPR 5000, coop.: NPR 7000 | Coop.: 10%, bank: 0% | 1 h | 0.5 h | 8.3.2014 | Dadeldhura | 1.5 | 9 | 60 | 2 |

| II | Chair, secretary, 2MCs | 50 NPR/hh/m | 1500 NPR/m | 1000 NPR/m | 200 NPR/m | NPR 5000 | 0% | 15 min | 0.5 h | 8.3.2014 | Dadeldhura | 1.5 | 30 | 150 | 8 |

| III | 3 MCs | 20 NPR/hh/m | 1440 NPR/m | 1080 NPR/m | 360 NPR/m | NPR about 3000 | 0% | 1 h | 0.5 h | 8.3.2014 | Dadeldhura | 0.5 | 72 | 420 | 6 |

| IV | Chair | 60 NPR/tap/m | 600 NPR/m | 500 NPR/m | 100 NPR/m | NPR 25,000 | – | 0–1 h | 1 h | 24.2.2014 | Dadeldhura | 6 | 29 | 170 | 10 |

| V | Chair, secretary, treasurer, 2MCs, 10 beneficiaries | 80 NPR/tap/m | 1680 NPR/m | 1680 NPR/m | 0 NPR/m | Bank: NPR 5000, coop.: NPR 15,500 | Coop.: 10%, bank: 0% | 0–1 h | 1 h | 26.2.2014 | Dadeldhura | 6 | 163 | 980 | 25 |

| VI | Chair, 1 MC, about 20 beneficiaries | 75 NPR/tap/m | 375 NPR/m | 500 NPR/m (paid mostly in kind) | 0 NPR/m | NPR 5000 | 0% | 3–5 h | 1 h | 25.2.2014 | Dadeldhura | 6 | 17 | 100 | 5 |

| VII | Chair, secretary, treasurer, 8 MCs | 50 NPR/hh/m | 5150 NPR/m | Planned salary in kind | 50 NPR/hh/m | NPR 16,00 | 0% | 5 h | 3–4 h | 2.3.2014 | Bajura | 0 (implementation phase) | 103 | 560 | 16 |

| VIII | Chair, secretary, treasurer, 3 beneficiaries | To be decided | To be decided | To be decided | Planned 20 NPR/hh/m to a coop. | NPR 42,000 | 0% | 3–4 h | 3–4 h | 2.3.2014 | Bajura | 0 (implementation phase) | 64 | 335 | 21 |

| IX | Chair, secretary, 1 beneficiary | 5 NPR/hh/m | 430 NPR/m | 160 kg/a cereals | 430 NPR/m | NPR 25,000 | Micro-loans: 24% | 3–4 h | 3–4 h | 2.3.2014 | Bajura | 2 (rehabilitation project) | 86 | 500 | 17 |

| X | VMW, vice chair, 1 beneficiary | 20 NPR/hh/m | 800 NPR/m | 200 kg/a cereals | 800 NPR/m | NPR 24,000 of which NPR 20,000 invested as micro-loans | Bank: 0%, micro-loans: 12% | 3–4 h | 3–4 h | 3.3.2014 | Bajura | 3 | 40 | 300 | 13 |

| XI | Chair, secretary | 0 NPR/hh/m | 0 NPR/m | No full-time VMW, tax 250 NPR/d | 3900 NPR/m general, 780 NPR/m water | NPR 54,000 in bank, NPR 10,000 in coop., NPR 39,000 loans | Bank: 0%, coop.: 10%, micro-loans: 24% | 3–4 h | 3–4 h | 3.3.2014 | Bajura | 1 | 156 | 880 | 30 |

| XII | Chair, 5 beneficiaries | 20 NPR/hh/m | 470 NPR/m | Planned 10 NPR/hh/m | 470 NPR/m | NPR 27,000 | 0% (cash savings, no bank account) | 3 h | 1 d | 11.3.2014 | Achham | 0 (just completed) | 47 | 139 | 10 |

| XIII | Chair, VMW | 50 NPR/hh/m | 1100 NPR/m | 20 kg/a cereals | 1100 NPR/m | NPR 7000 cash, NPR 5000 in bank | micro-loans: 24%, bank: 0% | 3 h | 1 d | 11.3.2014 | Achham | 4 | 22 | 130 | 5 |

| XIV | VMW | 10 NPR/hh/m | 220 NPR/m | 300 kg/a cereals | 0 NPR/m | NPR 5000 in bank | – | 1 h | 1 d | 12.3.2014 | Achham | 4 | 22 | 130 | 7 |

| XV | Chair, treasurer | 20 NPR/hh/m | 440 NPR/m | 440 NPR/m | 0 NPR/m | NPR 5000 in bank | 3–4% | 1 h | 1 d | 13.3.2014 | Achham | 0.75 | 22 | 144 | 4 |

| XVI | Treasurer, 1 beneficiary | 5 NPR/hh/m+ 4 kg/a cereals | 105 NPR/m+84 kg/a cereals | 84 kg/a cereals | 105 NPR/a invested as micro-loans | Exact sum not known | Bank: 3-5%, micro-loans: 0%, planned 12%. | 1 h | 1 d | 13.3.2014 | Achham | 2 | 21 | 93 | 5 |

| XVII | Chair | 10 NPR/hh/m+4 kg/hh/a cereals | 470 NPR/m | 188 kg/a cereals | 470 NPR/m | NPR 39,000 in bank | 0% | 3 h | 1 d | 14.3.2014 | Achham | 1 | 47 | 250 | 13 |

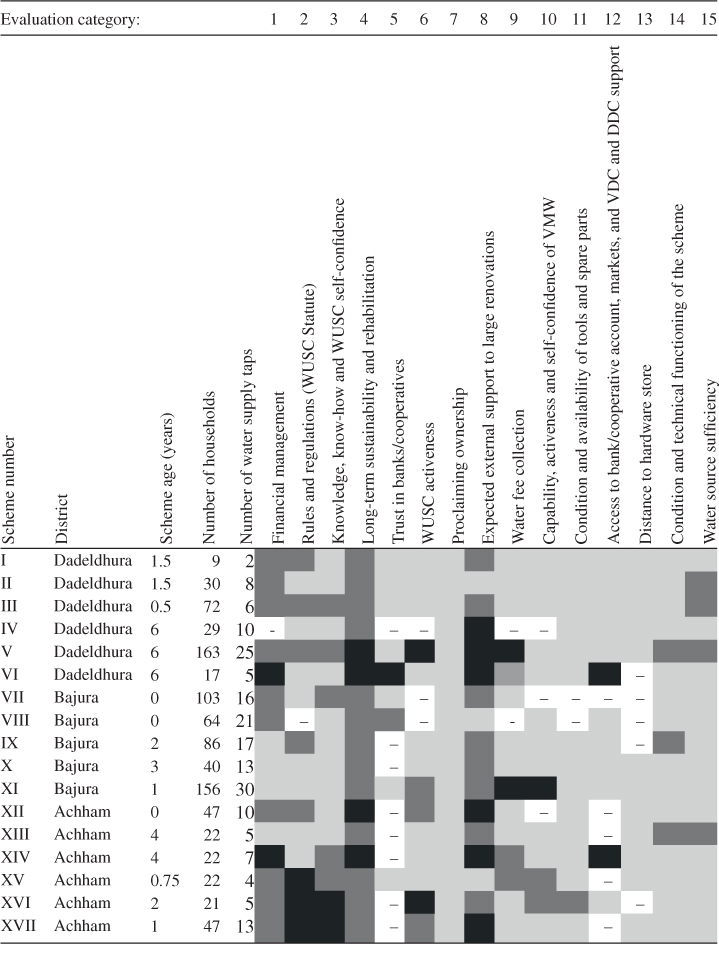

Table B:

Status of scrutinized WUSCs.

|

Coding: lighter colour indicates better performance in accordance with the institutional design of the project. White boxes with a dash indicate categories which remained undiscussed in the interviews. More specific details on the schemes (I–XVII) are presented in Table A. Specific evaluation criteria to each evaluation category (1–15) are presented in Table C.