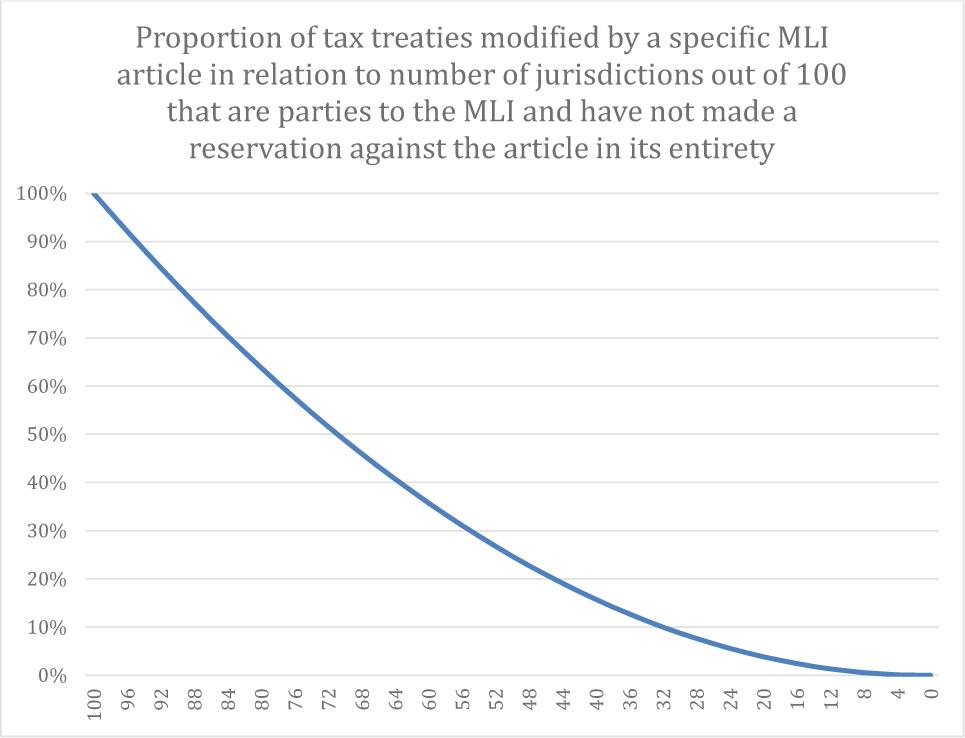

Figure 1

Reservations against articles in their entirety made by signatory states representing the world’s 20 largest economies

| State/Article | 3 | 4 | 5 | 8 | 9 With regard to Art. 9, a reservation against Art. 9(1) without opting in to Art. 9(4) has been deemed a reservation against the article in its entirety, as it would mean that the article is not given any effect. | 10 | 11 | 12 | 13 | 14 |

|---|---|---|---|---|---|---|---|---|---|---|

| China | R | - | - | - | - | R | - | R | R | R |

| Japan | - | - | - | R | - | - | R | - | - | R |

| Germany | R | R | - | - | - | - | R | R | - | R |

| United Kingdom | - | - | - | R | R | R | - | R | - | R |

| France | R | R | R | - | - | R | R | - | - | - |

| India | R | - | R | - | - | - | - | - | - | - |

| Italy | R | R | - Italy has not chosen to apply any of the options under Art. 5 but accepts that the other contracting state changes its method for elimination of double taxation and, therefore, does not make a reservation. | R | - | R | R | R | - | R |

| Canada | R | R | R | R | R | R | R | R | R | R |

| South Korea | R | R | R | R | R | R | R | R | R | R |

| Russia | - | - | R | - | - | - | - | - | - | - |

| Spain | - | R | - | - | - | - | R | - | - | R |

| Australia | - | - | - | - | - | R | - | R | - | - |

| Mexico | - | - | - | - | - | - | - | - | - | R |

| Indonesia | R | - | R | - | - | R | - | - | - | - |

| Turkey | - | R | R | R | - | R | R | - | - | R |

| Netherlands | - | - | - | - | - | - | R | - | - | - |

| Switzerland | R | R | - | R | R | R | R | R | R | R |

| Number of reservations | 9 | 8 | 7 | 7 | 4 | 10 | 10 | 8 | 4 | 11 |